LHX - L3Harris Technologies: A Powerful Dividend Growth Stock To Buy Now

2024-01-08 07:30:00 ET

Summary

- Since emerging from the merger between L3 Technologies and Harris Corporation in 2019, L3Harris has been an exceptional dividend grower.

- The defense contractor and aerospace multinational's revenue and backlog soared in the third quarter.

- L3Harris is making progress on deleveraging to strengthen its balance sheet.

- The company could be priced at an 11% discount to fair value from the current share price.

- L3Harris could outpace the S&P 500 both through 2025 and in the coming 10 years.

As a dividend growth investor, one of the most important attributes to me is a track record of vigorous dividend growth. Of course, a pattern of rewarding shareholders in the past doesn't always perfectly correlate to a future of rewarding shareholders when the fundamentals deteriorate (Walgreens Boots Alliance's ( WBA ) dividend cut , anybody?).

But in this rapidly changing world, I have found the dividend growth strategy to be a winner for me. That's because it keeps me as focused as a human being can be on fundamentals rather than market sentiment. This is why I believe a track record of dividend growth and promising future fundamentals are arguably the two best predictors of whether a dividend growth streak can continue. These two variables together demonstrate both the commitment and ability to grow a payout.

With that in mind, I want to focus on L3Harris Technologies ( LHX ) today. For the first time since June 2021 , I will revisit the company's fundamentals and valuation to discuss why I am maintaining my buy rating for this excellent dividend grower.

{kind=link}

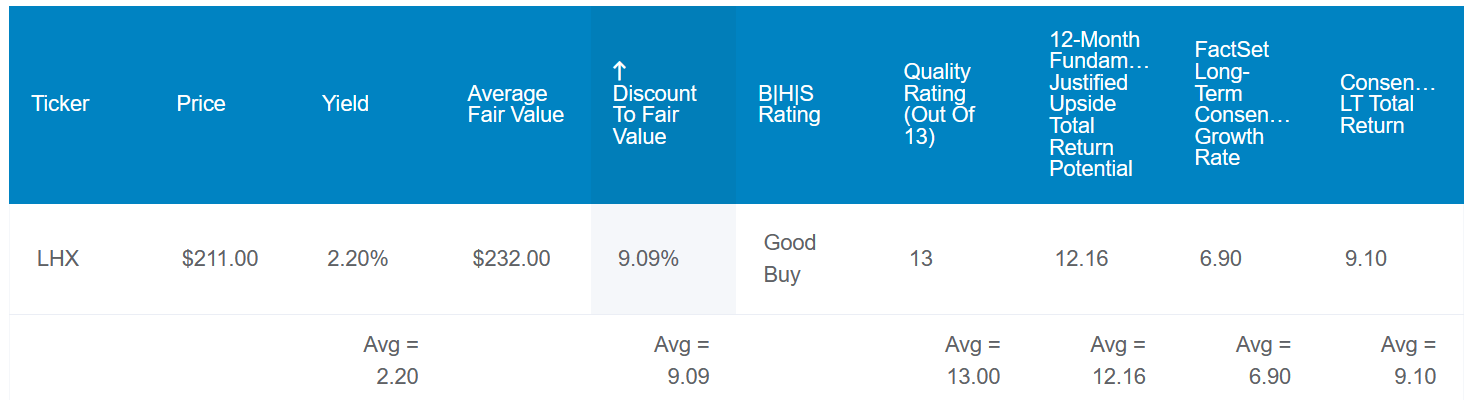

L3Harris' 2.2% dividend yield doesn't jump off the page in an environment when cash is yielding 4% or higher. However, this is a better entry yield than the 1.5% yield of the S&P 500 ( SP500 ).

