K - Kellogg: Decent Results And Cheap Valuation

2023-08-23 10:49:33 ET

Summary

- Kellogg's Q2 results were decent; although revenue slightly missed analysts' expectations, there was still an increase in net sales reported year-over-year, with adjusted EPS growing as well.

- The plans to split into two companies, Kellanova and WK Kellogg, remain on track with some guidance on what expectations are for each entity in terms of sales and EBITDA.

- The consumer staples food companies have been under pressure in terms of share price performance, and that includes K, which is presenting an attractive valuation to consider a position.

Written by Nick Ackerman.

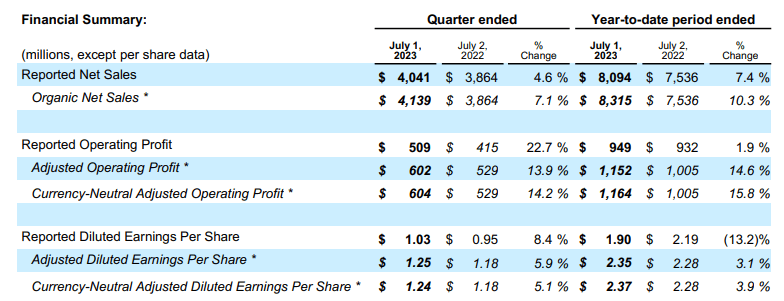

Kellogg ( K ) posted their Q2 results that topped EPS estimates but missed slightly on revenue. Still, revenue grew by around 4.6% year-over-year, even with such a slight miss. For adjusted EPS, it was good for an increase of 5.9% year-over-year.

We received another dividend increase since our last update as well. Kellogg's has a long history of consistent annual dividend increases, so this was mostly expected.

Additionally, the company's plans to split into two companies remain on course. We now know the names of these companies as well. Kellanova will be the growth tilted company with snacks and emerging market exposure. WK Kellogg will be the North American cereal business. There is expected to be some growth, but it should be fairly stable. It could also be a candidate for a takeover, as we discussed previously.

With all this being said, despite the decent results for this dividend grower, shares have been trending lower. It hasn't just been K, though, as other consumer packaged food companies have similarly faced downward pressure on their share prices.

Results And Forward Outlook

The latest results showed that K was able to pass on higher costs to consumers at 14.7% price increases. That being said, volumes did decline fairly meaningfully by 7.6%. The volume fell only around 4.8% in the first half, so the second quarter saw an acceleration in volume declines. Notably, in the earnings call , they anticipate improving volumes going forward.

I would say, on a go-forward basis, we're more optimistic and more constructive about our volumes. So I don't see – I don’t see this volume continuing this level. I see sequential improvement, and we do see, as we'll talk about next week in great detail exactly what that looks like as we return to a more balanced equation of volume versus price, but there's no question, this has been an unprecedented time in this industry with the type of pricing that's been necessary to take because of the input cost inflation.

As inflation has been raging on, this balance between prices and volume has been an important component of food companies. Diluted EPS increased 8% YoY for the latest quarter, and adjusted EPS was up nearly 6% YoY.

The first half year-over-year comparison shows that higher margins and strong growth in the snacks business have contributed positively. Adjusted gross margins came in at 33.7% compared to 32.4% in the prior year.

Despite these positive contributions, diluted EPS still saw a sizeable decrease though adjusted EPS saw a small increase. Adjusted EPS excludes mark-to-market and one-time charges.

{kind=link}

K Financial Summary (Kellogg)

They mentioned that this decrease was primarily driven by "unfavorable mark-to-market impact and adverse foreign currency translations."

However, the other factor was the costs associated with the company separation coming up. The one-time charges of the spin-off here are quite substantial, too, as reflected by the chart provided in their earnings presentation for the hit on cash flows.

K Cash Flow (Kellogg)

That has ultimately been the largest driver of their earnings hit this year, as separation costs have now resulted in a $0.37 per share hit in the first half.

