KEX - Kirby Bobbing Around Despite Strong Underlying Contracted Business

Summary

- Kirby posted better than expected fourth quarter results, with stronger results in inland marine on healthy demand trends.

- Petrochemical demand appears to be holding up and limited barge supply growth potential should be very supportive for utilization, pricing, and margins in 2023.

- Management has chosen to keep the D&S business for now, but a disposal would likely be the best outcome for shareholders.

- I see upside beyond $80 on strong underlying fundamentals for inland barging.

Despite good utilization trends and healthy contract rates, Kirby ( KEX ) shares can’t seem to build any real sustained momentum. Up about 5% since my last update , the shares have largely bobbed around between $60 and $70 for much of the last year before recently breaking out again above $70. While I understand concerns about a recession in 2023 and the navigability of the Mississippi River, I think the shares are undervalued today and offer upside into the $80’s.

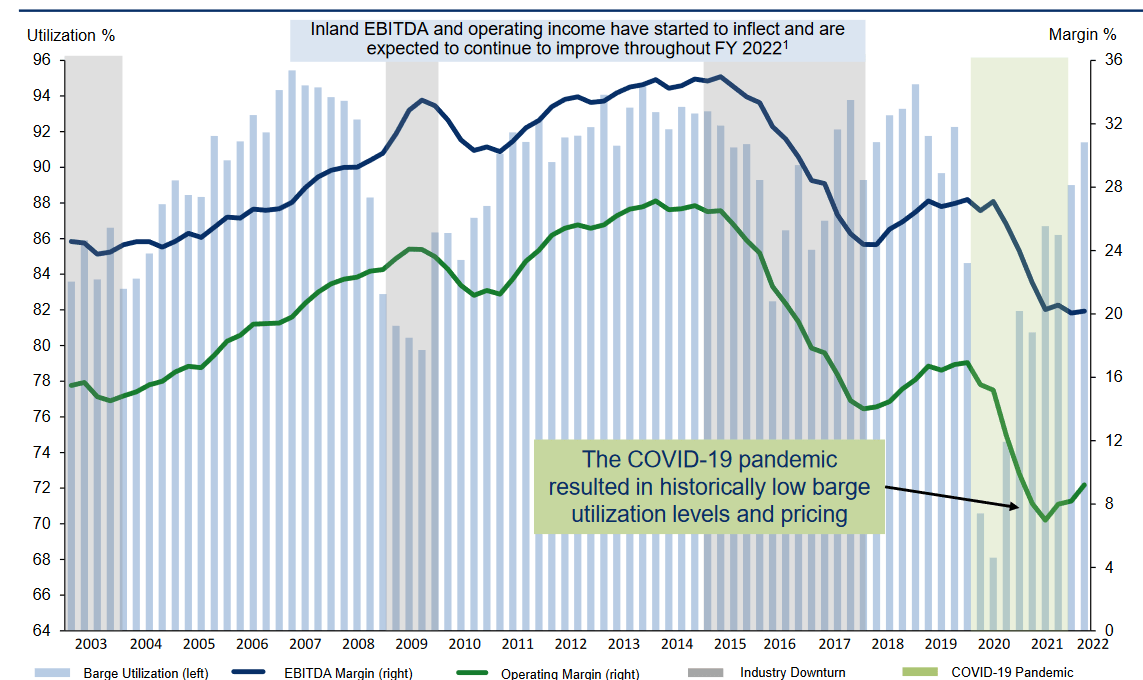

Strong Inland Results Propel The Quarter

Kirby’s fourth quarter results weren’t everything that an investor could have hoped for, but I thought they were strong on balance, with particular strength in the inland marine operations.

Revenue rose more than 23%, beating by more than 2%. Marine revenue rose almost 21%, with Inland up 24% and Coastal up 8%. Distribution and Services (or D&S) saw 28% revenue growth, with 44% growth in the oil/gas business and 18% growth in the other commercial and industrial operations.

Gross margin improved 30bp yoy and a point sequentially, reaching 26.9% despite pressures from higher wage and operating costs. EBITDA rose 36%, while adjusted operating income rose 86%, with margin up 270bp to 7.9%.