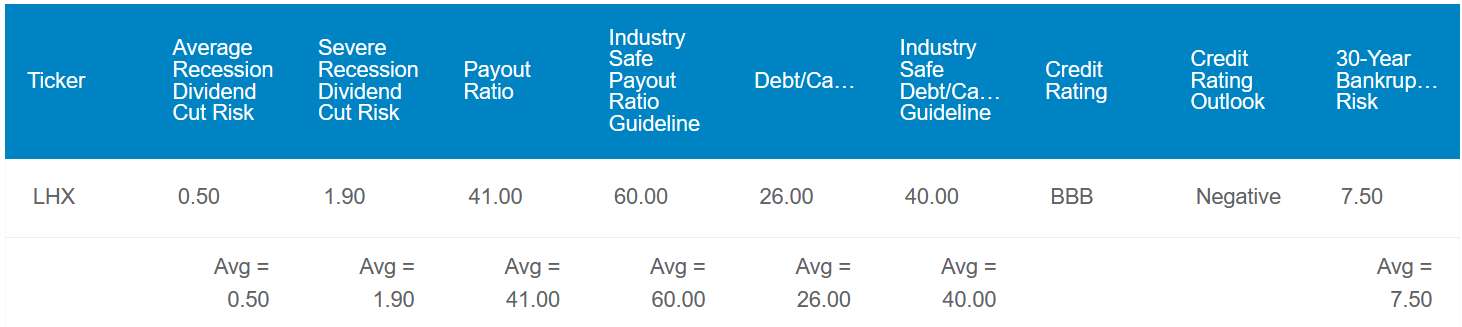

There are also reasons to believe that L3Harris can keep growing its dividend at a healthy clip moving forward. For one, the company's 41% EPS payout ratio is meaningfully below the 60% EPS payout ratio that rating agencies consider to be safe for the defense contractor industry. That builds a sizable margin of safety into the payout.

Additionally, L3Harris' 26% debt-to-capital ratio is below the 40% debt-to-capital ratio preferred by rating agencies (and the company is working on further reducing its debt). This is how the defense contractor and aerospace company earns a BBB credit rating from S&P on a negative outlook. That implies the risk of L3Harris going to zero over the next 30 years is somewhere around 7.5%.

For these reasons, the estimated probability of the company cutting its dividend in the next average recession is just 0.5%. In a severe recession, that rises to a still reasonable risk of 1.9%.

{kind=link}

L3Harris' shares have been flat in the past year, which I don't believe is justified by the fundamentals. In averaging out its historical dividend yield and P/E ratio, shares of the defense contractor could be worth $232 each. Relative to the $206 share price (as of January 5, 2024), L3Harris appears to be 11% undervalued.

If the company were to grow as expected and revert to fair value, here are the total returns that it could generate in the next 10 years:

- 2.2% yield + 6.9% FactSet Research annual growth outlook + a 1.2% annual valuation multiple boost = 10.3% annual total return potential or a 167% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

L3Harris Is Fundamentally Well

L3Harris Q3 2023 Investor Letter

When L3Harris shared its financial results for the third quarter ended September 29 in late October, it did what great businesses routinely do: Exceeded analysts' forecasts. The company's revenue climbed 16% over the year-ago period to $4.9 billion during the quarter. That came in $50 million ahead of the analyst consensus.

Two factors drove the bulk of this topline growth: The company's deal for Tactical Data Links and the acquisition of Aerojet Rocketdyne. Backing acquisitions out of the equation, L3Harris' organic revenue edged 3% higher in the third quarter.

Overall, the company grew revenue in two out of three operating segments. Space & Airborne Systems climbed 6% for the third quarter to $1.7 billion. This was due to new program ramps in its space and intelligence and cyber businesses and record backlog. Thanks to the Tactical Data Links acquisition, Communication Systems segment revenue grew by 18% to $1.3 billion. That was also aided by increased demand for tactical communications and greater availability of electronic components for its products.

The Integrated Mission Systems segment experienced a 4% dip in revenue to $1.6 billion during the third quarter. That was related to revenue timing more than anything else. As I previously alluded, the remainder of the revenue ($455 million) stemmed from the completion of the Aerojet Rocketdyne acquisition.

L3Harris' non-GAAP EPS decreased by 2.1% over the year-ago period to $3.19, which topped analysts' predictions by $0.16. Higher pension expenses and interest expenses were the elements that contributed to these results.

The most encouraging sign for the future during the quarter was news of the company's backlog. L3Harris' backlog soared 49% year-over-year to $31.8 billion to end Q3 2023. Geopolitical instability around the world has made natural security a top priority. Given L3Harris' trusted reputation within its industry, it's not a surprise that the demand for its products is soaring in this environment.

L3Harris Q3 2023 Investor Letter

One of L3Harris' few weaknesses is its balance sheet, but the company has taken notice and is committed to addressing this weak point. The company's net debt to adjusted EBITDA was 3.7 as of September 29. Through a combination of growth and $3 billion in planned debt repayment, L3Harris intends to reduce its leverage to below 3.

