MEI - Kimball Electronics: Consistently Topping Record Quarterly Sales

2023-09-28 07:47:44 ET

Summary

- Kimball Electronics provides electronic manufacturing services globally and has experienced significant growth in its stock price over the past 9 years.

- The company’s electronic solutions in the automotive, medical, and industrial services industries are delivering on all cylinders.

- Kimball Electronics has been achieving record sales figures and increasing margins, indicating potential for further growth.

- I rate KE stock as a Buy for its capacity of services which is displaying profound rates of improvement.

Kimball Electronics ( KE ) is a front-runner in the EMS industry with its reliable automotive, medical, and industrial services. The company projects further growth in its automotive segment as there is a megatrend in customers adding electronic components to their vehicles. I believe that its expertise in chassis control aligns well with this industry trend. As the population ages and healthcare becomes more affordable and accessible, it should continue to grow in this industry as well. Kimball has the right-sized devices to complement the industry movement toward high-precision smaller-sized medical devices. Meanwhile, a s consumers trend toward the righteous path of conserving water, gas, and electricity, Kimball powers the revolution through its natural resource consumption strategy. They are well-positioned in the value chain to provide residential and commercial heating and cooling, as well as smart metering in Europe, factory automation, and EV charging stations. As demand for electric vehicles and their parts grows more dominant, Kimball will reach record sales, and improving cash flow along with its low valuation are the reasons I rate the stock a Buy.

Company Overview

Kimball Electronics provides electronic manufacturing services to customers globally. The company has 7200 employees in facilities around the world, including in Indiana, China, California, Florida, Mexico, Poland, Romania, Thailand, and Vietnam. The company went public in November 2014 at a stock price of $5.19 and has gained 449% in the 9-year timeframe. The ISS ESG Corporate Rating places Kimball Electronics among the top 10% of its industry. Kimball has ranked in multiple categories for Service Excellence in the Circuits Assembly for nine consecutive years. This is exemplary.

My Qualitative/Business Discussion

Kimball is a single-source provider of its electronic components. The company generates recurring revenue with customers, keeping a range between 3-10 years in length of the contracts. This allows Kimball to accumulate predictable revenue, enabling the company to plan for expansions and operational efficiencies. Its relationships are based on guarantee and trust which translates into returning customers and an ongoing stream of orders in its pipeline. The company focuses its projects on return on invested capital, which shows that Kimball is concentrated on creating most of its profits from its investments.

Its industry segments are industrials, public safety, medical, and automotive. Industrials comprise 23% of its business and focuses on climate and automation controls. Public Safety is 4% and includes thermal imaging, first responder electronics, and security. Meanwhile, medical solutions are 29% and range from sleep care to drug delivery to patient monitoring. Lastly, its automotive segment comprises 43% of its business, focusing on solutions in electronic steering and braking, body controls, and automated driver systems. These various strategies to generate revenue and top-line growth are putting the pedal to the metal on its net sales, which have shown up enormously in its record-beating earnings results over the past 6 quarters.

