KTOS - Kratos Defense & Security: Steller Performance Comes At A Price

2023-09-07 11:48:20 ET

Summary

- Kratos Defense & Security offers cost-effective combat drones that enhance the capabilities of manned fighter jets.

- The company has shown progress in its Tactical Drone segment and has potential support from the Air Force.

- Kratos reported an impressive Q2 2023 and has a diverse backlog and bid proposal pipeline, indicating future growth opportunities.

- Despite positive operational metrics, Kratos appears overvalued compared to Aerospace and Defense peers.

Kratos Defense & Security (KTOS) presents an intriguing investment proposition, particularly for those looking to tap into the Department of Defense's evolving priorities. With the military's increasing importance and right-sizing budgets, there's a demand for cost-effective solutions. Capitalizing on this trend, Kratos offers affordable systems, predominantly seen through its combat drones. These drones can enhance the capabilities of manned fighter jets while being significantly more cost-efficient. The company has shown notable progress within its Tactical Drone segment, garnering attention, and potential support from the Air Force.

Kratos stock price is up 55% year-to-date as investors anticipate future financial and operational success. However, when assessing Kratos's stock valuation, much of this forward momentum and anticipated growth is already embedded in its current price.

Company Overview

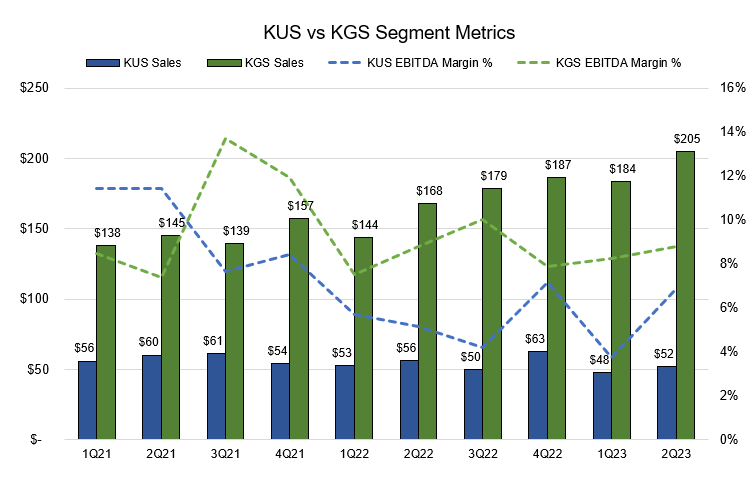

Kratos Defense & Security is a defense-oriented company operating predominantly as a primary contractor and subcontractor to the Department of Defense (DoD). The company's primary area of expertise lies in satellite communication systems. It functions in two main segments: Kratos Unmanned Systems (KUS) and Kratos Government Solutions ((KGS)).

{kind=link}

In the KUS segment, Kratos is an industry leader in manufacturing target drones, essentially used for target practice by fighter jets and missile defense mechanisms. This segment sees a high level of vertical integration, only outsourcing engines and parachutes for its drones. The KUS segment, established as a standalone segment in 2014, has witnessed minimal profit. This is largely attributed to ongoing investments in fresh unmanned offerings, implying a potential for future revenue growth. The core of KGS is satellite communications, accompanied by capabilities in command and control, signal intelligence, RF identification systems, and electronic warfare. Despite the KUS segment's growth potential, KGS is Kratos's primary revenue driver, accounting for 75% of the company's revenue and nearly 80% of its profit in 2022.

Kratos boasts a 3,600-strong workforce, mainly skewed towards engineering and technical roles. A significant portion of these employees are security-cleared, indicating the sensitivity and importance of their projects. The company's customer base predominantly revolves around National Security agencies, but its satellite communication vertical also caters to commercial markets. Kratos emphasizes technological innovation and intellectual property, striving to lead and be the first in the market across its core areas of expertise. This forward-thinking approach aligns the organization with future market trends and opportunities.

Q2 2023 Earnings Recap

Kratos Defense & Security reported an impressive Q2 2023 , positioning itself favorably to meet its financial goals for the year. The stock's positive performance post-earnings is a testament to this. The company is actively progressing in several areas, promising long-term growth. Their combat drone, Valkyrie, is undergoing significant tests as the Air Force proceeds with its Collaborative Combat Aircraft ((CCA)) effort. Additionally, management commented on notable advancements in hypersonic ((ZEUS)) and satellite ground controls (OpenSpace).

