K - Kellogg: Buy The Drop On This Moat-Worthy Brand

Summary

- Kellogg has a very strong portfolio of well-recognized brands and generates solid profitability.

- Its business has been rather resilient, and could see a return to meaningful growth after supply disruptions are worked out.

- I also highlight the dividend, balance sheet, valuation, and other important points.

Consumer staples stocks are one of the best places to shelter capital in times of inflation and economic uncertainty, yet the market has demonstrated time and again that it's not rational, with a number of these stocks trading materially down from highs last year.

Such I find the case to be with Kellogg ( K ), which has durable, well-recognized brands and whose stock has dropped materially from a near term high of $74 in December to $67 at present. In this article, I highlight the attributes that make Kellogg a solid buy for potentially strong long-term returns.

{kind=link}

Why Kellogg?

While most recognize Kellogg for its iconic breakfast cereal brands, such as Corn Flakes it also has consumer favorite snack brands such as Cheez-It, Pringles, Pop-Tarts, Eggo, Rice Krispies Treats, and newer brands such as RXBAR. The company was founded over a century ago with the introduction of Corn Flakes as its first product, and today, its products are available worldwide, generating $14.9 billion in total sales over the trailing 12 months.

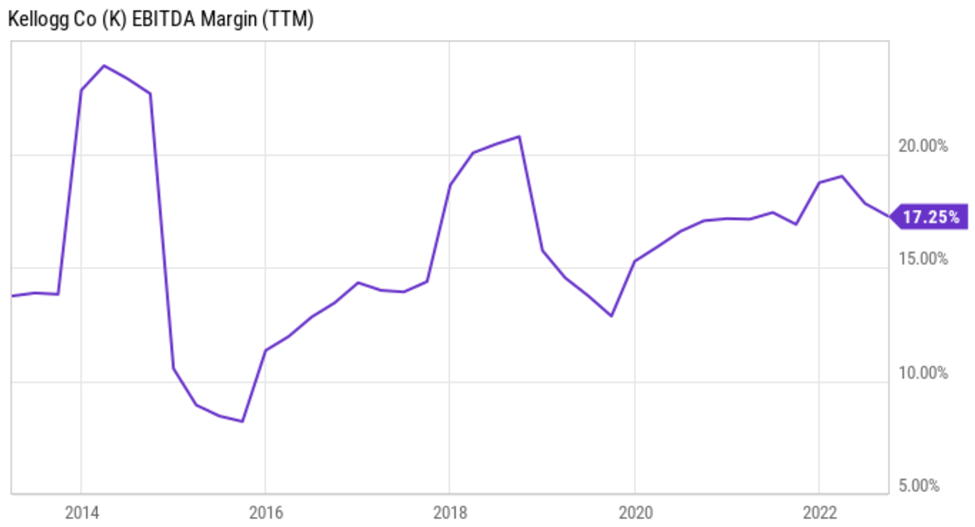

Cost inflation has been a key concern for consumer staples companies over the past year, and Kellogg is no different. However, management has done an overall good job of maintaining healthy margins over this timeframe, through productivity initiatives and strategic price increases. As shown below, Kellogg's EBITDA margin has seen an overall upward trend over the trailing 3 year period.

Kellogg EBITDA Margin (YCharts)