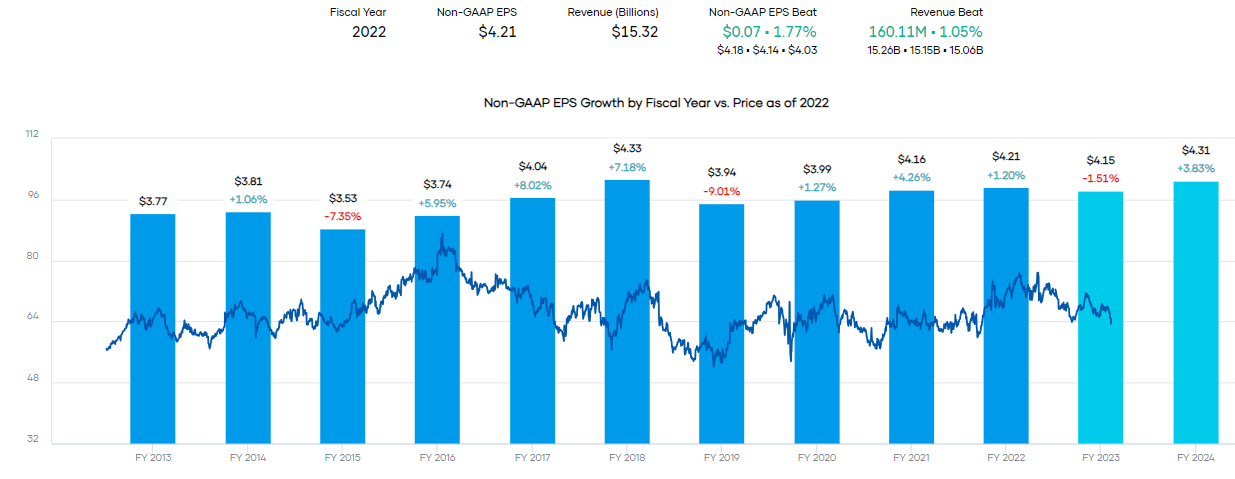

The overall growth in terms of earnings for K hasn't been particularly exciting. While there is a general trend higher over the years, the current estimates are for this year to show a slight decline. This would then be followed by earnings in 2026 that wouldn't even top the 2018 EPS figure. So it's definitely not the most exciting, but boring food consumer staples can still provide decent returns via their dividends and buying when they are cheap.

{kind=link}

K EPS History (Portfolio Insight)

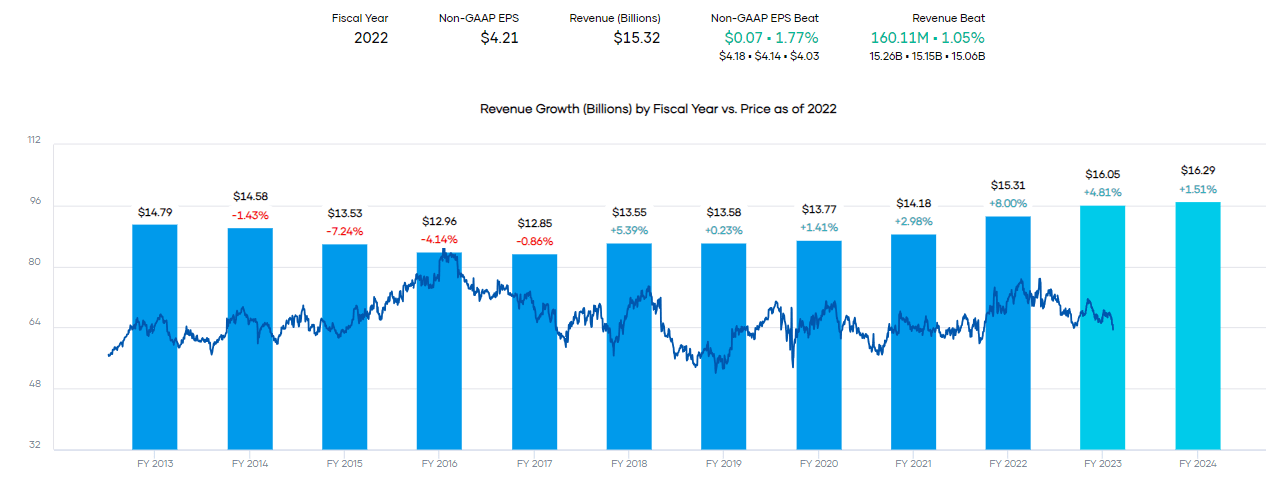

The trend in revenue has been a bit more stable in terms of generally growing in a more consistent, albeit slow manner.