Financials

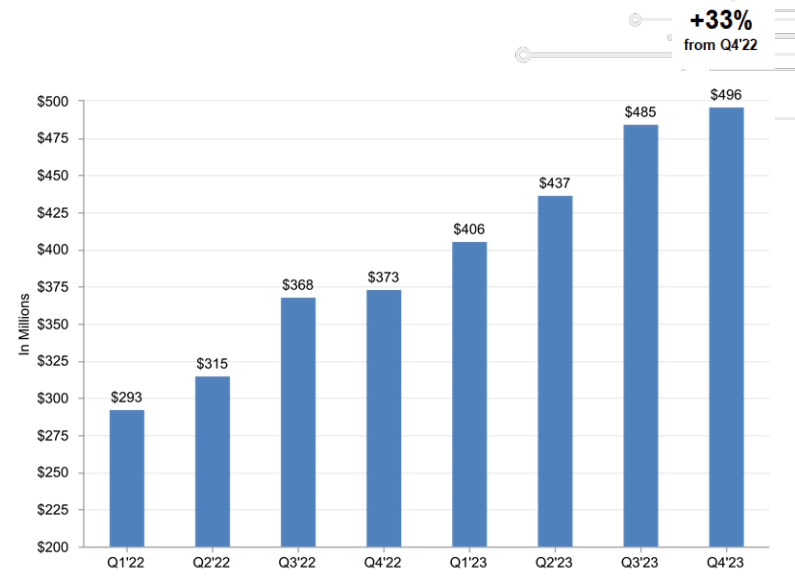

Kimball has been growing record sales figures for six consecutive quarters to go along with increasing margins at the same time. Inventory is leveling off, contributing to improved cash flow and the trend is expected to continue in fiscal year 2024. Automotive net sales were $220 million for the latest quarter (fourth quarter of fiscal 2023), representing an increase of 44% YoY. Medical net sales were $121 million, an increase of 6% YoY. Industrial net sales were a record $142 million, representing a 38% increase YoY.

KE Sales Chart (Investor Presentation)

{kind=link}

While the sales figures are impressive, KE still looks poised to make further growth. Gross profit has been on the rise beginning September 2022 and is currently $47.3 million . Record sales in electronic manufacturing services led to an 80-bps margin improvement, compared to the year-ago figure. This gross margin rate in Q4 was an all-time high at 10%. The company is making more money from each product sold, benefiting its top and bottom line growth. Furthermore, it has increased cash flow indicating an ability to hire additional labor which can lead to growth investments in its core businesses.

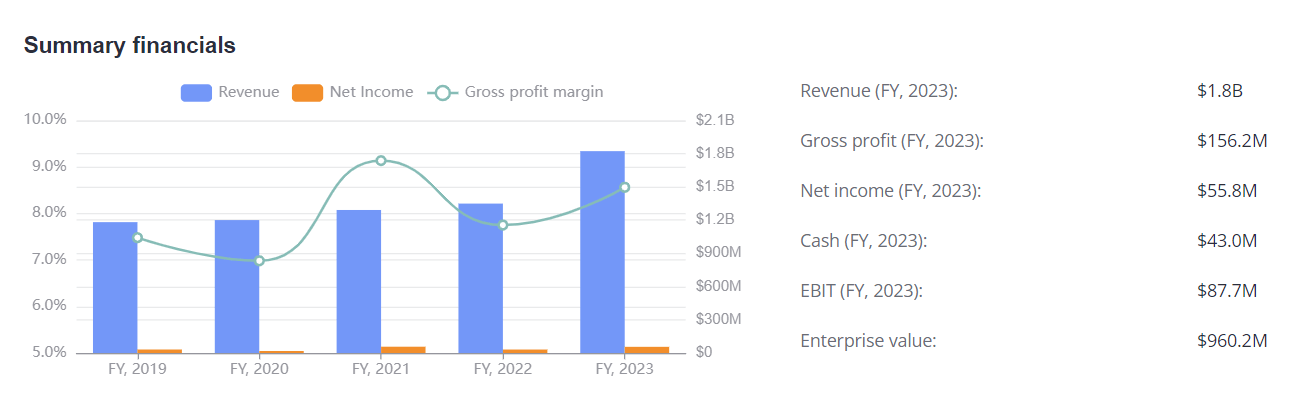

KE reported Q4 and FY 2023 financial statements at the same time on August 16. The graph below shows the financials for each of the last 5 fiscal years. As indicated by the green line is the gross margins. The average gross profit margin for electronic companies in 2021 was 3.49%. In 2021, Kimball's gross margin was nearly a staggering 9%, which is a 250% difference from the average. By doubling its primary credit facility from $150 million to $300 million , Kimball has granted itself greater flexibility to meet its CapEx and working capital needs. I strongly believe this action will improve its capacity for expansions, new product introductions, and long-term goals.

