KD - Kyndryl: The Improving Financial Profile Warrants Some Re-Rating

2023-08-01 15:32:37 ET

Summary

- Kyndryl Holdings is the largest IT infrastructure services provider globally, with operations in 60 countries.

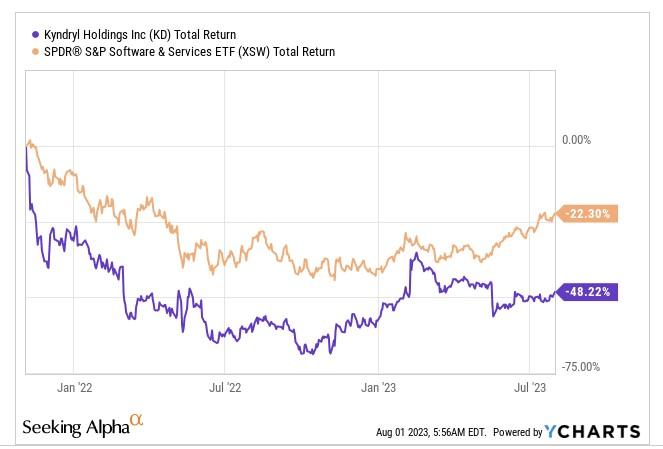

- The company's stock has underperformed its peers since its spin-off in Nov. 2021, but it is an underappreciated play with potential for higher valuation.

- Kyndryl's turnaround plan includes initiatives focused on alliances, advanced delivery, and accounts to drive revenue and profitability.

- Group EBITDA margins look poised to expand by 200bps over the next 3 years.

- The stock is going through a bout of volatility contraction, but as a rotational play within the spin-off universe, things don't look as enticing as they did late last year.

Introduction

Kyndryl Holdings, Inc. ( KD ), which was previously a captive unit of IBM (IBM), is today considered to be the largest IT infrastructure services provider in the world, with operations across 60 countries. With a 30-year track record of designing, building, and managing enterprise IT systems across various industries (although the financial services sector contributes half of the group revenues), the company has build-up ample credibility, which will likely be relied on by clients with even greater fervor, as the tailwinds emanating from cloud migration, digital transformation, cybersecurity, etc. gather steam.

Admittedly, the market hasn't taken too well to KD since it was spun off in November 2021. In fairness, in recent years, stocks within the software and services landscape haven't done too well either, but KD has fared a lot worse, underperforming its peers by over 2x.

{kind=link}

Given what's in store over the next few years, we think KD is an underappreciated play and probably deserves to be priced at a higher multiple

Forward Valuations Don't Reflect The Improvements In Store

Ostensibly, we believe most investors are wary of KD because annual revenue has been on a declining trend since FY18 , or they are concerned with the lack of profitable growth. These trends are likely to linger this year as well (i.e., the year ending March 2024) with consensus suggesting that revenue will decline by -5% , and an expected negative EPS of $-1.78. However, we'd urge investors to not get too bogged down with the historical track record as that is currently being driven by legacy contracts (which should fade), and focus on some of the initiatives that management has put in place to help drive revenue and profitability over time.

