KTOS - Kratos Defense: Bullish Business Overvalued And 'Hold' Rating

2023-11-22 16:56:06 ET

Summary

- Kratos Defense & Security Solutions specializes in defense and security technology, serving the US Department of Defense and international security agencies.

- The company's diverse platforms include unmanned aerial vehicles, missile defense, and communication technology.

- Despite positive business prospects, the stock is considerably overpriced. Thus, on balance, I think a "hold" rating is appropriate for now.

- However, the fundamentals look great, and KTOS could be a great buy on dips if they happen.

Kratos Defense & Security Solutions, Inc. ( KTOS ) is a technological company specializing in the defense and security industry. With operations extending worldwide, KTOS develops cutting-edge national security and communication technology, delivering unmanned aerial vehicles, missile defense, and C5ISR. The US Department of Defense, international security agencies, and private clients are its customers. The company signed important contracts in 2023, and with its acquisition of Sierra Technical Services, it's well-positioned to benefit from unmanned aircraft. Still, my valuation model suggests the company's stock is excessively expensive, as well as other multiples-based relative valuation metrics. Hence, while I remain bullish on the company's fundamental business, its stock is considerably overpriced and a "hold" due to valuation concerns.

{kind=link}

Business Overview

Kratos Defense & Security Solutions was founded in 1994 with headquarters in San Diego, California. The company operates worldwide in countries outside the US, such as France, Germany, Norway, Canada, the UK, Israel, Singapore, Saudi Arabia, and Australia. KTOS develops innovative technology for national security and communication needs with approximately 2700 employees, a large percentage of them holding national security clearances. KTOS's customers are the US Department of Defense, other countries' national security agencies, and commercial clients.

KTOS delivers diverse platforms and systems for battlefield and communications: warfighter, unmanned space, training, Command, Control, Computers, Communications, Cyber, Intelligence, Surveillance, and Reconnaissance ((C5ISR)), sub-orbital vehicles, and research rockets. The warfighter readiness systems range from unmanned aerial vehicles ((UAVs)) to mixed reality training systems. The ISR-tethered drones are systems physically connected to a ground station for intelligence, surveillance, and reconnaissance. The space systems are virtual ground systems for reliable communications. The training systems use augmented, virtual, and mixed-reality technologies for immersive training solutions. The C5ISR systems support missile defense, space, and ground-based radar programs. The sub-orbital vehicles and targets include Aegis Readiness Assessment Vehicles ((ARAV)), solid rocket-based vehicles that emulate ballistic missile threats. Research rockets are developed as part of R&D programs to support the NASA Sounding Rocket Program to carry scientific instruments into space.

Source: Kratos's website

Kratos' Dual Dynamics: Unmanned Systems and Government Solutions

KTOS works in two specialized segments according to their focus and type of services: Unmanned Systems and Kratos Government Solutions ('KGS'). The Unmanned Systems segment comprises the aerial systems (Kratos UAS) and the Unmanned Control Systems. Kratos UAS concentrates on high-performance aerial target systems and advanced unmanned tactical aerial platforms. It also provides personnel to locations for aerial target-related missions. The UAVs segment includes tactical UAVs with a range of capabilities and prices. This segment also offers customized aerial target services and immersive training. The KTOS Government Solutions ((KGS)) segment encompasses a significant revenue contribution for the company, and it presents four divisions: Technology and Training Solutions ((TTS)) for network operations, consulting and learning; the Defense Engineering Solutions ((DES)) provides services for C5IRS; Weapons Systems Solutions ((WSS)) offers logistics and target operation support, rocket program services, and advance R&D; the Public Safety and Security ((PSS)) focuses on security and surveillance systems for government and commercial users.

Source: Kratos's website

However, one of the most exciting M&A developments for KTOS has probably been the acquisition of Sierra Technical Services. This acquisition positions KTOS well for the upcoming transition towards unmanned air vehicles, particularly aerial fighters. In fact, the Pentagon's Replicator initiative is poised to make 60% of carrier-based aircraft pilotless eventually. Moreover, I think this particular revenue vertical is still nascent but can certainly become a prominent revenue contributor for KTOS over time.

