LHX - L3Harris Technologies: Buy The Dip On This Defense Stock

2023-07-28 12:02:03 ET

Summary

- L3Harris Technologies gets a buy rating today.

- Positives: dividend yield above sector average, valuation moderate or below sector average, capital & liquidity is high, share price dip below 200-day SMA a buying potential.

- Headwinds: Significant YoY drop in net income and EPS.

- Risks are caps in US defense spending, offset by growth in global and NATO spending.

Research Brief

A few months ago, I got to attend the Adriatic Sea Defense & Aerospace (ASDA) Exhibit in coastal Croatia, and this sparked a renewed interest in the homeland security sector along with researching all the various technology innovations in this space including ground, air, and maritime systems.

This brings me to today's research article covering a major player in that sector, L3Harris Technologies ( LHX ), who just had their Q2 earnings results released this week on July 26th, and what better time to take a moment to analyze those results and determine if this is a value opportunity for my readers, as a firm that transcends the realm of innovation / technology & security

Some notable points about this firm, from its company website : operates 3 business segments including integrated mission systems, space & airborne systems, & communication systems. 46,000 employees. Acquisition of Aerojet Rocketdyne ( AJRD ) currently pending. A major project this firm is part of, for example, is the US Department of Defense tactical radio modernization initiative.

Ratings Methodology

Our goal is to find undervalued stocks of companies with solid financial fundamentals, that pay competitive dividend yields. Our key industry focus is tech, financials, insurance, and innovation.

To simplify my rating of an equity, I have broken it down into whether I would recommend or not recommend based on these individual factors:

- Valuation vs Sector Average.

- Dividend Yield vs Sector Average.

- Positive YoY Net Income Growth.

- Capital & Liquidity Strength

- Stock Price vs 200 Day SMA.

If I recommend on all 5 categories, it is a "strong buy", 4 categories is a "buy", 3 is a hold, and less than that is a sell rating. Then I compare my rating to the consensus ratings from Seeking Alpha & Wall Street.

Valuation vs Sector Average: Recommend

When it comes to this stock, I consider it reasonably valued and the valuation data shows it. We will discuss the GAAP-based forward P/E and forward P/B ratios, and compare to the sector average.

When looking at the forward P/E, it is at 22.88, earning it a "C" grade from Seeking Alpha, and being close to 11% above the sector average.

L3H - P/E ratio (Seeking Alpha)

My own target range is that the P/E of a stock be at or below the sector average, or no more than 10% above average. This stock slightly skirts above that range, so I think it is slightly overvalued on price to earnings, being close to 23x earnings while its sector is closer to 21x earnings.

However, it makes up for it in terms of price to book, where you are looking at a share price that is 2x book value, and the good news is that this is almost 24% lower than the sector average, which is closer to 3x book value.

L3H - P/B ratio (Seeking Alpha)

So, when looking at these two valuation metrics together, based on the data I recommend this stock in terms of its current valuation.

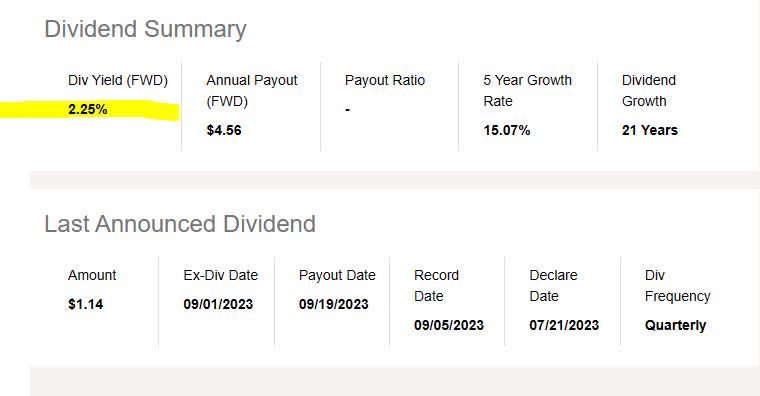

Dividend Yield vs Sector Average: Recommend

As of July 27th, this stock's dividend yield is modest, I would say, at 2.25%, with a quarterly dividend of $1.14 per share, and an upcoming ex-date on September 1st that investors can still take advantage of.