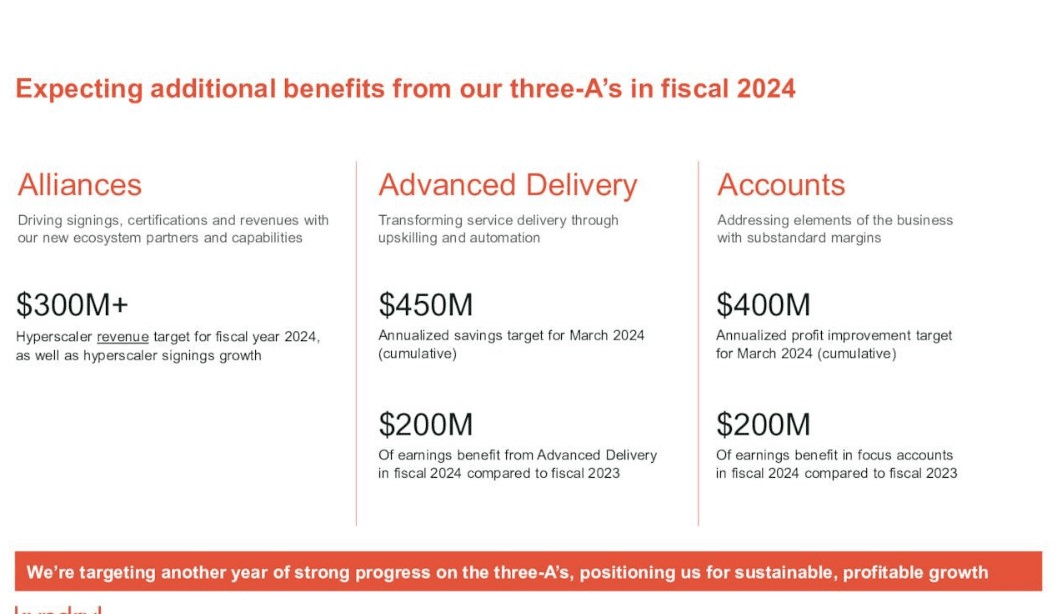

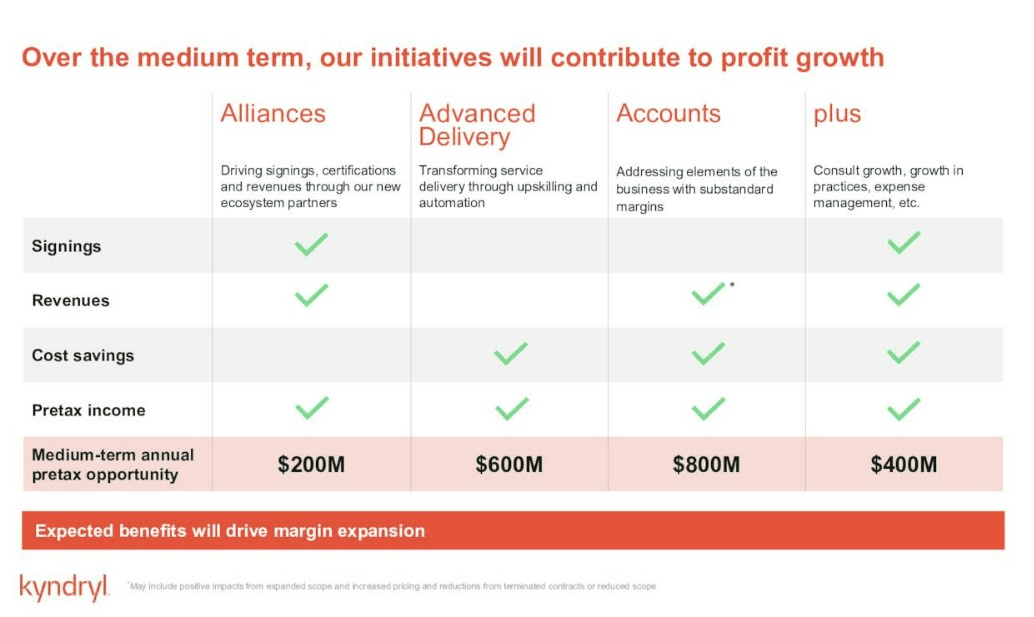

The bedrock of the Kyndryl management's turnaround plan are the "3-As" initiatives which stand for Alliances, Advanced Delivery, and Accounts.

{kind=link}

Under Alliances, Kyndryl will look to expand the tech solutions it can offer its clients by getting into more alliances and leveraging its linkages with hyper scalers and other tech vendors. Over the last 12-18 months, KD has already gotten into alliances with the likes of Microsoft (MSFT), Amazon (AMZN) Web Services, SAP (SAP), Dell (DELL), Google (GOOG) (GOOGL) Cloud, etc. We particularly like the thrust with the hyperscalers as previously, KD didn't have a great presence in the public cloud arena. Last year, they managed to bring in $1.2bn of hyperscale signings, which was above their $1bn target. KD will continue to incorporate more cloud-based content in their customer offerings, and next year they are targeting $300m worth of hyperscale-related revenue. At the pre-tax profit level, KD believes its initiatives under Alliances could result in benefits worth $200m

Under Advanced Delivery, the focus will be more on the cost base as the company pivots more to automation, upskilling, and productivity improvements. All in all, the company ended up delivering $275 of savings on account of this initiative ($75m for that they achieved), and this year the goal is to bring through another $200m by increased automation work. The medium-term goal is to bring through benefits of $600m at the pre-tax profit level.

Then you have the Accounts umbrella, which will play a key role in shifting the margin profile of Kyndryl. Currently, 60% of KD's accounts consist of those with a gross margin profile of 25% and above. However, the rest of the business consists of focused accounts that are not profitable at the gross margin level. KD intends to diminish this component and is even prepared to walk away from the client when it comes to an end if its terms are not met. What investors need to consider is that given the mission-critical work that KD carries out, customer stickiness tends to be an inherent theme. Thus, we think KD will have enough clout to levy the "take-it-or-leave-it" card and renew under better terms, which should eventually help improve the overall margin profile.

KD management believes that if they can get the sub-par 40% chunk of the existing accounts to a margin profile of 20-25%, it could end up generating $800m in pre-tax earnings.

