KEX - Kirby Corporation: Wait For Better Price Levels

2023-08-08 05:14:38 ET

Summary

- Kirby Corporation recently announced its Q2 FY23 results, with revenues rising by 11.3% compared to Q2 FY22.

- The company saw strong growth in its distribution and services segment, driven by the commercial and industrial and oil and gas markets.

- While the stock price has increased by 10% in the last 15 days, it is currently overvalued, and it is advised to wait for a retest of the breakout level before investing.

Kirby Corporation ( KEX ) operates domestic tank barges. It operates in two segments Marine Transportation and Distribution and Services. In the marine transportation segment, they offer marine transportation service and transports petrochemicals and refined petroleum products. In the distribution and services segment, they offer after-market service and sell authentic replacement parts for engines and reduction gears. KEX recently announced its Q2 FY23 results. I will analyze its financial results and technicals in this report. I believe one should wait for the stock to reach better levels. Hence I assign a hold rating on KEX.

Financial Analysis

KEX recently posted its Q2 FY23 results . The revenues for Q2 FY23 were $777.2 million, a rise of 11.3% compared to Q2 FY22. I believe the rise in revenues in its distribution and services and marine transportation segments was the main reason behind the revenue rise. The revenues from the distribution and services segment grew by 19.8% in Q2 FY23 compared to Q2 FY22. I believe the strength in its commercial and industrial, and oil and gas market was the main reason behind the revenue increase in the distribution and services segment. The commercial and industrial market revenues grew by 12% in Q2 FY23 compared to Q2 FY22. I think strong demand in its on-highway and marine repair businesses was the main reason behind its commercial and industrial market success. The revenues from the oil and gas market grew by 30% in Q2 FY23 compared to Q2 FY22, and I think higher demand for the new engines and transmissions was the major reason behind the success in its oil and gas market. Now talking about the marine transportation segment, its revenues grew by 5.2% in Q2 FY23 compared to Q2 FY22. I believe high demand and limited supply of barges led to an increase in term contract renewals, increasing the revenues in its marine transportation segment.

Its operating income margin for Q2 FY23 was 11.2% which was 6.6% in Q2 FY22. I believe there were many reasons behind the improvement in operating margin, like improved navigational conditions, but I think the major reasons were pricing efficiency and enhanced operational efficiency. With an increase in its revenues and operating income, its net earnings grew by 100.3% in Q2 FY23 compared to Q2 FY22. I believe KEX’s performance in Q2 FY23 was solid because they saw improvement in every aspect. Their revenues, margins, and earnings all saw strong growth, and I believe the limited availability of equipment in the inland marine market might result in further price increases, which might boost its revenues in the coming quarters. However, there are some issues that the company has been facing, like supply chain constraints and long lead times, that affected their operations in Q2 FY23. I believe these issues are improving and might not affect their operations in the coming quarters as much as they did in Q2 FY23. Hence considering these factors, I think we might see better financial results in FY23 compared to FY22. The management’s revenue guidance suggests the same they expect their FY23 revenues to be higher than FY22 by at least 10%, which is a positive sign, and considering all the factors, I think they might achieve the revenue targets.

