LHX - L3Harris: Trading At A Discount Despite Favorable Competitive Positioning And M&A Upside

2023-10-04 05:57:21 ET

Summary

- Recent geopolitical shifts to boost global military spending, providing an attractive investment case for the entire defense sector, with most of the additional funding estimated to go to US players.

- L3Harris stock currently trades at a c.18% FY23 estimated EBITDA multiple discount to peers due to uncertainty about its debt profile following TDL and AJRD acquisitions and recent margin contraction.

- This discount is not justified in my opinion given LHX's strong competitive positioning in key military growth areas such as Communications and Space and industry leading margins.

- Record order backlog with Q2 YoY growth at >5x that of key US competitors with highly visible revenues from a well diversified portfolio of products and end markets.

L3Harris Technologies ( LHX , "the company") is a leading US defense contractor, providing domestic and international armed forces with a wide range of mission-critical solutions with a special focus on Tactical Communication, Electronic and Cyber Warfare and Space. The company was formed in 2019 through a merger of equals between Harris Corp and L3 Technologies and recorded revenues of more than $17bn in FY22. Two announcements of debt-funded acquisitions of the Tactical Data Links ((TDL)) product line from Viasat for $2bn and Aerojet Rocketdyne ((AJRD)) for $4.7bn lead to worries about the company's increasing debt position and, coupled with operational challenges lowering margins in recent quarters, have depressed valuation. I see the company's current trading level at just 11 times estimated FY23 EBITDA, a c.18% discount to peers, as overly cautious given the strong competitive positioning in key military growth areas going forward. Initiate at BUY with a price target of $215.

Company Overview

LHX is a Delaware incorporated and Florida headquartered Aerospace & Defense company tracing its roots back to the 19th century and currently employing around 46,000 people. The company operates across three reportable segments with a strong focus on military communications systems which can be broadly clustered as Command, Control, Computers, Communications, Cyber, Intelligence, Surveillance, and Reconnaissance (C5ISR). The company also has a sizable exposure to space tech, which is to be further strengthened by the pending AJRD acquisition, expected to close during Q3. Other areas of expertise include electronic and cyber warfare, night vision solutions and avionics. Key competitors include the three major US prime defense contractors Lockheed Martin ( LMT ), Northrop Grumman ( NOC ) and General Dynamics ( GD ) (referred to as "peers"), hybrid military and commercial A&D players such as RTX ( RTX ), Boeing ( BA ) and Airbus ( EADSF ) as well as international defense firms such as Thales ( THLEF ), Leonardo ( FINMF ) and BAE Systems ( BAESF ).

End Market Exposure (Company Filings)

{kind=link}

Integrated Mission Solutions ((IMS)): c.38% of FY22 revenue

This segment offers its customers signals intelligence and communication systems, optical and infrared sensors as well as targeting systems. Main applications of the segment's products are Air and Naval combat with the US Air Force and Navy being the largest customers. This segment also has a sizable commercial aviation exposure through its offering of avionics and pilot training.

Space & Airborne Systems ((SAS)): c.37% of FY22 revenue

Through the SAS segment, LHX supplies solutions for commercial and military space operations ranging from weather monitoring over full satellite systems to high-altitude missile defense. The unit also offers avionics systems for military applications as well as solutions for warfare in the cyber- and electronic space. Due to the importance of those sectors for US National Security, a high amount of contracts in this segment are classified, with the US Air and Space Forces and NASA as key customers and only limited international revenue.

