CA - KYN: One Of The Highest-Yielding Energy Infrastructure Funds Around

2023-09-26 02:30:49 ET

Summary

- Kayne Anderson Energy Infrastructure Fund specializes in investing in energy infrastructure companies, which enjoy stable cash flows regardless of the broader economy.

- The fund's performance has lagged behind the Alerian MLP Index, but it delivers high direct payments to shareholders, which may not be reflected in price performance.

- The fund's largest holdings are stable companies focused on natural gas, and it employs leverage to boost returns, but at a reasonable level.

- The fund currently boasts a 9.61% yield, which was fully covered over the past eighteen months.

- The fund is currently trading at a very attractive discount on net asset value.

Kayne Anderson Energy Infrastructure Fund, Inc. ( KYN ) is a closed-end fund that specializes in investing in energy infrastructure companies. This is a category of company that we regularly discuss here at Energy Profits in Dividends, as it includes things like midstream companies, liquefied natural gas producers, and most master limited partnerships. One of the nicest things about all of these firms is that they typically enjoy remarkably stable cash flows regardless of the conditions in the broader economy. This is actually a pretty good place to be right now, as we are seeing increasing signs that consumers are financially pinched, and crude oil and natural gas prices are positioned to increase over the coming months.

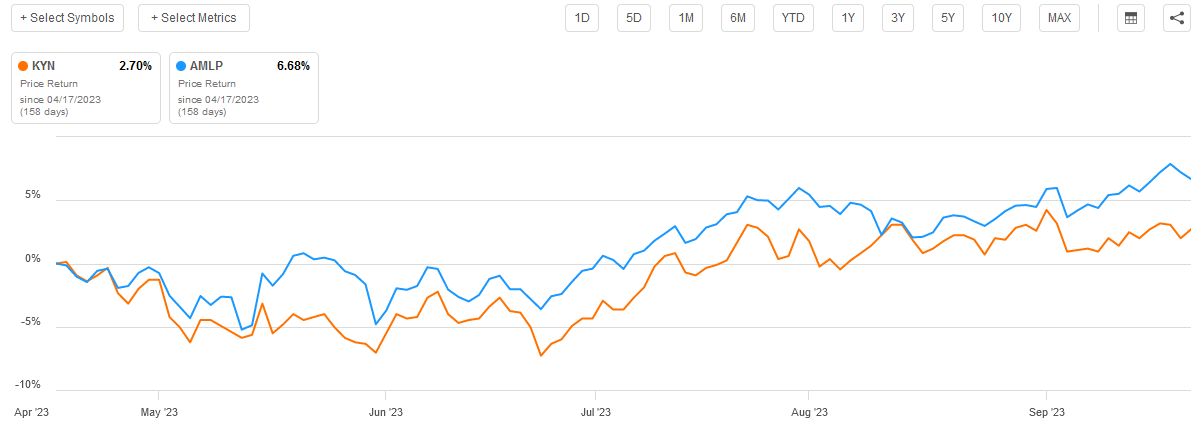

We last discussed the Kayne Anderson Energy Infrastructure Fund in April. Its performance has left something to be desired since that time. While the shares have gone up, they have lagged behind the Alerian MLP Index:

