K - Kellogg: The Problems Of A Low Margin Producer

2023-09-19 14:11:31 ET

Summary

- Kellogg continues to underperform its peers as 2023 gears to be a very disappointing year for shareholders.

- Tailwinds for topline growth are dissipating as volume declined by 7.6% during the last reported quarter.

- Improving margins would be a major challenge for Kellogg's management as macroeconomic environment is no longer supportive.

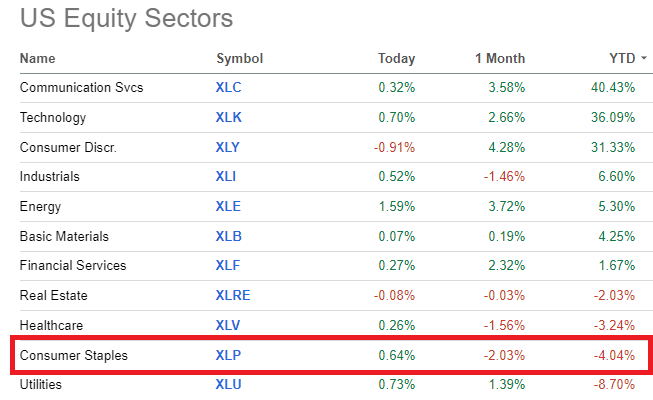

It has been a rough year so far for consumer staples as risk-seeking behaviour has driven growth tech stocks to new highs. As a consequence, the Consumer Staples Select Sector SPDR® Fund ETF ( XLP ) is one of the worst performing sector ETFs of the ones listed below.

{kind=link}

As a result, one would expect that a large cap Packaged Food company would not fare well in this environment either, but certainly not that it will significantly underperform the XLP.

This is now the case with Kellogg ( K ), which has a negative total return of nearly 14% since the start of the year.

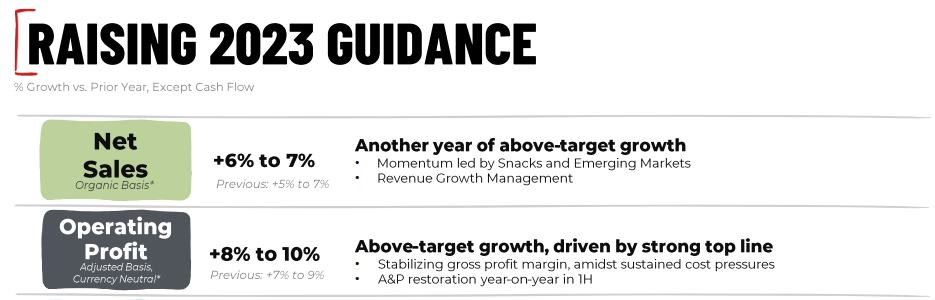

Even more surprising has been the fact that during this period the company has raised its guidance for the year as it makes good progress with the proposed restructuring of the business into two separate entities.

{kind=link}

Earlier this year, I warned that focusing on snacking would not be the silver bullet for Kellogg's shareholders and it appears that market does not believe in that either. Nevertheless, it is a step in the right direction as the company has been in a very tough spot within the Packaged Food segment and has been underperforming the market for more than 3 years now.

{kind=link}

Looking ahead, I see very small chances of Kellogg outperforming the XLP over the coming months, even though a wave of investor optimism is likely be experienced following the split.

Fading Tailwinds

As inflation accelerated, Kellogg alongside its peers have been in a race of who will be able to introduce the largest price increases to offset inflation, but also without sacrificing volume growth.