Communication Systems ((CS)): c.24% of FY22 revenue

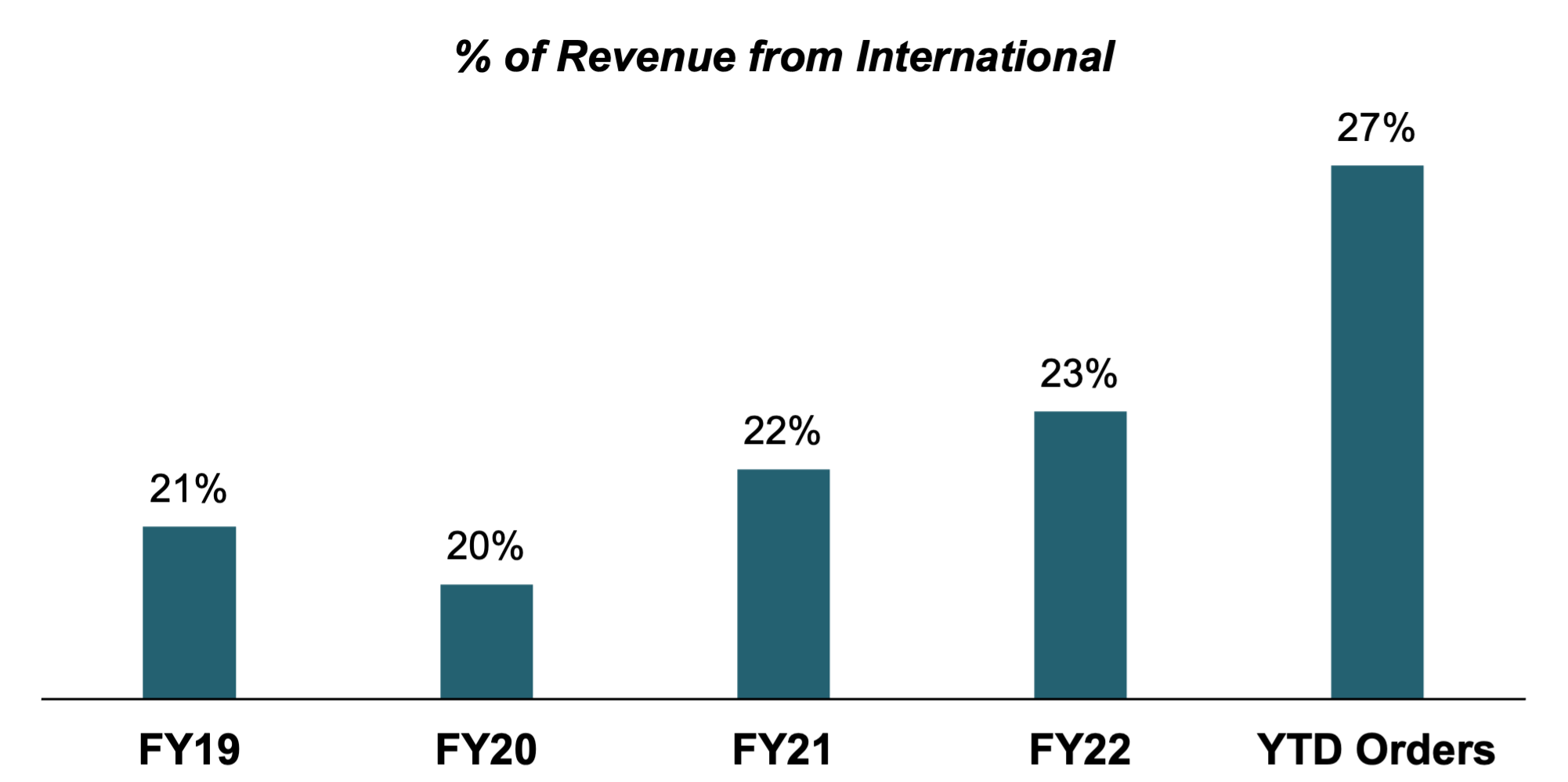

The CS segment is centered around tactical communication solutions mainly for land combat. Key products include tactical and public safety radio equipment, night vision systems and infrastructure for mission and battlefield networks. With around $2bn in revenue from tactical radio systems, LHX is currently the world's largest supplier, capturing a total market share of around 45%. Largest customer is the US Army, followed by Air Force and Navy with a large amount of segment sales also going to commercial and international military customers. Especially in tactical communications, LHX has greatly expanded their global reach growing their share of total ex-US markets from 21% in 2008 to 33% as of FY22. Recent international contract wins include armed forces from Australia, the UK and Saudi-Arabia.

Key Investment Thesis

Recent shifts in geopolitical climate to boost defense spending, particularly for ex-US regions

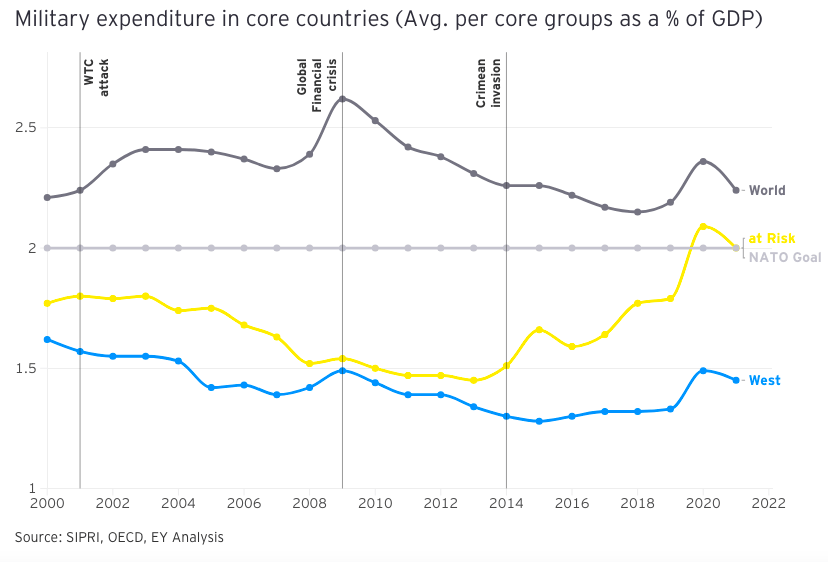

In my view, recent geopolitical developments including such as the Russian Invasion of Ukraine, increasing risk of Chinese expansion in the APAC region and reemerging tensions in the Middle East will serve as key tailwinds to lift the entire defense sector over the coming years. After a period of relative global stability which saw Western defense spending as % of GDP fall, especially ex-US, many countries are now rethinking their strategy being faced with new and re-emerging threats.

{kind=link}

LHX' growing international share of revenue should provide added benefit with estimated above-US defense spending growth in EU, APAC and EMEA driven by regional geopolitical tensions and catch-up investments with only 5 of 30 non-US NATO members meeting the 2% GDP spending target.

{kind=link}

Research from UBS estimates total ex-US defense budgets growing at c.7% through 2030, highlighting that if tensions in Eastern Europe and the South China Sea were to increase further this could rise to around 9.5%. In Europe, Germany has announced a special allocation of €100bn to boost the country's military capabilities and bring its defense spending to the 2% level , while France has recently greenlighted an expansion of around €100bn to bring total 2023-2030 defense budget to around €413bn . Irrespective of the issuing country, I expect the majority of those newly allocated funds to be going to US defense companies such as LHX given their best-in-class capabilities especially in vital areas such as Air Combat and Combat Intelligence compared to their foreign peers.

Highly diversified revenue base with best-in-class order growth and profitability

