KD - Kyndryl: Attractive Turnaround Opportunity Mispriced By The Market

2023-09-14 08:35:24 ET

Summary

- Kyndryl was spun off from IBM in 2021 and has performed poorly due to the lack of top-line growth.

- However, the company has been vigorously executing a strategic framework to improve profitability.

- The strategy has been yielding better than expected results but KD stock continues to trade at a depressed valuation, representing a perfect opportunity to go long.

Investment Thesis

Kyndryl ( KD ) was spun off from IBM ( IBM ) in 2021. Kyndryl is the largest managed infrastructure services provider in the world. It manages legacy data centers, hybrid cloud environments, and provides services including IT support, cybersecurity, consulting, cloud transitions, and more. At the time of the spin-off, investors labeled it as the 'bad part' of IBM.

However, we believe the market is underappreciating the opportunity for a turnaround due to Kyndryl's unimpressive top-line revenue growth. But the real opportunity lies in improving earnings through cost-cutting and renegotiating existing contracts. The stock is trading at very attractive multiples, and, based on the management's performance so far and the results they are obtaining, we believe the stock will appreciate significantly over the medium-term.

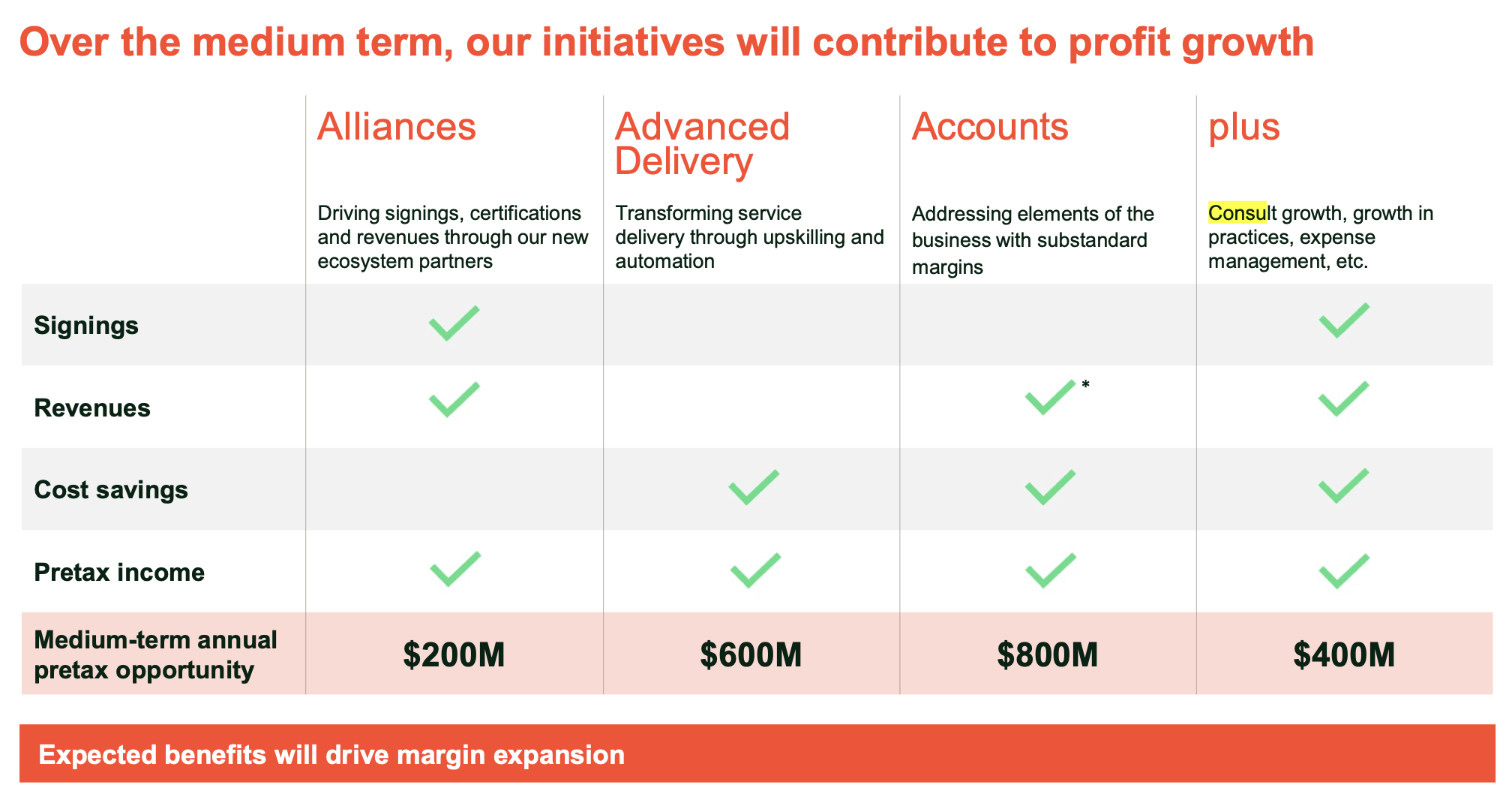

Three-A’s Strategy

In a bid to accelerate its return to profitable growth, the company is vigorously executing a strategic framework known as the "three-A" initiatives, which encompass Alliances, Advanced Delivery, and Accounts.