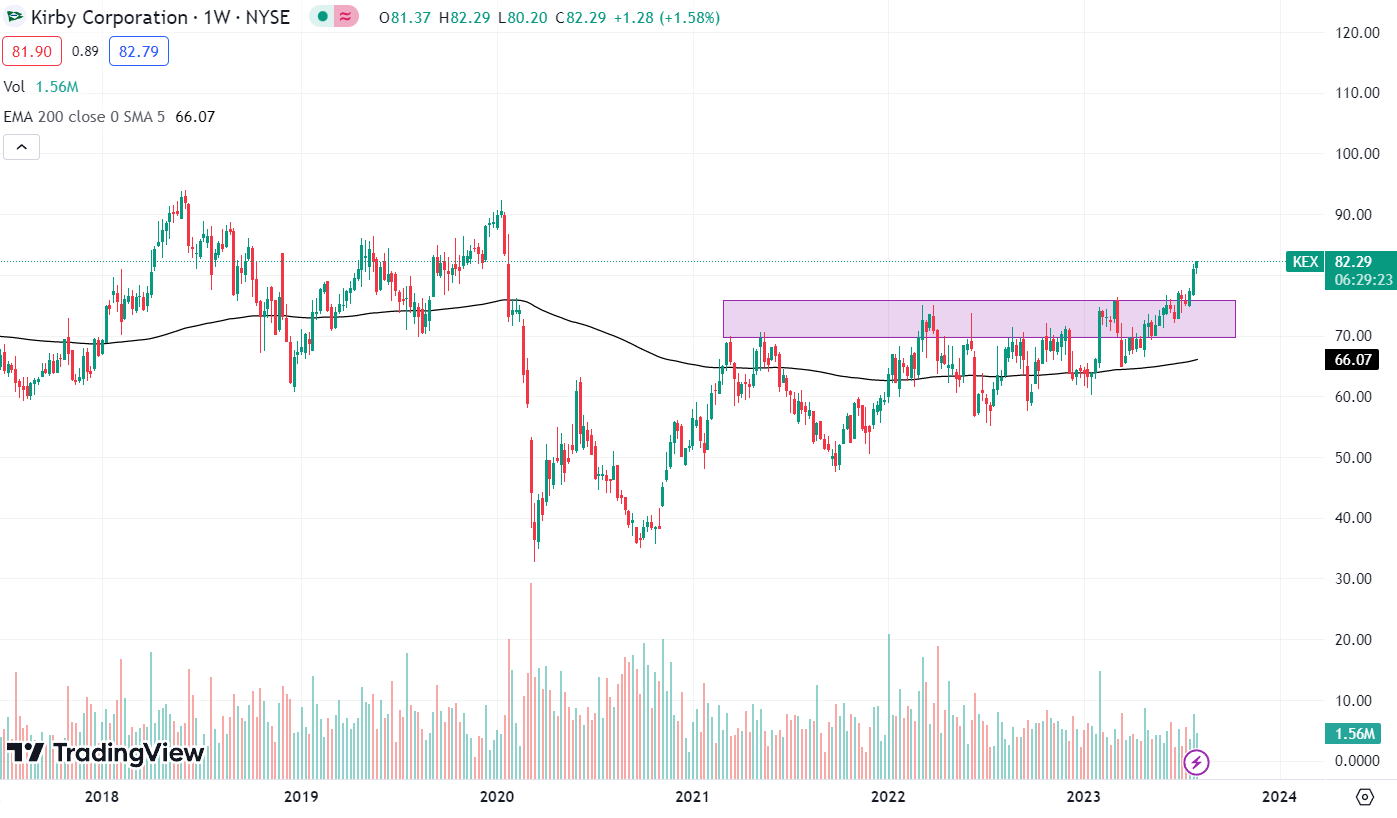

Technical Analysis

{kind=link}

KEX is trading at the $82.3 level. KEX delivered solid financial results as a result; its stock price increased by 10% in the last 15 days. In addition, the stock has recently broken out of an important resistance zone of $75, which the stock has been unable to break in the last 15 months. It shows that the stock is bullish and has great strength in it. But the ship has already sailed and is 10% above the breakout level. So I would advise not to invest at such high levels; instead, I would wait for the stock to come back to the breakout level of $75, and after the retest of the $75 level is done, then I would suggest investing in it. Because it would provide a better risk to reward trade, and retest of the breakout level increases the chances of the breakout being successful. Hence buying on retest will increase the chances of a breakout being successful, and it also seems a better option than investing at $82. Hence I assign a hold rating on KEX based on the technical chart.

Should One Invest In KEX?

First, talking about KEX’s valuation. KEX has a P/E [FWD] ratio of 22x which is higher than the sector ratio of 17.81x. KEX has an EV / EBIT [FWD] ratio of 21.92x compared to the sector ratio of 16.33x. Both the valuation ratios indicate that KEX is overvalued, and as I mentioned before that the stock price is 10% above the breakout level, and investing at higher levels is not what I would advise. Hence looking at the higher valuation and high price levels, I assign a hold rating on KEX for now.

Risk

The outdated infrastructure of the inland waterways could increase expenses and cause interruptions to KMT. The Company's operations depend heavily on maintaining the inland canal system of the United States. The system comprises more than 12,000 miles of commercially navigable waterways backed by more than 240 locks and dams that serve as flood control measures, keep pools of water at a specific level in certain parts of the country, and make interior river travel easier. The inland canal system in the United States is deteriorating, with more than half of the locks being older than 50 years. Due to the age of the locks, maintenance outages may therefore occur more frequently, causing delays and escalating operational costs. Currently, marine transportation businesses pay 35% of the cost of new construction and significant lock and dam rehabilitation through a 29-cent per gallon diesel fuel tax, while general government tax collections cover the remaining 65% of the cost of canal infrastructure and upgrading. The federal government's future ability to maintain and upgrade infrastructure would have an adverse effect on the Company's capacity to provide items for its clients on time. Additionally, any further user taxes that could be enacted in the future to pay for infrastructure upgrades will raise the Company's operating costs.

Bottom Line

I believe their financial performance in Q2 FY23 was quite impressive, and the stock looks bullish. But I believe buying at the retest level is more sensible than buying the stock at 10% above the breakout level. In addition, their valuation seems high; hence I assign a hold rating on KEX.

For further details see:

Kirby Corporation: Wait For Better Price Levels