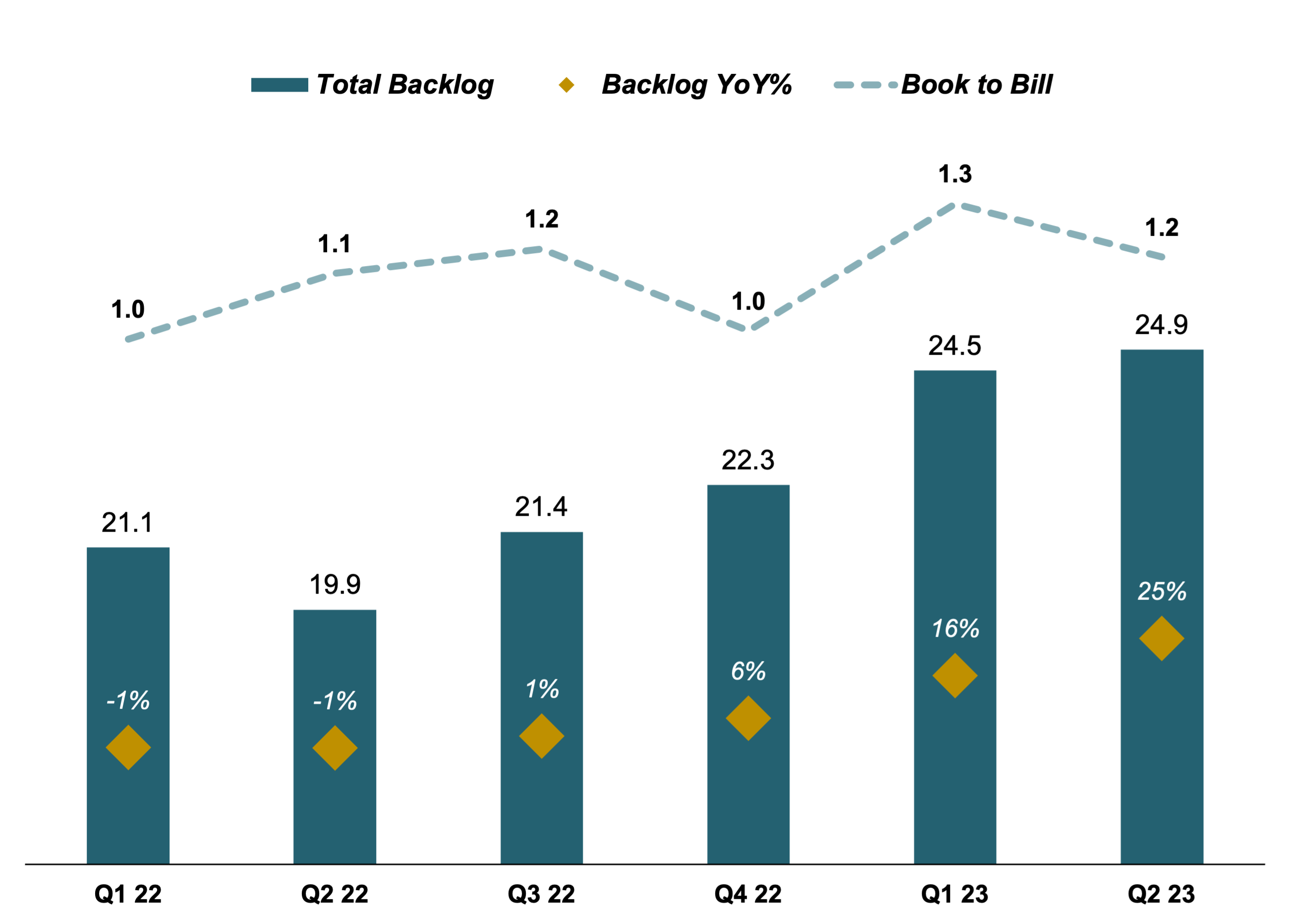

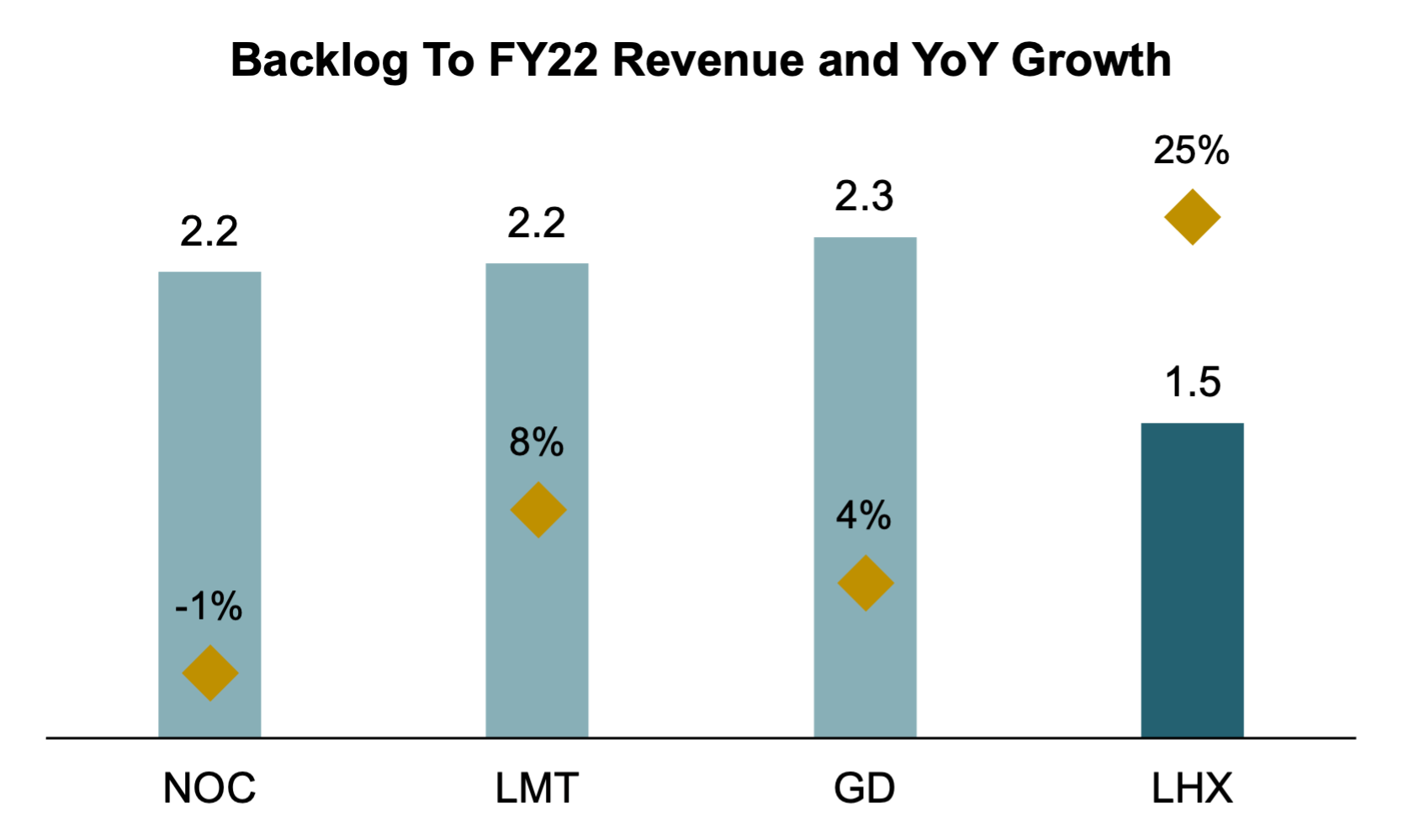

I view the defense sector, especially in the US, as a highly attractive investment case due to high earnings visibility through fixed-price, long-lasting government contracts and steady demand for its product offerings. Contracts are typically awarded in advance and recognized as revenue over the next 1 to 3 years making future earnings highly predictable with the book-to-bill ratio reflecting the proportion of new quarterly orders to recognized revenues. Given this structure, I place a great emphasis on a company's order backlog and its development in order to evaluate future return prospects. LHX currently has a record high order backlog of $24.9bn, up $5bn YoY. After a period of flattish backlog due to macroeconomic tensions, since Q4 22 backlog growth has accelerated at YoY growth rates of 16% and 25% for Q1 and Q2.