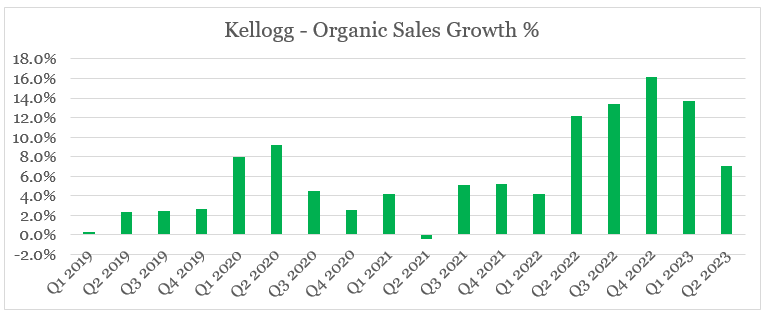

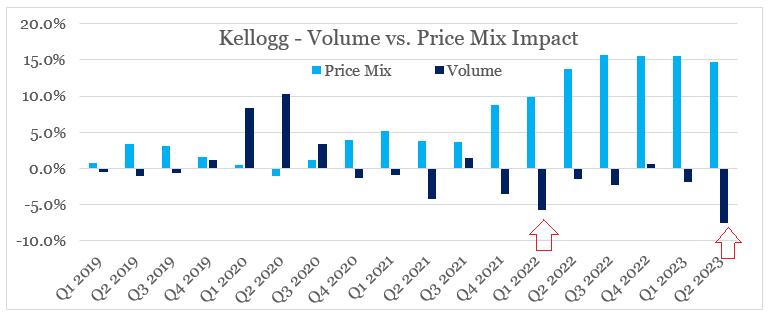

That is why, organic sales growth skyrocketed in recent quarters and reached 16% during the last 3-month period of 2022. Unfortunately, however, as we could see on the graph below, Kellogg's topline growth is down sharply during the latest quarter and is already at mid-single digits.

prepared by the author, using data from Quarterly Presentations

{kind=link}

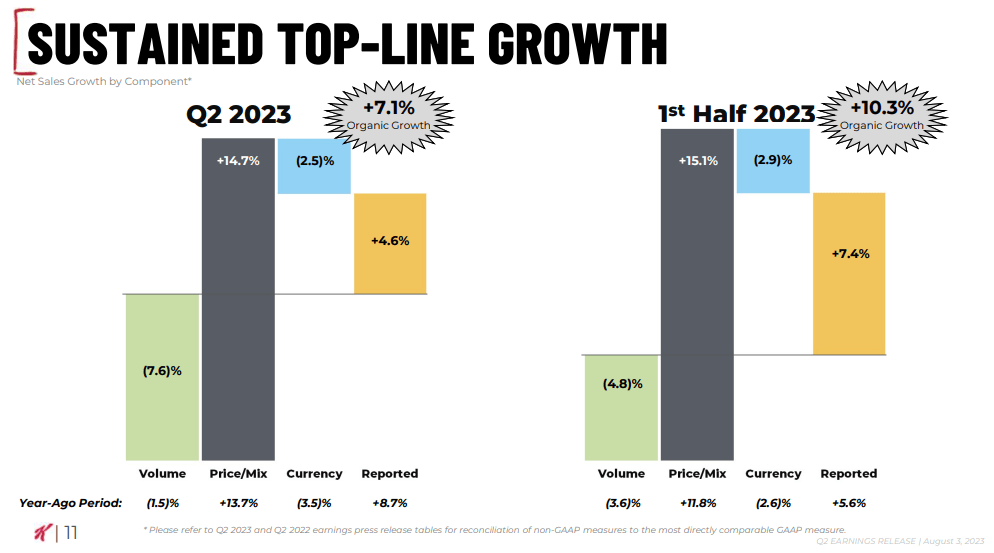

As we break down the topline growth figure, we could see that the 7% organic growth during the latest quarter was entirely driven by pricing initiatives as volumes declines by a staggering 7.6%.

{kind=link}

The management was blaming price elasticities in combination with a lapping of the period when the company significantly increased its inventories.

As expected, price elasticities continued to move higher around the world, and this weighed down our volume.

Also contributing to our volume decline was lapping last year's replenishment of trade inventories , particularly as we recovered from the cereal strike.

Source: Kellogg Q2 2023 Earnings Transcript

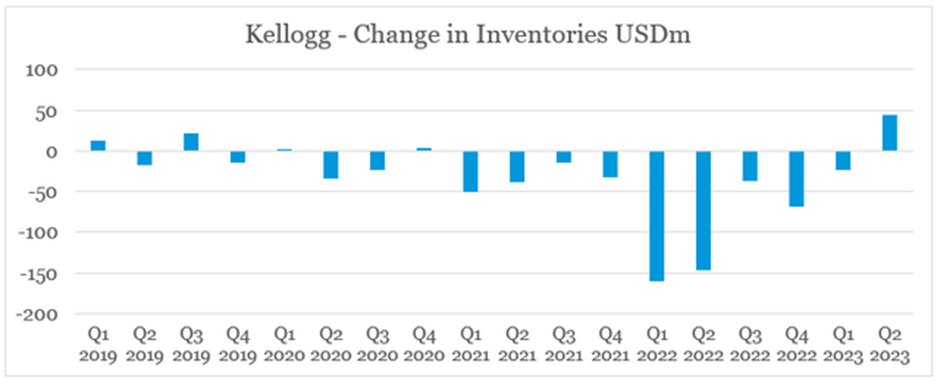

The latter could be seen in the graph below, where in Q1 and Q2 of 2022 Kellogg's invested heavily into trade inventories is already reversing this course.