Lately, KTOS has secured several important contracts. First, on November 7, 2023, KTOS signed a contract with a ceiling value of $579M with the Space Systems Command to provide post-production development for the current Command-and-Control System Consolidated ((CCS-C) for military communication satellites. This work is expected to be completed May 30, 2032. On October 19, 2023, KTOS defense secured a $16.9 million contract for three UH-60M aviation trainers, with the US Army's Program Executive Office Aviation Utility Project Office being the end customer of the Australian Defense Force Rotary Wing Aircraft Maintenance School.

Valuation Analysis

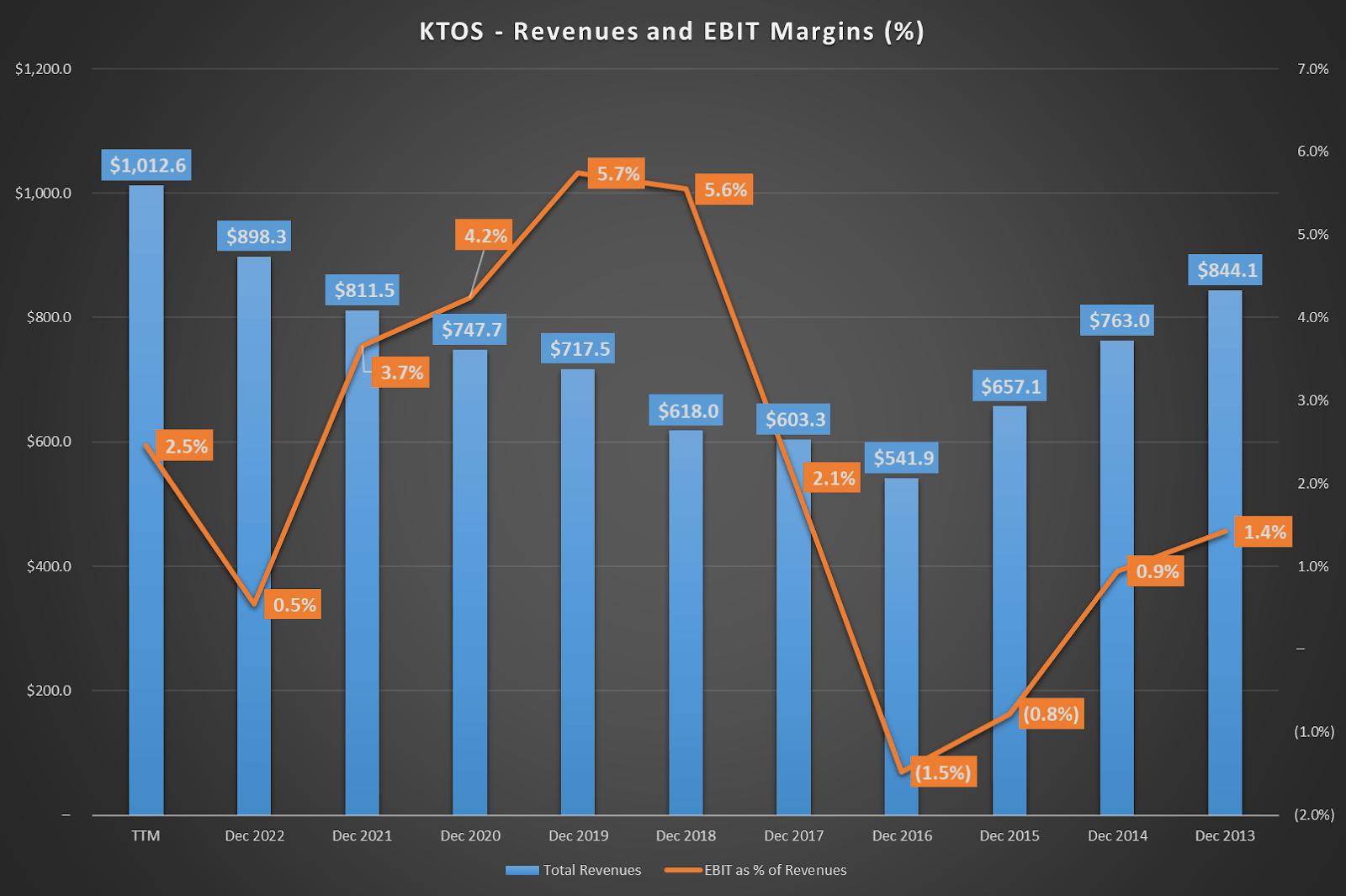

From a valuation perspective, KTOS's revenues have increased significantly since 2016. This has been mostly due to the solid demand for drone solutions but also because of the intensifying conflicts across the world. Moreover, defense spending has increased over that time and has become a significant tailwind for KTOS's operations.

{kind=link}

It's also important to note that while the company's overall revenues have increased at a CAGR of 1.8% since 2013, the revenue mix of KTOS doesn't have the same pace. Concretely, KTOS's Unmanned Systems quarterly revenues increased 13.4% YoY. However, Kratos Government Solutions quarterly revenues grew by 22.0% YoY. The latter makes up 79.4% of KTOS's total revenues, meaning the quarterly growth rate is 20.1% YoY. This is key because it seems that KTOS is in a cyclical upswing, likely due to the increased wars seen across the globe. However, it's likely that over the long run, KTOS's revenues will grow at the global aerospace and defense forecasted CAGR of 7.5% until 2027. With that in mind, I'll use the analyst forecasts for KTOS's 2023 and 2024 revenues and taper down that growth rate to the overall sector's CAGR by 2027. In fact, note that I'm forecasting higher full-year revenues for 2023 than the company's guidance of roughly $1.0 billion .