{kind=link}

Kyndryl Q1 F24 Earnings Presentation

Alliances Initiative

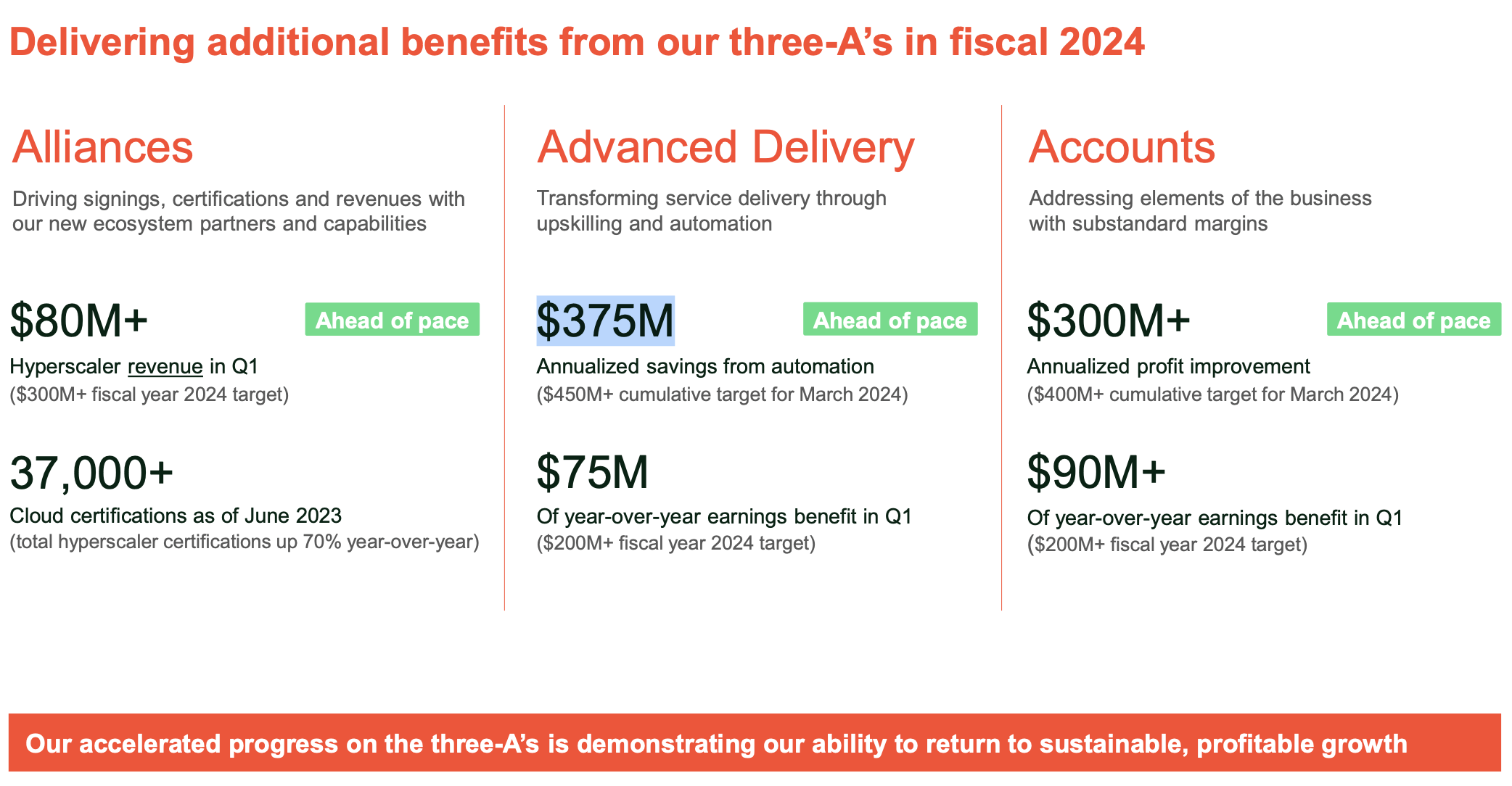

This initiative focuses on forging strategic partnerships and expanding collaboration with key players in the technology ecosystem to drive signings, certifications, and revenue. As an independent company, Kyndryl can now move outside of the legacy IBM ecosystem to partner with other technology and cloud providers in order to access a wider customer base. Notably, they already announced significant business alliances with industry giants like Microsoft, Amazon Web Services, Google Cloud, SAP, Dell, Cisco, and Nokia, among others.

In the first quarter, they recognized more than $80 million in hyperscaler related revenue, putting their run rate ahead of their $300 million full year target. They also continued to increase their hyperscaler certifications to more than 37,000, which is 70% higher than a year ago. In the medium-term, they believe this represents an opportunity of $200 million pre-tax income.

Advanced Delivery Initiative

The Advanced Delivery initiative is centered around reducing their cost to serve their clients through a combination of upskilling the workforce and automation. As more processes become automated, Kyndryl can either reduce their headcount or re-position employees towards efforts that may generate more growth.

To date, they've been able to free up more than 6,500 delivery professionals to address new revenue opportunities and to backfill attrition. This is worth roughly $375 million a year, representing a $75 million increase in their annual run rate this past quarter. Management estimate that these cost saving measures could reach +$600 million in pre-tax income in the medium term.