Besides that, also note that KD has been making tweaks to its workforce and real estate, which are poised to generate $200m of savings in FY24 (75% is workforce related), and $250m in FY25.

{kind=link}

All in all, these three-As initiatives of KD and the workforce and real estate initiatives could meaningfully boost ITS margin profile over time. It looks like consensus too is buying into the narrative, as margins are poised to increase every year henceforth, particularly for the year ending March 2026, where annual improvements could come in as high as 100bps!

YCharts

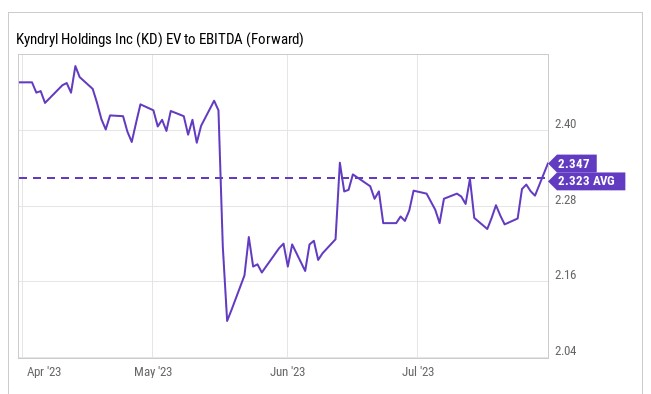

Considering the multi-year margin improvement trajectory that's on the cards, we think it's a bit of a farce that KD is only priced at 2.35x forward EV/EBITDA, largely in line with its listing history average. Crucially, the sector median multiple is a lot higher at 15x ; this massive gap doesn't quite feel right.

{kind=link}

Closing Thoughts - Technical Considerations

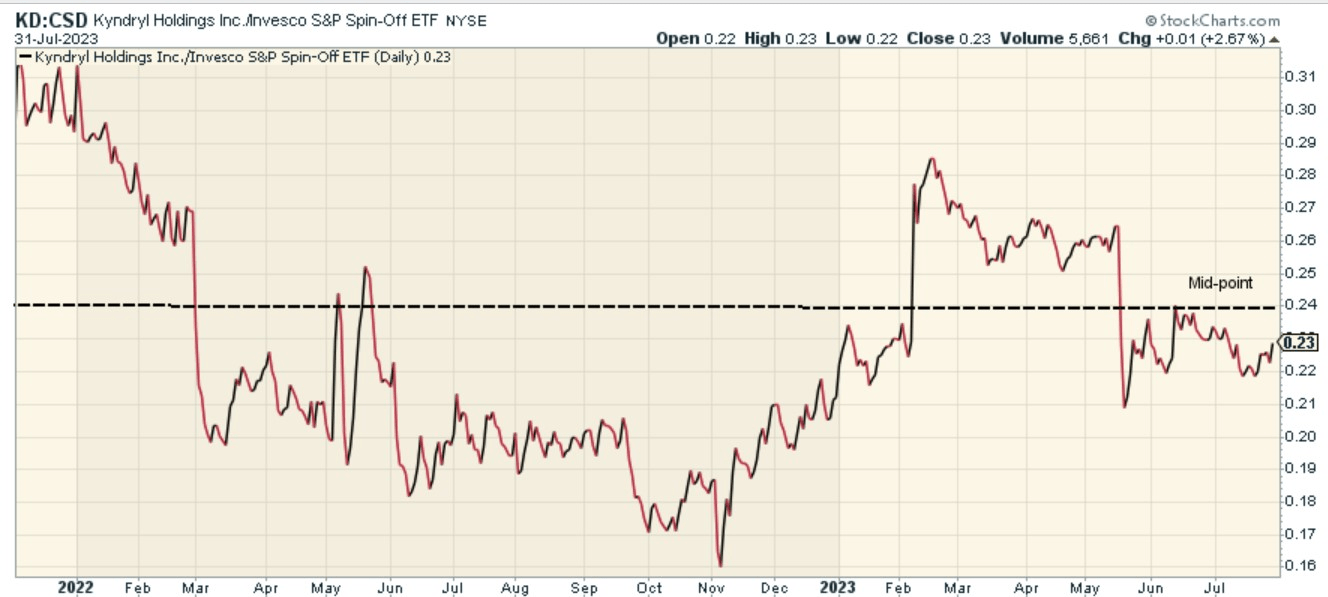

As far as the stock's rotational quotient is concerned, we don't see any compelling reasons to get on board. The Invesco S&P Spin-Off ETF ( CSD ) focuses on US companies that have been spun off from their parent companies within a 4-year duration. If one measures the relative strength of KD to CSD we can see that the former could have been a rather attractive mean-reversion play within this space, back in November last year. However, at current levels, there's limited incentive to turn gung-ho now, with the RS ratio close to the mid-point.