{kind=link}

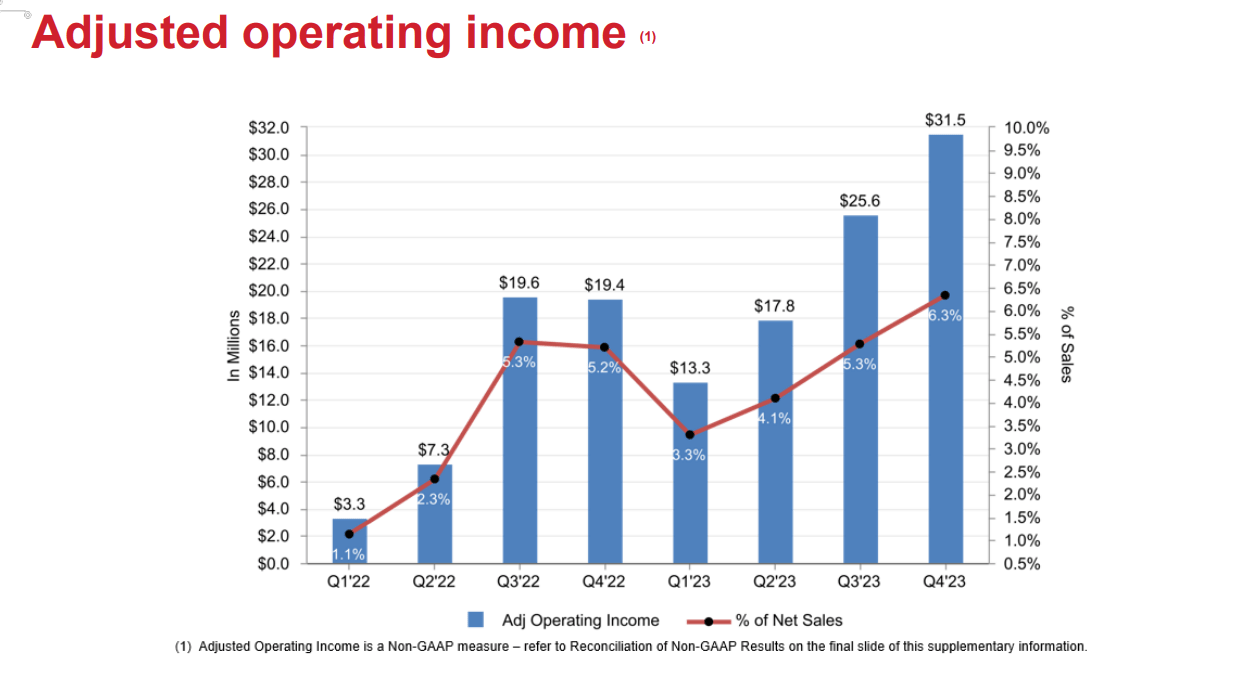

Cash flow from operations has increased significantly from $1.5 million to $44.1 million YoY while expenses as a percent of sales have decreased 30-bps from 4% to 3.7%. This left the company with more capital to be more aggressive with its strategic planning. Adjusted operating income was $31.5 million, or 6.3% of net sales. The chart below shows that in the latest quarter, the % of net sales going to operating income has cruised above the previous high in Q3 2022. From a trough in Q1 2023, the trend has been nearly a straight 45-degree line upwards, indicating that the company is gradually growing with room to expand further.