{kind=link}

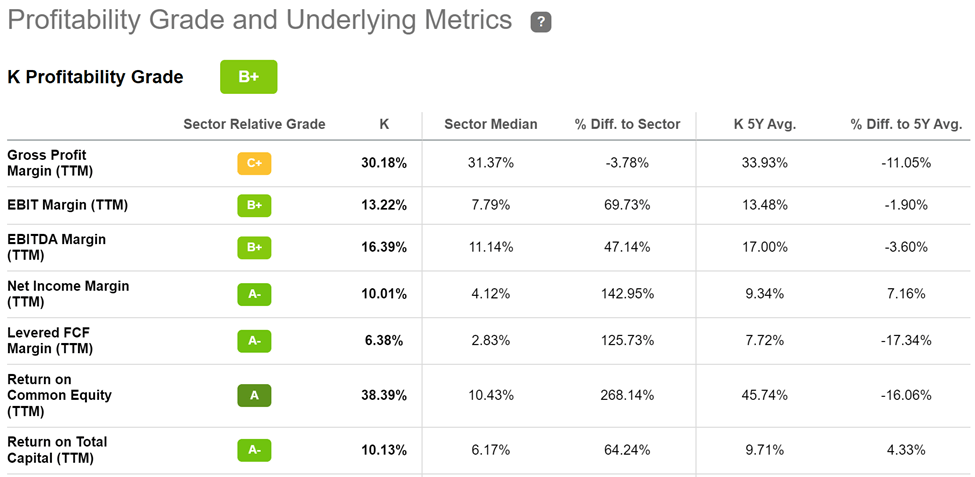

Importantly, this has helped Kellogg to earn a B+ Profitability rating relative to the Consumer Staples sector. Through effective cost management Kellogg generates a healthy Net Income margin of 10%, which is well in excess of the 4% sector median, as shown below.

Kellogg Profitability (Seeking Alpha)

{kind=link}

Meanwhile, Kellogg has demonstrated resilience amidst an inflationary backdrop, with total sales growing by 9% YoY (13% on an organic basis) during the third quarter. This was driven by momentum around Kellogg's snacks, noodles, and cereal businesses, which more than offset impacts to volume due to price increases, halted shipments to Russia, and adverse currency translation (due to a strong dollar). It's worth noting that operating expenses also grew, by Kellogg was still able to seek out 3.7% adjusted operating profit growth on a currency neutral basis.

Looking ahead, it appears that that market is not taking into consideration a potential rebound in Kellogg's other breakfast foods segment, MorningStar Farms, as it was severely impacted by supply disruptions last year. Management sees this as being a temporary issue with potential for improvement this year, as exemplified by their Sausage Links category growing by double digits in the last reported quarter.

Moreover, it appears that Kellogg has more ways to create value rather than just price increases. This includes cost savings potential as well as ROI potential on product innovation. This was highlighted by Morningstar in its recent analyst report :

We don't surmise that price hikes are Kellogg's only mechanism through which to lessen the profit hit. Rather, we continue to anticipate the pursuit of cost saves and price/pack management will remain key facets of the equation. Encouragingly, even in the face of these challenges, management's rhetoric suggests brand support hasn't faltered; our forecast calls for Kellogg to expend 7% of sales ($1.2 billion) on research, development, and marketing in the aggregate annually the next decade, which we view as prudent against the intense competitive landscape.

Meanwhile, Kellogg carries a strong BBB rated balance sheet with $375 million cash and short-term investments and a net debt to EBITDA ratio of 2.9x. It currently yields a respectable 3.5% and the dividend is well-protected by a 57% payout ratio and come with 18 consecutive years of growth. Kellogg hasn't been a high dividend grower in recent years, including just a $0.01 bump in the last dividend raise. However, I would expect to see more meaningful raises down the line, as it works out near term issues around the supply chain and disruptive cost inflation.

Admittedly, Kellogg stock isn't particularly cheap at the current price of $67 a forward PE of 16.3, sitting slightly below its normal PE of 17. However, patient investors should be rewarded over time, as the stock could return to 5% to 10% annual EPS growth in the coming years. Morningstar has an $82 fair value estimate and analysts have an average price target of $73.53, which translates to a potential 12.5% total return potential in the near term.

Investor Takeaway

In summary, while Kellogg faces near term headwinds, its strong balance sheet, profitability metrics, and resilient top line growth should allow it to weather the storm. It also has potential for growth with product innovation and cost savings initiatives. Though the stock isn't particularly cheap, patient investors could be rewarded over time as Kellogg works out near term issues around its supply chain, while getting paid to wait with a well-protected dividend.

For further details see:

Kellogg: Buy The Drop On This Moat-Worthy Brand