KD - Kyndryl: The Comeback Kid

Summary

- Kyndryl was the worst part of underperformer IBM, and was spun off in November 2021.

- The company struggled at first with declining revenues and losses.

- Management provided a detailed plan with earnings improvements totaling $2 billion.

- The company has hit or exceeded its goals so far, and is very close to revenue growth and earnings.

- Meanwhile, the stock still trades for about 20% of revenues, well below peers.

My most successful strategy is turnarounds, though I generally only find a handful of good ones each year. A turnaround to me is not a beaten down stock. It's a beaten down stock that has shown clear signs of improvement. That is where Kyndryl ( KD ) is. The stock is clearly beaten down, trading for only 20% of sales. But the most recent quarter and success with earnings improvement initiatives indicate a turnaround is in progress.

On December 6, 2021, just after its spinoff from IBM, I published an article on Kyndryl titled IBM Spinoff Kyndryl Is The Worst Of The Worst: Buy It. By that I meant, Kyndryl was the most underperforming portion of IBM a company which itself had underperformed for years. After I wrote the article, the stock price plummeted from $18.34 at the time of publication to as low as $7.93. Also after my article, management presented a plan to turn around the company from revenue decline and losses to a solidly profitable grower. The market clearly did not buy this plan at first. However, the most recent earnings report shows a much better picture. The company continues to meet or exceed the plan. Revenues are stabilizing and earnings are now at breakeven and guided for profits.

Background

On November 3, 2021 IBM distributed 1 Kyndryl share to IBM shareholders for every 5 of IBM. This represented 4.8% of the market cap of IBM at the time of the spinoff, for a business with 20% of the combined revenues. Kyndryl joined the S&P Midcap 400 on November 5 th and there are about 227 million shares outstanding. It has about 90,000 employees, most of which are highly skilled.

What is now Kyndryl was a major growth business for IBM in the 1990s into the 2000s as it expanded from its traditional mainframe hardware and software business. This ended about a decade ago when the cloud emerged and many large corporations moved their IT datacenters to cloud providers such as Amazon Web Services and Microsoft Azure. Kyndryl was the IT data center services portion of IBM formerly comprising most of IBM Global Technology Services. It traditionally operated and designed datacenters for large corporations and governments. Kyndryl handles most or all IT infrastructure for these corporations.

Being freed of IBM has allowed Kyndryl to pursue many new markets it could not before. In fact, management claims its total addressable market went from $240 billion to $520 billion.

The customer base is global with only 28% of revenues coming from the U.S. Another 35% comes from what they call principal markets, which are the major European countries and Australia and New Zealand. Japan accounts for 15%.

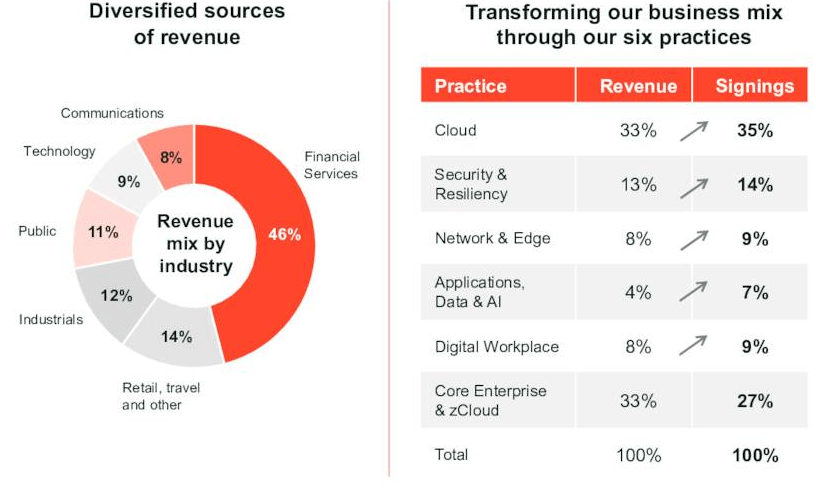

The chart below from their most recent earnings presentation breaks out revenues by business and industry.

Kyndryl 3Q 2023 earnings presentation

{kind=link}

As shown above, the company is steadily moving away from its traditional Core Enterprise and toward growth areas such as cloud, edge, data, AI and digital workplace.