{kind=link}

The company's funded book-to-bill ratio, where funded refers to orders that have already been allocated funds and thus represent future income with high certainty, has also been comfortably sitting at or above 1 and as per Q2 stands at 1.2. Total current backlog relative to FY22 revenue is 1.5, below peer average of 2.3; however I see this as a logical consequence of LHX' greater exposure to short-cycle end markets as opposed to sometimes decade-spanning development of new weapons platforms. Compared to peers, LHX has also shown a stronger trajectory in backlog YoY growth, outgrowing peer average by more than 5x, reflecting the strong demand for the company's products.

{kind=link}

What sets LHX apart from other US prime defense contractors in my view is its high amount of diversification across product lines and end markets. Despite deriving the majority of revenues from C5ISR, single products and product lines are spread among several different platforms and areas of application. When comparing this to peers such as Lockheed Martin, which generates around a quarter of their revenue just from the (albeit highly successful) F-35 program, and Northrop Grumman with its key B-21 bomber program, I see a lower amount of cluster risk in LHX' revenues. The benefit of such diversification can be seen in competitors RTX with its GTF engine program and Boeing with the 737 Max losing a sizable amount of their market valuation after technical issues in those flagship programs were revealed. Compared to peers, LHX also has the highest profitability with adj. operating margins at c.15% compared to peer average of around 10%.

Attractive competitive positioning as US and Int. defense prime contractor in key growth areas

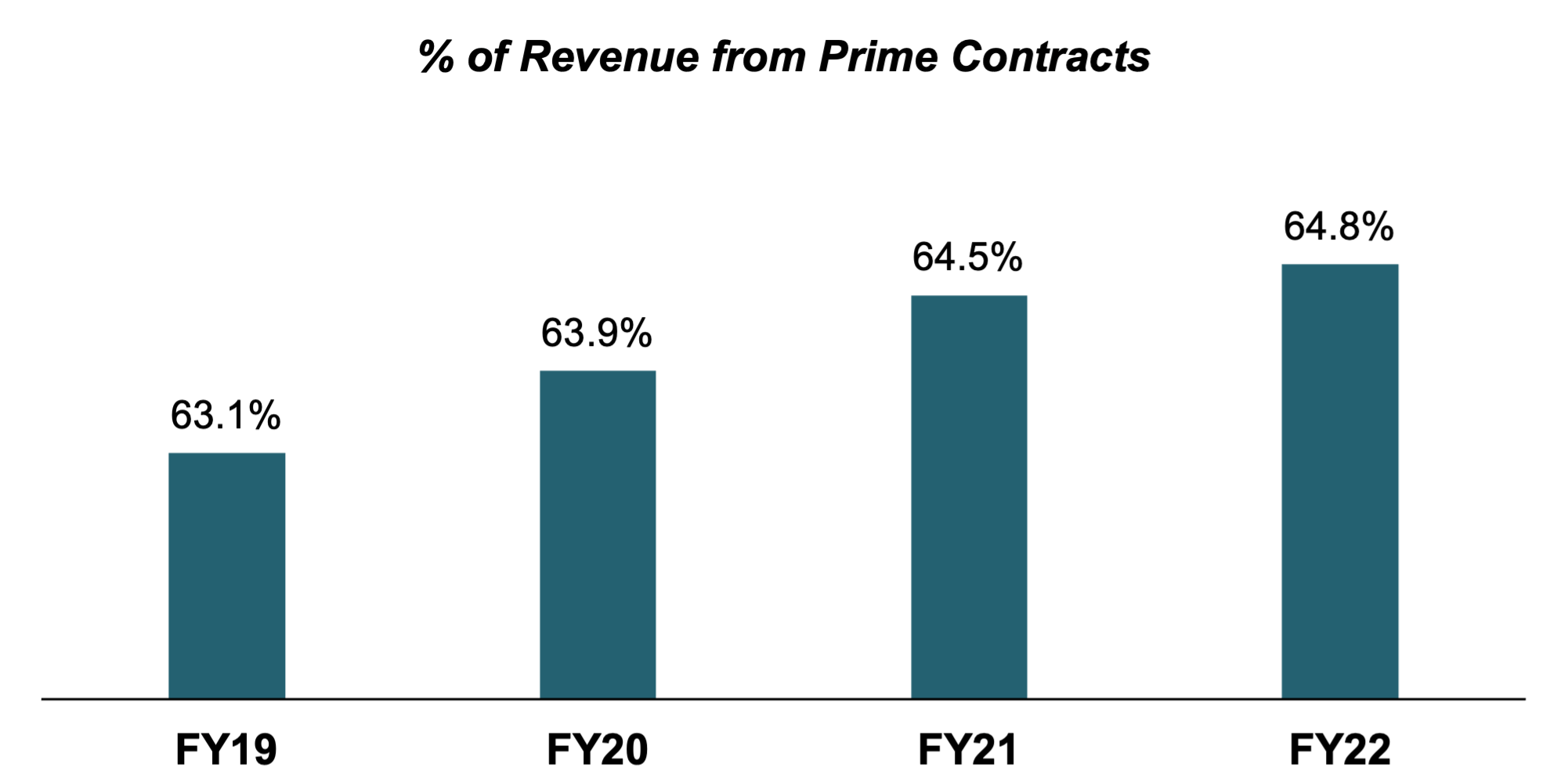

One of the key considerations for the L3 and Harris merger under the company's Trusted Disruptor Strategy was the combined strong positioning as an emerging US and International prime contractor at the crossroads between decade-long established primes and new, smaller entrants which often only act as subcontractors. As opposed to prime contractors, which receive their orders directly from governmental agencies such as the Department of Defense (DoD) in the US, subcontractors are hired by prime contractors and thus have less operational flexibility and do not have the ability to outsource part of their work themselves. Due to their responsibility for the entire project, prime contractors typically also enjoy higher visibility aiding them in being awarded future contracts domestically and abroad. Since the merger, LHX has been able to steadily increase their share of US Government prime contracts with a share of c.65% as of FY22 compared to c.63% in FY19 right after the merger. The segment that saw the strongest increase in percentage of prime contracts was SAS with a c.11% increase from 57% to 63%, reflecting the growing strategic importance of LHX' solutions in the segment.