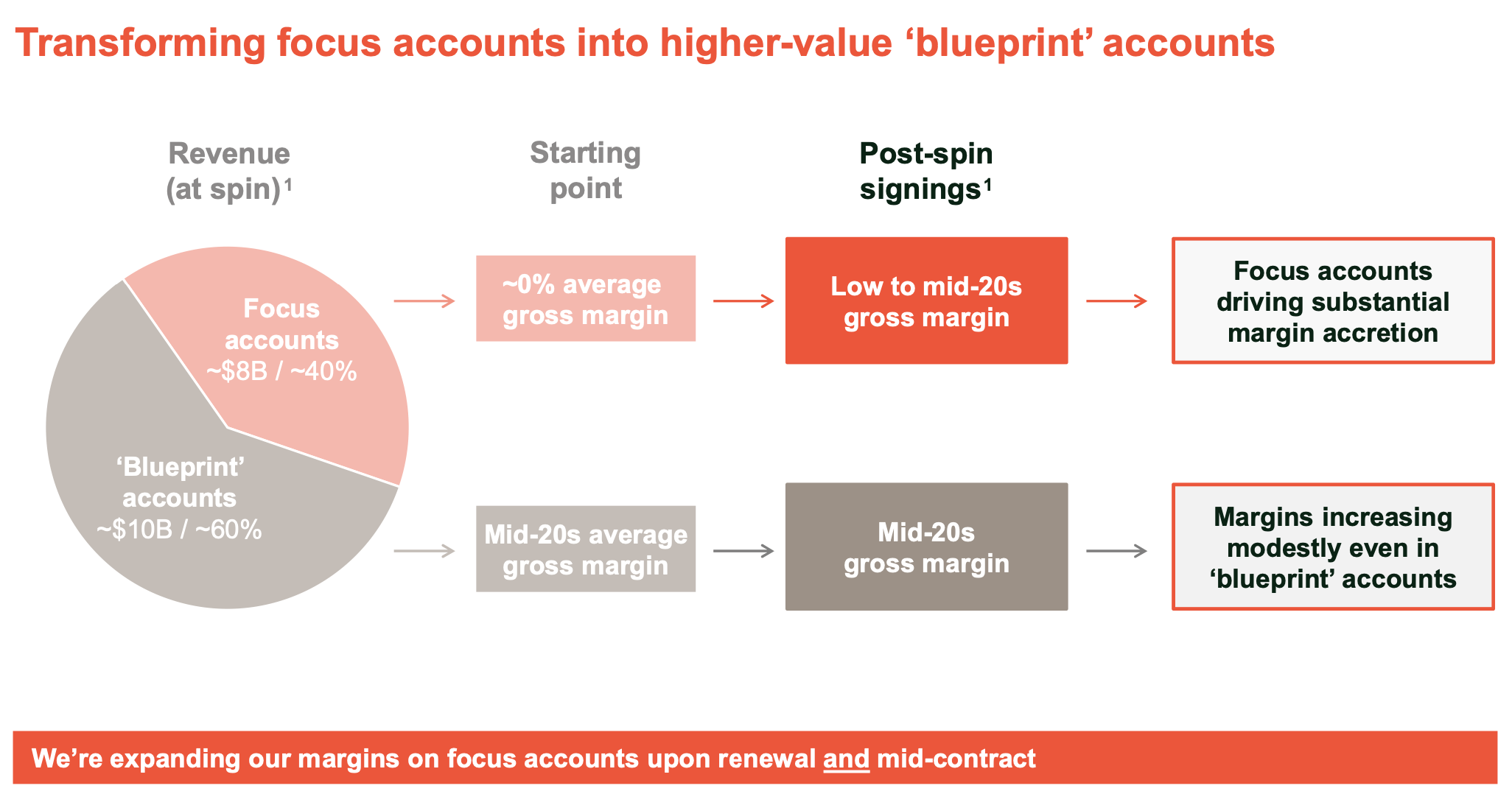

Accounts Initiative

When Kyndryl became an independent company, they identified that around 40% of the sales ($8 billion) had an average gross margin of 0%, while the remaining 60% of their business generated Gross Margins in the low/mid 20% range. This profitable section of their business supports their entire G&A structure and interest burden and gets the company to roughly breakeven. Any improvement with the problematic contracts, labeled “Focus Accounts”, should lead to a meaningful improvement in gross profit and earnings.

