LHX - L3Harris Q3: Widening Valuation Gap Despite Solid Execution On-Track Aerojet Integration

2023-11-03 06:25:57 ET

Summary

- L3Harris reported its Q3 results on October 27, beating estimates on top- and bottom-line.

- Next to a solid 3% YoY organic revenue growth, Q3 saw a second sequential quarter of margin expansion due to the roll-out of enterprise-wide initiatives and easing operational pressures.

- Closing of AJRD acquisition pushes consolidated backlog to record $32bn, with a slight caveat in declining QoQ organic backlog and orders falling 10% QoQ.

- With most of US defense peers seeing a rerating following the military escalation between Israel and Hamas, LHX's valuation gap vs peers has widened to 19% based on FY23ae EBITDA.

- I continue to view this discount as not fully justified and increase my price target to $218 based on an updated 13.5x EBITDA multiple and management guidance of $1bn+ in FY23 revenue from AJRD.

On October 27, L3Harris Technologies (LHX) issued its latest quarterly filing for Q3 of 2023, revealing what I believe are very solid figures and well representative of the investment thesis I laid out in my initiation article ( L3Harris : Trading at a Discount Despite Favorable Competitive Positioning and M&A Upside), beating estimates on both top- and bottom-line in the process. Notably, LHX did not participate in the sector-wide rerating following the Hamas-Israel conflict that saw surging multiples for US defense prime peers Lockheed Martin (LMT), General Dynamics (GD) and Northrop Grumman (NOC) with the gap to peer average EV/FY23 EBITDA now standing at 19% based on my projections for LHX FY23 EBITDA. I continue to view this gap as not fully justified as, despite the higher debt levels which will put management's near- and mid-term focus on debt repayment rather than growing shareholder distributions, execution remains solid with slight organic topline growth and continued re-expansion of margins, partially offset by a slowdown in new orders which I however expect to be only of temporary nature.

Performance Highlights

From a topline perspective, quarterly performance has been solid but not outstanding with 3% YoY organic growth increasing to 16% when accounting for pro-rata revenues generated by Aerojet (AJRD) in the newly created business segment as well as the inclusion of acquired Tactical Data Links "TDL" in the CS division. Adjusted operating margin has expanded slightly by 20bps to touch the 15% mark for the first time since Q3 22, mainly driven by 190 and 110bps increases in IMS and SAS segment margins respectively, the latter of which attributed mostly to an early adoption of LHX NeXt and favorable one-time effects. CS saw an on-paper decline in profitability mainly due to the integration of TDL into its revenue figures and new division AJRD came in at 12.3% (10.5% if not accounting for c.$8MM of one-time PPA gains).

On a more negative note, order flow has been somewhat subdued during the quarter with new orders (excl. AJRD) coming in at slightly above $5bn, down c.10% from Q2 to stand at a quarterly book-to-bill of just above 1. Standout wins include a $200MM prime contract to deliver underwater tracking for the Australian Navy and several funded contracts in upgrading US Air Force combat platforms such as the F-35 and B-52 which are worth a combined $250bn.

To acquire AJRD, LHX has also significantly increased its debt position by adding c. $4.7bn through offerings of 3,10 and 30-year maturity senior notes (totaling $3.3bn) and a $1.5bn raise by increasing the scope of the outstanding commercial paper program. Total debt ending the quarter stood at $13.5bn with net debt just over $13bn for a net leverage ratio of 3.7x.

Key Takeaways

AJRD to Contribute $1bn+ in Revenue for FY23

With the inclusion of 5 months of AJRD, management has increased its FY23 guidance to now call for revenues of $19.2-19.4bn. With LHX stand-alone business guidance unchanged from Q2 at $18-18.3bn this puts expected AJRD pro-rata revenues at c.$1-1.2bn for the months August to December. Management has also updated its operating profit guidance to account for c.$120MM provided by AJRD at a c.11% margin, bringing expectations for company-wide FY23 margin to around 14.8%. Q3 saw a 12.5% margin for the division, however this was skewed to the upside by accounting for c.$8MM of PPA with management expecting an organic operating margin of c.10.5% for Q4.

During the analyst call, management has also restated their confidence in the combined entity being able to increase deliveries at a faster pace than a stand-alone AJRD by means of better sales channels and redesign of previous LHX facilities, guiding for a noticeable ramp-up in output from FY24 onwards. Another key focus area has been cited in working to increase AJRD's supplier base which still has meaningful bottlenecks especially in nuzzles and igniters. Overall, I remain highly confident in the segment going forward due to the consolidated company's stronger negotiating position in contracts and the additional visibility being part of LHX brings to AJRD.