{kind=link}

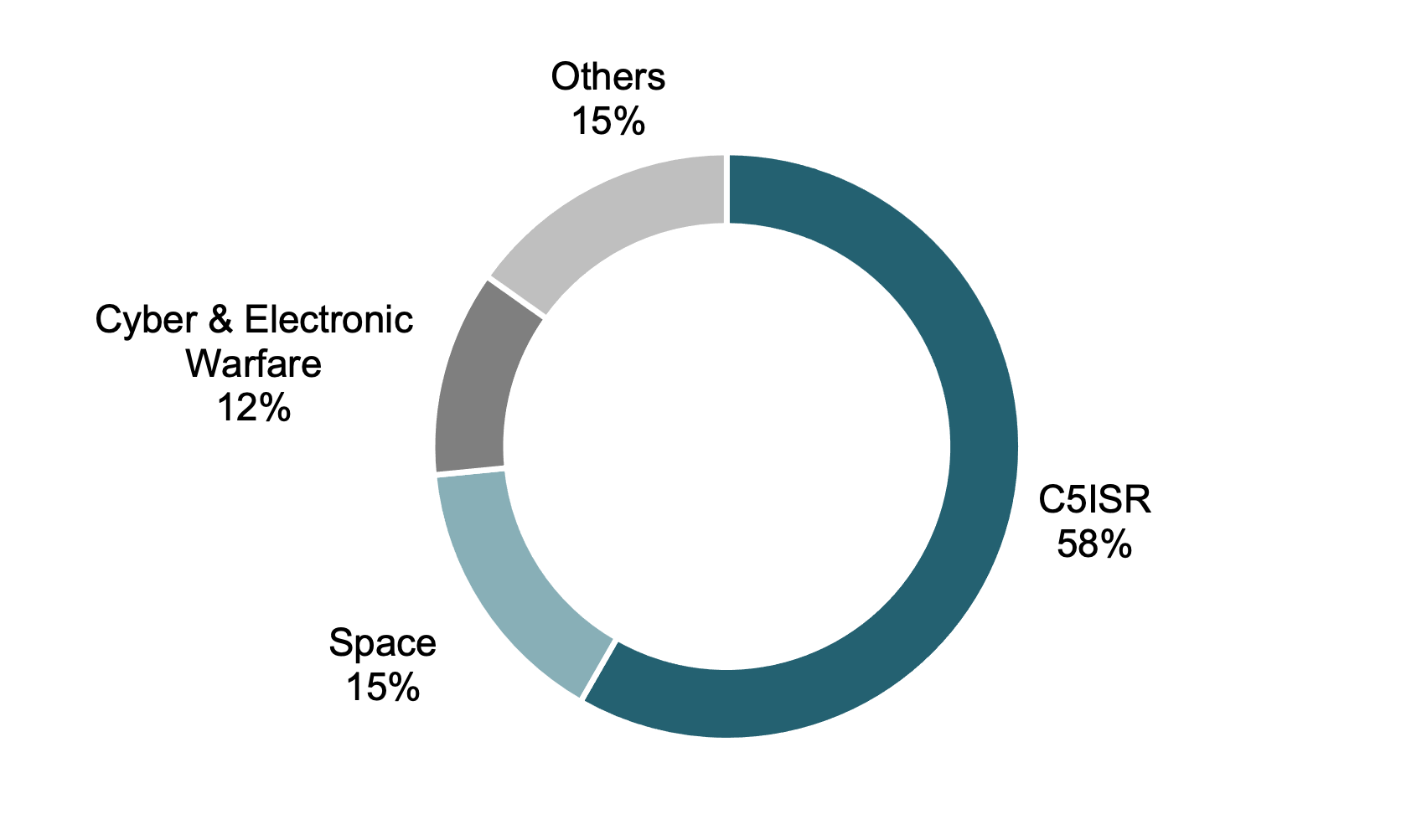

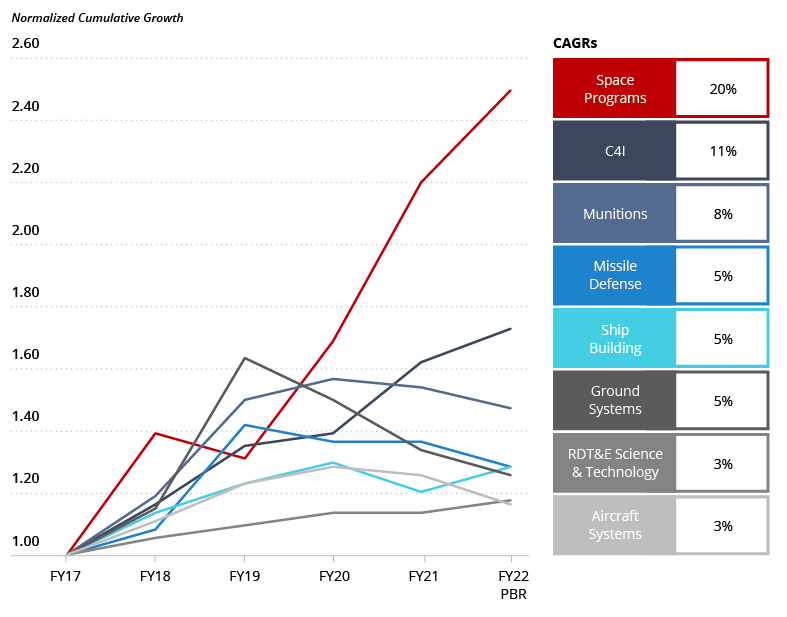

Adding to its increasing status as Prime contractor, I see LHX as very well positioned in the current and future military environment given the company's strategic focus on C5ISR, Electronic Warfare and Space Solutions (enhanced going forward via the AJRD acquisition) which are estimated by Consulting Firm EY to be key defense capabilities going forward. Further strengthening LHX's competitive positioning in those areas was the acquisition of the Tactical Data Links technology line from Viasat, which saw its largest ever contract win in Q3 at $150MM, reflecting high customer demand for state-of-the-art communication solutions. This outlook is confirmed by recent DoD budget trends with Space and C4ISR as the strongest growing segments among budget allocation, growing at respective CAGRs of 20% and 11% from 2017 to 2022 as per A&D consulting firm Avascent.