{kind=link}

Kyndryl Q1 F24 Earnings Presentation

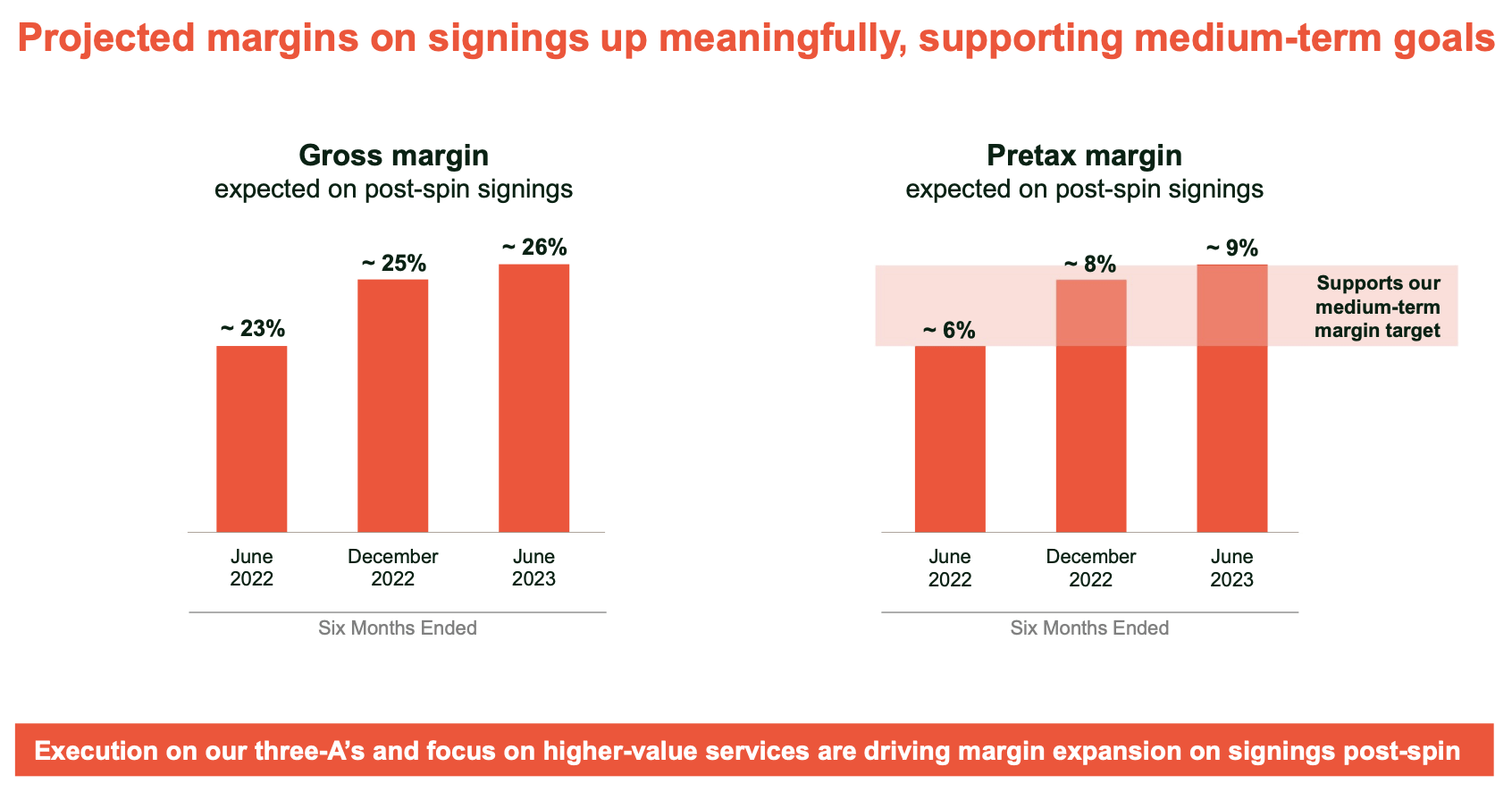

The company has already seen more than $300 million of annualized benefits, and they are on track of exceeding their $400 million fiscal 2024 year-end goal. Moreover, the margins negotiated on the new contracts keep surpassing their own expectations quarter after quarter.

{kind=link}

Kyndryl Q1 F24 Earnings Presentation

Plus

Plus serves as a catch-all for everything else. It includes everything from G&A optimization to growing business lines such as Kyndryl Consult. Consult encompasses a wide range of advisory and implementation services offered across all six of their practices. It is one of the fastest-growing segments of the company and its growth engine, with revenue jumping 20% YoY in Q1 F24. It accounted for 12% of their total revenue in F23, and they expect it will reach ~20% in F27.

{kind=link}

Kyndryl Q1 F24 Earnings Presentation

The IT industry is undergoing a swift transformation, presenting a host of fresh prospects, and Kyndryl is strategically positioned to harness these opportunities. Anticipating growth in various domains, including security, artificial intelligence ((AI)), 5G technology, hybrid cloud solutions, and intelligent automation, the company is set to expand its reach now that is free to recommend products outside the IBM ecosystem. Moreover, they will also benefit from a larger TAM.

Kyndryl expanded its TAM from $240 billion to $415 billion post spin-off, and subsequently, the management has even revised this figure to an impressive $520 billion. In other words, the TAM has more than doubled. It would be unwise to assume that the company won't be able to gain any market share now that it is independent and a more flexible organization.

