KNX - Knight-Swift: Uncertain Macroeconomic Outlook Putting Pressure On Transportation Sector

2023-10-30 11:03:17 ET

Summary

- Knight-Swift's recent third-quarter results showed weak revenue growth and a substantial drop in operating margin.

- The Less Than Truckload segment showed resilience and promising performance, while the truckload sector faced challenges.

- The company's forward Price/Earnings ratio reflects its superior margins, but with limited potential upside, a hold rating is recommended.

Overview

My recommendation for Knight-Swift Transportation Holdings (KNX) is a hold rating. The most recent third-quarter results showed weak revenue growth, which was largely due to the ongoing difficulties in the transportation sector. Moreover, the company's operating margin saw a substantial drop, decreasing by more than half. While there are evident challenges in the truckload sector, the Less Than Truckload [LTL] segment has a silver lining, showcasing resilience and promising continued robust performance in the foreseeable future. It's worth noting that my previous rating for KNX was also a hold, and I am reiterating it.

Recent results and updates

KNX reported dismal results for the third quarter of 2023 . Without the fuel surcharge, revenue increased by 7.6%. With the fuel surcharge, it's 6.5%. In addition, adjusted operating income fell by a jaw-dropping 60.8% despite the increase in revenue. The negative $20.4 million impact on these results year over year can be attributed to rising interest costs. The non-reportable segment's third-party insurance business also saw a $22 million decline in operating income.

Included in the non-reportable segment are operations such as insurance and maintenance, equipment sales and rentals under the Iron Truck Services brand, equipment leasing, and equipment warehousing. Revenue for the division was down 14.2% from the same period a year ago. The company's efforts to resolve issues with its third-party insurance program, which included substantial cuts to exposure, were largely responsible for the decline.

A slight improvement from the previous quarter's $7.1 million operating loss was seen in this non-reportable segment's operating loss of $ 5.4 million . This improvement was due to better performance in other services, which provided a greater offset to the ongoing losses within the third-party insurance business. KNX is actively considering strategic options for the insurance business. To protect their business from the uncertainty caused by past losses, they are looking into reinsurance options for their current liabilities.

In addition, KNX faced a challenging truckload freight market in the third quarter. Spot rates were unsustainable because shippers' rate expectations hovered close to or even below operating costs. Late in the third quarter, instead of the usual seasonal build in truckload activity, KNX saw a continuation of the previous quarter's trend into early October. On the other hand, the LTL market demonstrated strength. Despite the robust performance of the LTL market, the truckload sector faced challenges marked by subdued demand and unviable spot rates, contrasting with the success of the LTL market. While there were glimpses of potential positive shifts in rates for the upcoming bid season, the immediate market landscape remained tough, especially for the truckload segment, due to depressed rates and weak demand.

The third quarter's earnings call provided insights into the market outlook for the remainder of 2023. The LTL market is poised for sustained demand, a trend attributed to recent disruptions in capacity. As the industry recalibrates over the coming months and as new contracts are negotiated at potentially higher rates, yield improvements are anticipated.

In addition, KNX is optimistic about having moved past the inventory destocking phase in the truckload arena. As they implement cost-saving measures, I anticipate a modest easing in cost pressures for the fourth quarter. Additionally, only a marginal rise in interest expenses is expected for the next quarter compared to the previous quarter.

"And we expect minimal increase in interest expense from Q3, assuming the rate hiking cycle is largely complete" source

Valuation and risk

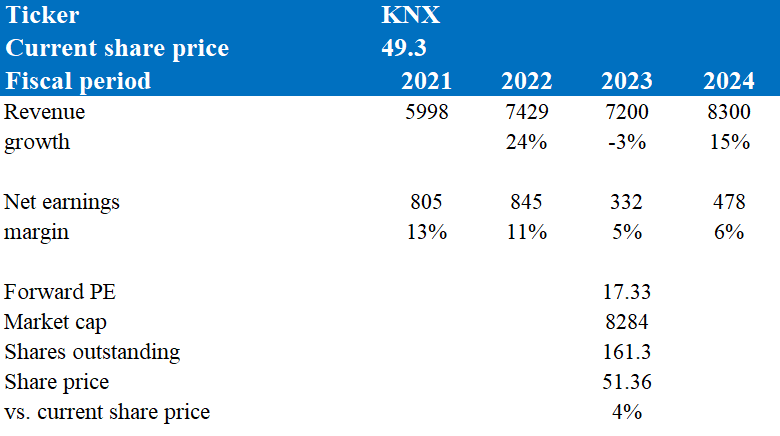

According to my model, my target price of KNX is ~$51 in FY24, representing a 4% increase. KNX third quarter results showcased certain challenges that justify a forecasted decline of 3% for FY23, which is in line with market consensus. The company reported weak revenue growth of 6.5% year-over-year vs. last year's same period of 15.5%. In addition, the adjusted operating income faced a notable dip, and this was primarily due to rising interest expenses and a decrease in operating income from the third-party insurance business. The non-reportable segment, which includes insurance and equipment-related services, encountered hurdles, especially within their third-party insurance program.

However, looking ahead to FY24, there are several indicators suggesting a potential 15% growth, which is in line with market consensus. The truckload freight sector, although currently facing headwinds with unsustainable spot rates, is expected to stabilize as the company moves past the inventory destocking phase and anticipates cost relief. More promisingly, the LTL market has shown robustness and is poised for continued growth, bolstered by recent industry disruptions. Given the resilience of the LTL market and the company's proactive strategies to address challenges in other segments, there's a strong case for a positive growth trajectory for KNX in FY24.

{kind=link}

Currently, KNX's forward Price/Earnings ratio is 17.33x, which exceeds the median of its peers at 13.46x. This higher ratio can be linked to KNX's superior margins relative to its peers. Specifically, KNX has an impressive EBITDA margin of 24%, surpassing the peer median of 19%. Additionally, with a net margin of 11.38%, KNX outperforms the peer median, which is at 6.4%. Given these factors, I believe that KNX's higher forward Price/Earnings ratio is, in my opinion, fair. However, with a mere potential upside of 4%, which doesn't offer substantial room for capital growth, I'm maintaining my hold rating on KNX, especially considering the challenges the transportation sector is currently grappling with, as discussed above.

{kind=link}

One upside risk to my hold rating on KNX could be the potential for a faster-than-anticipated recovery in the transportation sector. If the industry challenges are addressed sooner than expected or if there are positive macroeconomic shifts that boost demand for transportation services, KNX might benefit significantly. This could lead to improved financial performance and a potential re-rating of the stock, making my current target price seem low in hindsight.

Summary

KNX's third quarter 2023 results showcased a complex financial landscape. While there was growth in revenue when excluding fuel surcharges, the adjusted operating income saw a significant dip, influenced by increased interest expenses and challenges in the third-party insurance business. The non-reportable segment, covering activities like insurance and equipment services, also faced revenue declines due to challenges in their insurance program. On the market front, while the LTL sector showed resilience, the truckload sector faced headwinds with unsustainable spot rates and soft demand. The company's forward Price/Earnings ratio surpasses that of its peers, reflecting its superior margins. However, given the limited potential upside and ongoing challenges in the transportation sector, I maintain my hold rating for KNX until it sees a recovery in the transportation sector.

For further details see:

Knight-Swift: Uncertain Macroeconomic Outlook Putting Pressure On Transportation Sector