DoD Budget Allocation (Avascent Analysis)

{kind=link}

AJRD acquisition to increase exposure to high-growth and long-cycle space market

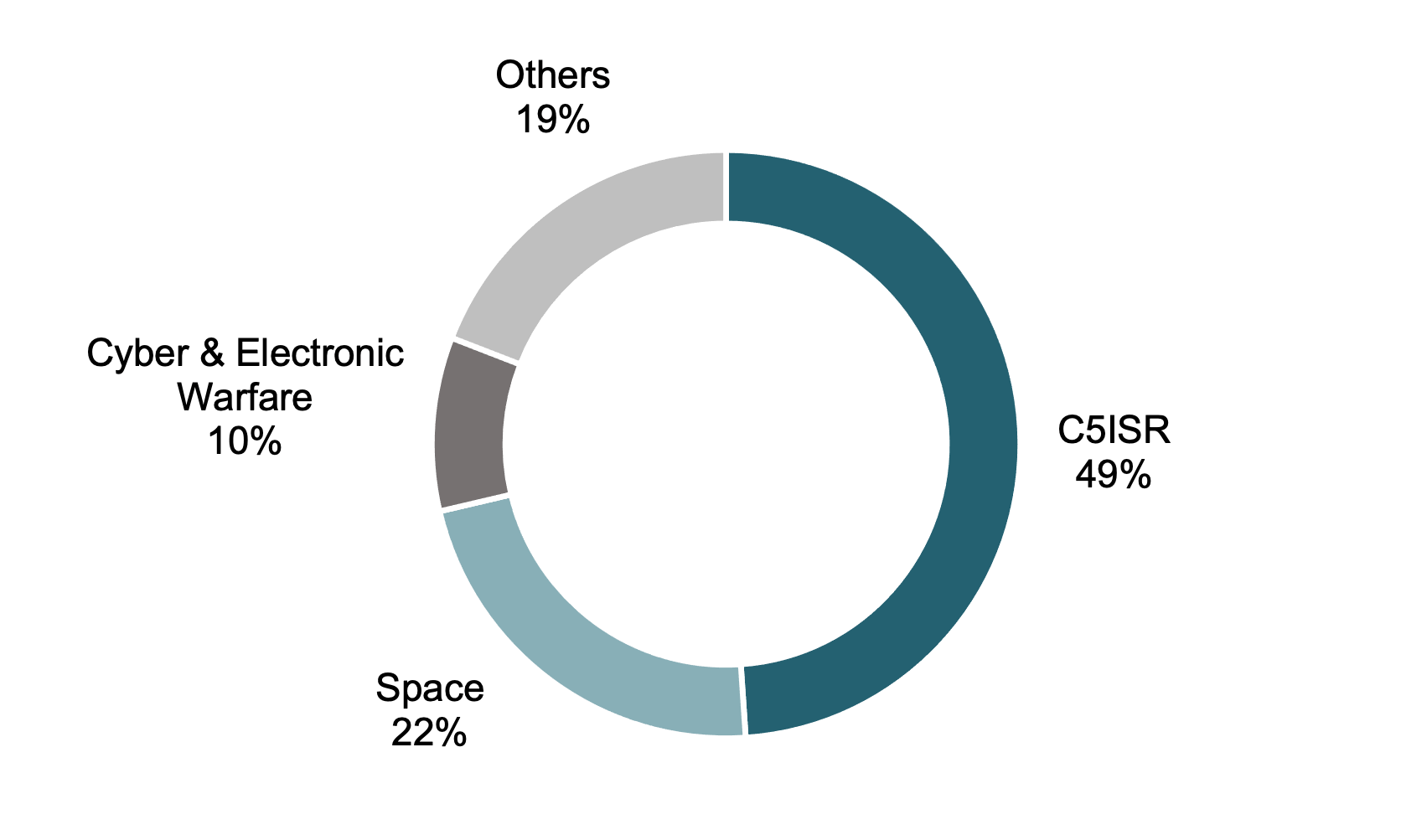

The acquisition of $7bn of Aerojet Rocketdyne's backlog will add to LHX' earnings visibility and brings Pro Forma backlog to $28bn (excl. TDL acquisition) with the additional backlog exposed to several critical programs such as the Patriot and THAAD missile defense systems. Using FY21 numbers as provided by the company in their merger announcement, this will represent a 33% increase to LHX standalone backlog and a Pro Forma FY21 Backlog/Revenue expansion to 1.4 from 1.2. By combining AJRD's 100% exposure to the space and missile market with LHX' existing assets, I expect the company to be in a strong competitive positioning to become the partner of choice for US and International military and civil agencies in this above-average growing market.

LHX+AJRD Pro Forma End Market Exposure (Company Filings)

{kind=link}

DoD allocated budget for space and missiles alone has grown at 20% CAGR from 2017 to 2022 (see above) with NASA budget growing at 7% CAGR in that period , reflecting strong demand for commercial and military aerospace solutions across missile technology and space exploration. The deal will also help LHX to further increase their exposure to longer-cycle end markets and thus provide investors with additional earnings visibility beyond current backlog.