{kind=link}

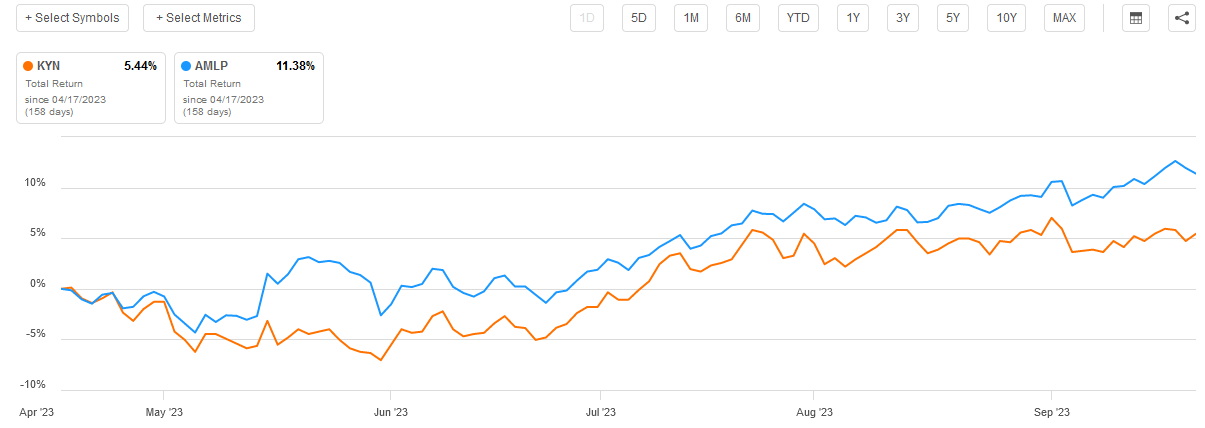

However, as I have pointed out in previous articles, midstream companies tend to deliver a high proportion of their returns in the form of direct payments to shareholders. This naturally still puts money in the shareholders' pockets, but it will not be reflected by looking at the fund's price performance. As such, the better metric to use to judge the fund's performance over time is total return. Unfortunately, here the Kayne Anderson Energy Infrastructure Fund still does worse than the Alerian MLP Index:

{kind=link}

This is disappointing, but as we discussed before, the Kayne Anderson Energy Infrastructure Fund does have some advantages over the Alerian MLP Index. These advantages could become even more pronounced now that the merger between ONEOK ( OKE ) and Magellan Midstream Partners ( MMP ) is apparently going through, as it will remove yet another master limited partnership from the universe of companies that can be contained in the Alerian MLP Index.

About The Fund

According to the fund's webpage , the Kayne Anderson Energy Infrastructure Fund has the primary objective of providing its investors with a high level of after-tax total return. As is frequently the case, the fund's website provides a more detailed objective:

[The fund's objective is] to provide a high level of after-tax total return with an emphasis on making cash distributions to stockholders. KYN intends to achieve this objective by investing at least 80% of its total assets in securities of Energy Infrastructure Companies.

The focus on after-tax total return is a fairly common objective for energy infrastructure funds, so this is not particularly surprising. We note though the fact that the fund's description does not specify any particular type of securities that the fund may invest in, only that they be issued by an energy infrastructure company. These companies have issued a variety of securities over the years, including common equity, preferred equity, and bonds. This fund invests pretty much exclusively in common equity, however:

CEF Connect

This allocation is almost identical to what we saw the last time that we discussed this fund, which is not especially surprising. After all, the Kayne Anderson Energy Infrastructure Fund only has a 28.20% annual turnover, so it does not change its assets very often. The fund's description does imply that it could change its allocation to favor preferred stocks and bonds should the situation warrant such. It seems unlikely that this would ever be the case, however. As I pointed out in a previous article , there is almost no reason for an energy infrastructure fund to invest in either preferred stock or bonds:

The high yield on the common equity in most cases gives master limited partnerships a higher yield on the common equity than on the preferred. In such an environment, it makes no real sense for a fund seeking total return to purchase the preferred equity over the common equity. After all, the common equity has a higher yield and significantly better capital gains potential so it will almost always be the higher returning instrument. The only real reason to purchase the preferred is that the preferred equity will be somewhat less volatile than the common equity. This could be advantageous during certain circumstances but generally, the common equity of midstream companies has reasonably low volatility. In addition, the preferred equity is theoretically safer in a bankruptcy or forced liquidation scenario. However, in most bankruptcy situations, the assets of the company are insufficient to cover all of the debt so both the common unitholders and the preferred unitholders will get wiped out.

While the above quote does specifically refer to master limited partnerships, it generally applies to midstream corporations as well. The difference is somewhat less pronounced though because midstream corporations usually have somewhat lower yields than master limited partnerships. For example, here are some of the major midstream corporations and their yields:

| Company |

| Current Yield |

| Enbridge Inc. ( ENB ) |

| 7.60% |

| Pembina Pipeline Corporation ( PBA ) |

| 6.52% |

| Kinder Morgan, Inc. ( KMI ) |

| 6.81% |

| The Williams Companies, Inc. ( WMB ) |

| 5.32% |

The Alerian MLP Index yields 7.90% right now, so it clearly exceeds the yield of all of these companies. This is, admittedly, one reason why I am not a particularly big fan of the trend of master limited partnerships converting into corporations over the past few years.

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing midstream companies and other energy infrastructure firms here at Energy Profits in Dividends and on the main Seeking Alpha site. As such, the largest positions in the fund will probably be familiar to most readers. Here they are:

Kayne Anderson

I have discussed all of these companies except for Western Midstream Partners ( WES ) at some point in the past. Thus, they all should be reasonably familiar to most regular readers. This is good, because the fundamentals of all of these companies are quite strong. We also see a marked preference towards those companies that are more heavily focused on natural gas than on crude oil. As I pointed out in a previous article, the fundamentals of natural gas are stronger than the fundamentals of crude oil so this should put the fund in a good position for growth going forward. In order to understand why, we have to consider the business model that is used by midstream companies. I provided a brief summary of this model in another article:

In short, the company enters into long-term (typically five to ten years in length) contracts with its customers. Under the terms of these contracts, the midstream company moves a customer's natural gas, natural gas liquids, and crude oil through its network of pipelines and other infrastructure. In exchange, the customer compensates the midstream company based on the volume of resources that are transported.

