K - Kellogg: Spinoff Benefits Don't Yield A Clear Picture

Summary

- Kellogg Company's revenue remain strong at currently highest level in its history, but so does its costs that rose along with it.

- Its pursuit of snacks seems to make sense, but emerging market expansion may not help its margin as much.

- Labor side of the equation for the spinoff should be factored into the management's consideration.

Investment Thesis

Company Overview

Kellogg Company (K), founded in 1906 and incorporated in Delaware in 1922, is an American snack and convenience foods company with manufacturing facilities in 21 countries and sales in more than 180 countries. The company's products are snacks, convenience foods, and frozen, protein-based food.

Strength

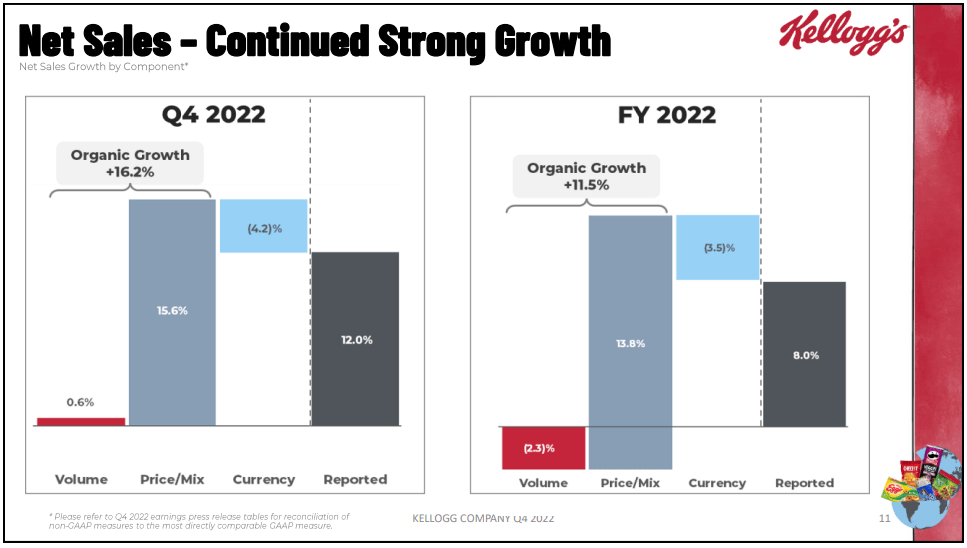

First, we want to lay out the current positive momentum in Kellogg. Kellogg's latest quarter results show continued strong sales growth.

Kellogg Net Sales (Company Q4 Presentation)

{kind=link}

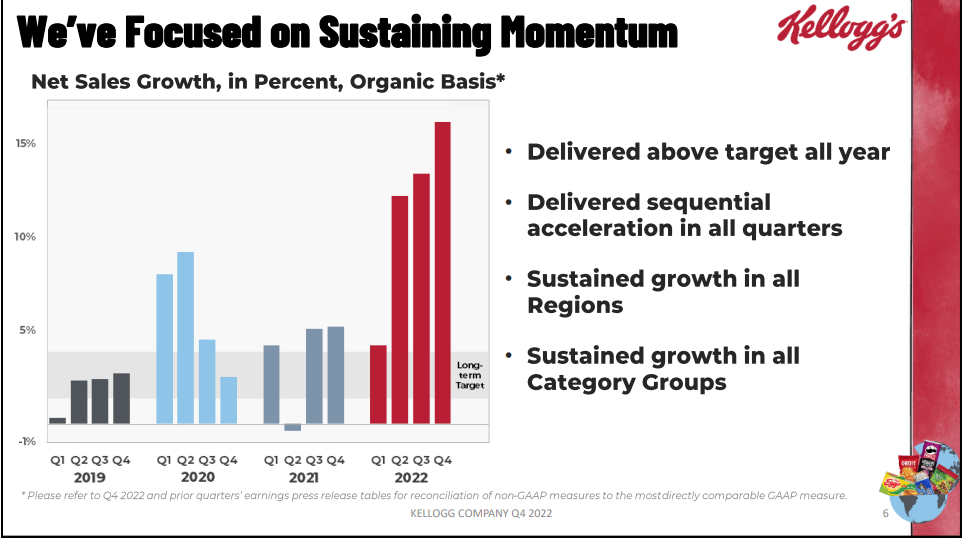

This is in addition to its full-year growth momentum in 2022.