Peer leading and well covered dividend, strong history of returning cash to shareholders via buybacks

Over the last 10 years, LHX and its predecessor companies have grown their dividend at a CAGR of 11.5%, reflecting a premium to its key US defense peers LMT, NOC and GD with an average of 10.4% and the wider sector at 8.1% as per Seeking Alpha figures. Given the recent fall in LHX share price and consensus DPS estimate of $4.75, current FY23e dividend yield stands at 2.73% vs peer average of 2.3% and a sector-wide consensus yield of 1.61%. For FY22, total cash dividends of $864MM were paid to shareholders at a FCF payout rate of c.40%, making the dividend highly safe with enough margin of safety to continue recent growth even in a flattish FCF environment.

Next to paying a quarterly cash dividend, LHX has also been actively returning cash to shareholders through share buybacks, having retired about 13% of outstanding shares since the beginning of 2020. Going forward, management has repeatedly stated their commitment to maintain a clear capital allocation focus on buybacks along with raising the cash dividend in any sub 3.0x net leverage environment.

Key Risks

Weak balance sheet with high debt and goodwill limits strategic options

LHX currently stands at 2.5x net debt to EBITDA ratio which will increase to 3.5x following the AJRD acquisition as per my calculations. Management has expressed near-term capital allocation focus to shift away from buybacks and towards lowering leverage below 3.0x in order to protect the company's investment grade BBB+ credit rating. With c.$14bn in outstanding debt at an assumed weighted cost of debt around 4%, I estimate interest expense to be around $550MM annualized for the next quarters, which should depress bottom-line profitability and offset any positive EPS impact from the AJRD transaction in the near term. However, management has guided for non-GAAP EPS accretive effects from FY24 on, an assumption I find reasonable given the company's strong cash flows enabling it to pay down debt consistently. Should however, near-term headwinds to cash generation be stronger than expected by management, i.e. through inventory buildup or an increasing cash conversion cycle, this debt pile could become a greater concern.

Another potential issue I see within LHX' balance sheet is the large amount of Goodwill related to the initial merger and prior acquisitions with Goodwill reflecting c.52% of total assets as per Q2 23. With such a large portion of total assets allocated to Goodwill, non-GAAP/non-adjusted operating and bottom-line profitability can be at risk given the potential risk of impairments. This has happened in Q3 22 when the company had to write-down $802MM of goodwill due to weaker than assumed sales outlooks for legacy programs and rising interest rates, bringing down quarterly EPS and non-adjusted operating margins into negative territory. Overall, the amount of adjustments the company uses to derive non-GAAP figures is quite high with spacious gaps between GAAP and non-GAAP EPS. This is not a problem per se but investors should definitely be aware of this and the risks associated with it. Overall however, I do not see a huge threat here, as such charges are usually non-cash related and thus will not have an influence on LHX' ability to pay down debt, return cash to shareholders or expand their business.

Reemergence of inflation could compress margins further for fixed-price contracts

LHX operating margins have seen a downtrends in recent quarters due to supply chain issues and cost inflation in labor and material inputs, falling from 16% in FY21 to 14.8% as of Q2 23. Management has guided for a re-expansion in margins across SAS and CS and to a lesser extent in IMS over the coming quarters, however investors should remain cautious in next reports to watch where the trend is going. Given that the majority of the company's contracts are fixed price (75% as of FY22 which is higher than for peers with i.e. NOC having only around 50%), inflationary pressure in both wage costs and input material has a high effect on underlying operating margins as the company is not able to readjust negotiated prices to underlying costs. US and global inflation levels have trended down over recent months, however with oil prices having risen again and US headline inflation ticking up again since troughing in June, investors should carefully monitor upcoming data. On the positive side however, core inflation which is adjusted for fuel and food prices has continued to trend down.

Valuation

As part of my initiation, I would like to employ two separate approaches to obtain an estimated fair value for LHX' equity, a 5Y DCF and a multiple valuation based on FY23ae (author estimated) EBITDA. While my stated price target is solely derived from the multiple valuation to reflect current market environments as well as recent developments in the company's financials, the DCF valuation aims to provide long-term investors with an estimation of the company's fair value going forward.

Multiple Valuation

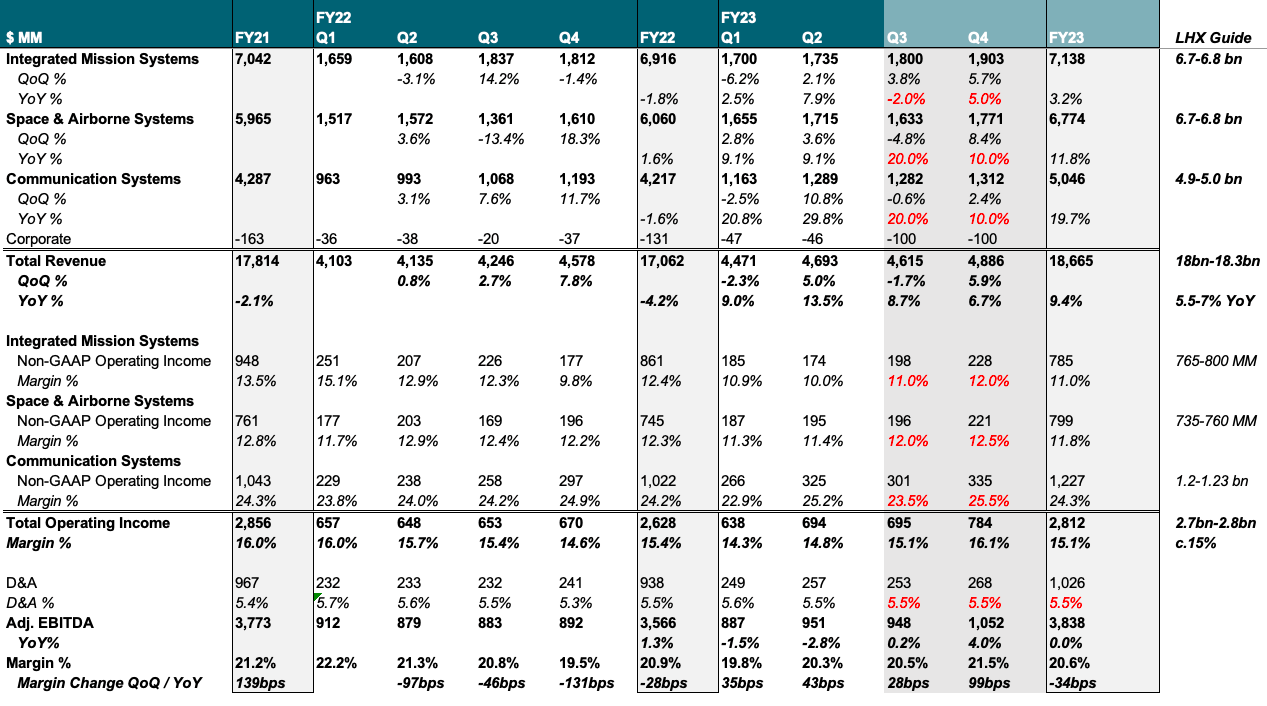

LHX Financial Model (Company Filings and Author Projections)