Financial Results And Outlook

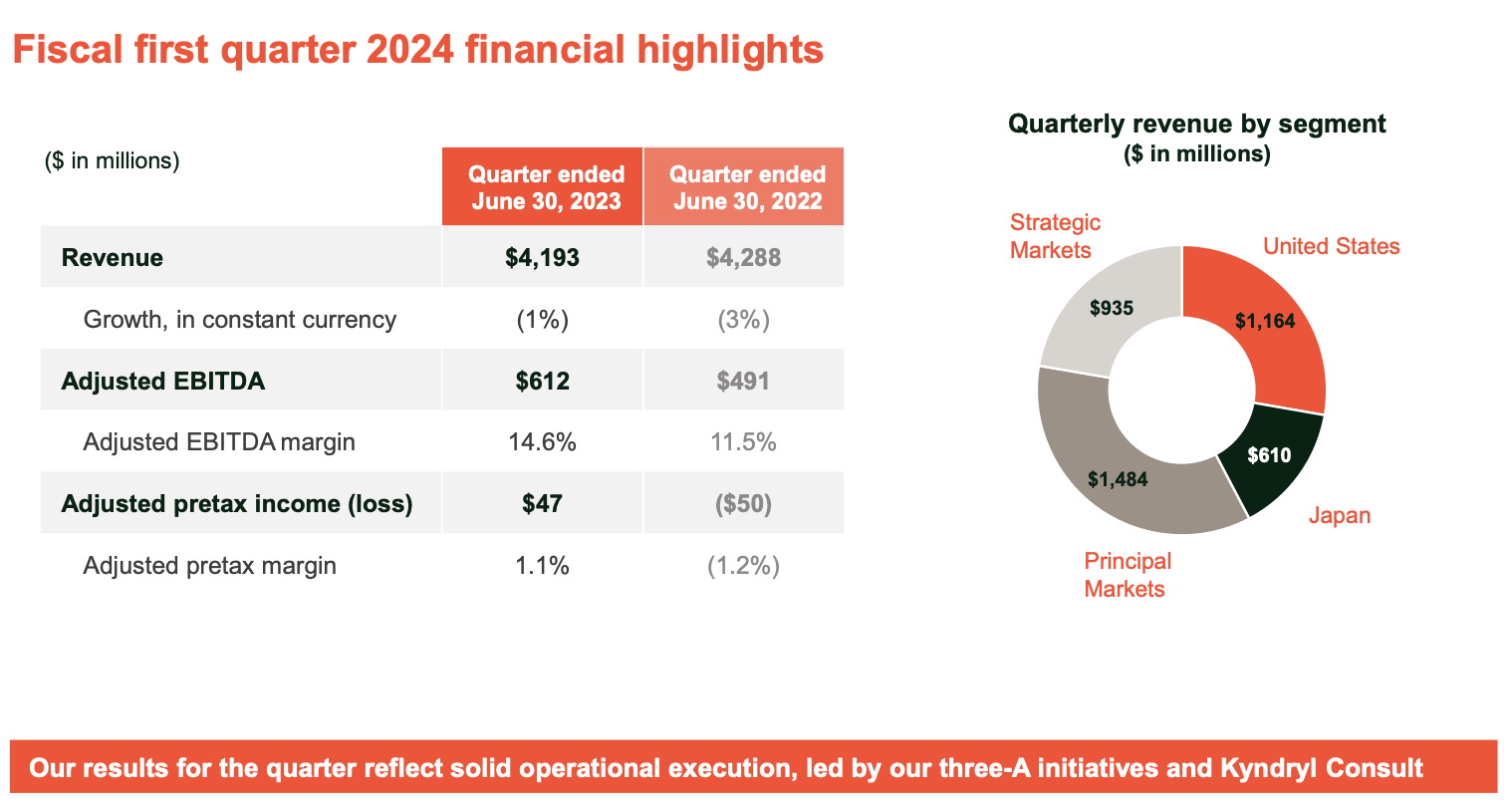

Kyndryl reported Q1 F24 financial results on August 8, and they are starting to see the benefits from the "Three A's" strategy already. Revenue came in at $4.19 billion, a YoY decline of 2% in constant currency. Signings were down 5% year-over-year in constant currency. However, through July 31, the year-to-date signings were up 9% to $3.6 billion.

Where we can see real progress in the margins. EBITDA increased 24.6% YoY from $491 million to $612 million. This represented a 14.6% EBITDA margin, +310 bps YoY. Adjusted pretax income turned positive to $47 million, a 1.1% margin, which is 210bps higher than a year ago.

