KTOS - Kratos: Funding Window Open To Unlock Long-Term Risk Capital Rate Buy

2023-09-07 08:17:45 ET

Summary

- Defense contractor Kratos Defense & Security presents compelling value despite high multiples and an extensive backlog to work through.

- Accelerated demand in space and satellite communications is driving growth in Kratos' satellite business.

- KTOS has a deep pipeline of proposed orders and is increasing drone production, indicating confidence in securing contracts and financing.

- Incremental gains in profitability are attractive. Net-net, rate buy.

Investment briefing

Defense contractors have opened up a funding window to unlock long-term risk capital in FY'23. Multiple names have caught a strong bid on U.S. indices, with some exceptional issues on offer at the time of writing. Within this list, there are selective opportunities that have differentiated, and insulated offerings as part of their core business model. Kratos Defense & Security ( KTOS ) is one such name in my informed opinion, and we've had the name in our long account since May this year.

This report will unpack some of the moving parts in the KTOS investment debate, linking this back to the broader buy thesis. Net-net, there is compelling value to be realized in owning KTOS, despite 1) the multiples it sells at, and 2) the company's extensive backlog it still has to work through. Measures of KTOS' compounding value imply the company has plenty of growth upside to be priced in at current market values, supporting a bullish rating. Net-net, rate buy.

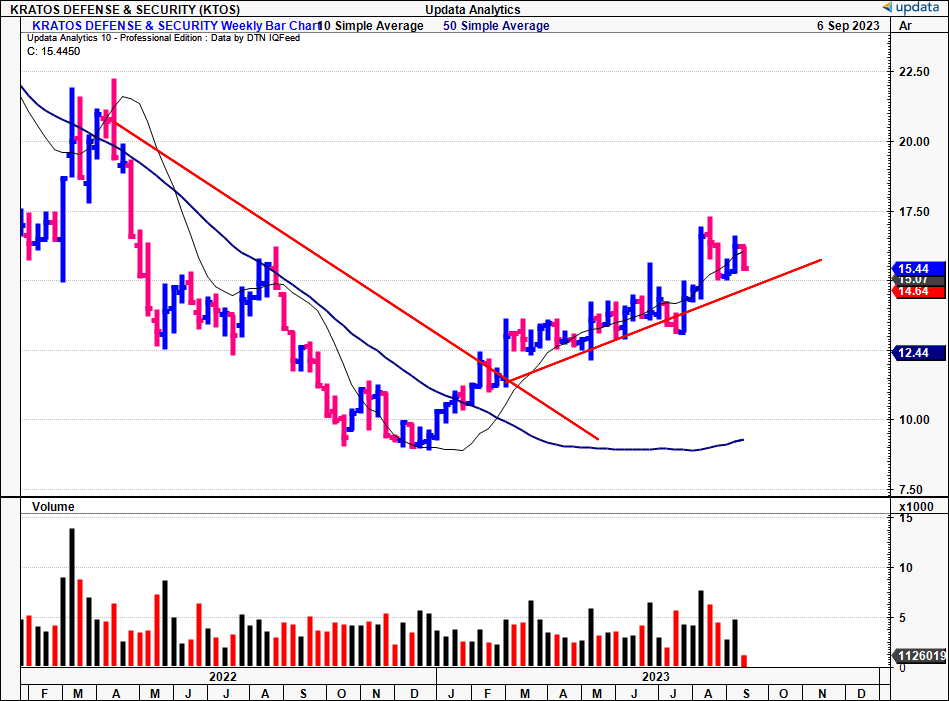

Figure 1. KTOS weekly price evolution, 2022 - date

{kind=link}

Critical facts underpinning buy thesis

Three critical facts underscore the buy thesis presented here:

- Accelerated demand in space and satellite communications

The company's core business in space and satellite communications has ramped up heavily this year, including its software-based OpenSpace virtualized Command and Control ("C2"), and its telemetry, tracking, and control ("TT&C") subsystems, and ground system products.

The proliferation of satellites in what's known as low Earth orbit, medium Earth orbit, and geostationary Earth orbit, is driving demand for KTOS' satellite business for both commercial and national security markets.

- Investment in 'Space Domain Awareness' ("SDA")

The company has also invested in, and independently funded, its global SDA network , which plays a crucial role in monitoring space-based radio frequency signals. This provides essential information about satellites and other objects in orbit. KTOS' SDA network is currently spread across over 20 global sites, and houses ~150 fixed and steerable radio frequency sensors. These have the capacity to detect and track vehicles, and objects within space vehicles, then relay the data in real-time back to KTOS' customers.