Kellogg Sales Growth (Company Q4 Presentation)

{kind=link}

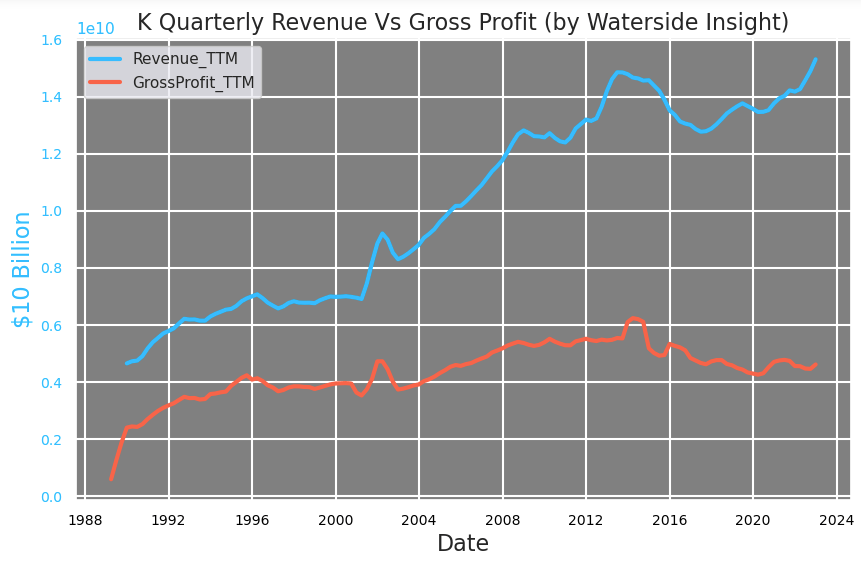

Historically, its revenue is almost at an all-time high, exceeding the previous high in 2013. And its gross profit had recovered to higher than when the pandemic started.

k (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

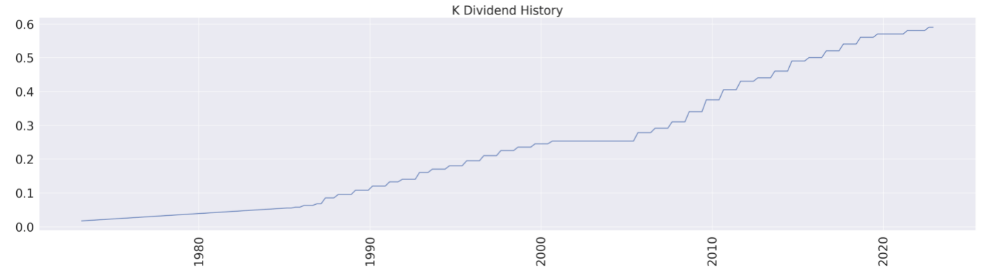

As a consumer staple, Kellogg has been raising dividends throughout the course of the last 17 years.

Kellogg Dividend History (Charted by Waterside Insight with data from the company)

{kind=link}

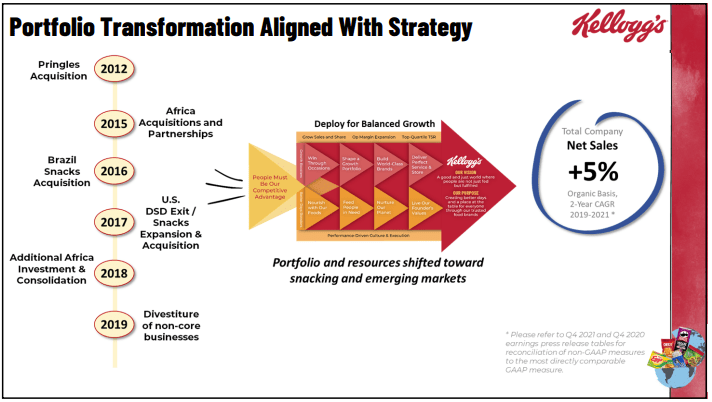

With this strong top line growth as a backdrop, we want to focus on its portfolio restructuring in motion. Kellogg's three business segments are all made up of well-known everyday brands, in which the snacks segment is the largest, followed by the cereal business, and then frozen plant-based segment.

Kellogg Global Portfolio (Company Portfolio Transition Announce June 2022)

The company announced a plan to separate these segments into three companies in June last year. They would be "Global Snacking Co.," "North America Cereal Co.," and "Plant Co." In that plan, it will also pursue a sale of the frozen, plant-based business. Although the latest change announced last month was to cancel the sale of the frozen unit as the company believes there is more growth ahead. This still is an ambitious plan that will fundamentally change the company. And this plan seems to be primarily due to its change of business strategy. The company wants to direct its focus on pursuing growth in snacking and emerging markets.

Kellogg Portfolio Transition Strategy (Company Portfolio Transition Announce June 2022)

{kind=link}

To understand this, we take a look at the growth by segment. By net sales % YoY change, the frozen and plant-based foods segment has been declining. Its cereal segment's growth experienced some volatility, with a sharp decline in 2021, and a rebound in 2022. The only segment that has a steady and continuous growth rate is snacks.