{kind=link}

K Revenue History (Portfolio Insight)

An Update On The Spin-Off

They recently also provided an update on their own growth projections in terms of net sales and adjusted EBITDA for each company that is split. The spin-off is expected to be completed in the fourth quarter of this year.

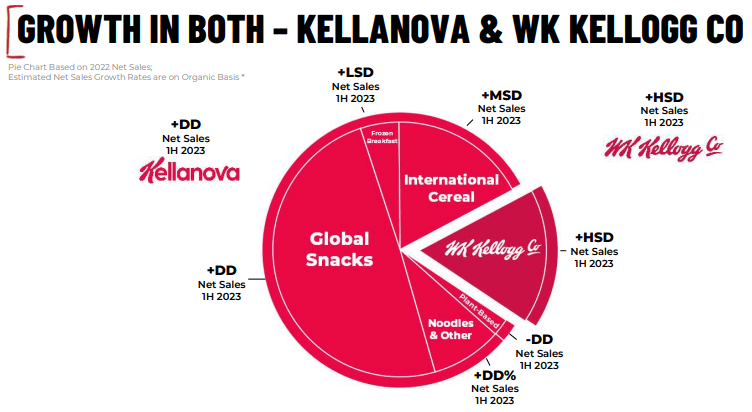

Kellanova is looking at net sales of around $13.5 billion and adjusted EBITDA of $2.275 billion, as well as delivering 7 to 9% in EPS growth. This really highlights how much the North American cereal business seems to be dragging on the overall operations as growth is anticipated to pick up on the new standalone, mostly snacks business.

{kind=link}

K Segment Performance (Kellogg)

Although Kellanova will also still contain the plant-based frozen food segment, which has now begun shrinking. When the company originally announced its plans to split, it had the plant-based foods business going to be spun out into its own operations. However, due to the shrinking demand and along with that much lower valuation in the plant-based space, it didn't make sense anymore. Fortunately, this is only a small part of the overall pie for the company.

WK Kellogg is looking to hit net sales of $2.7 billion with an adjusted EBITDA of $260 million. While they don't provide an earnings projection, they do anticipate they can increase EBITDA margins "through supply chain modernization and a stable top-line trajectory."

Now, if you're a dividend investor like me, then news on the dividend is also going to be important.

Kellanova is going to target a dividend payout of 50% , but due to the EPS growth of 7 to 9%, it could be quite a quick grower in time. The combined company has an EPS payout ratio of around 58% currently.

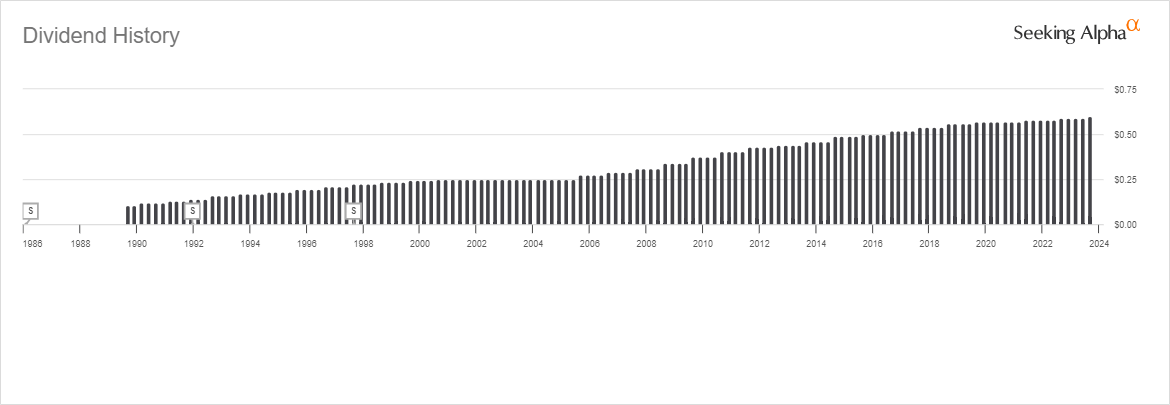

The combined company has provided consistency in terms of dividend growth, but the 10-year CAGR comes in at ~3%. So the pace of increases might not change in the near term until they hit their target payout, then could trend similar to EPS growth going forward.