Moreover, EBIT margins are trickier because, as shown in the figure above, they've been volatile since 2013. However, on average, KTOS's EBIT margins have been roughly 2.2% since 2013, reaching 5.7% in 2019. Thus, I think it's reasonable to taper down my model some, for EBIT margin improvement by 2027 in the valuation model as well. I assume a gradual EBIT margin improvement towards 5.0% EBIT margins by 2027. Finally, I simply used the historical D&A , CAPEX , and NOWC margins, as well as a flat 21% tax assumption.

Author's elaboration.

However, the company's valuation appears excessive even under relatively favorable revenue growth rate assumptions and EBIT margins. This aligns with relative valuation multiples that signal that KTOS is significantly overvalued. My numbers suggest KTOS has a 67.3% downside potential from the current levels, which is significant and implies a $6.14 intrinsic value per share. Naturally, if the market thinks global conflicts will remain and even intensify, KTOS should have some premium due to its strategic importance. Nevertheless, it seems it's an excessive premium and already factoring in several favorable assumptions. So overall, I think it's prudent to reign in the bullish thesis on KTOS at this time, mainly due to its valuation concerns.

Conclusion

Overall, it's undeniable that the market is pricing KTOS as the next big thing in the defense sector. Indeed, unmanned vehicles are likely the future, and the Pentagon has already showcased a commitment to making that shift. Moreover, conflicts such as the war between Russia and Ukraine have shown that cheap unmanned drones can take out heavy armored tanks and infantry , as well as other artillery , thus marking a strategic shift in modern warfare. As such, KTOS should have favorable tailwinds supporting its revenue growth for years to come because the future of war favors drones and, by extension, KTOS's operations. However, ignoring that the stock trades at an excessive valuation is difficult. Naturally, revenues can quickly jump up with big government contracts, a potential wildcard for the upside. However, if KTOS's historical revenue growth and sector growth indicate the future, then it appears it's overvalued at current levels. Thus, while I remain bullish on the company's fundamentals, I think the stock's price is ahead of itself, giving it a "hold" rating on balance.

For further details see:

Kratos Defense: Bullish Business, Overvalued, And 'Hold' Rating