K - Kellogg: The Business Is In A Secular Decline

2023-07-13 18:12:56 ET

Summary

- Kellogg's revenue shows almost no growth and profitability metrics are declining due to changing consumer demands for healthier food, suggesting the company may be in the final stages of its lifecycle.

- The company's financial performance over the past decade has been weak, with a significant decrease in levered free cash flow and a shrinking gross margin indicating weak pricing power.

- Despite a history of dividend growth, the current valuation of the stock seems unattractive, leading to a "Hold" rating for the company.

Investment thesis

Kellogg Company ( K ) has a vibrant history tracing the beginning of the twentieth century. According to my analysis, the business is highly likely to be in the latest stages of its lifecycle. Revenue demonstrates almost no growth and profitability metrics are shrinking due to weak pricing power amid changing consumers' demands for healthier food. The valuation also does not look attractive, according to my analysis. Therefore, I assign K a "Hold" rating.

Company information

Kellogg is a leading global breakfast cereal manufacturer and a significant producer of snacks and convenience foods. Kellogg sells its products worldwide and has multiple manufacturing and warehousing facilities across the globe. The company owns a diverse portfolio of well-known brands.

Kellogg

Kellogg shares are a component of the S&P 500. The company's fiscal year ends on December 31. Kellogg disaggregates its sales by geographic areas: North America, Europe, Latin America, and AMEA [Asia Middle East Africa]. More than 40% of revenue in FY 2022 was generated outside North America.

Financials

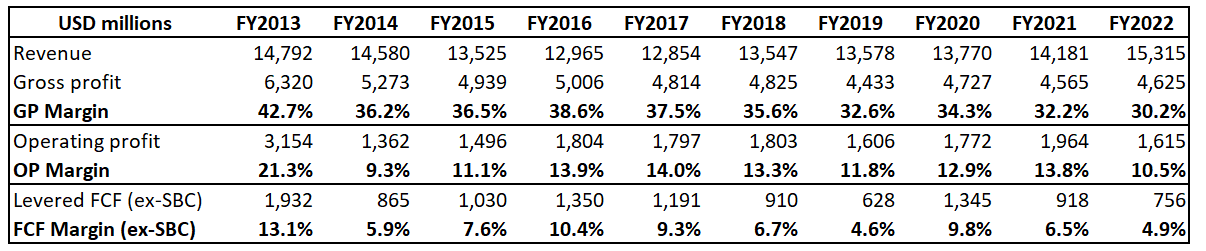

Kellogg's financial performance over the past decade definitely cannot be called strong. The top line almost did not grow, and profitability metrics shrank substantially. The gross margin deteriorated from about 43% to 30%, and the operating margin more than halved. The worst part is that the levered free cash flow [FCF] suffered the most with an almost three-fold decrease.

{kind=link}

The management took action to improve the SG&A to revenue ratio. Still, it was insufficient to offset the decrease in the gross margin due to inflationary pressure on the cost of revenue. The shrinking gross margin suggests the weak pricing power of the company.

The business is relatively capital intensive with between $500 and $600 million invested in CAPEX each year to sustain its revenue level. It represents a significant portion [about a quarter] of the company's cash flows from operations. That said, to drive revenue growth the company has few options but to increase prices or acquire new brands. A stable CAPEX over the past decades suggests that notable organic growth is not planned.