{kind=link}

For IMS , I expect above guidance growth at $7.1bn FY23ae revenue, up c.3% YoY (LHX management expects $6.7-6.8bn). I project revenue tailwinds due to a stronger USD and higher seasonal growth in H2 due to product deliveries as forecasted by management with Q3 down YoY on strong comps. I further expect margins to have hit a trough in Q2 with a slight expansion in H2 in line with company guidance as cost pressures alleviate and internal cost management programs (Performance First, NeXt) get rolling. Given segment-specific ongoing operational challenges as communicated by management I still expect margins to be down around 140bps YoY to come in at 11%.

For SAS , I forecast strong wins in space to drive continued strong revenue growth (record H1 book-to-bill) with only limited FX impact. Easy comps for Q3 should drive strong YoY development with lighter growth in Q4 to come in at $6.8bn FY23ae revenue on the higher end of management guidance for $6.7-6.8bn. For margins I expect a development in line with company communication to expand sequentially and project a full year margin of 11.8%, down 50bps YoY.

I expect CS FY23ae segment revenue to strongly benefit from FX tailwinds and sustained high demand from H1 to come in above estimate at c.$5bn in line with guidance of $4.9-5.0bn. Margins have seen almost no impact from cost pressures which I expect to further continue with LHX guiding towards a slightly weaker Q3 and a stronger Q4. Full year I expect margins to expand slightly to 24.3%.

Taking into accounts slight corporate revenue headwinds from M&A integration cost I project total FY23ae revenue $18.7bn vs $18.0-18.3bn guided by management with margins at 15.1% in line with c.15% guidance bringing total FY23ae operating profit to slightly above $2.8bn. Assuming a constant D&A ratio at 5.5% of revenue I forecast FY23ae EBITDA around $3.8bn at a slightly down 20.6% margin. Using this metric, LHX currently trades at 11.0x forward EBITDA, a discount that I don't find justified given the reasons laid out in my investment thesis.

Using a 13.0x multiple which is slightly below peer average of 13.3x to reflect debt concerns and recent margin contraction, I obtain an enterprise value of $49.9bn. Adjusting for net debt and minority interests I value LHX equity at $40.6bn, implying a fair value per share of $215 and a 23% upside to current trading levels.

Company Filings and Author Projections

DCF Valuation

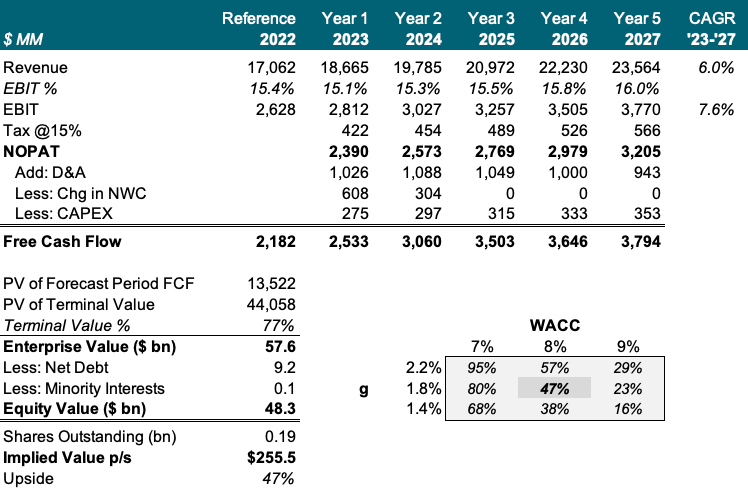

As laid out before, I also employ a 5Y-DCF model to appropriately reflect the company's long-term prospects and offer a second valuation. I use a revenue growth rate through FY27 of 6% which is a blended mix between US and International defense spending projections, adjusted for strength in higher-growth space and C5ISR segments. I further expect operating margins to expand slightly to reflect alleviating supply chain and input cost pressures along with company initiatives such as Performance First and NeXt which I expect to ramp up over the coming years.

Given the lower margin acquired AJRD business and remaining uncertainty about inflation trajectory however, I chose to remain relatively conservative and project only a slight sequential improvement to 16% in FY23. For CAPEX I follow official management communication to keep spending at c.1.5% of revenue and D&A is forecasted to decrease slightly over the period from 5.5% to 4% to reflect lower capital spending. As always, I expect changes in net working capital to equal out in the long-run and model a gradual decrease towards 0 in FY25.

Using a WACC of 8% and an infinite growth rate of 1.8% which is the Fed's long-term estimate for US GDP growth , I get an enterprise value of $57.6bn. Adjusting for net debt and minorities this translates to an equity value of $48.3bn and a fair value per share of $256, giving 47% potential upside.

LHX DCF Model (Company Filings and Author Projections)

{kind=link}

Wrap-Up And Outlook

Getting to the bottom line, I see LHX as a strong investment case in the current environment as the company benefits from sustained sector tailwinds and has positioned itself as a key partner for US and international governments with peer-leading growth in backlog and a strong book-to-bill. I expect this competitive positioning to be further reinforced by the acquisitions of TDL and AJRD which, while leading to some uncertainty about the company's balance sheet in the near-term, will strengthen the company's product offering in key military areas going forward and help to increase exposure to longer-cycle business.

Getting to Q3 earnings, which are to be released on Oct 26, I advise current and prospective LHX investors to pay special attention to management guidance around the company's debt position post-AJRD as well as operating margins for the quarter, with the company having essentially called a trough on margins in Q2.

For further details see:

L3Harris: Trading At A Discount Despite Favorable Competitive Positioning And M&A Upside