{kind=link}

In the first half of 2022, however, volumes fell significantly (see Q1 2022 on the graph below) and Kellogg invested heavily in inventories in anticipation of growth picking up. In hindsight, this did not materialize and as volumes fall dramatically once again, Kellogg's management is forced to reduce the level of inventories.

prepared by the author, using data from Quarterly Presentations

{kind=link}

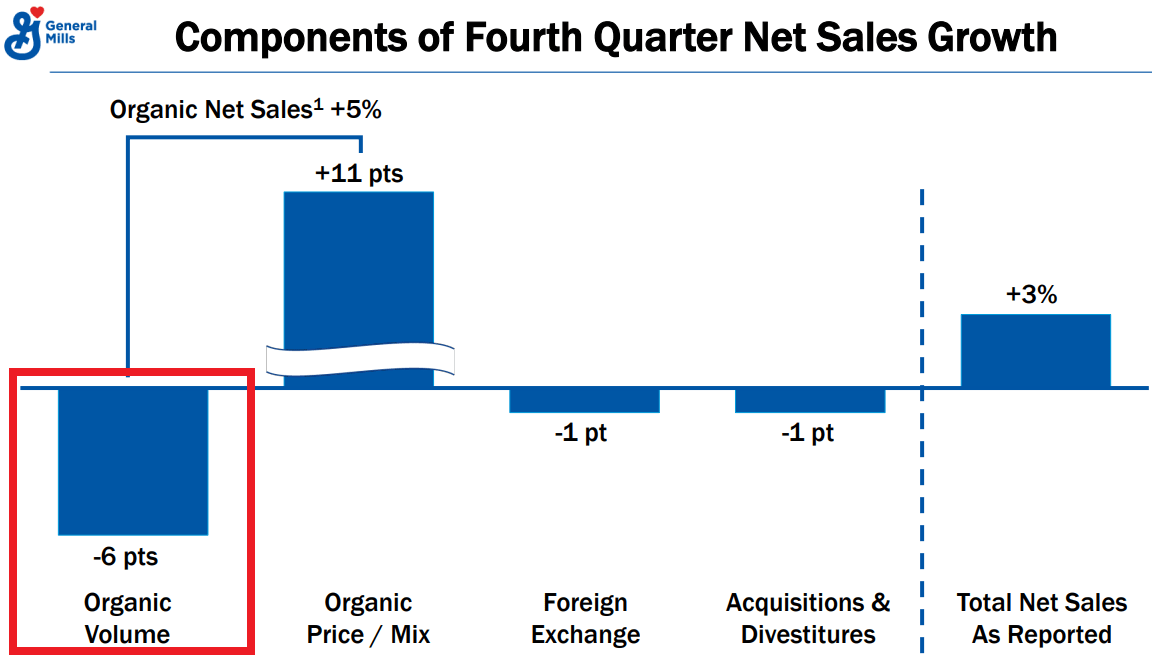

The impact of Price/Mix on the company's topline figure is also slowly fading away, but more importantly Kellogg's major peers, such as General Mills ( GIS ) are recording lower volume drops.

{kind=link}

At first glance, it would appear that Kellogg is in a better position since the 14.7% price/mix impact we saw above is far higher than the 11% for GIS in the graph above. But in reality, K has one of the lowest gross margins within the large cap Packaged Food segment and is well-below the broader sector median.

Seeking Alpha

What that means is that the company needs to sacrifice much larger percentage of its volume growth with the implementation of more aggressive pricing measures, in order to sustain its low gross margin. Higher gross margin peers, such as GIS and Mondelez ( MDLZ ), are in a much better position to benefit from the recent rise in inflation.