KE Operating Income (Investor Presentation)

{kind=link}

Valuation

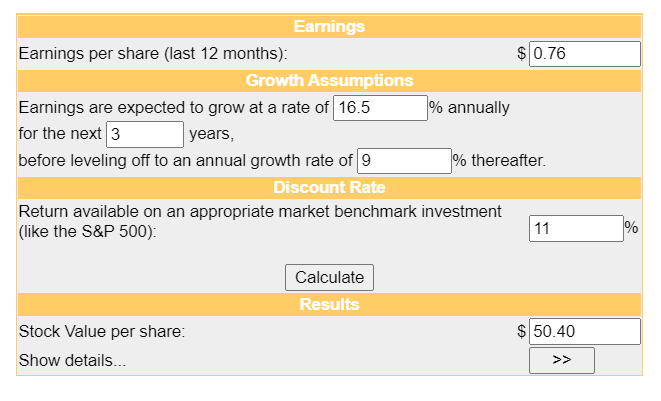

My valuation of KE begins with the DCF model. I will use the following in my estimation:

TTM EPS: $0.76

Expected growth rate for the next five years: 16.5%

Terminal rate: 9%

Return on benchmark S&P: 11%

{kind=link}

In this calculation, the stock is fairly valued at $50.40, representing 184% upside. In fiscal 2023, Kimball reported a nearly 80% improvement in EPS. Based on this performance, it would be hard to see why KE can't grow at 16.5% annually for the next three years. This average rate was taken from the growth rates of the next two years given by Seeking Alpha. KE will grow more mature after leveling off to a growth rate of 9% compared to the S&P of 11%. I expect KE to grow its customer base further, especially in automotive, as EVs become more dominant on the roads, where nearly half of its sales are derived from. By 2028 the EV market is projected to grow between $434 to $1318 billion . The fact that KE already has the capacity to produce parts at its factories for these vehicles translates into higher revenues and that is a sign that business will be good for years to come for Kimball Electronics.