The Dividend Has Room To Fly Higher Over Time

Since its formation in 2019, L3Harris' quarterly dividend per share has surged 52% higher to the current rate of $1.14 . The most recent dividend raise of 1.8% last February was the 22nd consecutive year of dividend growth (including its pre-merger dividend growth streak). Until L3Harris reaches its leverage target over the next couple of years per CFO Michelle Turner's remarks during the Q3 2023 earnings call , I would anticipate dividend growth will be modest.

The good news is that once the company does so, it has the free cash flow to return to high-single-digit dividend growth annually. L3Harris generated $1 billion in free cash flow through the first three quarters of 2023. Against the $652 million in dividends paid in that time, this equates to a 65.5% free cash flow payout ratio (info per page 7 of 63 of L3Harris' 10-Q filing ).

Risks To Consider

L3Harris is a quality business, but it has the risk profile that I expect from a defense contractor.

For one, the company derived 74% of its sales from the U.S. government in 2022 (page 7 of 157 of L3Harris' 10-K filing). This exposes the company to concentration risk. If a government shutdown were to occur, this could weigh on L3Harris' operating results. In the long term, the more pressing threat is the potential that U.S. spending priorities could shift. If this happened, L3Harris' growth prospects could be negatively impacted.

Another risk along the same lines is the possibility that cost overruns on projects could hurt the company's results. This is because 73% of L3Harris' total revenue came from fixed-price contracts in 2022.

