LHX - L3Harris: Building Momentum And Fading Headwinds

2024-01-08 22:00:29 ET

Summary

- On December 12, L3Harris held its much anticipated Investor Day, presenting guidance for its mid-term strategy following the post-merger portfolio realignment.

- Across all segments, operating margins are projected to improve by >110bps through 2026, resulting from higher bidding scrutiny and LHX NeXt which saw its anticipated savings guidance raised to $1bn.

- Further insight was offered on capital allocation with management committing >$3.7bn to share buybacks from 2024-2026 at 100% cash return post delevering, alleviating investor concerns post 2023 debt raises.

- Management reacted to D.E. Shaw’s involvement in the company, announcing further operational review and realignment of incentive structures towards shareholder returns.

- Rolling forward my valuation and raising my target multiple to 14.0x, I increase my price target by 18% to $268 per share and make LHX my 2024 Top Pick.

Key Highlights

Strategic Refocus towards Core Assets has created a resilient and profitable Portfolio in Key Defense Growth Areas

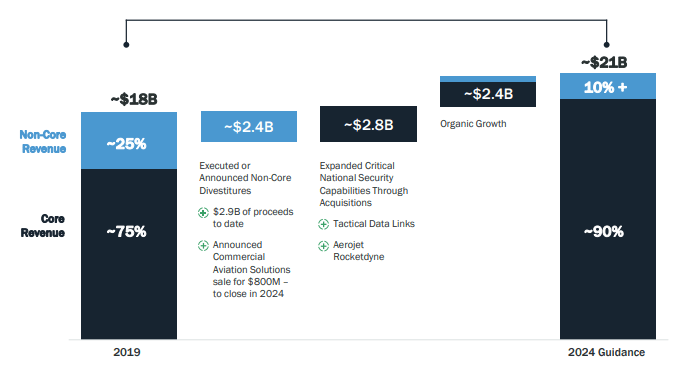

Since the L3 and Harris merger in 2019, L3Harris Technologies, Inc. ( LHX ) has divested c.$2.9bn in non-core assets, latest of which the (pending) $800MM sale of its commercial aviation solutions business announced in November. Simultaneously, the newly combined business has added several assets to its portfolio, looking to expand its footprint into new growth markets such as space (through acquiring AJRD) and strengthen its footprint in communications (TDL acquisition). Through this reshuffle, LHX's revenue base has developed from a rough 75/25 core/non-core split as of the merger to a 90/10 split projected for 2024 (assuming in-time close of commercial aviation solutions divestment).

Revenue Split Core/Non-Core (LHX Investor Day)

{kind=link}

Management has not specified the exact nature of those non-core assets, however, it has been indicated that it the company is continuing to strategically review those areas and is potentially already in preliminary divestment talks. As of current, LHX therefore operates across 4 segments, three of which consolidated from former L3 and Harris divisions and one created in 2023 following the close of the AJRD acquisition.

Current Operating Structure (LHX Investor Day)

{kind=link}

Building on this four segment operational structure and a more balanced split between long- and short-cycle end markets, management during Investor Day conveyed the message that LHX is in the end part of this transition phase. While the previous years saw extensive M&A activity to both simultaneously slim down and selectively enhance the company's footprint, the next phase of management's plan for LHX will be to execute on its new positioning. Building on my strategical assessment from prior notes on LHX (see here and here ), I estimate LHX's competitive footprint to be among the most favorable in its peer group ( LMT , GD , NOC ) through its dedicated focus on high growth end markets in space, missiles and C5ISR in line with its "Trusted Disruptor" strategy.

With management now fully free to execute on this position and only minor portfolio optimization remaining, I estimate significant runway for operational improvements in the years ahead as indicated by the recent launch of the LHX NeXt performance improvement program. Internal initiatives will be supported by the commitment to c.$2bn in annual R&D (o/w 75% customer funded) to further enhance LHX's best-in-class position in resilient communication networks and multi-domain warfare.

LHX NeXt is the next Step in the combined entity to significantly boost Margins in a post-Covid World