{kind=link}

Kyndryl Q1 F24 Earnings Presentation

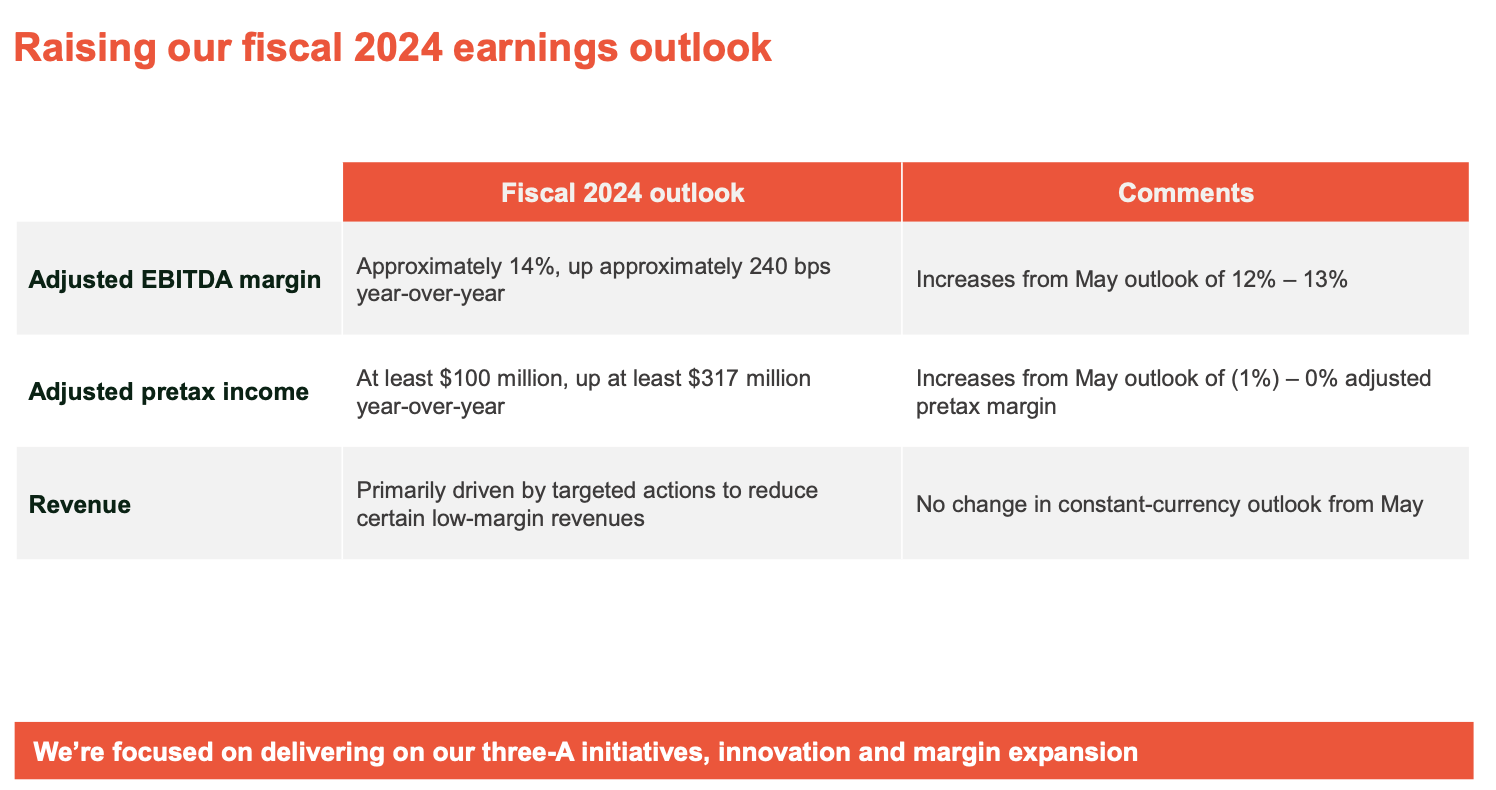

But the real reason why the stock jumped 15% after the results is because they raised their F24 full-year guidance. The company now expects the EBITDA margin to be approximately 14%, versus 12%-13% in May. Moreover, they estimate that adjusted pretax income will be at least $100 million, an increase from breakeven to slightly negative in May.

The management made very clear on the earnings call that annual losses are behind now and that as the company continues to hit its profit goals, margins should continue to expand.

However, they maintained their revenue estimate between $15.8-$16.2 billion, which represent (8%)–(6%) growth in constant currency. They also continue to estimate $750 million in capex and $120 million in interest expense.

{kind=link}

Kyndryl Q1 F24 Earnings Presentation

Lastly, they ended the quarter in a solid financial position. The company holds $1.5 billion in cash and equivalents in its balance sheet and only has $3.3 billion of total debt. Moreover, they have $3.2B of undrawn senior unsecured credit facility to boost liquidity in case of need.

Valuation

We believe the market is not recognizing the potential of Kyndryl, given that it is trading at very attractive multiples. The stock is priced at around 0.42x EV/Sales, 2.5x EV/EBITDA, and approximately 11x EV/FCF (all forward measures). For a tech company with growing profits, it is definitely very attractive. For comparison, the sector's average EV/SALES is 2.73x and EV/EBITDA 14.5x.