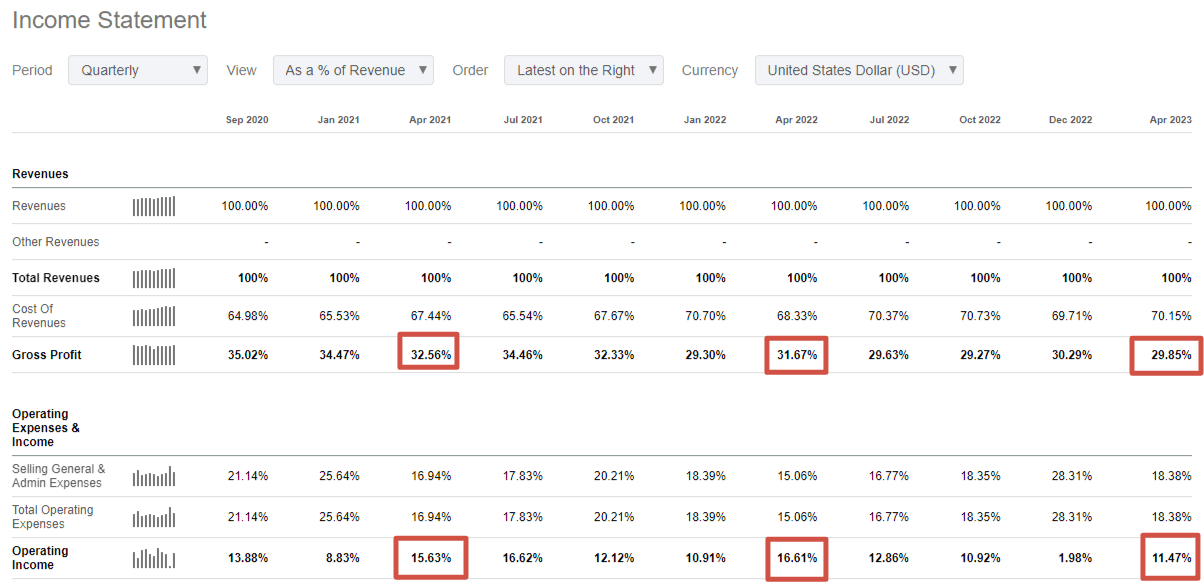

Now let me narrow down my financial analysis to the quarterly level. The latest quarterly earnings were announced on May 4 , with a slight beat of consensus estimates.

Seeking Alpha

Revenue grew about 10% YoY, and the adjusted EPS was flat compared to last year's quarter. The gross and operating margins demonstrated a YoY decline again, which is a bearish sign for me.

{kind=link}

According to the consensus forecast , revenue growth momentum is expected to decelerate substantially in the upcoming quarter with about 5% revenue growth. Profitability is also poised to suffer again, with an adjusted EPS projected to decline from $1.18 to $1.10. The upcoming quarterly earnings are expected to be announced on August 3.

The company's balance sheet also demonstrates some red flags for me. First, Kellogg is in a substantial net debt position about ten times higher than the company's FY2022 levered FCF ex-SBC. Liquidity ratios also look weak to me.

Seeking Alpha

Overall, the company's financial performance and its financial position look below average, in my opinion. Now let us move forward to the "Valuation" section of my analysis.

