CA - Kelt Exploration Changes Strategy

2023-11-10 12:12:22 ET

Summary

- Kelt Exploration has changed its strategy to focus on living within cash flow and keeping debt low.

- CGX Energy, in contrast, has no source of income. It therefore constantly needs to raise cash. The income source if any is probably years away.

- The success of management, including selling to Exxon Mobil, demonstrates Kelt Exploration management is very experienced which lowers investment risk.

- Frontera controls CGX which creates a natural conflict of interest and probably puts CGX shareholders at a considerable disadvantage.

- Kelt Exploration is a growth story with a bright future and the cash flow to finance it. It may at some point become an acquisition candidate.

Mr. Market has not noticed that Kelt Exploration Ltd. ( OTCPK:KELTF ) has changed its strategy. Kelt received a lot o f attention by selling acreage to Exxon Mobil a few years back. That accomplishment got the company a lot of publicity at the time. However, management continued to sell acreage to raise cash to continue to develop its acreage while piling up debt. This method of growing became unpopular with the market and the debt market. Now management has switched strategies, but the company is still known as an asset story. Some patience is required. But eventually the market will catch on to the company's new strategy of living within cash flow while keeping debt low.

Past Rapid Debt Fueled Growth

Once a small company gets a reputation it's hard for that company to get the same amount of attention when things change. A company like this one was known for rapid debt-fueled growth followed by a sale to reduce the debt, keep some production, and then "rinse and repeat." It did not help that the main source of production was natural gas.

The result is that the latest quarterly and probably annual reports do not get the same attention across the market which may be frustrating to management.

(Note: This is a Canadian company that reports in Canadian dollars)