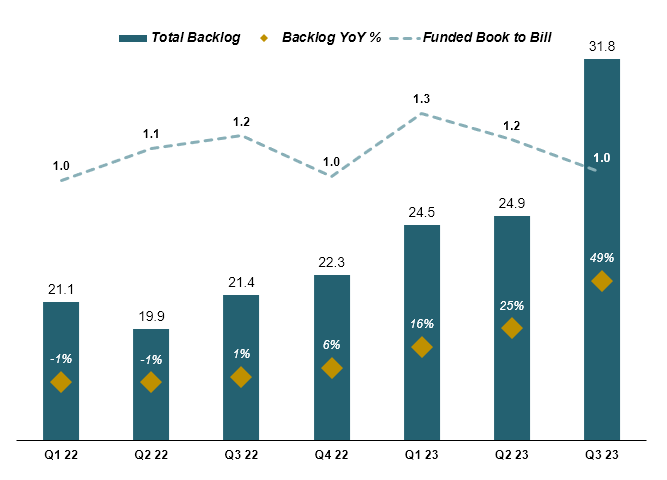

AJRD Pushes Backlog to Record $32bn, Standalone LHX Backlog Flat QoQ

With the addition of c.$7bn of new backlog from the AJRD acquisition, total consolidated backlog has grown to almost $32bn, up 49% compared to Q3 22 and up 28% vs Q2. One key point to highlight here is the strategic and longer-cycle nature of this additional backlog which I, as laid out in my prior note, expect to greatly benefit earnings visibility going forward.

Consolidated Backlog Incl. AJRD (Company Filings)

{kind=link}

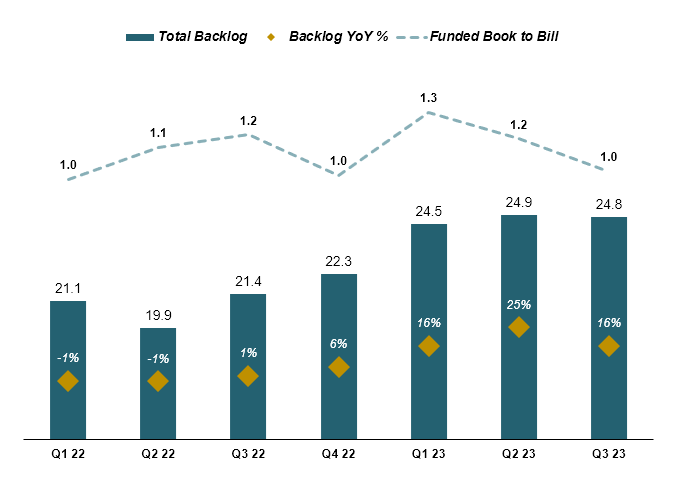

When excluding AJRD however, order situation looks a bit weaker with stand-alone LHX backlog down slightly vs the previous Q for the first time since Q2 22. YoY backlog growth subsequently dropped to, a still strong, 16%, down from 25% for Q2. Book to bill has also receded from its recent heights and is touching the 1.0x mark. This is a development which I did not expect and thus a bit worrying at first, however I do believe the significant global developments during the period, mainly increasing threat levels in the Middle East following the Israel-Hamas incursion will help reverse this slowdown in the coming Qs as LHX has strong business relationships with several ME governments including local top dog Saudi Arabia.

Stand-Alone Backlog Excl. AJRD (Company Filings)

{kind=link}

Margins Seem to have Bottomed and Now Give Ample Room for Expansion

Q3 has seen the second consequential quarter of margin improvement, which gives me the confidence to call a bottom on operating margins during Q1 23. Next to improvements across the supply chain, management has also cited roll-out of the short-term Performance First program and early benefits from LHX NeXt as key factors. I do see some minor near-term setback as AJRD and SAS segments should come in lower due to non-recurring one-time effects during the period and expect Q4 operating margins more around Q2 levels.