Struggling With Profitability

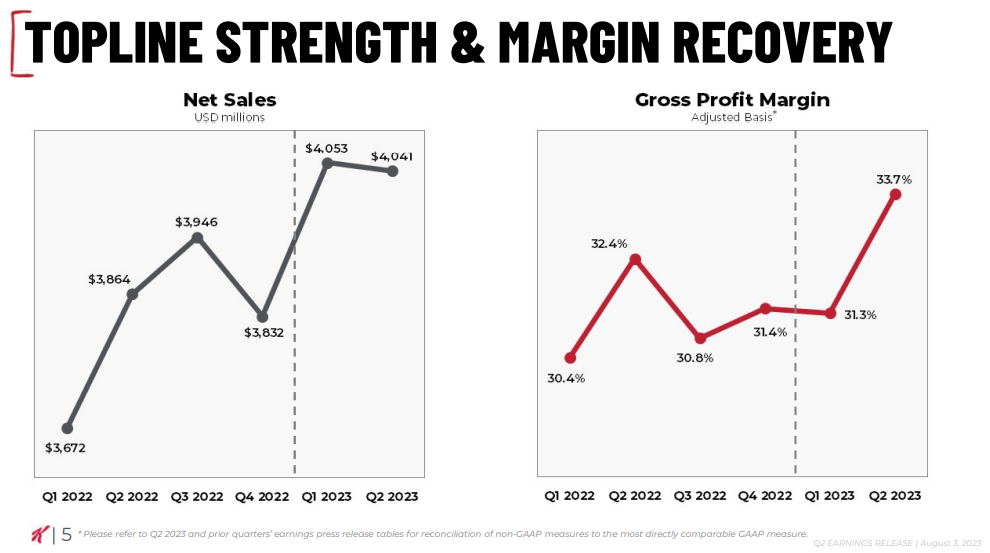

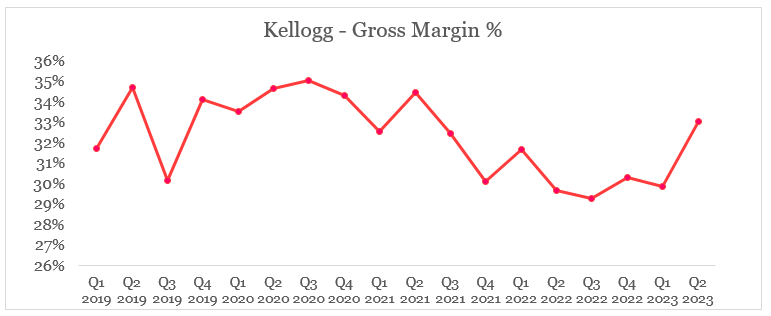

During the most recent quarter, Kellogg's management has highlighted the progress made as far as margins are concerned. On the graph below, we could see that gross margin is now at its highest level since Q1 of 2022.

{kind=link}

Zooming back a few more quarters, we could see that the non-adjusted gross margin figure for the company is at much lower levels than it used to be prior to 2021.

{kind=link}

In order to achieve its previous levels of gross profitability, I suspect that Kellogg would need to implement more price increases going forward, unless the cost of raw materials falls sharply.

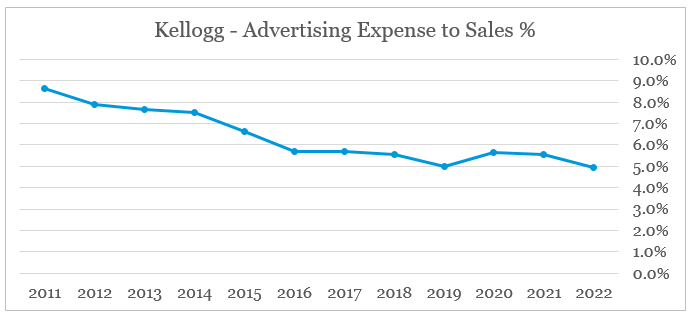

In addition, Kellogg has been gradually reducing its advertising expenses relative to sales over the past decade (see below). On itself, this is a major red flag given the very broad brand portfolio that needs to be nurtured through consistent marketing and advertising spend.

{kind=link}

Reducing brand building activities at a time when you need to hike prices and volumes are falling, is not a good recipe for sustainable long-term growth.

Even after all these measures, Kellogg's operating margin is still at record low levels and once again near the pre-pandemic lows.

To make matters worse, non-operating expenses, such as interest expense, are also increasing which creates additional problems for the company's profitability on a net income basis.

Interest expense increased significantly year-on-year due to higher interest rates. In the second half, we expect to see modestly lower interest expense than we recorded in the first half, owing to the timing of cash flow.

Source: Kellogg Q2 2023 Earnings Transcript

All that puts the company in a very delicate position where margins need to improve through higher product pricing and restructuring, but at the same time more resources will be needed to combat the negative volume growth and fending-off higher margin peers.

Conclusion

Kellogg's disappointing share price performance year-to-date is hardly a surprise for anyone who has considered the company's tough competitive positioning within the Packaged Food space. Having low gross margin has now turned into a problem for the company as management is struggling with rising costs of raw materials and more pressure from competitors. Although the ongoing restructuring would most likely bring a wave of optimism for investors, I remain skeptical of the company's ability to outperform higher quality peers over the long-term.

For further details see:

Kellogg: The Problems Of A Low Margin Producer