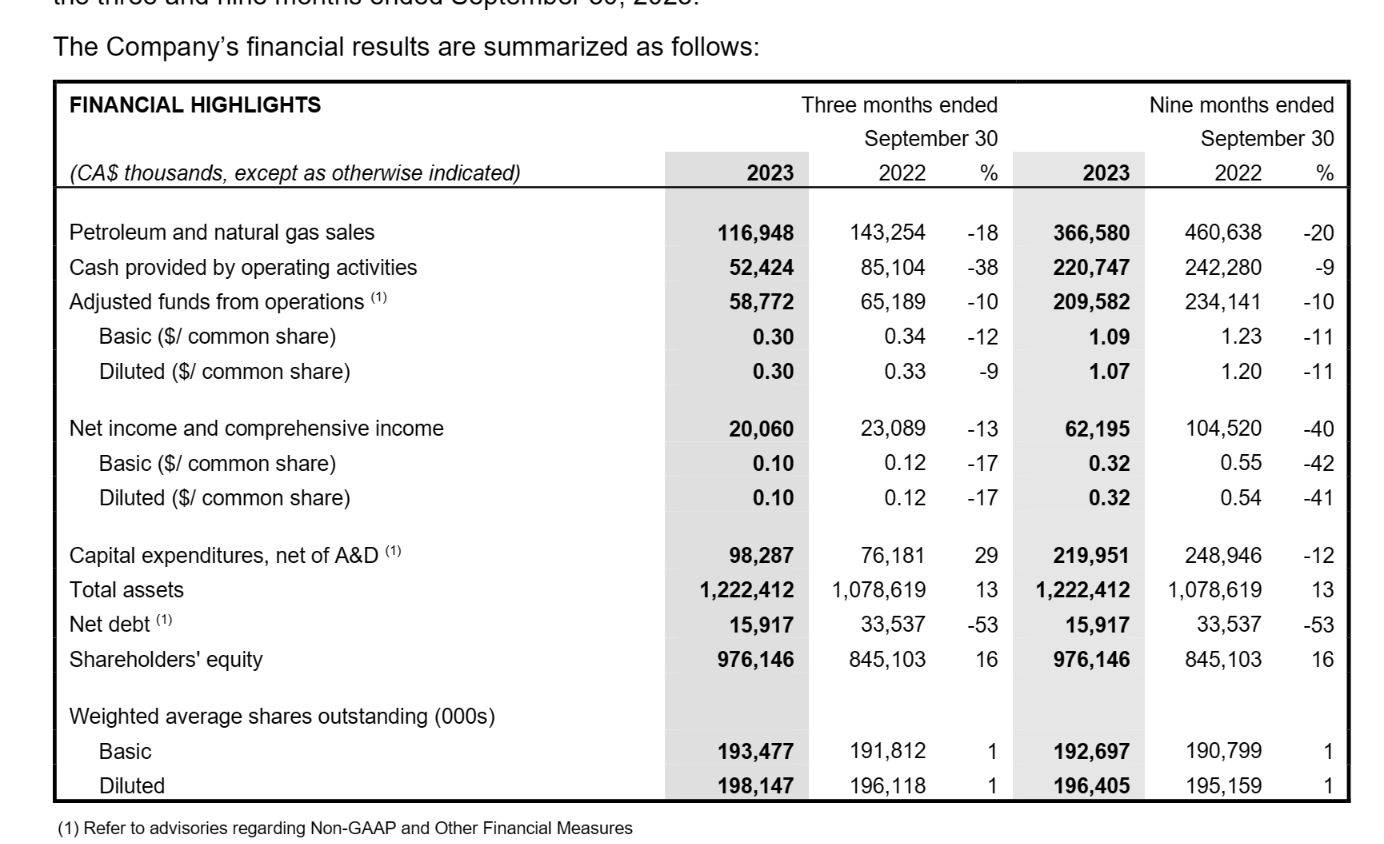

Kelt Exploration Summary Of Third Quarter Results 2023 (Kelt Exploration Third Quarter 2023, Corporate Presentation November 2023)

{kind=link}

Kelt reported good progress. Now the growth is slower than in the past. But the debt also decreased from the previous year to keep things conservative. The investment opportunity here lies in the fact that the conservative strategy takes a lot of small company risk out of the equation.

The company also has rich gas production. So, there's oil and other liquids that raise the average price of the production sold. At the same time management has good enough acreage to keep production costs low which allows for a bigger margin to increase profitability.

Patience Needed

It takes a little bit of time for this kind of result to affect the stock price because price-earnings ratios collapsed throughout the industry. This is especially true with small companies (and doubly true with small Canadian companies).

But any management that can sell to the likes of the Exxon Mobil Corporation ( XOM ) is likely worth watching. The small company world has a whole lot of "pretenders," and worse. Therefore, you need an edge when you consider investing in a company like this. This success of management as shown in the latest presentation in addition to selling to Exxon Mobil is likely to be that extra edge needed for a small company investment to succeed.