Thus, as the global demand for natural gas increases going forward, midstream companies should see a higher volume of natural gas moving through their infrastructure. After all, the United States is one of the few countries that have sufficient natural gas reserves to increase its production by any significant degree to meet growing demand. These resources will need to be transported from the oil and gas fields where they are produced to the market where they can be sold, which will result in higher midstream volumes. As midstream volumes correlate with cash flows, this should boost the cash flows of most of the companies in the portfolio.

As some readers might point out, Cheniere Energy ( LNG ) and Sempra Energy ( SRE ) are not midstream companies. Cheniere Energy is a producer of liquefied natural gas, which should position it well for growth as the demand for liquefied natural gas grows. Cheniere Energy also sells its products under long-term contracts that provide it with a great deal of stability regardless of changes in energy prices. Sempra Energy should also prove to be relatively stable due to its status as a utility provider of natural gas. Overall, then, we see that all of the companies that are included in this fund's largest holdings should be relatively stable over time.

Leverage

As is the case with many closed-end funds, the Kayne Anderson Energy Infrastructure Fund employs leverage as a means of boosting its effective returns and the yield of its portfolio beyond that provided by the assets themselves. I explained how this works in my previous article on the fund:

Basically, the fund borrows money and then uses that borrowed money to purchase partnership units of midstream companies. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As a result of this, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for that reason.

Fortunately, the Kayne Anderson Energy Infrastructure Fund meets our requirements with respect to its leverage. As of the time of writing, the fund's levered assets comprise 22.50% of its portfolio, which is in line with the levels possessed by most other energy infrastructure funds. This is also a very reasonable level that should strike a balance between risk and reward. It is also quite a bit less than the 27.56% leverage ratio that the fund had the last time that we discussed it, so it does not appear that it is leveraging up as the market for energy stocks improves.

Distribution Analysis

One of the biggest reasons why investors purchase shares of energy infrastructure companies is because they tend to have higher yields than most other things in the market. As we saw earlier in this article, the Alerian MLP Index has a trailing twelve-month yield of 7.90% and even most midstream corporations have much higher yields than money market funds or U.S. Treasuries today. This is a stark difference from pretty much every other sector in the market. The Kayne Anderson Energy Infrastructure Fund collects these large dividends from the assets in its portfolio. It then adds any capital gains that it manages to realize on top of that. Finally, the fund even goes so far as to apply a layer of leverage to its assets to boost both the effective yield and any gains. The fund then pays all of this money out to its shareholders, net of expenses.

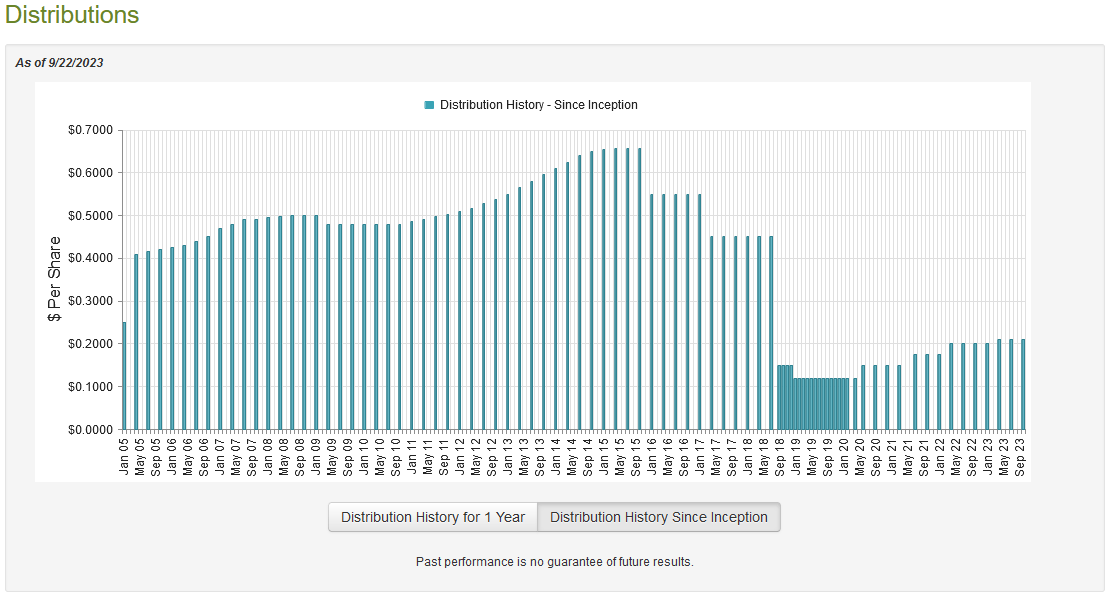

This can be expected to give the fund a fairly high yield on its own, which is certainly the case. The Kayne Anderson Energy Infrastructure Fund pays a quarterly distribution of $0.21 per share ($0.84 per share annually), which gives it a 9.61% yield at the current price. This actually makes this one of the highest-yielding energy infrastructure funds on the market. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years, as we can see here:

{kind=link}

We can see that the fund's distribution has varied considerably over the years, as it has been both raised and cut several times. The recent trend is positive though, as the fund has been consistently raising its distribution since the COVID-19 pandemic of 2020 that collapsed energy prices and the market performance of midstream companies. This is a good sign as it indicates that the fund is actively trying to reward its shareholders as the market improves.

As is always the case, we want to see how sustainable the distribution actually is. After all, we do not want to be the victims of another distribution cut, since that would reduce our incomes and probably cause the fund's share price to collapse.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a much newer report than the one that we had available to us the last time that we discussed this fund. This is nice, as it should be able to give us some insight into how well the fund performed during the first half of the year. As everyone reading this is no doubt well aware, the first half of this year was somewhat weaker for anything in the energy industry than 2022 was, as lower energy prices generally dragged on performance.

During the six-month period, the Kayne Ander Energy Infrastructure Fund received $31.907 million in dividends and distributions and $37,000 in interest from the assets in its portfolio. However, as is normally the case with energy infrastructure funds, some of this money came from master limited partnerships and is not considered to be income for tax purposes. As such, the fund only reported a total investment income of $13.598 million during the period. It paid its expenses out of this amount, which left it with $1.349 million available for shareholders. This was obviously nowhere near enough to cover the distributions, which totaled $55.814 million during the period. At first glance, this may be concerning as the fund's net investment income was clearly insufficient to cover its payouts.

However, the fund does have other methods through which it can obtain the money that is needed to cover the distributions. For example, we have already seen that the fund received $18.346 million from the various master limited partnerships in its portfolio. This money is not considered investment income, but it obviously does still represent money coming into the fund that could be used to pay the distribution. In addition, the fund might have been able to achieve some realized capital gains that could be paid out. Unfortunately, the fund failed miserably at this task during the period. The Kayne Anderson Energy Infrastructure Fund reported net realized losses of $1.607 million and had another $102.433 million net unrealized losses during the period. Its net assets declined by $158.533 million after accounting for all inflows and outflows during the period. This is quite concerning, as the fund clearly failed to cover its distributions during the period.

However, this does not take into account the fact that the fund delivered a very impressive performance during the preceding year. During the full-year period that ended on November 30, 2022, the Kayne Anderson Energy Infrastructure Fund saw its net assets increase by $321.543 million after accounting for all inflows and outflows during the period. That was more than enough to cover the shortfall in the distribution that happened during the most recent six-month period. As of May 30, 2023, the fund had higher net assets than it did on December 1, 2021, so it did manage to cover its distributions and all other expenses over the eighteen-month period. Ultimately, the long-term sustainability of the fund's distribution will depend on how well it manages to perform going forward. It is reasonable to assume that it was probably able to generate some gains so far as midstream companies have been trending up since mid-July, so the fund's finances and distribution are probably okay. We will naturally want to keep an eye on it, though.

Valuation

As of September 22, 2023 (the most recent date for which data is currently available), the Kayne Anderson Energy Infrastructure Fund has a net asset value of $10.27 per share but the shares only trade for $8.85 each. This gives the fund's shares a 13.83% discount on net asset value. This is an incredibly large discount, albeit not as good as the 14.58% discount that the shares have averaged over the past month. However, anytime a fund's shares get a double-digit discount, the price is quite reasonable. Overall, the current price is an acceptable one to pay for the fund's shares.

Conclusion

In conclusion, the Kayne Anderson Energy Infrastructure Fund is a decent way to get exposure to the very high-yielding energy infrastructure industry. The tailwinds for energy are strong right now, as crude oil prices are positioned to rise over the next few months and global natural gas demand is likely to grow. The companies in this fund are well-positioned to take advantage of this situation. The fund has one of the highest yields in the energy infrastructure space, which may be appealing to income-seekers, and it is trading at a very attractive valuation. Overall, this fund is worth further investigation.

For further details see:

KYN: One Of The Highest-Yielding Energy Infrastructure Funds Around