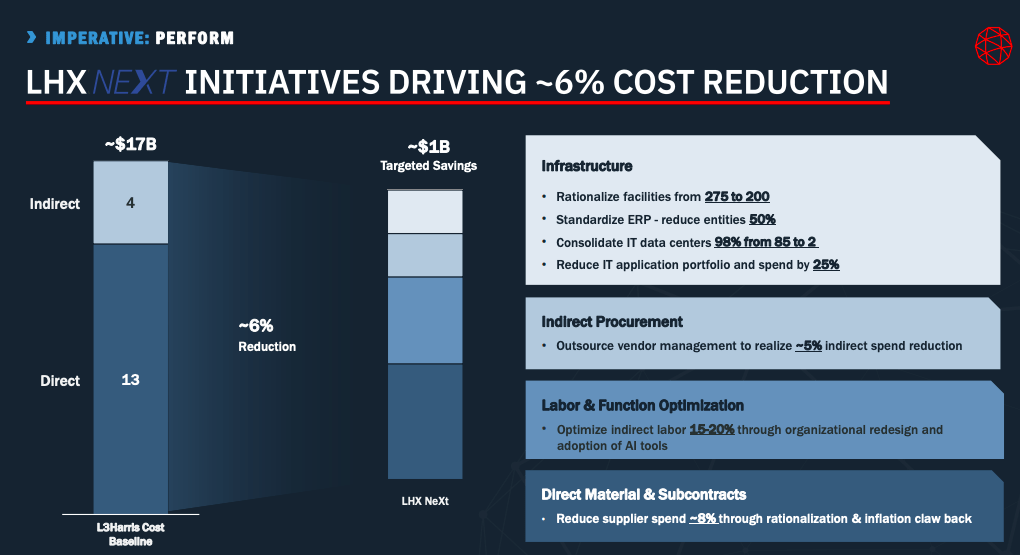

Internally, most of LHX's performance improvements are projected to be achieved through the launch of LHX NeXt which had been rolled out across the firm starting in Q3. Running until 2026, this program seeks to achieve significant cost savings through a combination of organizational rightsizing and leveraging the new scale of the combined company. Costing an estimated $400MM to implement, management expects this to generate an annual savings run rate of $1bn by FY26, around double the previously communicated $500MM and c.6% of the firm's total current cost base of $17bn.

A key component of this at more than 50% is planned to come from reducing procurement costs, both for directly purchased materials and subcontracting. LHX's margins had contracted significantly from higher raw material costs due to the COVID-19 supply chain issues and broad-based wage increases among the workforce of both itself and subcontractors. LHX NeXt aims for a decrease of 8% in direct purchasing and subcontracting costs, achieved through supply chain rationalization and inflation clawbacks, both areas in which the company will be able to leverage its new scale and increase recognition as a US Prime contractor. Vendor management will also be outsourced, delivering an estimated 5% reduction in indirect procurement costs.

LHX NeXt Structure (LHX Investor Day)

{kind=link}

On the internal side, the program does not include direct manufacturing-related job cuts, instead looking to generate incremental efficiencies by slimming down the corporate structure and labor overhead. LHX's geographic footprint will be rationalized from 275 facilities to 200 while IT systems will be harmonized across the entity resulting in a 98% consolidation from 85 to 2 systems. Significant savings potential has also been identified in the company's overhead (indirect) labor force with LHX NeXt aiming for a 15-20% optimization through organizational redesign and targeted adoption of AI tools. To get a sense of the achievability of this, in the SAS segment, where LHX NeXt had been first rolled out, the program was able to cut total overhead labor cost by c.25% in the first 21 months of adoption.

With contributions from LHX NeXt and targeted, segment-specific performance improvements, management expects a baseline of c.110bps of margin expansion across each segment. Additional upside risk comes from a further increasing share of Prime contracts, where LHX's growing capabilities in space will serve as a key growth driver with satellite production for commercial and military users expected to grow almost 5x through 2027, and an announced bidding stop for highly cost-risk exposed fixed price contracts ( "Price to Execute not just Win" ).

With <3x Leverage reached by Q4 24 and New Buyback Allocation, LHX could turn from Laggard to Leader in Shareholder Distributions

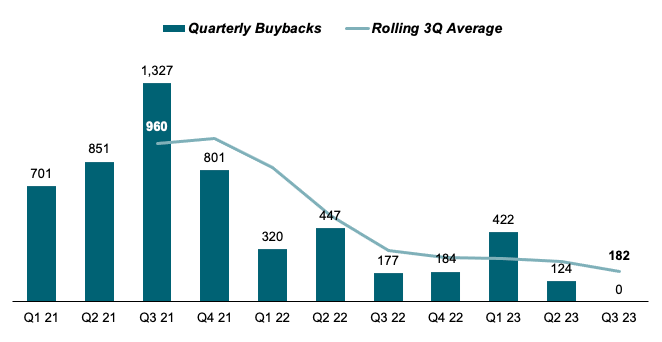

One recent key investor concern regarding LHX and its standing compared to the wider A&D sector has been its comparably low shareholder distributions. In an industry that often generates >100% FCF payout ratios, LHX's buyback profile has gone down significantly in recent quarters with Q3 23 marking the first quarter with no buybacks since the initial merger. Rolling 3Q average has also declined by more than 75% from $960MM in Q3 21 to $182MM in Q3 23.