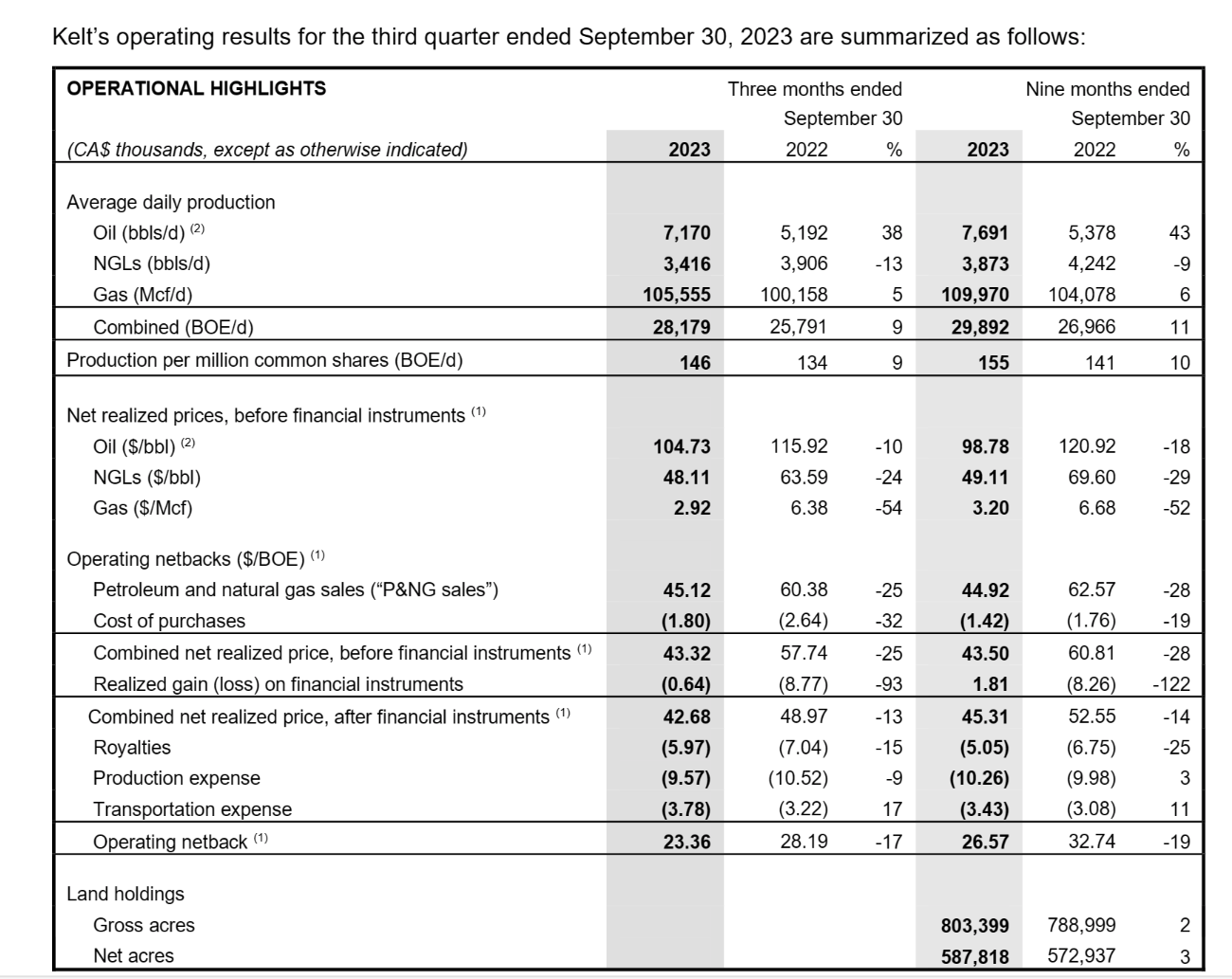

Production Stream

This rich gas production has a fairly large amount of oil in the production stream compared to other rich gas producers. This gives the company a competitive edge even though there are costs associated with separating out the various products and getting them to market.

Kelt Exploration Production Mix And Margin Calculation (Kelt Exploration Corporate Presentation November 2023)

{kind=link}

This company also may be an asset story as well which would make it a potential acquisition candidate for the right price. Notice the huge amount of acreage compared to the relatively small amount of production. Given management's past success in selling acreage (with production on it), there's likely value there in excess of the current stock price.

That value will take time to realize. But management has demonstrated time and again through those asset sales that they know how to find good acreage and sell it for a profit back when this was a viable strategy. That acreage is likely still good. Management just has to go about realizing value differently.

Also, notice that the operating netback is roughly half of the weighted average selling price per barrel. That implies a very profitable company that's likely to make money under some very hostile industry conditions. The diversification of the sales stream also aids in the overall company profitability throughout the market cycle.

The last thing to note is that the company is dependent upon a matrix of prices to calculate the breakeven point for any one given product. Therefore, the breakeven point is dependent upon the prices assumed for the other significant products (as there could be some without enough volume to matter).

Growth Story

This Canadian producer is part of the Canadian oil and gas industry that's primarily based in Alberta but can extend into the neighbors which have sizable production as well depending upon industry conditions and what management can buy when they are shopping.