{kind=link}

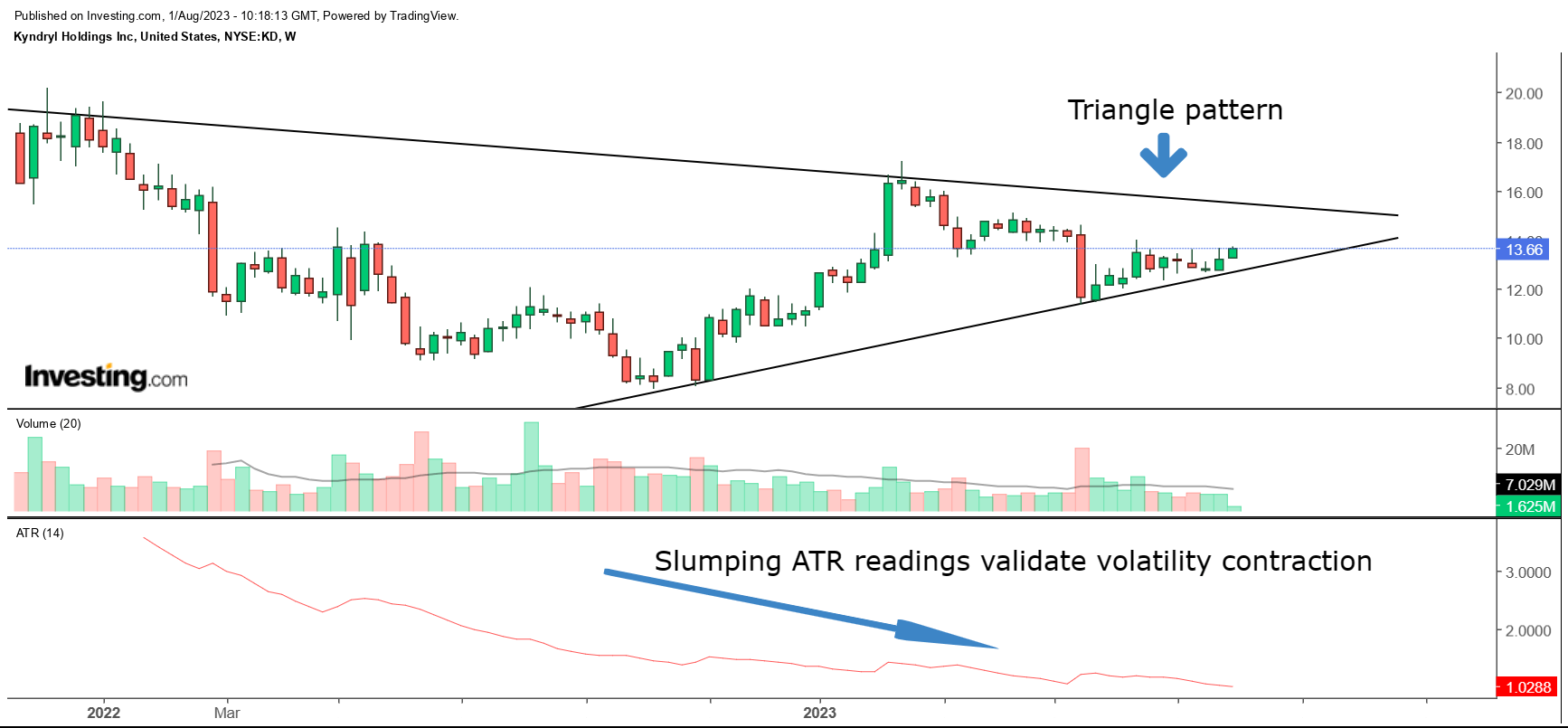

On the weekly chart we can see that this year, the KD stock has largely failed to make any meaningful one-way trending moves, with a lot of choppiness seen through May. Since then, we've seen some small incremental buildup in the price action, but nothing to suggest that the onus is with the bulls.

{kind=link}

Basically, what's quite evident is the formation of a triangle pattern (with two converging upper and lower lines), and the validation of volatility contraction, as exemplified by the lower ATR (Average True Range) readings, which have halved from levels seen in 2022. When you see a triangle, combined with lower ATRs it suggests that the stock is building up for a breakout or a breakdown. With the company's Q1 results just a week away, we could finally have a catalyst that may stimulate the stock to move strongly one way or the other.

For further details see:

Kyndryl: The Improving Financial Profile Warrants Some Re-Rating