Peer Comparisons

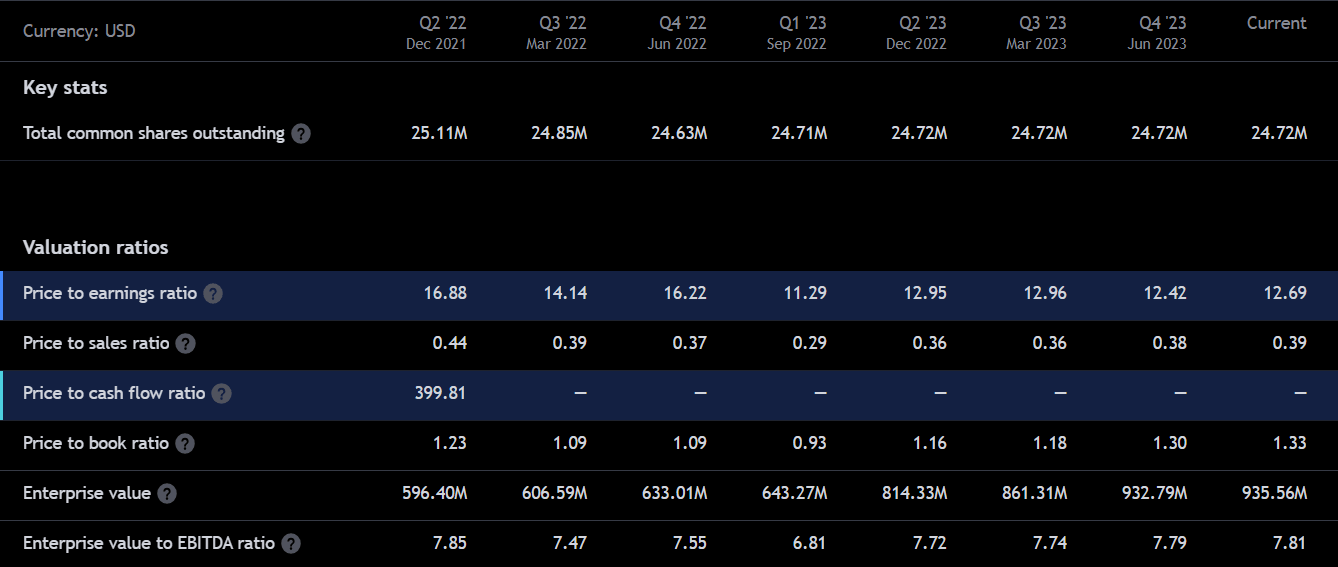

Kimball Electronics is an attractive investment for several reasons. It is undervalued based on many metrics such as price-to-earnings ratio, price-to-sales ratio, and price-to-book ratio. With a P/E of 12.69, Kimball stands out as undervalued compared to peer Methode Electronics ( MEI ) whose P/E is 25.37. While KE has an undervalued P/E, its market cap is less than that of MEI. Not surprisingly, KE has gained 45% in the past 365 days, while Methode Electronics has lost -40% in the same period. KE remains attractive at this moment while MEI is less than desired. A comparison with Benchmark Electronics ( BHE ), another peer to Kimball, shows that BHE is within range with a P/E of 12.03. However, as KE has surged in the last year, Benchmark Electronics has remained stagnant, shedding more than -6%. This points to the fact that BHE's revenues have not changed since last year and neither has its stock price. Although BHE may seem undervalued like KE, it does not have the potential that is evident within Kimball Electronics.

{kind=link}

I look further at the enterprise value to EBITDA ratio, which includes debt, of KE compared to its peers. At 7.81, it is relatively undervalued compared to the broader market. With MEI at 7.72 and BHE at 7.41, given their relative stock performance, this is an indicator that the electronic manufacturing services industry as a whole is underappreciated. It is evident in the price return of MEI and BHE but not with the likes of KE which has appreciated nicely.