Marine operating profits rose 82%, with margin up almost four points yoy (and 150bp qoq) to 11.1%. I estimate that Inland made up more than 90% of Marine profits, with margins supported by strong price realizations. D&S operating profits rose 128% yoy, but slipped 23% qoq and missed my expectations on component/part shortages. Margin improved 240bp yoy and declined 160bp qoq to 5.5%, with the commercial/industrial side delivering high single-digit margins and oil/gas limited to low single-digit margins.

Barging Isn’t At The Top, But It’s On Its Way

Kirby continues to benefit from a combination of healthy demand for inland barging services and limited capacity. Utilization of 90% was an improvement from the mid/high-80%’s of the year-ago quarter and down a bit sequentially. Ton-miles declined 12% and Kirby saw more delay days due to water levels and weather, but revenue per ton-mile rose 41% to $0.10, and I believe this is the second-highest quarterly revenue/ton-mile rate in company history.

With limited shipyard capacity and elevated costs for new barges (around $4M according to management), new capacity isn’t much of a risk. At the same time, petrochemical companies are still seeing healthy volumes. Spot rates continue to rise, up low-to-mid-20%’s from last year and up low single-digits from the prior quarter, and Kirby is locking in new contract prices 10% to 15% higher than a year ago (and about a third of the time charters renewed in the fourth quarter at these higher rates).

Coastal is holding steady, with utilization in the low-to-mid-90%’s, low-to-mid single-digit sequential spot price improvement, and contract renewal prices up at a low-teens rate.

{kind=link}

I had been concerned about the risk of a peak/decline cycle in inland barging, but I think that has been pushed out a bit. While I do see the economy slowing in 2023, underlying activity is holding up and I don’t think petrochemical volumes are going to weaken all that much (likewise with refinery volumes). That should support healthy utilization rates and pricing, and while a return to one-time peak margins in the 20%’s doesn’t seem likely, a mid-teens operating margin for inland barging doesn’t seem like an aggressive guide from management.

Holding On To D&S For Now

Kirby’s D&S business has long been controversial, as this diversification outside of barging has never really lived up to expectations or produced meaningful shareholder value (relative to reinvesting in barges and/or buying back stock, it has likely destroyed value). Even so, management conducting a strategic review and decided to keep it for now.

D&S isn’t operating at its fullest potential now due to parts shortages caused by well-known supply chain issues across many industries, including delays that have limited Thermo King sales (so I’ll be curious what Trane ( TT ), the owner of Thermo King, says on their earnings call).

Still, it is benefiting from stronger oil/gas activity (D&S is a significant player in manufacturing and servicing well equipment like fracking rigs), as well as healthy marine and on-highway activity. While I can understand the idea of keeping D&S a little longer and working through some of these supply-side issues, I don’t think the outlook or performance of this business is going to get substantially better, and I think this is likely a good time to pursue a sale, even if Kirby can’t get top dollar because of those supply challenges.

The Outlook

At some point there will be a cyclical decline again in the barging business, but healthy petrochemical volumes and limited barging capacity seem likely to postpone that downturn for a little while longer. This does underline some of the modeling challenges here, though, as a cyclical reversal at some point is highly likely, but modeling it precisely is more luck than anything else.

Based on the strong trends in barging, as well as healthy oil/gas activity, I expect double-digit revenue growth in FY’23, but my longer-term growth expectation is still in the 3%-4% range (and consistent with the company’s long-term history). Maintenance needs will likely depress free cash flow below my long-term trend line for a couple of years, but I believe low double-digit FCF margins are attainable and I’m expecting adjusted long-term FCF growth in the 5% to 6% range.

Between discounted cash flow and an EV/EBITDA approach (using a 10.5x forward multiple), I believe Kirby is undervalued below the $80’s.

The Bottom Line

I don’t think Kirby is a buy-and-hold candidate, but I’m surprised the shares haven’t seen a bigger move and more positive rerating given the strength in the inland marine business. I think this strength will become more evident in the coming quarters, and I think this is a name that still has some appeal despite a slowing economy.

For further details see:

Kirby Bobbing Around Despite Strong Underlying Contracted Business