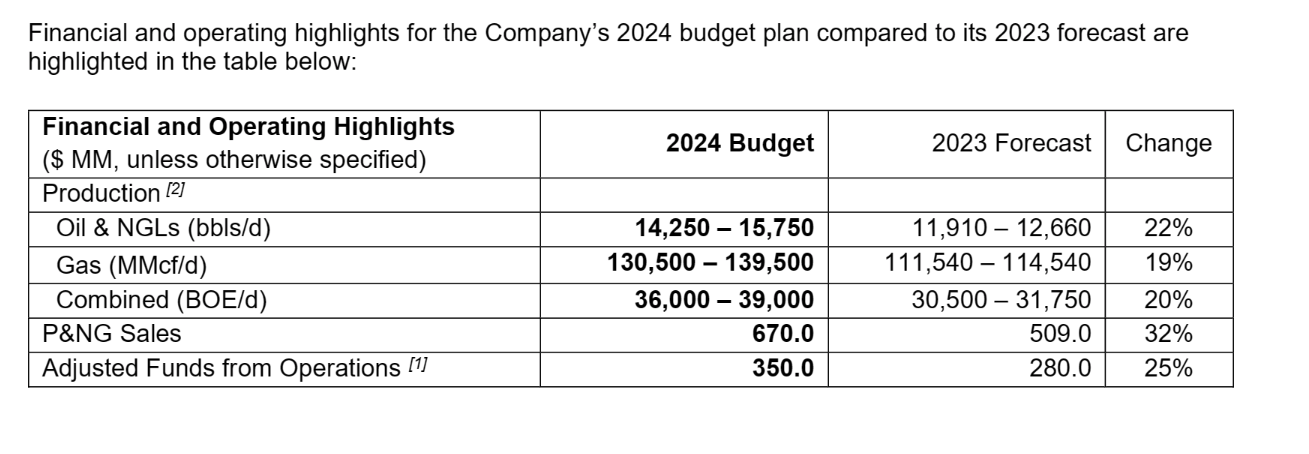

Kelt Exploration General Budget Guidance For Fiscal Year 2024 (Kelt Exploration Corporate Presentation November 2023)

{kind=link}

This management has scored enough "victories" that the issue is probably much safer than many larger upstream plays. However, volatility and low visibility are very characteristic of the industry. Smaller companies like this one with a low stock price can be far more volatile. Therefore, only shareholders that are OK with a lot of stock price volatility and uncertainty about the future should consider this stock.

That being stated, this is a growth story and the management behind this growth story has a lot of experience growing and then selling that growth for a profit. That plus the low debt takes even more risk out of the investment. But because it's a small company it probably should be considered as part of a basket because smaller companies like this one often lack management depth if something happens to a key officer.

Compare To CGX Energy Inc.

CGX Energy Inc. ( OTCPK:CGXEF ) is a Canadian company doing business in Guyana. This company i s largely controlled by Frontera Energy Corporation ( OTCPK:FECCF ). A major issue is that both companies are involved in Guyana. Therefore, the management of Frontera has a conflict of interest when it comes to the interests of CGX Energy. The chances of management favoring Frontera's interests as a result are huge (to the detriment of CGX Shareholders).

