LHX - L3Harris: Why It's Time For Buyers To Catch This Falling Knife

2023-10-18 11:13:20 ET

Summary

- L3Harris Technologies is diversifying its business through recent acquisitions, including Aerojet Rocketdyne, to gain entry into missiles and munitions.

- The company expects its space business and the Aerojet business to drive its growth moving forward.

- However, LHX's recent acquisitions have not been well-received by buyers, as it fell more than 40% from its highs toward its recent lows.

- As such, LHX is no longer overvalued. Also, the Middle East conflict could spur medium- to long-term earnings growth as the structural dynamics in the region have been altered.

- With more constructive price action in October, I argue why it's time for buyers to return and catch the falling knife.

L3Harris Technologies, Inc. (LHX) is a leading defense contractor with a diversified business model. Its recent acquisitions, including Aerojet Rocketdyne, are expected to transform its business, gaining an entry into missiles and munitions. The company stressed that it's confident about its Aerojet acquisition as being free cash flow or FCF accretive (year two) and EPS accretive (year one).

Notably, it's a pivotal aspect of the company's business, ascertained as a " double-digit growth area." Bolstered by its space business, L3Harris expects these two segments to underpin the company's growth profile moving ahead.

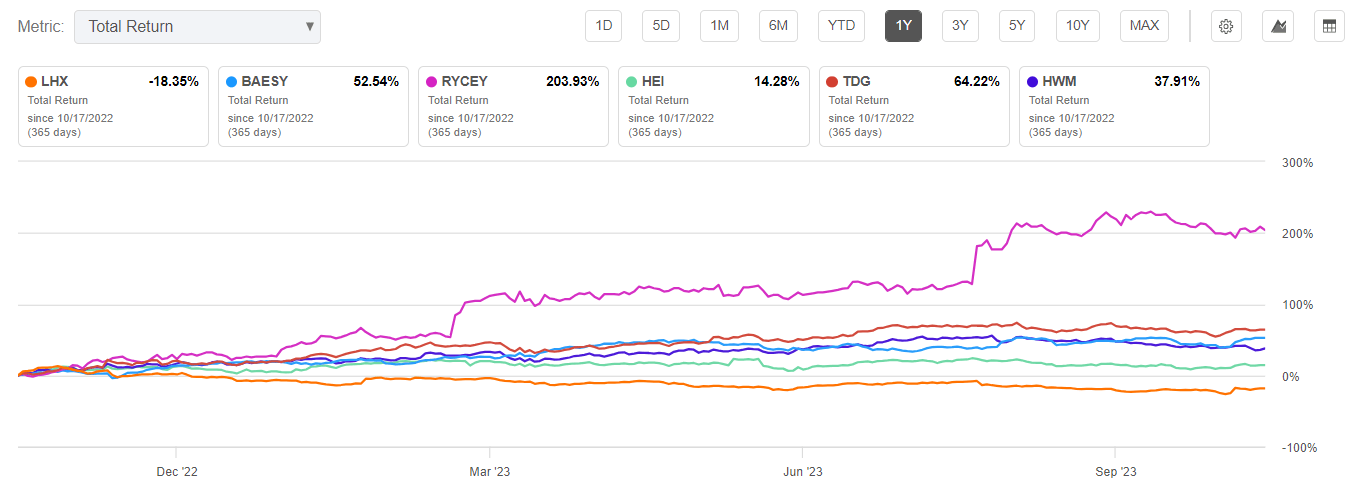

LHX Vs. Peers (1Y total return %) (Seeking Alpha)

{kind=link}

Despite that, LHX's buyers have not responded well to the recent acquisitions. Accordingly, LHX delivered a 1Y total return of nearly -19%, significantly trailing its peer group above. While the Aerojet acquisition is expected to improve its product cycle visibility to about 36 months, its legacy portfolio is still "closer to 18 months." As such, I believe investors need time to assess the revenue and cost synergies emanating from better cycle visibility from Aerojet's business before re-rating its valuation upward.

LHX Quant Grades (Seeking Alpha)

Still, the defense business is a moaty business. As such, I have confidence that L3Harris is well-primed to continue its market-leading "A-" profitability grade. While it isn't considered a top-3 prime contractor with the DoD, its valuation is no longer expensive and is assessed as relatively fair.

Seeking Alpha's "C-" valuation grade corroborates my relative valuation assessment. Furthermore, LHX's forward EBITDA multiple of 11.3x aligns with its 10Y average of 11.8x, suggesting slight undervaluation. Despite that, its higher adjusted EBITDA leverage ratios could have caused concern.

Accordingly, L3Harris is expected to finish FY23 with an adjusted EBITDA leverage ratio of about 3.53x, well above its 5Y average of 1.74x. Given the elevated interest rates, I believe the market is pricing in the impact of its debt profile on anticipated cost synergies from its acquisitions. Moreover, the company isn't expected to have sufficient bandwidth to conduct aggressive capital allocation activities in the near term as it looks to lower its leverage ratio back below its 3x target.