- Deep pipeline of proposed orders and increasing backlog

KTOS has ramped up drone production this year and is re-centring on domestic manufacturing. The company intends to produce ~150 jet drones within the U.S. this year, including its Targets, Valkyrie, Mako, Air Wolf offerings. In my view, the Valkyrie unmanned air vehicle, the Valkyrie XQ-58A, is the most exciting prospect with the most attractive economics involved. I'd also point out the company is aiming to double its annual drone production to c.300 units within the next 18 months. This tells me that 1) it is confident in securing contract wins to fulfil this, and 2) it has the financing (either internal or external) to finance these developments.

1. Q2 FY'23 insights - $10Bn in the pipeline, backlog growing, cash flows strong

KTOS put up Q2 revenues of $256.9mm , up 14.6% YoY, on a gross margin of 25%. It pulled in $14.6mm in core EBITDA on this. Critically, the company's revenue growth was underscored by a diversified portfolio of contract pricing, with fixed price contracts making up 67%, cost-plus contracts making up ~27%, and time and material contracts representing 6%. Around 69% of the total revenue clipped in Q2 stemmed from contracts with the U.S. government, including the Department of Defense ("DoD"), other Federal Government Agencies, and foreign military sales ("FMS") contracts.

Its Kratos Government Solutions ("KGS") business was a major revenue driver, booking a 17% gain in turnover. Upsides were observed across most of the portfolio, including space and satellite, turbine technologies, microwave products, and Command, Control, Communications, Computers, Cyber, Intelligence, Surveillance, and Reconnaissance ("C5ISR"). Excluding the impact of its SRE acquisition , core business growth was still a firm 10.7%.

The CFO didn't mince words on the call as to the origins of growth:

It [growth] was organic growth literally in every business unit within KGS across the board. Space satellite training, C5ISR, microwave products, turbine technologies, air and defense rocket, all across the board."

Further disaggregation of the company's top-line includes the following:

1. Booking and Backlog

KTOS reported a book-to-bill ratio of 1.1 in Q2 and consolidated bookings of $281.9mm by the end of the quarter. As a reminder, a ratio >1 is preferred, indicating order volume is higher than goods shipped. As far as demand-pull goes, this is the kind of dynamic you want. For the TTM, it was $1.07Bn on a book-to-bill of 1.1 as well. For its unmanned systems business, it was even higher at 1.2. KTOS' backlog tallied $1.16Bn by the end of June, a sequential growth from $1.13Bn in Q1. I'd note here that the backlog comprises a funded value of ~$864mm, and unfunded commitments of $293.4mm.

But most critically, the company's proposal pipeline was $10Bn by the end of Q2. This is a record for the company and represents immense value in my opinion. Moreover, management is equally as bullish on the opportunity this presents. Per the CEO: " We are in my opinion...three or four years ahead of the competition...". I'd also point out that lead times on its Valkyrie unmanned stealth fighters are currently at ~15 months due to the engine. So to work through its backlog won't be at lightning speed, but the $10Bn proposal line cannot be overlooked in my view.

2. Customer Base and Workforce

Crucially - as mentioned a little earlier - KTOS has diversified its customer base this YTD. This has transposed to immediate positives. Around 11% of the Q2 top-line came from commercial customers, 20% from foreign orders. Hiring and retention of skilled technical labour has also been a key challenge faced by KTOS these past few years. To this point:

- It has brought 37 new employees onto its C5ISR headcount since the end of 2022.

- This includes 18 new hires during Q2 plus another 12 recently went through pre-hiring.

- The total increase in headcount since 2022 is 152, and it had 3,797 staff on the books by the close of Q2.

This gets you to revenue per employee of $67,685.0 for the quarter ($270,700 annualized).