Buyback Development (Company Filings)

{kind=link}

Compared to its peers, which spent on average 112% of their FCFE on buybacks in the first 3 quarters of 2023, LHX only spent 87%, missing the peer average by a considerable 23%. Much of the recent stress on LHX's buyback capacity comes from the significant leverage it has on its balance sheet, recently growing to 3.7x as of Q3 23 due to debt raises in 2023 to finance the AJRD and TDL acquisitions. Previously having aimed at reaching its target of <3x leverage by the end of 2025, during Investor Day management shifted forward this date to roughly Q4 of 2024, driven by strong anticipated cash generation and proceeds from divestments.

Projected Leverage Development (LHX Investor Day)

Next to this, management also announced the potential for upwards of $3.7bn in buyback capacity through 2026, which together with $2.6bn allocated to sustaining and growing its common dividend would equal a FY24-26 FCF payout ratio of c.78% (including proceeds from divestitures).

FY24-26 Capital Allocation (LHX Investor Day)

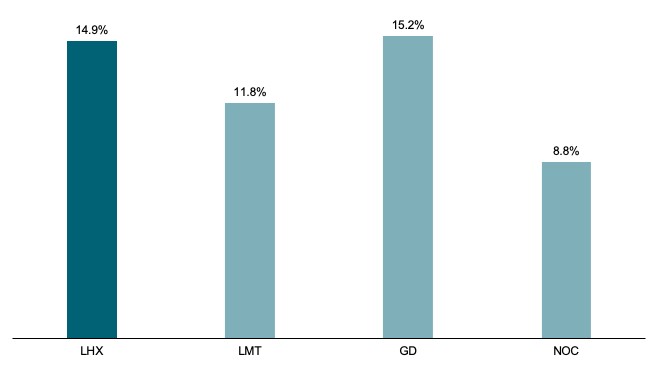

Assuming a buyback capacity of stated $3.7bn and market cap as of current, management could retire roughly 9% of outstanding shares through FY26. While this would still rank around 20% below peers' authorized or assumed potential average buyback capacity over the period (12%), I estimate a significant upside to these numbers through further divestitures. As mentioned, management still sees c.10% of non-core revenue in FY24. Based on Investor Day guidance of c.$21bn in FY24 revenue and assuming a 1x sales multiple, this could add around $2.1bn in additional buyback capacity, pushing FY24-26 buyback yield to c.15% or 25% above my estimated peer average.

Potential FY24-26 buyback yield vs peers assuming total divestment of non-core activities (LHX Investor Day, S&P Market Intelligence)

{kind=link}

While it is not clear yet that those divestments will happen and, how the cash proceeds will be allocated, I view both assumptions as reasonable given management's commentary on further streamlining the business and the recent investor push to grow focus on shareholder returns (see below). Along with largely derisking investor concerns about LHX's lack of shareholder returns, such announcements could further serve to turn the story upside down, giving LHX among the strongest distribution profiles in its peer group and paving to way to significant EPS upside through FY26 and beyond.

D.E. Shaw initiated Business Review and Board Additions to provide additional Upside beyond Investor Day Targets

On December 11, LHX announced it had struck a deal with major global hedge fund D.E. Shaw which will see the company adding two new members to its board and agreeing to a review of its "operational performance". Both new board members have significant industry and leadership experience with Kirk Hachigian being former CEO of electrical manufacturer Cooper Industries and William Swanson having formerly served as industry peer Raytheon's CEO from 2004 to 2014, a period which saw the company's stock price grow at an annual CAGR of 12%. An additional independent director is to be added in the course of 2024.

The operational performance review will primarily focus on the areas of performance, cost structure and portfolio composition and is expected to be completed in 2024. Notably, all of the areas cited by D.E. Shaw have also been key aspects of management's communication during the Investor Day, suggesting some previous discussions between investors and board. Next to operational performance, the review will also entail an adjustment to management incentive structures to incorporate total shareholder return as a new core metric. While hedge fund activism is often frowned upon, I view this involvement as a strong signal to the market and estimate significant further upside above LHX's investor day margin targets from the review. Specifically concerning capital allocation and portfolio composition, I view it as greatly supportive of the thesis I laid out above assuming a full non-core divestment to further grow LHX's buyback capacity.

Valuation

I continue to value LHX by applying a multiple on my estimate for EBITDA, now rolling forward my valuation to FY24 to incorporate additional guidance offered during the investor day.