Financial Results

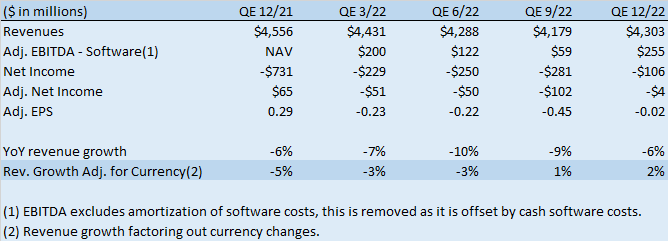

Kyndryl had shown a slow but steady revenue loss in the years prior to the spinoff. The first 5 quarters of Kyndryl's results as an independent company are shown below. We are currently in fiscal 2023 which ends March 31.

Kyndryl earnings announcements

{kind=link}

The most important line from the chart is the shaded bottom one. It shows revenue, when adjusted for currency adjustments, improving every quarter from declines to growth. Currency is a big factor for Kyndryl which gets 72% of revenues outside the U.S. Adjusted for currency, revenues in the U.S. increased by 7% in QE 12/22, and were up by 2% in Japan. It increased in all 4 of their market segments last quarter.

The next line to look at is adjusted net income. This number declined through September and then improved in the most recent quarter to almost breakeven. The adjustments are mostly onetime items or intangible amortization. It does include some stock compensation which I normally remove, but it is a small amount so I kept it in.

Adjusted EBITDA requires some explanation as it is misleading and way overstated. They include amortization of deferred costs in adjusted EBITDA. Kyndryl defines deferred costs as costs for software, contract setup and other contract costs. While it's Okay for accounting purposes to capitalize and amortize these costs, it is misleading to add it back to adjusted EBITDA without then subtracting the costs. That is because the amortization is mostly offset by cash paid for the initial costs that were capitalized. Keep in mind, most amortization is of intangibles which is not offset by anything. Kyndryl's EBITDA therefore is about double what most companies would show if they didn't capitalize these costs, and few companies do. To put it another way, Kyndryl's EBITDA is about double what most companies show using the same data. What I did with the EBITDA figure is subtract out amortization of capitalized costs from EBITDA. Deferred costs totaled $1,063 million in first 3 quarters of Fiscal 2022 and amortization of them was $909 million.

My figure for adjusted EBITDA increased significantly in the most recent quarter from all the prior quarters.

Kyndryl did have $58 million of free cash flow in the first nine months of fiscal 2023 (defined as cash from operations less capex). However, this was due to lower accounts receivable and inventory numbers.

Guidance

The strength of revenues in the most recent quarter is described as somewhat seasonal by management. They are guiding for revenues of $4.1 billion at the midpoint for the current quarter.

At the earnings announcement on February 7, 2023, management raised it revenue guidance in fiscal 2023 to $16.8 to $17.0 billion from $16.3 to $16.5 billion. The guidance increase was primarily due to currency but also more new signings in their Kyndryl Consult (defined in Catalyst #14 below) segment than expected. They also reiterated guiding to return to revenue growth by 2025. But on a currency neutral basis Kyndryl is already there.

They further guided the adjusted pretax net income margin to -0.5 to 0.5% for fiscal 2023 in constant currency or -1 to -2% unadjusted. Since there is only one quarter remaining, and the others had unadjusted losses exceeding 4%, that indicates a profit in the current quarter, a big step forward. I believe this is why the stock rallied on the date of the earnings announcement.

Balance Sheet

The balance sheet is adequate. On December 31, 2022, interest bearing debt totaled $3.2 billion and cash was $2.0 billion. Net debt was $1.2 billion on that date. There was also a $3.0 billion undrawn line. The debt is all rated investment grade by Moody's and S&P.

Catalysts

Kyndryl has a large number of catalysts available to drive earnings and revenues higher. These are discussed below.

1. Big increase in TAM - Kyndryl was heavily tethered to IBM in the past. According to a Kyndryl presentation dated October, 2021 being free of IBM increases Kyndryl's total addressable market ((TAM)) from $240 billion to $415 billion. Management has since increased that to $520 billion. Kyndryl is no longer a captive to IBM and can recommend and sell anyone's products and provide new services. Some of these new services are discussed in catalyst #14.

2. Eliminating contracts with substandard margins - On page 18 of its most recent earnings presentation management indicates that 60% of its contracts have an average gross margin of mid 20% and the other 40% average 0%. This is an $800 million pretax net income per year opportunity to renegotiate the underperforming 40% of contracts as they mature. So far about 20% have been renegotiated on terms similar to the 60%, improving pretax earnings by $130 million per year. As shown in the operating results section, they do not appear to be losing significant numbers of customers over this. This should continue to play out over the next three years as contracts signed when part of IBM end.

3. Consultant growth and expense reduction - This is a $400 million pretax net income per year opportunity with no numbers yet published for progress.