Kellogg Net Sale Change % (Calculated and Charted by Waterside Insight with data from the company)

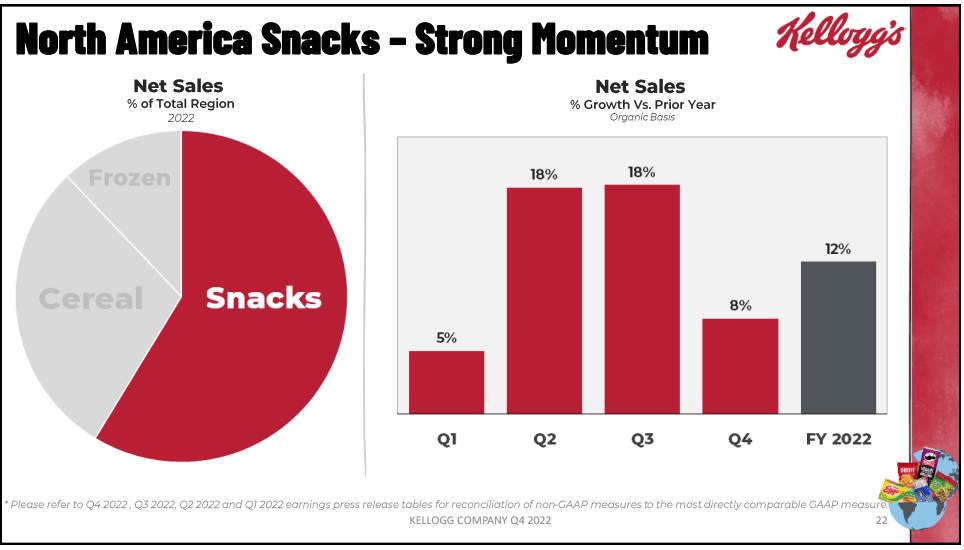

In fact, last year's growth momentum of its North America Snacks segment was singled out by Kellogg in its presentation, which recorded two-quarter of double-digit growth amid a rising inflation environment.

Kellogg North America Snacks Segment (Company Q4 Presentation)

{kind=link}

Its CEO K)%20will%20separate%20into,its%20net%20sales%20in%202021." > explains the rationale for this splitting is to help each business realize its distinctive potential and have better resource utilization for each of them. We calculate the earnings-to-sale ratio for each segment, and we see that its largest segment, snacks, also has the highest profit margin at 17.54%, while cereal trails far behind at 10.42%. And the plant-based segment, although it also has a high margin of 14.71%, is quite small in size. So, combining this ratio with their various net sales growth rate, perhaps the spinoff could make more focused improvement in each of them.

Kellogg EBITDA-to-Sales Ratio (Calculated and Charted by Waterside Insight with data from the company)

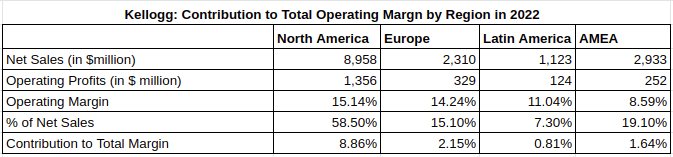

On the other hand, Kellogg's business has significant international exposure. In 2022, its sales outside of North America accounted for 41.5% of the total, while North America 58.5% in 2022. This reflects both the declining sales growth in North America and higher growth internationally.

Kellogg Net Sales by Region (Calculated and Charted by Waterside Insight with data from the company)

As we have calculated, in 2022, its international sales only contributed 5% of the total operating margin of 14%, while North America contributed 9%. Indeed, the international market's sales have been growing faster than the North American region, but in the new plan, Kellogg will need to generate almost double the margin of its international business, with a much more fragmented and diversified customer base and manufacturing setup. That means the company will need to either almost double its sales without raising costs or cut the cost by half from emerging markets to make this plan worthwhile. Will that be easier to achieve than perhaps boosting the North American region's already higher margin? What we meant here is that simply chasing marginal sales growth may not improve its margin. We don't see a decisive advantage here in its plan.