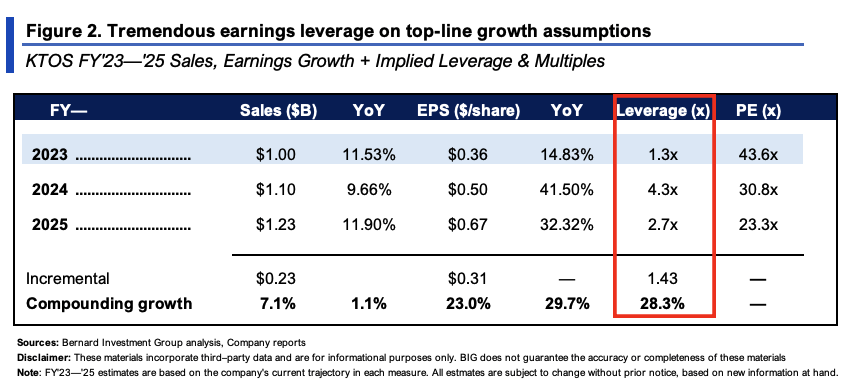

Given the momentum YTD, management revised guidance higher for Q3, and now calls for ~5-13% YoY growth from Q3 FY'22. It looks to $980mm-$1Bn in sales by yearend. In my eyes, it could to $1Bn in FY'23 sales at this run rate, and spin off $20-30mm in cash after ~$50-80mm in CapEx towards its main programs. I'd see $0.50 in earnings by FY'24 on this trajectory. Critically, based on these growth assumptions, the potential earnings leverage is extraordinarily significant - I get to 1.3x in FY'23, stretching up to 4.3x by FY'24. That implies for every new $1 in revenues, KTOS could produce $1.30-4.30 in earnings over the coming 2 years.

{kind=link}

3. Collaborative breakthroughs with Valkyrie

KOTS' partnership with Shield AI - who is aiming to "build the world's best AI pilot - is an important milestone to the growth of its tactical drones business. The collaboration involves the integration of Shield's AI technology into KTOS' Valkyrie XQ-58 drone. Shield AI has already developed an AI pilot that's been deployed in combat scenarios. This AI pilot has demonstrated its capabilities by flying on a variety of platforms, including 1) a quadcopter, 2) its own manufactured Group 3 unmanned aircraft system (called the V-BAT ), and 3) a modified F-16 fighter jet. In my view, the collaboration adds to KTOS' offering and could potentially reduce average lead times for its Valkyrie's pipeline.

Secondly, the United States Air Force's ("USAF") successful completion of a historic 3-hour test flight marked the first-ever flight where AI agents and algorithms controlled the Valkyrie drone. The flight was done at the Eglin Test and Training Complex in Florida in August. Hence, you're looking at Valkyrie gaining considerable traction, and the test flight only corroborates the unmanned units heading into combat sometime in the near future.

2. Valuation

The stock sells at exorbitant multiples - 43x forward earnings; 26x forward EBITDA. Both are >100% premiums to the sector. The premiums are indeed noted, but a more thoughtful analysis is required.

KTOS is ploughing as much capital as it can back into the business to expand operations, that much is true. It invested another ~$11mm in CapEx into its core programs in Q2, around 1x the quarterly average from 2020 to that point. Since late 2020, it has put a total of $286mm of new capital commitments to work into its operations, including CapEx, acquisitions and purchase of intangibles.

Critically:

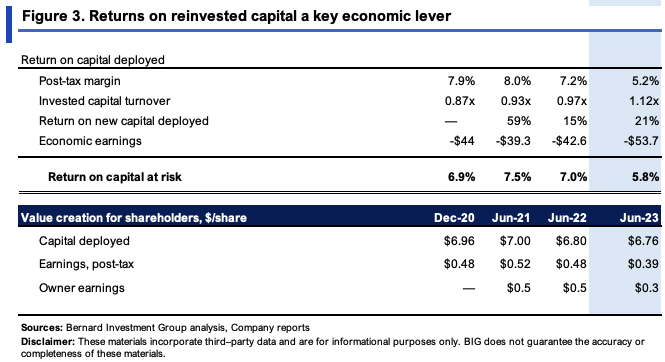

- Its existing investments return ~6-7% on a rolling TTM basis, not the most exciting numbers or value proposition [Figure 3]. This was ~$50mm trailing NOPAT produced on ~$1.2Bn capital at risk (see notes in figure 3).

- But the key thing is this - the company is ratcheting up incremental investments on a rolling basis as well. Growth in incremental profits is running concurrent to this. This is where the value is seen.

- Looking at Q2 FY'21-'23, the return on new capital deployed has scored double-digits each period, at 21% trailing return in Q2 '23.

