LLY - Lantheus: Fast-Growing Radiotherapeutics Specialist Can Benefit From Lilly's POINT Biopharma Takeover

2023-10-12 16:35:30 ET

Summary

- Lantheus Holdings' stock price has increased more than 1000% since its IPO in 2015, with most gains occurring since 2022.

- The success of its product PYLARIFY, a PSMA-targeted PET imaging agent for prostate cancer, has driven significant revenue growth.

- Lantheus acquired rights to two radioligand drug candidates from Point Biopharma in 2022, targeting prostate cancer and neuroendocrine tumors.

- Eli Lilly's buyout of Point last week - at an 80% premium to last traded price - underscores both the importance of radiopharmaceuticals and the fact the market may be undervaluing them.

- Date from a pivotal study of PNT-2002 indicated for prostate cancer will be available this year. If approved, Lantheus may receive a helping hand commercially from Eli Lilly, which are eligible to receive ~$1.3bn of milestone payments originally pledged to Point, plus royalties.

Lantheus Holdings ( LNTH ) - a provider of diagnostics, radiotherapeutics and artificial intelligence solutions to the healthcare industry - IPOed back in 2015, raising ~$65m via the issuance of ~10.8m shares valued at $6 per share. The company has since delivered outstanding value for shareholders - its stock price at the time of writing is $68 per share, which represents a return on investment of >1000%.

It's worth noting that the majority of Lantheus' gains have been generated since the beginning of 2022. Founded in 1956, the Bedford, Mass.,-based company's revenue growth after listing was initially flat, with revenues growing from $294m in 2015, to $339.4m in 2022, however in February 2022 Lantheus' stock price jumped from ~$24, to ~$54 more or less overnight after the company announced 2022 revenues of $425.2m - up 38% year-on-year - and guided for FY22 revenues of $685 - $710m, and earnings per share ("EPS") of $1.95 - $2.05.

In the end, Lantheus drove $935m of revenues in FY22, and adjusted, fully diluted EPS of $4.22, although GAAP EPS was just $0.4. The difference maker was the full commercial launch of PYLARIFY, described by Lantheus in its 2022 10-K submission / annual report as follows:

PYLARIFY (also known as piflufolastat F 18, 18F-DCFPyL or PyL) is an F 18-labelled PSMA-targeted PET imaging agent used with PET/computed tomography ("CT"). PYLARIFY is indicated in the U.S. for PET imaging of PSMA-positive lesions in men with prostate cancer with suspected metastasis who are candidates for initial definitive therapy and in men with suspected recurrence based on elevated serum prostate-specific antigen ("PSA") levels.

Launched in June 2021, PYLARIFY earned ~$43m of revenues in that year, before sales exploded in 2022, exceeding $500m and taking the market by surprise. According to Lantheus' annual report, the product "works by binding to PSMA, a protein that is over-expressed on the surface of more than 90% of primary and metastatic prostate cancer cells" and has been welcomed as a superior alternative to CT scans, bone scans and magnetic resource imaging ("MRI").

In March 2022, Lantheus entered into a strategic collaboration with Swiss Pharma giant Novartis ( NVS ) to use PYLARIFY in combination with Novartis' PSMA targeted therapy Pluvicto, a drug that earned $271m of revenues in 2022, $451m in 1H23, and is pegged by analysts for peak sales >$2bn by the company. PYLARIFY revenues in 1H23 were $405m - up 82% year-on-year - so it seems clear that PYLARIFY revenues have substantially more growth potential - Lantheus' guidance for total revenues in 2023, issued alongside Q223 earnings, was for $1.245bn - $1.27bn, and diluted adjusted EPS of $5.6 - $5.7.

Not Resting On Its Laurels - Lantheus Targets Radiopharmaceuticals Receives Shot In The Arm As Lilly Buys Point Biopharma

Lantheus developed other products prior to PYLARIFY that continue to generate important revenue streams for the company. Alongside PYLARIFY's $211m revenues in Q223 (based on >200k PET scans), the ultrasound enhancing agent DEFINITY drove $71m of net sales - up 13% year-on-year - while TechneLite - a "self-contained system or generator of Tc-99m, a radioactive isotope with a six-hour half-life, used by radiopharmacies to prepare various nuclear imaging agents" - earned $22m of revenues. Other precision diagnostics - $5.4m - and strategic partnerships and other revenue - $13m - comprised the remainder of Lantheus' $322m of revenues in Q2 2023.

From a forward price to sales perspective, Lantheus stock - priced at $68 at the time of writing - trades at ~3.7x forecast FY23 revenues, and from a forward price to earnings ("PE") perspective, based on adjusted forecast EPS of $5.65, the ratio is ~12x. These are competitive figures that might persuade investors to buy Lantheus stock based on its current product portfolio alone - especially when shares traded ~$100 as recently as May - but Lantheus also is pursuing an exciting new opportunity that could help the company maintain its stunning recent revenue growth. The new area of focus is radiopharmaceuticals.