4. Advanced delivery - This involves upskilling the workforce and automation and is a $600 million per year pretax net income opportunity. More than 4,500 professionals have been redeployed to new revenue streams and to backfill attrition. The Company had a fiscal 2023 (ends March 2023) objective of $200 million improvement and now expects to get to $225 million this fiscal year.

5. New alliances - This is a revenue growth initiative expected to add $200 million in pretax net income per year. If you have been following Kyndryl you have seen numerous alliance announcements with many of the major IT companies. In their earnings presentation they stated " In the nine months ended December 31, 2022, Kyndryl signed contracts tied to cloud hyperscaler alliances with an aggregate value of approximately $750 million, putting the Company on track to achieve its $1 billion hyperscaler signings". Hyperscalers are large cloud companies. These alliances include Microsoft, AWS, Google, Cisco, Dell, Oracle, Red Hat, SAP and VMware.

6. Free of poor management - The decade IBM was under Ginny Rometty was, in my opinion, a disaster. In January, 2020 she was replaced as CEO by Arvind Krishna, the head of IBM's cloud division. It must be noted that Kyndryl CEO Martin Schroeter, like Krishna, was a member of IBM's executive team, in his case for 7 years. However, I believe anything is better than Rometty and CEO Schroeter is off to a good start at Kyndryl.

7. Growth areas - The IT business is rapidly evolving, leading to new opportunities. Kyndryl is positioned to benefit from many. They expect to get growth from areas such as security and resiliency, AI, 5G, a hybrid cloud, and intelligent automation. New signings are already growing in these areas as shown in the first chart of this article. They are now free to recommend non-IBM equipment and services. Kyndryl can expand its consulting and cloud services formerly handled by other parts of IBM.

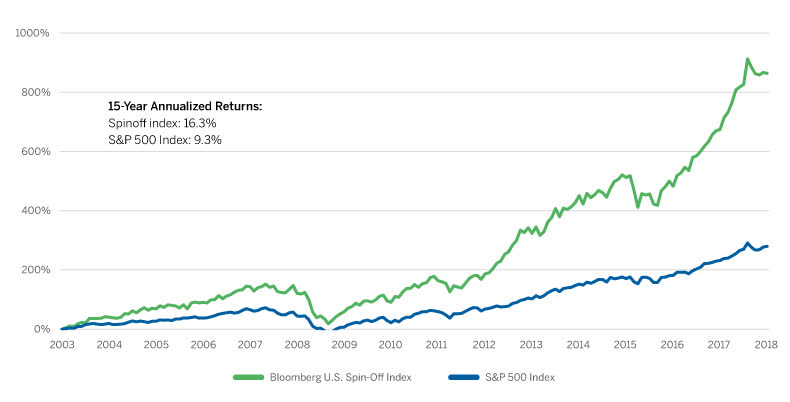

8. Spinoffs do well - The following is from Investopedia " Historically, spinoffs have been good for investors. On average, both the parent company and the subsidiary outperform the market during the 24-month period following a spinoff. Investors who have been able to withstand the unpredictability of the initial days and weeks have seen nice gains."

A study of spinoffs by Brown Advisory is shown in the following chart. It clearly shows outperformance to the parent and the stock market. How can this be? Many believe it's due to management being more focused. I also believe it's due to management being better incented with stock and option compensation directly tied to the business. Further, underperforming businesses like this tend to be underinvested in by the former parent. Kyndryl is reinvesting in the business.

{kind=link}

9. Tax loss and IBM shareholder selling - Kyndryl had two overhangs it needed to get past when it was spun out. The first was an IBM shareholder overhang. The initial Kyndryl shareholders were all IBM shareholders. Many long term IBM holders sold for various reasons. IBM has long been a big dividend investors stock and Kyndryl currently does not pay one. Kyndryl's market cap is 4% of IBM's, making it too small for large cap funds and investors. Kyndryl also has the stigma of being the junk IBM needed to jettison to grow again. Add to this massive tax loss selling toward the end of 2022. Both should be over now.

10. Insider purchases - In the past 6 months insiders have acquired 167,800 shares at market price and have sold none other than to pay taxes on vested stock grants. On November 9, 2022, CEO Schroeter purchased 109,000 and CFO Wyshner 20,000.

11. Dividend initiation - Once the smoke clears and it's apparent Kyndryl is solidly profitable, a dividend is likely. This will attract a new group of investors. It may take a couple years as management wants to pay down some debt first and reinvest in the business. However, the balance sheet is already strong enough.