Summary: A Superb Dividend Grower At A Reasonable Valuation

{kind=link}

{kind=link}

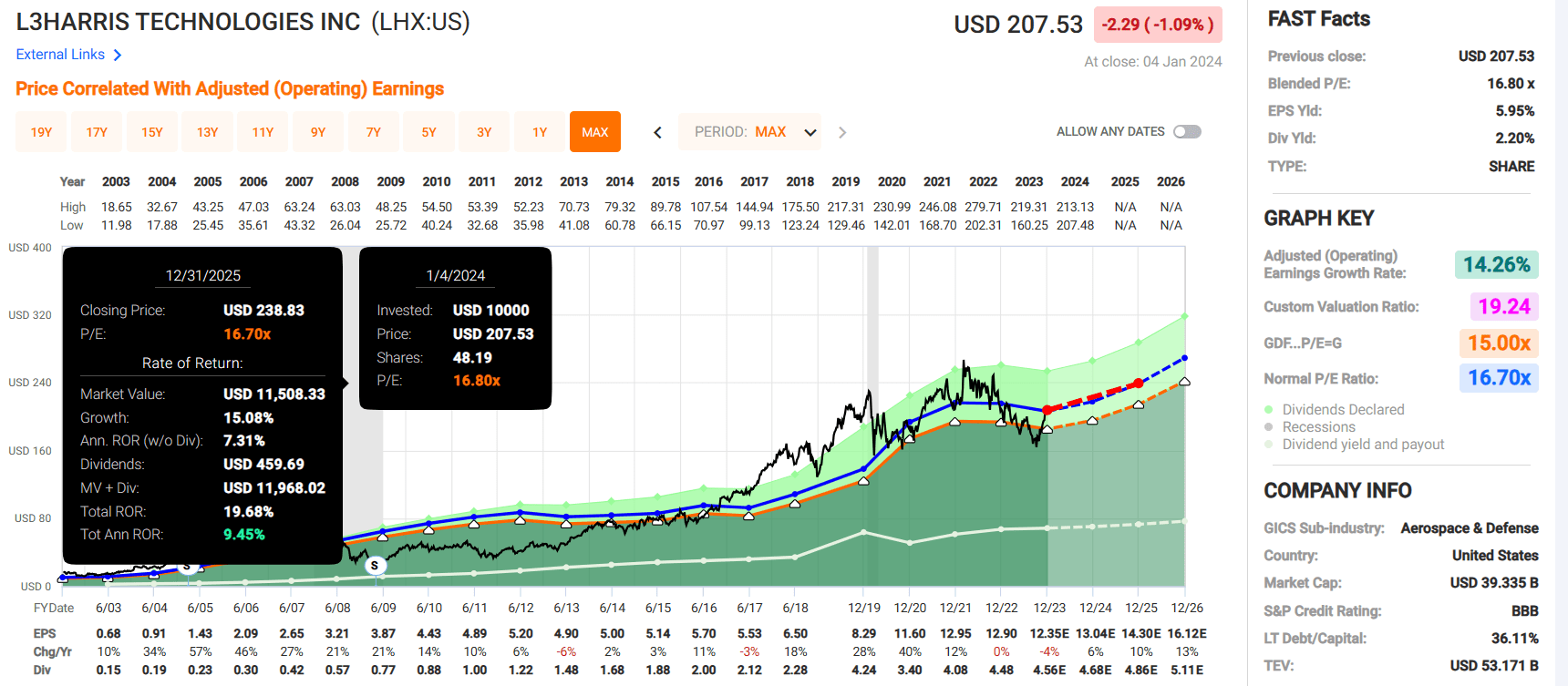

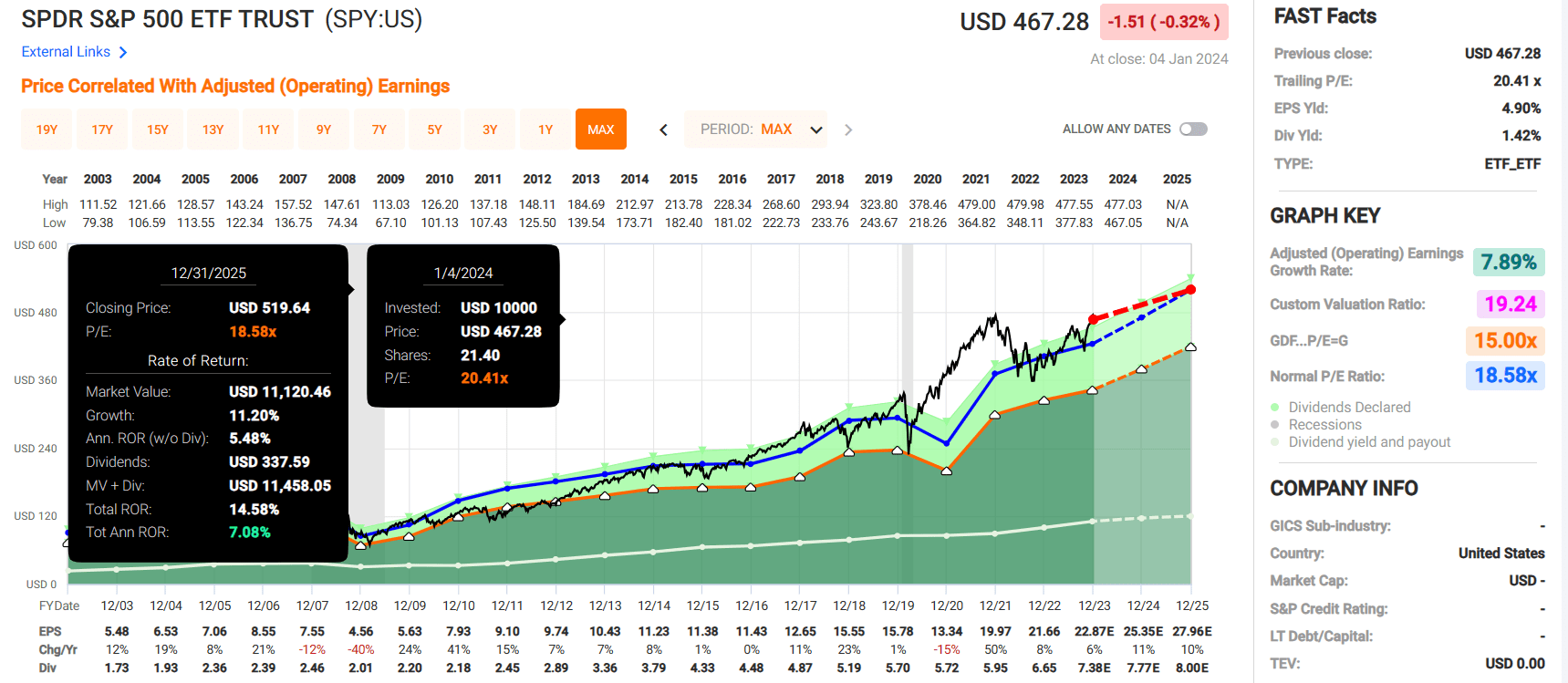

L3Harris' blended P/E ratio of 16.8 is about in line with its normal P/E ratio of 16.7 per FAST Graphs. If it were to remain around its current valuation and grow as projected, L3Harris could generate 20% cumulative total returns through 2025. That's superior to the 15% cumulative total returns projected for the SPDR S&P 500 ETF Trust ( SPY ) over that time. This is why I am reiterating my buy rating for L3Harris.

For further details see:

L3Harris Technologies: A Powerful Dividend Growth Stock To Buy Now