Kellogg Contribution to Total Operating Margin by Region (Calculated by Waterside Insight with data from the company)

{kind=link}

Weakness/Risks

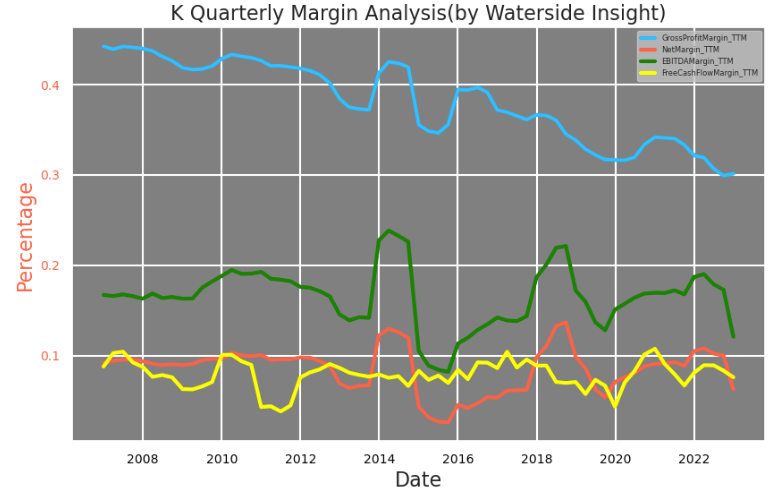

What's really dragging the company is its declining margin. Kellogg's gross profit margin is at its lowest since before the last recession, while all other margins have turned lower in 2022. Although its earnings beat expectations in the latest quarter, its growth of it is not keeping up with the revenue growth. As we can see, the decline in the ratios indicates that the costs and expenses side is growing too fast. Even the fast growth of revenue could not compensate for them.

Kellogg Margin Analysis (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

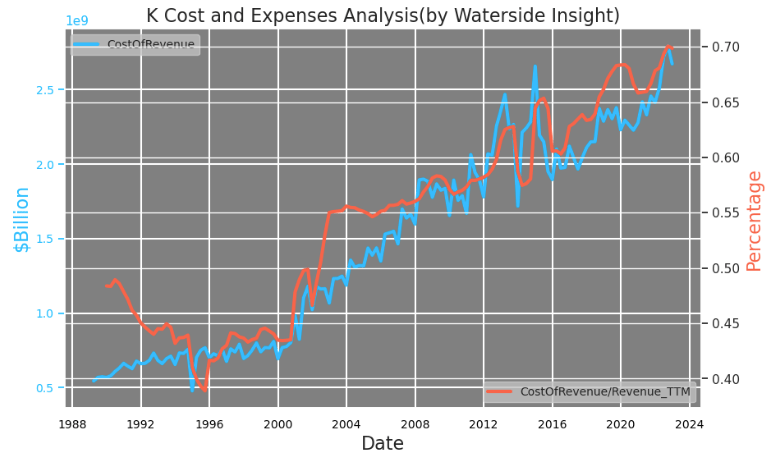

Its CEO mentioned "cost" seven times last September during his conversation with the Barclays Consumer Staples Conference host. From the chart below, we can see that its cost of revenue not only rose to its highest in absolute terms, but also in comparison to its revenue in relative terms. It now stands at almost 70% of its revenue. Increasing its profit with a sticky high cost of goods will be tough.

Kellogg Cost of Revenue (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

The company cited bottlenecks and shortages from the supply chain to be the problems. Also, it had a fire and strike in 2021. These could all be the reasons. However, commodity prices, such as for corn or other raw materials, could also be coming down if Fed succeeds in its mission to cut down inflation.

Its CEO mentioned that the shortage problem could go away after some time, but the most sticky part of the cost is the wage that, once it was raised, will not come back down again. We could be wrong, but an important part of restructuring the company is restructuring its personnel and employees as well. The company could be laying off its workers without actually laying off them, as some employees may not go along with the new changes and leave. So the wage can be renegotiated for the new company.

But it could be a wrong bet to count on improving the margin, as the company could also lose the most productive employee as well. Other than this, we don't see how spinning off could fundamentally help alleviate or change the cost and improve the margin. As the data suggested, increasing sales also increases the cost at a similar rate. The company needs to dig deeper into why its costs have risen so fast and so high while figuring out how to solve the problem effectively.

Also, getting back to its dividend payout. Last time it took a pause after raising the dividend for about 15 consecutive years. Maybe it's time for Kellogg Company to take another pause and re-deploy the cash to bring down the costs and expenses.

Financial Overview

Kellogg Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

{kind=link}

Conclusion

Without a clear picture of how the company plans to restructure its units, it is hard to look ahead and assess Kellogg Company's price fairly. Our analysis suggests that the spinoff doesn't yield a decisive advantage for its emerging market business, but it could make sense segment-wise to help boost each one of them to become more profitable. But if this strategy only focuses on increasing the top-line sales, then it will not address the fundamental drawback to its margin, which is an ever-growing cost basis. While on the other hand, the spinoff would cause messiness in its personnel profile and company synergy, which is hard to quantify and assess. We lean more towards doubts than benefits at this juncture and recommend a hold for Kellogg Company.

For further details see:

Kellogg: Spinoff Benefits Don't Yield A Clear Picture