Still, investors should consider that the company's supply chain challenges could bottom out this year. In addition, L3Harris' confidence in lifting its EPS and FCF accretion should bolster its earnings profile moving forward. Wall Street estimates are constructive, suggesting a 2Y adjusted EPS CAGR of 9.2% from FY23 to FY25. As such, its adjusted EPS growth is expected to bottom out this year before inflecting higher over the next two FYs.

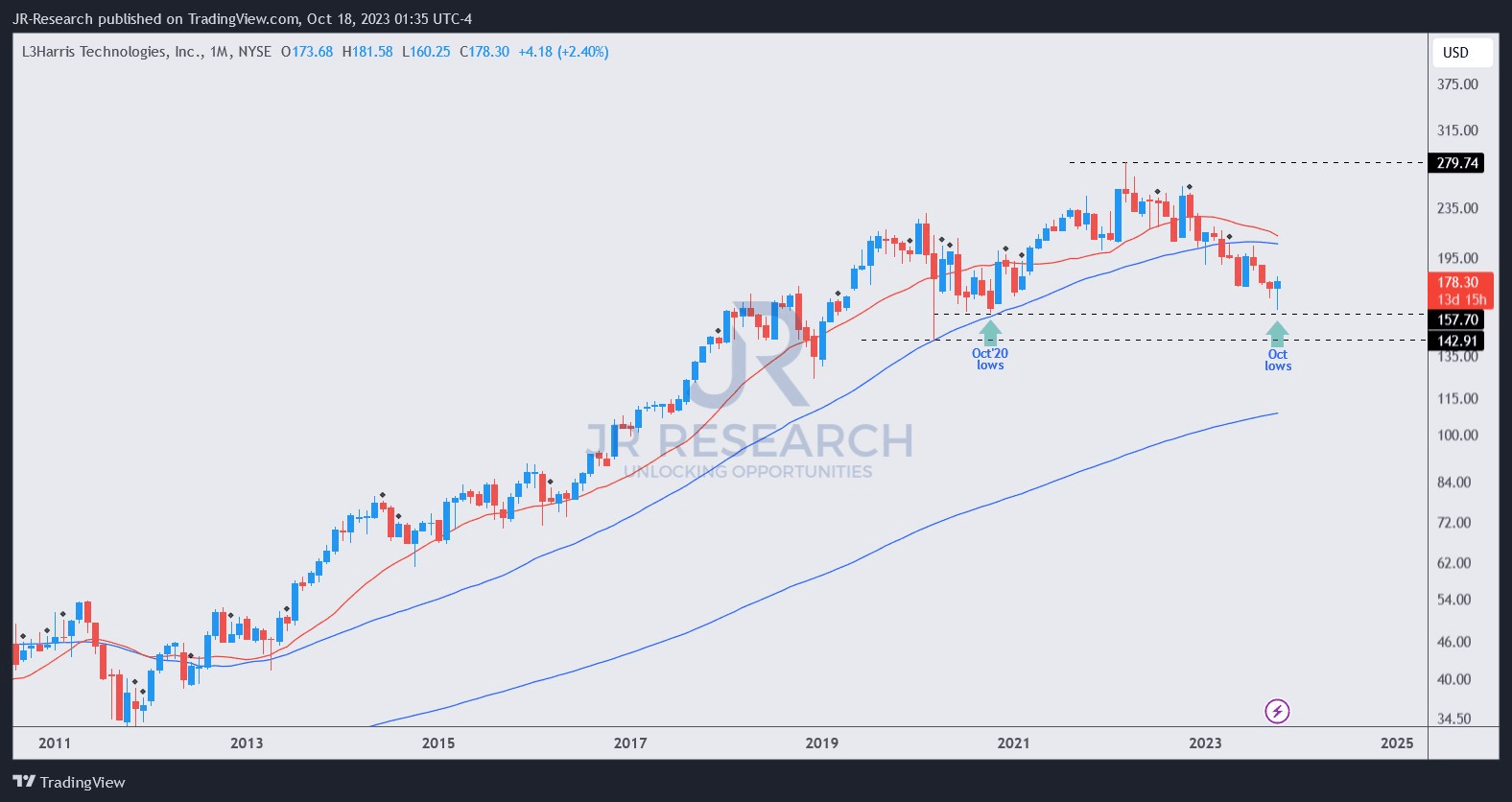

LHX price chart (monthly) (TradingView)

{kind=link}

LHX nearly re-tested its October 2020 lows this month, completing a 3Y round-trip, falling almost 43% from its March 2022 highs.

Ring a bell? LHX topped out at the height of the Russia-Ukraine conflict in early 2022, as investors sent it surging toward a bull trap (false upside breakout). However, LHX was overvalued then, as astute sellers capitalized on the opportunity from the spike to cut exposure and take profits.

The recent Middle East conflict has also attracted investors, as LHX looks like it could form a bottom based on its most recent price action. In other words, dip-buyers likely saw an attractive opportunity to return more aggressively to LHX, given its massive battering. Hence, the risk/reward profile for LHX is markedly different from the one investors encountered in March 2022.

Although I don't expect a near-term revenue growth inflection from the Israel-Hamas conflict, I believe the Middle East crisis could change the structural dynamics in the region, bolstering the medium- to long-term opportunities for L3Harris.

Rating: Initiate Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

L3Harris: Why It's Time For Buyers To Catch This Falling Knife