{kind=link}

K Dividend History (Seeking Alpha)

With WK Kellogg, it looks like they are actually targeting a bit less of a payout at around 45% . Along with that, they mentioned "attractive dividend" repeatedly in the investor day presentation. Then providing "increasing cash returned to shareowners as cash flows improve."

I would have originally thought that this segment would have a higher payout ratio to compensate for what is likely going to be a lack of growth. That said, leaving more financial flexibility can set up the company in a better position having additional cash for growth opportunities. Additionally, this appears to be a business that is being spun out due to it being relatively unattractive with difficulty growing. That could see a rather low share price, and ultimately a higher yield could develop on its own.

Conclusion

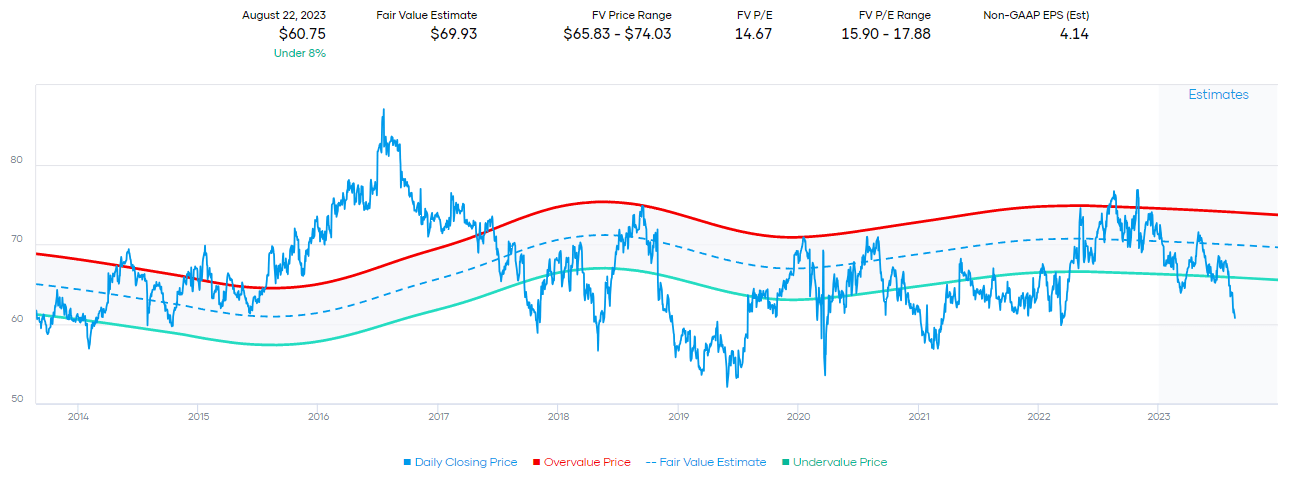

Shares of K have been selling off, and that has pushed it to an attractive valuation. The company is currently trading below its fair value range based on historical P/E.

{kind=link}

K Fair Value Estimate (Portfolio Insight)

Analysts also have an average price target for K of $72.56.

However, this company is about to be shaken up when the split happens. Generally speaking, the faster-growing Kellanova should be able to trade at a higher multiple while WK Kellogg is looking forward to potential margin expansions - with speculation for being potentially acquired.

Both are expected to pay a dividend going forward, but the payout ratio targets are lower than what the company pays now. That could see the slow growth in dividends remain until they get the payout in line with their target.

For further details see:

Kellogg: Decent Results And Cheap Valuation