This is telling. For one, the new investments are more profitable than the 'legacy capital' put at risk. Secondly, it squares off with the economics of the business - the firm's pipeline and backlog grow, so it deploys more cash into fulfilling demand and expanding operations. Third, it's precisely what we want to see . We want KTOS' new inventories/orders to be driving incremental profitability. We want the new orders to turnover capital at higher rates (1.12x last quarter). We also want the incremental returns on investment to be reinvested back into meeting more demand - true capital recycling, and a robust economic flywheel.

Note: Net operating profit used in these calculations are equated with 100% of R&D and full amortization charge added to earnings before interest and tax. These are then capitalized on the balance sheet and amortized in a straight line over a 7-year useful life. ( )

{kind=link}

So the company trades at trailing ~45.8x EV/NOPAT as I write (2,290/50 = 45.8x). It also grew post-tax earnings 21% off ~$16mm of net new investment (CapEx plus working capital changes). It would theoretically need to put another $16-$25mm to see these incremental returns again by FY'23, and my estimate is that it will, and can do this going forward. Management guide to $50mm in CapEx this year, calling for $31.3mm in H2 just to hammer this in. At 21% profit growth on the capital reinvested, this gets you to $55.40mm in NOPAT (50x1.21 = $55.4), and presuming the same 45.8x multiple, implies an EV of $2.54Bn or $19.80/share. (45.8x55.4 = $2,540) At the current share price, this is a 27% value gap, and wide margin of safety. This supports a bullish view.

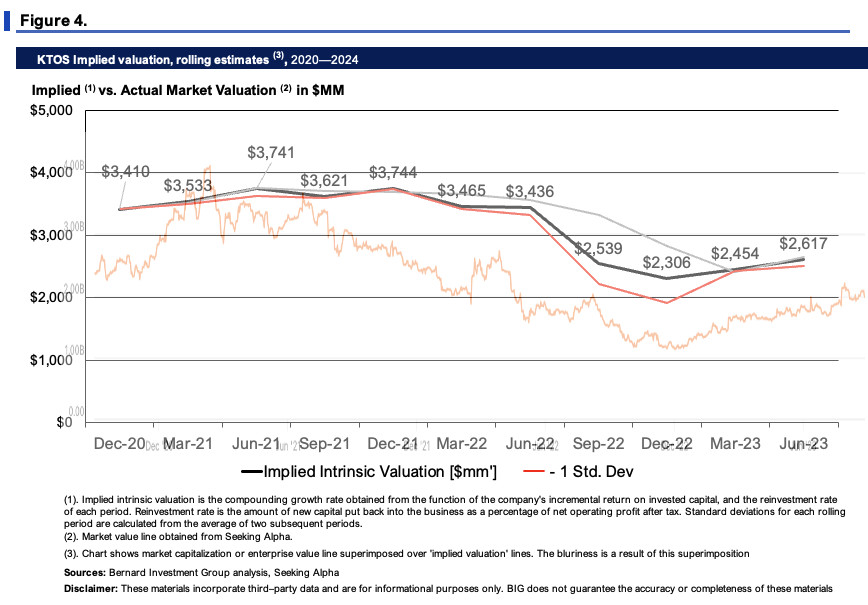

A firm can compound its intrinsic value at the function of its incremental return on investments and what amount it actually reinvests at these rates. Applying the calculus to KTOS' equity line throws off an implied market value of $2.6Bn, in line with the figures described above and a 30% value gap. You can see the gap in market value to implied intrinsic value in Figure 4. Both factors support a buy rating in my view.

{kind=link}

In short

Net-net, there are multiple economic levers KTOS is pulling within its growth arsenal right now. Major contract wins, key partnerships, and evidenced demand for its products are three points to consider. It is also recycling profits earned on capital invested back into growing the business and meeting order demand. The stock is pricey on a relative basis, sure. But the key is identifying gaps in price and value. Based on the firm's economic characteristics, it looks comprehensively undervalued and my assumptions have it priced at $2.54-$2.6Bn, 27-30% value gap at the time of writing. Further updates will be provided along the remainder of FY'23. Rate buy.

Risks to investment thesis:

Investors must realize the following risks in full:

- The stock sells at high relative multiples/valuations. This may play some role in the forward pricing of the company's market values.

- Macro-headwinds are also worth mentioning, and could potentially play a role in obtaining parts, components and the likes. It could also slow down order growth for the company.

- Further geopolitical changes could result in policy changes that slow the progress of the company's top-line and order growth.

Investors should recognize these risks in full prior to making any investment decisions.

For further details see:

Kratos: Funding Window Open To Unlock Long-Term Risk Capital, Rate Buy