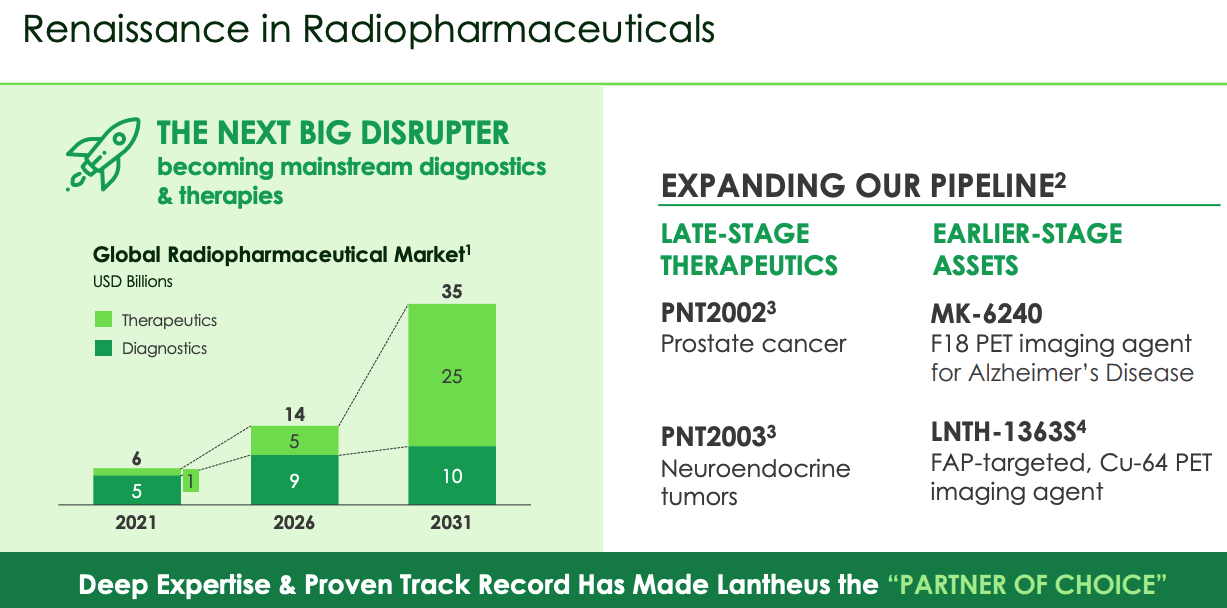

Renaissance in Radiopharmaceuticals (Lantheus investor presentation)

{kind=link}

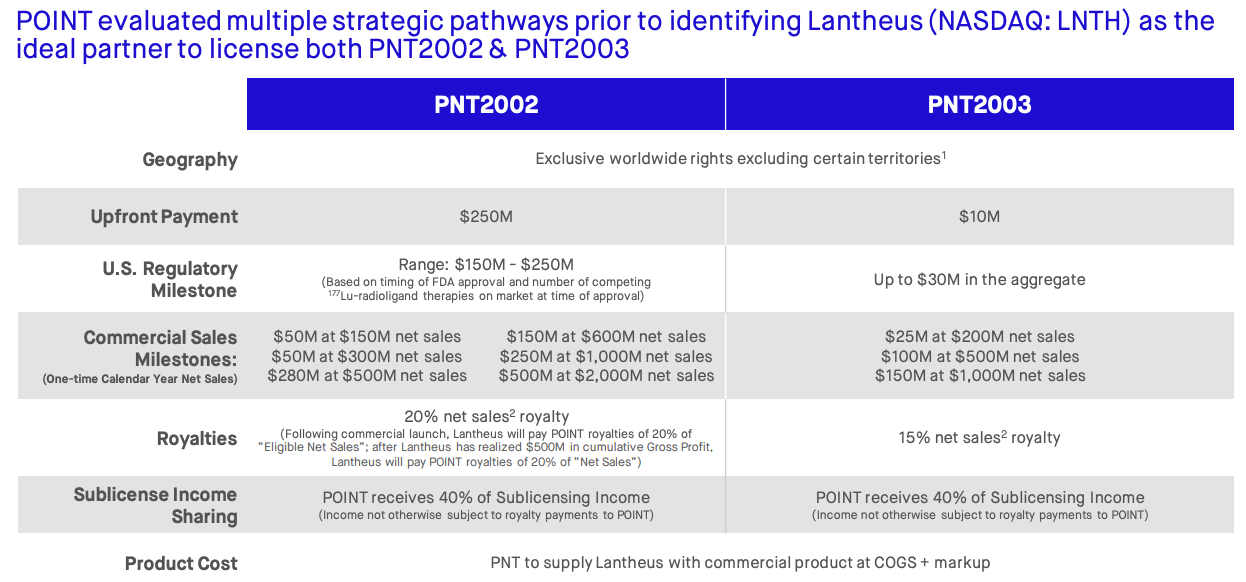

As we can see above, Lantheus' research suggests that radiopharmaceuticals is a market that's expected to quintuple in size between 2021 and 2031. In December 2022, Lantheus entered into a strategic collaboration with POINT Biopharma ( PNT ) through which it gained a license to the exclusive worldwide rights (excluding certain Asian territories) to two of Point's drug candidates - PNT2002 and PNT2003. The collaboration agreement is broken down as follows in a recent Point investor presentation.