{kind=link}

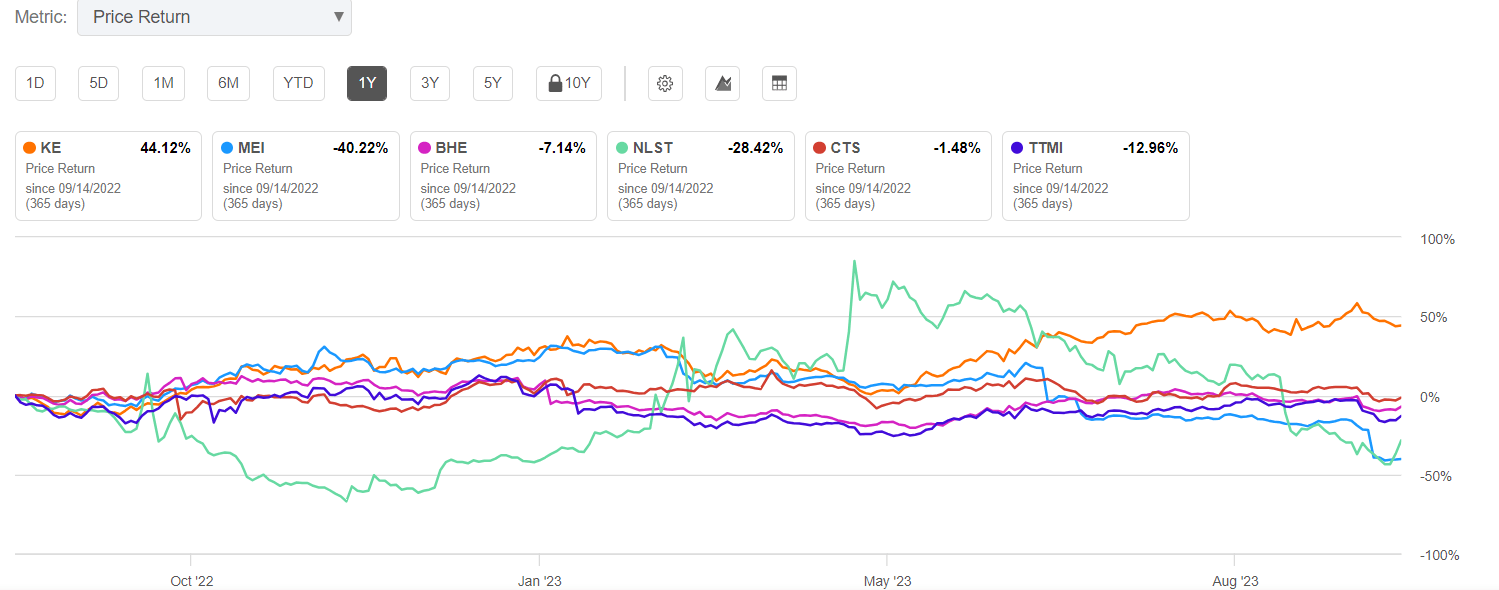

The chart above shows the price return for KE and several similar stocks in the electronic manufacturing services industry. It is clear that KE has been the sole gainer among its peers over the last year, gaining 44% while the rest have not made much improvements or sustained their gains. There can be multiple reasons for this disparity, but it is most clear that Kimball Electronics has its stock price safely secured in the hands of its investors. While Methode Electronics has added 10% more inventory in the last quarter, KE has lowered its inventory by 7.8%. This explains the reason why MEI reported a more than -100% drop in operating cash last quarter while KE has increased its own by over 300%. The trend is expected to continue for KE in fiscal 2024 and the same cannot be said for Methode.

I look to the EPS of Benchmark Electronics compared to that of KE to show that KE is a better investment there as well. While revenues for BHE at $733 million are more than the revenues for KE at $496 million, the EPS of BHE is lower than that of KE ($0.48 for BHE compared to $0.76 for KE.) EPS is a gauge of how a certain amount of earnings relates to its price level. The higher earnings-per-share for Kimball Electronics indicates that the company is more highly regarded when next to Benchmark Electronics, despite the lower revenues KE generates. In this comparison, KE comes out as the better investment choice if you are looking for a more valuable stock to add, in the electronic manufacturing services industry.

{kind=link}

Revenue Growth reports in the above comparisons are also at odds with Kimball. Kimball reported 35% year-over-year growth in revenues. An A grade was applied for that by Seeking Alpha's Quant Ratings. Compared to the 14% (B grade) of Benchmark Electronics or the 2.4.% (C- grade) of Methode Electronics, Kimball looks to be the clear winner here. Forward estimates of revenue growth tell a similar story, with Kimball Electronics receiving a B grade (15.5%), BHE receiving a C+ grade (10.6%), and MEI receiving a D grade (2.4%.)

Some Risks

The company derives a lot of its income from countries outside the United States, which poses certain risks. There can be geopolitical disruptions that occur in the foreign countries where Kimball manufactures and operates, which could impede the company's goals and timeliness. There can be economic and political instability in those regions that cause Kimball to slow down its schedule.

Kimball's automotive industry is one to note that could be interrupted by the Russia-Ukraine war that has been continuously disrupting supply chain operations around the globe. Kimball's European operations in Poland and Romania, which the company cites may have to take precautions in the future. I don't expect this to be a dramatic concern because the company has reported record sales numbers in automotive for the last six consecutive quarters while the war has been ongoing.

Summary

Kimball Electronics is rated a Buy from me. At current valuations, it represents a healthy stock that is not excessively inflated. At the current price of $28, I project that given the runway that the company has to operate, the price has an upside of 184%. Operating income as a percent of sales has just begun on the path upwards, breaking out to a fresh high last quarter. I expect that sales will continue to grow at a steady rate and the company will be within reach of its seventh record of quarterly sales next quarter.

I conclude by reminding that this is not financial advice. Everything is my opinion based on facts I have gathered from reputable sources. Do not make any investment without conclusively doing your due diligence on fundamentals, technicals, and macro factors.

For further details see:

Kimball Electronics: Consistently Topping Record Quarterly Sales