LHX Financial Model (Company Filings and Author's Projections)

{kind=link}

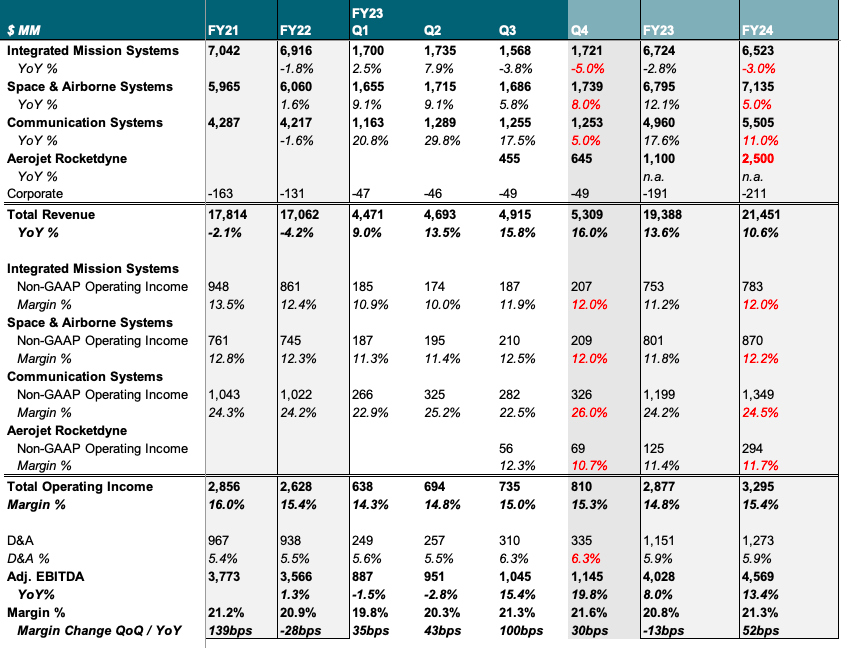

For IMS, I estimate FY24 YoY growth of -3% to c.$6.5bn which is in line with management guidance of mid $6bn. It should be noted that this segment previously held the CAS business (revenues undisclosed), thus organic revenue growth will still be positive. For margins, I estimate an expansion to c.12% on the back of LHX NeXt implementation and further easing supply chain pressures which is in line with Q3 and Q4 24.

In SAS, I model 5% YoY revenue growth to reach c.$7.1bn, again in line with LHX guidance although I see some upside potential from an earlier-than-expected ramp-up in security-grade microelectronics. On the margin side, I project a YoY 40bps expansion to 12.2%, slightly above Q3 and 4 24 and largely related to LHX NeXt implementation.

In CS I see the largest potential upside to management guidance of low-mid $5bn and estimate a higher YoY growth of 11% for FY24 segment revenue of $5.5bn, driven by the segment's higher exposure to international customers, specifically its strong footprint in Saudi Arabia which should profit from the further raised tensions in the Middle East following the Israel-Hezbollah border dispute, the Iran bombings and the issues in the Red Sea. I also see some margin expansion of c.30bps YoY helped by the higher profitability in international contracts.

Given the lack of history, I largely stick to LHX's guidance for the AR segment and estimate in-line $2.5bn of FY24 revenue at a slightly expanded margin of 11.7% (20bps YoY).

Overall, I model c.$21.5bn in FY24 revenue (10.6% YoY) with the headroom to $21bn guidance largely arising from the outperformance potential I see in CS' international operations. I calculated the total FY24 operating margin at 15.4%, around 40bps above guidance (c.15%), helped by recent strong margin performance in IMS and SAS, the rollout of LHX NeXt, and the higher margin profile of CS' international contracts. Assuming a D&A ratio of 5.9% of revenues in line with FY23, I estimate FY24ae EBITDA at around $4.6bn (up 13.4% YoY) at a margin of 21.3% (up 50bps YoY).

On a valuation side, I raise my target EV / FY24 EBITDA for LHX to 14.0x, representing a 5% premium to peer average of 13.3x which I view as warranted given the combination of three factors:

I) Best-in-class competitive positioning in key growth markets of space and C5ISR, strong growth in higher-profitability international footprint and margin leadership vs peers

II) Investor Day both laying out a clear and credible path to margin re-expansion and derisking investor concerns on near-term leverage and capital allocation

III) D.E. Shaw's involvement offers further margin upside potential through the 2024 business review while adding experienced new leadership incentivized by shareholder return

Applying this multiple to my FY24ae EBITDA, I calculate an Enterprise Value of $64bn and a fair equity value of $61bn. On a per share basis this translates to a new price target of $268 (up by 18% vs my last note) and a current upside potential of c.31%.

LHX Multiple Valuation (Company Filings and Author's Projections)

Wrap-Up and Outlook

After a period of reshuffling and heightened investor scrutiny due to falling margins and rising debt levels, I think management has done a tremendous job during the Investor Day of laying out its strategic vision for the next period in the company's history. With a clear path to margin expansion (including a raised savings guidance for LHX NeXt) and faster than expected delevering freeing up cash to reaccelerate buybacks to c.9% of current capitalization through FY26, I think management has been able to sufficiently derisk most investor concerns around the stock, paving the way for the market to rerate LHX according to its best-in-class end market positioning and margin levels.

For further details see:

L3Harris: Building Momentum And Fading Headwinds