Valuation

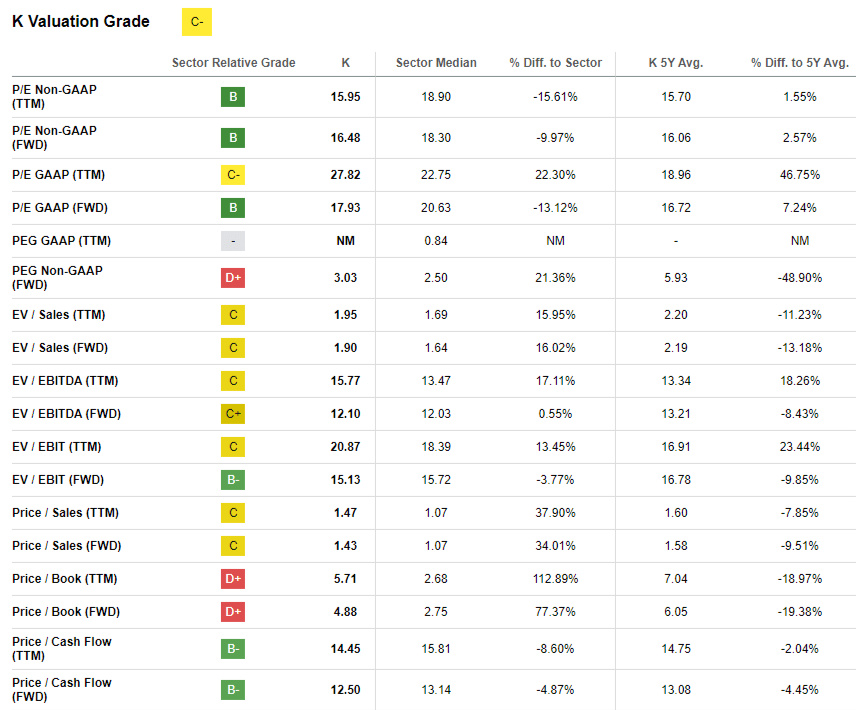

The stock significantly underperformed the broad market year-to-date, with an approximately 5% decline in the stock price. Seeking Alpha Quant assigned the stock a "C-" valuation grade suggesting the stock is fairly valued with limited upside potential. Indeed, multiples analysis of the comparison between current and historical multiples and the sector median, suggests mixed results.

{kind=link}

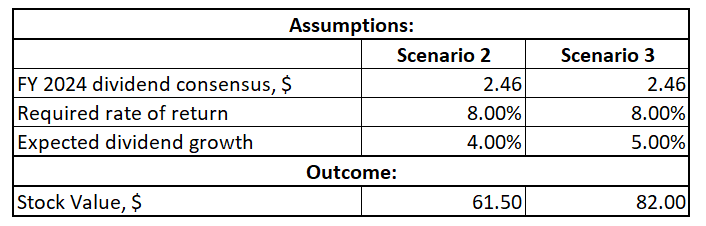

The company has a stellar dividend history with eighteen consecutive years of dividend growth and multiple decades of consecutive dividend payouts. Therefore, I implement a dividend discount model [DDM] approach to expand my valuation analysis. Dividend consensus estimates expect an FY 2024 dividend of $2.46, which I use as the current dividend for the DDM formula. I use an 8% WACC for the required rate of return, which aligns with a suggested valueinvesting.io range. K has a decent "B+" dividend growth rate from Seeking Alpha Quant, but the metrics related directly to the dividend growth are lagging behind the sector median and the 5-year averages. I use a long-term 10-year dividend CAGR, which is close to 3% for my base-case scenario.

Author's calculations

With a conservative 3% dividend growth rate, the stock's fair value is about $49. It is about 30% lower than the current market share price. The DDM outcomes are susceptible to the dividend growth rate, so let me demonstrate a couple more scenarios in the table below.

{kind=link}

As we can see above, the stock becomes attractively valued with about 20% upside potential only when the dividend growth rate approaches 5%. Let me refer to the dividend history to assess the probability of a sustainable 5% dividend increase. Over the past ten years, there was only one year of above 5% dividend growth. Times of aggressive dividend growth seem to be in the rearview mirror, and there is little evidence that dividend growth will bounce back to 5% in the nearest future.

Compiled by the author

I am highly convinced that the dividend growth is doubtful to bounce back to 5% for several reasons. First, the payout ratio is rather high at 55%. Second, the company's revenue is expected by consensus forecasts to grow at low single digits. Third, in the financial analysis section, we saw that the company's profitability metrics are in a long-term stagnation, and the FCF margin has deteriorated substantially over the past decade. Overall, I believe it is highly unlikely that the company will achieve a sustainable high dividend growth rate in the foreseeable future. Therefore, I think that the valuation is unattractive.

Risks to consider

A vast portion of the company's sales are generated outside of North America, meaning earnings are vulnerable to several risks related to international trade. The company's operations may be disrupted in case of unfavorable changes in international trade regulations or tariffs. Also, generating more than 40% of sales outside North America means the company has extensive exposure to foreign exchange volatility.

It is also obvious that there is an unfavorable secular shift for Kellogg related to consumers' shift in preferences toward healthier food. Due to a solid brand and vibrant history, it would be a big challenge for Kellogg to change its public image to become perceived as a health food producer.

The company also faces significant risks related to the high volatility of raw materials and other elements of cost inflation.

Bottom line

Overall, I am not investing in the stock. The business seems to be in a secular decline due to changing consumer preferences. I see no quick wins for the management to overcome secular challenges. Profitability metrics are declining, and recent and upcoming quarterly performance suggest that the trend will continue. Moreover, the valuation does not look attractive. A 3.5% forward dividend yield does not outweigh all the cons of investing in the stock. Therefore, I assign the stock a "Hold" rating.

For further details see:

Kellogg: The Business Is In A Secular Decline