From a financial standpoint, Kratos reported Q2 consolidated bookings of $281.9 million and a 1.1 book-to-bill ratio. The consolidated backlog stood at $1.16 billion, a marginal increase from $1.13 billion in the prior quarter. The $1.16 billion is comprised of a funded backlog of $863.9 million and an unfunded backlog of $293.4 million. Kratos has a record backlog and a bid proposal pipeline of $10 billion. This pipeline encompasses hypersonics, space, propulsion systems, satellite communications, and drones, showcasing the company's diverse opportunities. Given the nature of long-term contracts, Kratos backlog provided visibility into future cash flows and revenues. The company expects to recognize 56% of the total backlog as revenue in 2023,

From an operational standpoint, Valkyrie achieved a major milestone by completing a simulated three-hour combat mission for the Air Force using the Skyborg AI capability. Concurrently, Kratos's Rocket Systems ventured into hypersonics by successfully launching a new payload and conducting a static fire test for the Zeus 1 rocket motor. Upcoming tests for the Erinyes and Dark Fury hypersonic vehicles indicate Kratos's commitment to this domain, expecting it to be a substantial growth catalyst.

Company Reports

Guidance for FY23 remains unchanged in terms of sales and adjusted EBITDA. However, there's growing confidence in these projections, with Q3 anticipated to mirror Q2 and Q4 expected to see an uptick due to seasonal strength and profitable OpenSpace software sales. Management is optimistic about sustaining its organic growth, forecasting consecutive annual growth in revenue, EBITDA, and cash flow without major acquisitions in the pipeline.

Risks

Investing in Kratos Defense & Security comes with a set of potential downside risks that potential shareholders should be aware of:

- Customer Risk: A significant portion of Kratos's revenue is derived from the U.S. Government. In 2022, the U.S. Government contributed to 70% of the company's total revenues. Any changes in the U.S. Government's fiscal policies or budgetary constraints could adversely impact Kratos's revenue stream and overall financial health.

- Execution Risk: The company faces uncertainties related to scaling up its production. Particularly in the Unmanned segment, Kratos has not previously produced target drones at the current pace, and the company has yet to venture into making combat drones on a large scale. Thus, the capacity to maintain or improve margins in this area needs to be proven and can be seen as an execution risk.

- Operational Risk: One of the significant challenges that Kratos encounters is sourcing and retaining qualified personnel capable of executing both existing and forthcoming program awards. This includes individuals willing and qualified to secure National Security Clearances. The increased costs associated with hiring such individuals add to the operational challenges. Addressing these challenges is a collective effort, with all Kratos's business units collaborating closely.

- Competition Risk: Kratos operates in highly competitive markets, facing fierce competition for contract acquisitions. Competitors range from mid-tier federal contractors with niche capabilities to large-scale defense contractors and IT service providers. Competition could intensify due to various factors, including the emergence of new competitors, industry consolidations, or a decrease in the total number of government contracts available. Additionally, there's a risk from prime contractors for whom Kratos currently serves as a subcontractor. These prime contractors might opt to provide services that Kratos now offers, essentially becoming competitors. Moreover, existing subcontractors to Kratos may seek to elevate their status to prime contractors on contracts, further intensifying competition.

Valuation

Kratos appears to be overvalued when compared to other Aerospace and Defense peers. Despite being a small-cap company, Kratos trades at a similar forward EBITDA multiple as Heico (HEI), which is almost ten times more enterprise value. The smaller aerospace names trade at a forward EBITDA multiple from 9x-15x, while Kratos trades at nearly 23x.

Capital IQ

Translating to more tangible terms, if Kratos were to trade at the peer median multiple of 15.26x, its implied enterprise value would be around $1.53 billion. Accounting for cash and short-term investments of $50 million and deducting total debt of $340 million, we would be left with an implied equity value of approximately $1.24 billion. About 128 million shares are outstanding, resulting in an implied share price of $9.68. This implies a 60% premium compared to its current share price of $15.53.

In conclusion, Kratos offers an enticing investment opportunity as it aligns with the Department of Defense's emphasis on cost-effectiveness. The company's strides in combat drones and satellite communication solidify its standing in the defense sector. However, Kratos is trading at a significant premium to its Aerospace and Defense peers, especially considering its relatively low EBITDA margin. Investors should exercise caution and scrutinize the reasons for Kratos's elevated valuation, especially considering that its price is trading at a premium.

For further details see:

Kratos Defense & Security: Steller Performance Comes At A Price