LHX Operating Margin Development (Company Filings)

Going forward I continue to see two main levers for LHX to stabilize and expand margins in both, fully realizing projected synergies from the AJRD acquisition and continuing the post L3-Harris merger transformation by means of the NeXt program. During the Q3 analyst call, management has reconfirmed its expectations to realize a run-rate of $40-50MM in annual cost savings from eliminating double competencies and leveraging L3Harris tools to drive operational efficiency in the new AJRD unit. It also reaffirmed its projection for LHX NeXt to generate total run-rate savings of $500MM+ from FY26 through a network of operational improvements and streamlining across the entire business. Some of those have already started to be implemented with the creation of a more centralized HR and a start to the rollout of new IT systems, both expected to generate meaningful overhead savings going forward.

Debt Repayment the Near-Term Priority

With more than $4.7bn in new debt issued during the quarter, a significant portion of which short-term, management has been steadily reminding investors that reducing this is their number one priority for the coming years and quarters. For Q4, management guides to a closing debt level around $13bn at 3.5x leverage which is projected to reduce down to c.3x over the next couple of years. Clear repayment focus will hereby lie in the short-term portion of the newly issued debt due to less favorable and variable interest rates.

Valuation Update

The main change in model and valuation arising from Q3 is the inclusion of the new segment which is AJRD as well as the addition of the $4.8bn in new debt issued to finance the transaction. On a topline base I expect full year revenues of c.$19.4bn in line with management guidance of which $1.1bn are attributable to AJRD. QoQ growth should be positive for all divisions except CS where I project a small QoQ decline due to upwards skewed Q3 comps (TDL acquisition). From a margin perspective I expect an overall slightly weaker Q4 mainly given my reasoning above. In the IMS segment I see a small 10bps expansion given management stating they " largely solved" operational challenges from H1, all while remaining clear that it will remain a "lumpy part" of LHX' portfolio for the coming Qs. For AJRD I expect Q4 to be slightly above the organic (not accounting for the PPA) print we saw in Q3 at c.10.7% to bring FY23 operating income to $125MM at 11.4% margin. SAS should also come in a bit weaker at 12% as one-time effects helped the 110bps growth in Q3. Finally, I project CS to be the star of the show for Q4 with margins expanding to 26% as management had guided earlier to a strong Q4 which would be offset on a full year basis by a weaker Q3 but should still deliver a FY23 segment margin in-line with FY22. On an enterprise-wide level I thus estimate a total FY23 operating margin of 14.8% at roughly management guidance. Accounting for a slightly higher D&A rate following the AJRD acquisition, I now project a total FY23ae EBITDA of $4,028MM, up 8% YoY with EBITDA margins having contracted slightly by c.10bps due to a particularly weak H1.

LHX Financial Model Q3 Update (Company Filings and Author's Projections)

For my valuation I continue to use a multiple approach with a peer-derived EV multiple applied to my FY23ae EBITDA forecast. Compared to my previous note, I am assigning LHX a slightly higher multiple of 13.5x (vs 13.0x prior) given the overall rerating in the US defense sector following the Hamas-Israel incursion and heightened regional and global threat levels. Target multiple discount to peers ( LMT , GD , NOC ) average of 14.3x has slightly expanded to a high mid-single digit percentage to reflect higher debt levels and mid-term focus on debt repayment. Using this valuation method yields an Enterprise Value of $54.4bn which, adjusted for net debt and minority interests, translates to a 1% higher new target price of $218 or around 19% upside to current. The DCF-based price target I presented in my initiation to give a view on LHX' long-term value remains unchanged and will probably require more meaningful input concerning long-term margin development.

LHX Multiple Valuation Q3 Update (Company Filings and Author's Projections)

Wrap-Up & Outlook

Overall, I thing LHX delivered a very solid performance for the Q3 period in terms of top- and bottom-line expansion and a well under-way AJRD integration with some minor hiccup from a slowdown in order growth and QoQ backlog decline. Management has remained largely unchanged regarding expected Q4 figures but did deliver some new insight into what AJRD will add to the combined entity.

I think the next major catalyst that investors should look ahead to going forward will be the company's investor day, scheduled for December 12. Management has stated that this will offer additional visibility into the company's long-term strategy, especially considering the two major acquisitions we saw in FY23 and the long-term impacts of the recently launched NeXt program. On a more mid-term basis, I think the most crucial part of the LHX equation will remain the question of how quickly the added and existing debt stack can be paid down and I advise investors to keep track of this during the next quarters with Q4 earnings coming in late December.

For further details see:

L3Harris Q3: Widening Valuation Gap Despite Solid Execution, On-Track Aerojet Integration