{kind=link}

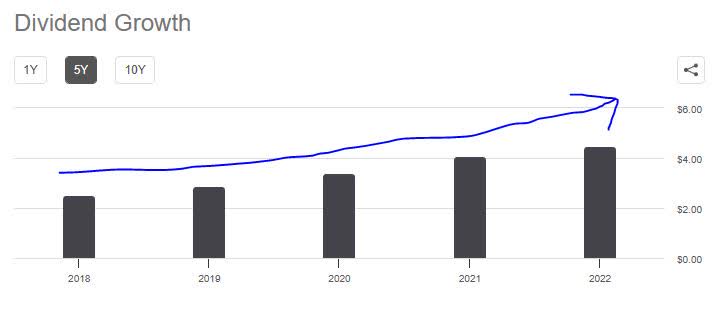

In addition, I like their 5-year positive dividend growth rate, which went from an annual dividend of $2.51 in 2018 to $4.48 in 2022, a 78% increase over 5 years. This is good news for dividend-oriented investors & analysts like myself, as it shows a longer-term positive uptrend in returning capital back to shareholders, an important metric I look for in companies.

{kind=link}

Notable to mention is that the dividend yield, which earned a "B+" grade from Seeking Alpha, is nearly 50% higher than its sector average, another key metric to look at. Consider that the sector average dividend yield is just 1.5%. After rating some recent bank & insurance stocks that were well over 5% yield, this may seem paltry in comparison, but then again it is a completely different industry than banking & insurance.

L3H - dividend yield vs sector avg (Seeking Alpha)

For example, major defense contractor Northrop Grumman ( NOC ) has a dividend yield of just 1.64%, while Lockheed Martin ( LMT ) is just slightly higher than L3H with a yield of 2.65%.

If you want over 5% yields, this generally is not the industry to invest in, however we can still achieve full-year dividend income from a stock like this, and will illustrate this later in our investing idea simulation.

With that said, we certainly recommend this stock as a dividend play due to the yield being above sector average.

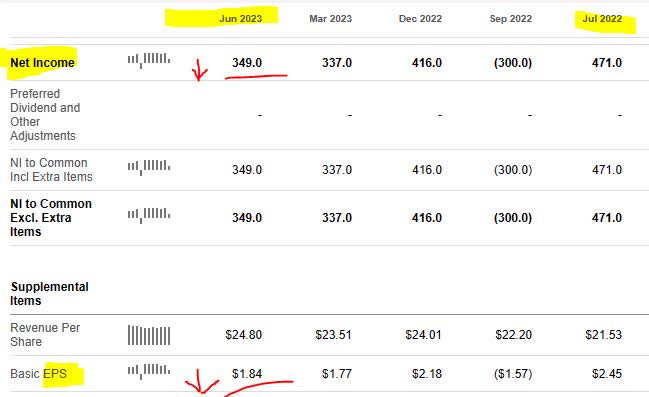

Positive YoY Net Income Growth: Not Recommended

This week was the company's Q2 earnings call so let's look more closely at the data from their official release .

It is possibly what drove the share price down on the 27th after investors reacted to the earnings data, but nevertheless the firm saw a significant YoY drop in both net income and earnings per share which should be noted.

In fact, net income went from $471MM to $349MM. In addition, looking at the overall trend over the last 4 quarters it has been lopsided rather than growing at a steady pace.

{kind=link}

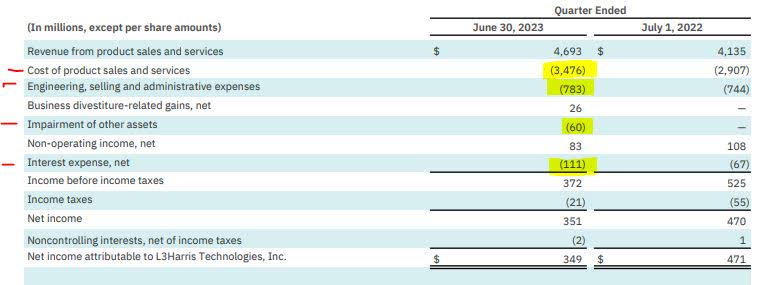

On closer look, these results do not appear to be driven by drops in top-line revenue, which actually increased YoY, but rather costs. Consider the following from the consolidated income statement for Q2:

L3H - consolidated Q2 income statement (L3H - q2 presentation)

{kind=link}

As you can see, the top line revenue grew YoY, but net income was impacted by costs, impairments, and increased YoY net interest expense.

Until the firm gets a better grip on that cost side, currently I don't recommend the stock in the category of net income growth, however I am optimistic about improvement in Q3 results.

Capital & Liquidity Strength of Company: Recommend

When evaluating this company's capital & liquidity health, we will use their own data from the Q2 earnings presentation .

This company shows evidence of returning capital back to shareholders in the form of dividend payouts and share repurchases. Consider in their earnings commentary they mentioned:

$216 million in dividends in the second quarter; $436 million year-to-date > $122 million in share repurchases in the second quarter; $518 million year-to-date.