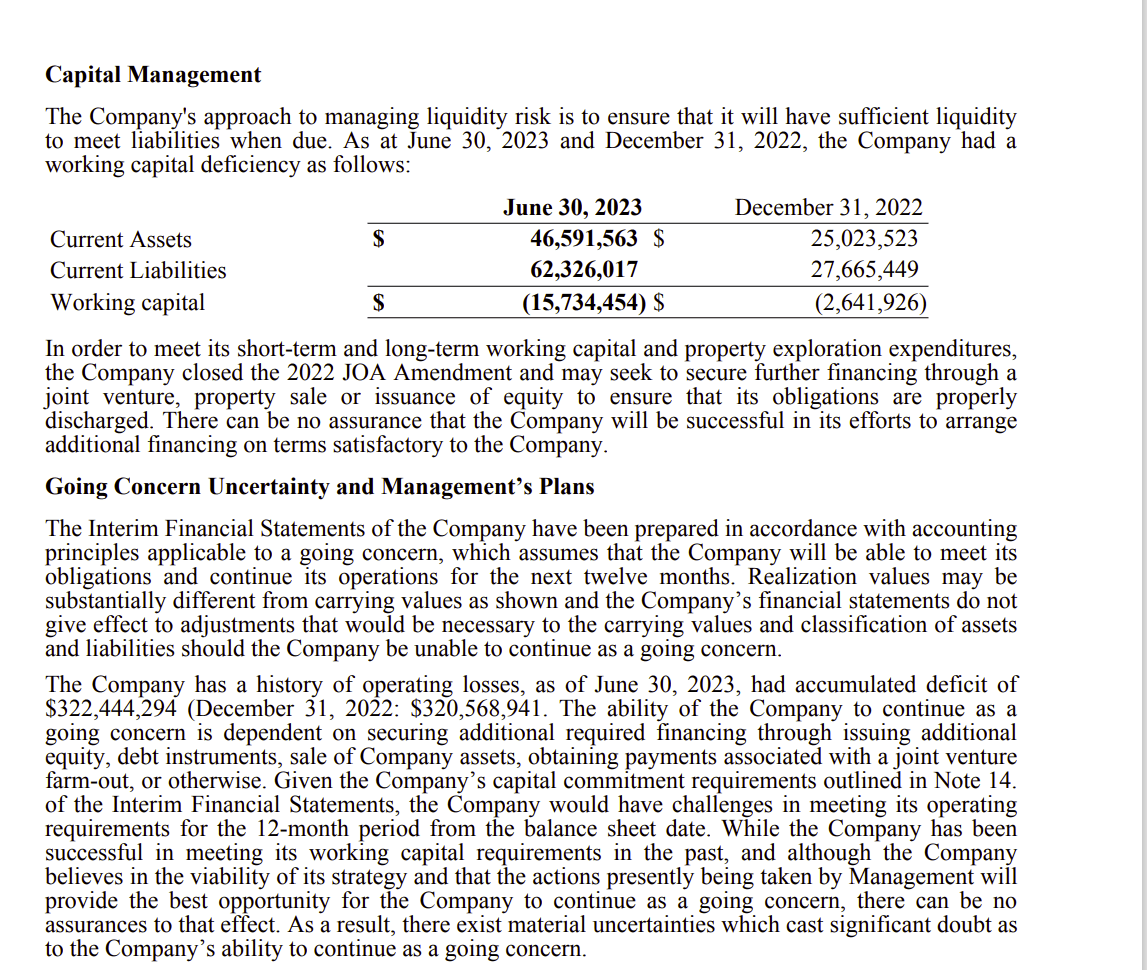

CGX Energy Inc. Going Concern Issues

Everyone needs to read all the details about the going concern and then read every last financial report (especially the fine print).

CGX Energy Working Capital Deficit And Going Concern Statement (CGX Energy Management and Discussion Analysis As Of June 30, 2023)

{kind=link}

At times, the management of CGX has approved the issuance of debt even though the company has no income. This puts the shareholders of CGX in a very poor position to bargain for anything that needs to be bargained about.

Even if there was no debt issuance, CGX needs to raise money constantly until it has a source of income. That need dims the capital appreciation outlook for some years to come. What's left is a potential trading situation based on the volatility of the low price of the stock. CGX is probably years away from any reasonable amount of revenue (if any).

But more importantly, even Frontera is too small to be dealing with offshore projects. Those projects are giant projects. So a far larger company like Hess Corporation ( HES ) which is partnered with Exxon Mobil Corporation ((XOM)) in Guyana is considered a small player in this particular "sandbox." Hess has at times had billions of dollars available on credit lines and kept a large cash balance to participate in this venture. Frontera and CGX are nothing close to the size of Hess which leads to all kinds of financing questions for a (very small) company of this size.

Furthermore, large companies in the area tend to play hardball with smaller companies that have less financing. That makes both CGX and Frontera highly risky and only for investors who realize they are likely to lose the total investment rather than achieve that "homerun" they're looking for. Both companies likely are at a big disadvantage in Guyana.

Because of this CGX is far too dangerous for most investors as it would be considered a specialty investment at best and a lottery ticket most of the time. Frontera does have income and is a going concern. But Frontera, likewise, is much too small to handle an offshore project let alone all the other stuff the two companies claim to be involved in the area. As long as this is part of the Frontera portfolio, this likewise makes Frontera an extremely speculative investment proposition even though it has better survival chances than CGX.

Summary

Kelt Exploration has experienced management and the ability to live within its means. While Kelt is a growth story, the experience of management indicates this upstream play is far safer than most upstream competitors. The low debt and conservative balance sheet further lower the risk.

CGX on the other hand lacks offshore experience. Both this and the controlling company, Frontera, are far too small for offshore and related projects. At best, investors will suffer a lot of dilution with the risk that the dilution will likely eliminate capital gains and could produce a loss.

CGX in particular has a going concern note in the financial statements which means the public accountants see a significant risk of the total loss of an investment.

Frontera is far more likely to survive. But investors do not invest based on survival prospects (mainly, though it's a consideration). Investors invest for capital gains. That prospect, when the company is too small, is low at best and probably is far worse.

For further details see:

Kelt Exploration Changes Strategy