12. Mergers and acquisitions - Kyndryl has the balance sheet to pursue acquisitions. An acquisition can make it quicker and easier to move into adjacent businesses they couldn't offer before. There have been no acquisitions since 2016. Kyndryl can now also be bought itself. Its price at about 20% of revenues will be very attractive one it becomes solidly profitable.

13. Currency reversal - Revenues in the first 5 quarters as a public company were significantly reduced by the strength of the dollar. The dollar is currently dropping versus other major currencies. What was a drag is likely to become a tailwind.

14. New services - Kyndryl has created the following new services.

Kyndryl Bridge is to help customers manage modernization across their complex global IT. Since its launch in late September 2022, nearly 500 customer accounts have been added.

Kyndryl Vital is their ability to be an objective expert across many technologies allowing Kyndryl to advise and collaborate with customers in ways we they couldn't under IBM.

Kyndryl Consult ties the two together. This is a big growth area with 12% of revenues last quarter, up from 10% at the time of the spin. They expect to get to 15% in the intermediate term. They cited this as a big growth area last quarter.

Negatives

I always mention concerns and weaknesses of the companies I review. Here are ones I see for Kyndryl.

Management is not projecting any more than single digit growth once the business is transformed.

Kyndryl's historical core business of managing data centers for large customers is in secular decline due to the emergence of the cloud. Kyndryl expects to more than offset this by helping customers migrate to the cloud and many other new services.

Kyndryl is susceptible to a recession. However, management says it's less impacted than most due to servicing mission critical components of customers. It is still susceptible though. In a recession some customers may go under and new contracts may get delayed. Also, many of the new areas Kyndryl is moving to are less mission critical.

With 72% of revenues outside the U.S. currency swings have been an issue. They are hedging but not enough.

No dividend or stock buybacks (other than to offset insider tax withholdings) currently.

Valuation

The initiatives discussed in catalysts #2-5 of the catalysts are expected to generate $2.0 billion in annual pretax earnings going forward. But they are expected to take about another 3 years to be fully realized. It appears about 20-25% of these have already been realized. That leaves about $1.6 going forward over the next three years. The company is running about breakeven now so that indicates pretax earnings of $1.6 billion in three years. To be conservative and to account for a likely recession I will take 25% off that bringing pretax income of $1.2 billion in three years and after tax net income of $960 million assuming a 20% tax rate.

An appropriate PE ratio for a slow but steadily growing company with a very diversified customer base is around 12-15. Multiply that by the $960 million net income I determined and market value is $11.5 to $14.4 billion in 3 years. That is $50.75 to $63.44, with a midpoint of $57, which is my 3 year share price target.

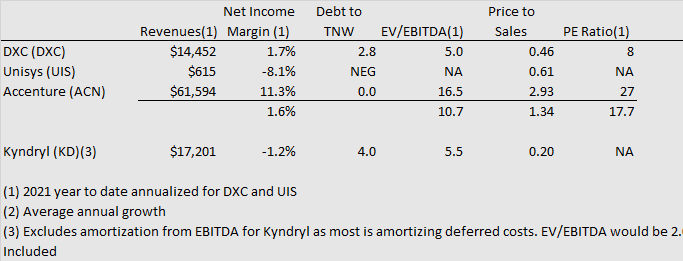

For a one year price target I looked at comparable companies. Below is a chart showing 3 comparables.

Value Line, SEC filings, Yahoo Finance

{kind=link}

[[DXC]] and Unisys (UIS) both have declining revenues and weak or no earnings. They represent the industry Kyndryl has been in. Accenture represents more where Kyndryl wants to go. Accenture is a blue chip company, very profitable, with almost no debt. Kyndryl is nowhere near Accenture and won't be for a long time. However, Kyndryl is already superior to DXC and UIS due to a likely near term return to growth with better margins and a stronger balance sheet. Once the turnaround becomes apparent to the market, it should trade for at least a similar multiple to revenues or at least 50% of revenues. That would put market value at $8.6 billion which is $37.89 per share. My one year price target is $38.

Takeaway

The turnaround is now apparent. I recommend a long position in KD with a one year price target of $38 and a three year price target of $57. The current stock price as of February 10, 2023 is $16.31. Management has identified a number of initiatives to boost earnings and resume sales growth. The company has been meeting or exceeding its goals so far. The other big catalyst is Kyndryl's new opportunity to pursue a whole range of business they couldn't before. They already have relationships with the majority of the companies those opportunities are with. They also already have a highly skilled workforce that can be retrained to move into adjacent businesses. It's just a matter of if they can execute on it, which so far has been the case.

For further details see:

Kyndryl: The Comeback Kid