Additionally, the firm continues to have positive cashflow, despite a YoY drop in the number, as shown below.

L3H - cashflow (L3H - q2 presentation)

From its Q2 consolidated balance sheet, the firm has a huge one, with $35.3B in total assets and $16.8B in total liabilities, achieving positive equity of $18.5B.

A notable mention is the company's commentary that they will be focused on debt repayment.

For example:

During the quarter, L3Harris repaid $800 million aggregate principal amount of its 3.85% 2023 Notes through the combination of cash on hand and commercial paper.

This is a positive sign, and I like firms that manage debt effectively, especially in this high interest rate environment. A firm of this size & scale also will no doubt have many financing options to tap into, rather than just one.

I think it is a safe bet for now in terms of capital & liquidity.

Stock Price vs 200 Day SMA: Recommend

After the earnings call and a major price dip during trading on Thursday July 27, shares ended the day at $189.76, or 7.94% below the 200-day SMA:

My investing idea calls for tracking the 200-day SMA and trading within a range of 5% below / above the SMA. Based on the current SMA of $206.13 shown in the chart above, our target trading range is $195.82 to $216.43.

The most recent share price dipped just below that range, so the question is whether it is a value trap and will continue to freefall, or just a temporary dip post-earnings, and will rebound. I predict it is a short-term dip with potential to rebound, so I recommend this stock in relation to its 200-day moving average.

The following table illustrates our investing idea graphically, if we were to buy at the last close price of $189.76:

{kind=link}

In the above investing idea, we are buying 100 shares at the most recent close price of $189.76, holding for 1 year to take advantage of the full-year dividend income, selling at 5% above the current 200-day SMA, and taking both a capital gain plus dividend income, generating 16.46% return on the capital we invested. Because of the price dip, the adjusted dividend yield is around 2.40%.

A risk to this idea is the potential for the moving average to move downward after we buy the shares, potentially exposing our position to an extended period of unrealized capital losses.

Ratings Score: Buy

Today, this stock won in 4 of my 5 rating categories, which gives it an overall buy rating. This is in line with the current consensus from Wall Street and SA analysts, but more bullish than the SA quant system.

L3H - ratings consensus (Seeking Alpha)

Risks to my Outlook: Public Defense Budget Limits

A risk to my modestly bullish outlook on this stock is unique to the sector it is in, and therefore this firm as well, is the question of reduced government defense budgets which are influenced by the executive & legislative branch, but certainly can impact this firm's pipeline of contracts & revenue.

The firm mentioned in its "demand outlook" the fact that the recent Fiscal Responsibility Act of 2023 signed in June established budgetary limits in this sector.

Capped Government Fiscal Year ((GFY)) 2024 national defense funding at $886B, which includes $842 billion for the Department of Defense (DoD) specifically. GFY 2024 non-defense funding is capped at $704B.

However, my counterargument to that is that this being a global firm like many of its peers it is not limited just to US government contracts, but also can tap into international demand as well for its products & solutions. Something like combatting terrorism, for example, or patrolling maritime waters for smugglers or stranded boats, is much more of a global issue than simply national.

Consider the following from its Q2 commentary on positive trends in the international demand for such services & products:

The company anticipates this positive trend to continue as North Atlantic Treaty Organization (NATO) allies and other nations increase their defense expenditures to address ongoing global threats. Notably, Germany recently approved a draft 2024 budget reflecting a €1.7B increase to defense spending.

The following chart is a good example of this trend, which I believe will fuel demand going forward for L3H and its solutions:

NATO budget (L3H - investor presentation)

So, I think this will mitigate any risks to the firm of the US government capping defense spending, which in and of itself is also not a major risk, but one worth mentioning, since the revenue of these firms is so tied to government spending.

Analysis Wrap Up

To wrap up today's analysis, here are key points from the article again:

I am rating this stock a buy today, in line with the consensus from Wall Street and SA analysts.

Positives: dividend yield vs sector avg, valuation vs sector avg, current price vs 200-day SMA, capital & liquidity.

Headwinds: net income YoY growth down.

A risk to my outlook is reduced or capped government spending on defense, and this risk has been addressed.

In closing, these so-called "defense sector" stocks I will be keeping a closer eye on as they are not simply defense contractors but more importantly have penetration in the homeland security space which includes cyber threats, border control, maritime & aerial surveillance and intelligence as well.

Consider the amount of accidents & natural disasters at sea, which requires rapid & capable seaborne response, and the technology powering modern naval vessels.

Those who continue to out-innovative will continue to lead in this sector, I think, along with those with international market penetration, and L3H appears to be on the right track in that regard.

For further details see:

L3Harris Technologies: Buy The Dip On This Defense Stock