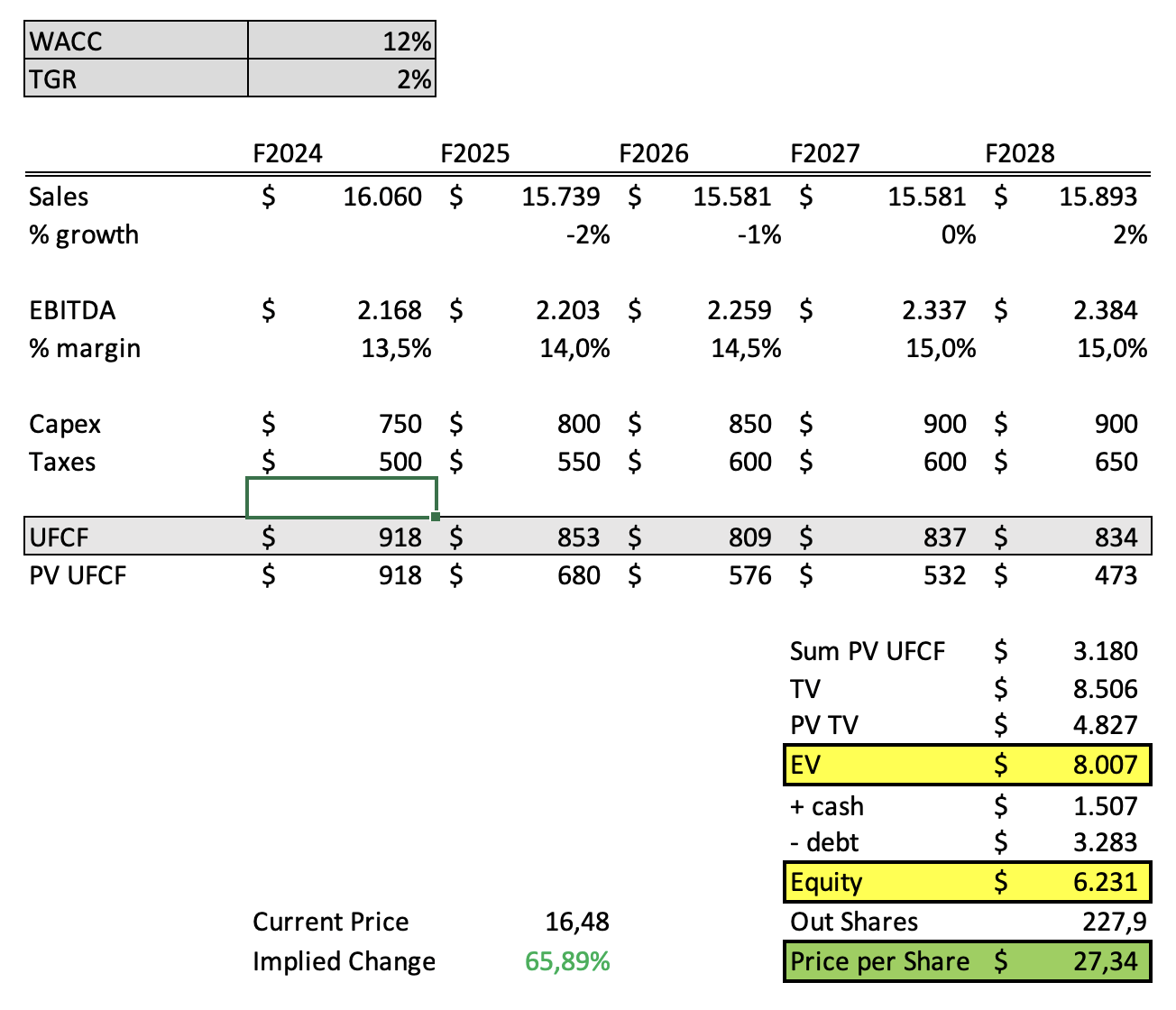

We also decided to do a DCF model. We assumed the revenue estimates from WS analysts for F24 and F25, and then modeled a modest decline and a return to growth after F27. EBITDA margins this year are expected to be around 14%, and with the ongoing improvement in margins, we think it is very conservative to assume they will reach 15% in F2028. Lastly, we took F24 estimates for capex and taxes and increased them slightly year after year. Finally, we also assumed a WACC of 12% and a TGR of 2%.

{kind=link}

Author

Even with these modest growth assumptions, we arrived at an implied price per share of $27.34, a ~66% increase from current levels. However, we believe EBITDA margins can reach higher than 15% and that multiples will expand to those closer to their competitors. Returning to all-time highs is not out of the picture. Furthermore, as the company starts generating free cash flow again a dividend and buyback program will likely be put in place, which can boost the stock price.

Risk

As we mentioned, Kyndryl isn't growing revenue. On the contrary, it is declining YoY. This is due to the fact that Kyndryl's traditional core business, focused on managing data centers for major clients, has been facing a steady decline due to the rise of cloud computing.

However, Kyndryl anticipates that it will not only compensate for this decline but also surpass it by assisting clients in their transition to the cloud and offering a range of innovative new services. We anticipate that revenue will return to single-digit growth in a couple of years, but it is still unclear how things will play out and how management will execute.

Takeaway

To sum up, we believe the changes that Kyndryl is undergoing are going to positively affect their financial results, and the market is not pricing it yet. At current prices, we think it represents an attractive risk-reward opportunity.

For further details see:

Kyndryl: Attractive Turnaround Opportunity Mispriced By The Market