POINT / Lantheus collaboration re PNT2002 / 2003 (POINT presentation)

{kind=link}

As we can see, as well as making an upfront payment of $250m, Lantheus has pledged $150m - $250m in regulatory milestones and up to ~$1.3bn in commercial sales milestones, plus royalties on net sales.

PNT2002 and PNT2003 are "radioligands," a new class of drug described as follows by the Health Policy Partnership :

A radioligand is made of two parts: A ligand, which can find cancer cells that have a particular surface molecule, and a radioisotope, which emits therapeutic radiation to kill cancer cells. The radioligand can target cells anywhere in the body.

PNT2002 is a PSMA-targeted therapy for metastatic castration-resistant prostate cancer ("mCRPC") that has reached the Phase 3 clinical study stage - a ~52k patient population, and should that study be successful, Lantheus will take responsibility for filing a New Drug Application with the Food and Drug Agency ("FDA"), requesting permission to market and sell the drug commercially. Top line data from Point's Phase 3 SPLASH study is expected to arrive this year.

To add an additional layer of intrigue, it was announced last week that Eli Lilly ( LLY ) - the world's largest pharma by market cap valuation - is set to acquire Point Biopharma, in a deal worth $12.5 per share - an aggregate of "approximately $1.4bn." Jacob Van Naarden, President of Loxo@Lilly, the oncology unit of Eli Lilly, commented on the deal:

We are excited by the potential of this emerging modality and see the acquisition of POINT as the beginning of our investment in developing multiple meaningful radioligand medicines for hard-to-treat cancers, as we have done in small molecule and biologic oncology drug discovery and development

It's not clear if Lilly will approach Lantheus and attempt to restructure elements of the deal to try to gain a larger share of future revenues from PNT2002, and PNT2003, which is indicated for neuroendocrine tumors, and also progressing into a Phase 3 study, but either way Lilly's takeover of Point appears to be good news for Lantheus.

At the very least, Lilly will be able to leverage its significant marketing and sales infrastructure to try to realize all the milestones promised to Point by Lantheus, and the big pharma may be able to assist Lantheus with the prior approval processes also, an area in which Lilly is vastly experienced.

Nothing is guaranteed - PNT2002 still has a Phase 3 to negotiate in patients with metastatic castration-resistant prostate cancer who have progressed following PNT2002 treatment with an androgen receptor pathway inhibitor ("ARPI"), with the primary endpoint being "Radiographic or imaging-based progression-free survival, as assessed by blinded independent central review."

Back In April, the FDA granted Fast Track status to PNT2002, and given the drug has a similar mechanism of action to Novartis' Pluvicto, a successful trial followed by approval is arguably the likeliest outcome. The fact that Lantheus has already paid $260m upfront to Point Bio, and Eli Lilly's buyout of Point Bio, suggests that these two companies believe the same. Of course, the fact that PNT2002 targets prostate cancer is another win for Lantheus, as it can help widen the market for PYLARIFY.

Some Risks To Consider and Thoughts On The Opportunity In Play For Lantheus

Until the SPLASH study is complete, and the data is in front of the FDA, it's not possible to judge with certainty whether PNT2002 merits approval. The signs may be promising, but radioligand drug development is still in its infancy and the dangers of off-target toxicity are very real. The safety readout from the SPLASH needs to be impeccable.

PNT2002 will additionally need to establish itself as comparable, at the very least, to Novartis' Pluvicto, which showed in its own pivotal study that it could reduce risk of death by 38% when used alongside standard of care, helping patients with metastatic castration-resistant prostate cancer live four months longer. If PNT-2002 data falls short of this standard it may struggle in the marketplace, or even fail to secure an approval. It also should be noted that Novartis has an approved radioligand therapy, Lutathera, directed against neuroendocrine tumors - the same indication targeted by PNT-2003.

Production of the ingredients used in PNT-2002 has caused Novartis significant problems, and could affect Lantheus also, although Point has a 180k square foot manufacturing facility based in Indianapolis, which, conveniently, is also where Eli Lilly's headquarters are based.

Even taking into account these risks, however, I'd be really reasonably excited about Lantheus' growth potential. First of all, the company's PYLARIFY product is likely a long way off reaching its peak revenue potential, so even if revenue growth plateaus somewhat, they will likely keep growing at a decent click even if PNT-2002 does not make it to market. Lantheus has done a good job of pivoting the company back toward profitability, generating positive EPS on both a GAAP and non-GAAP basis for the first time in three years in 2022.

The fact that Lilly completed its buyout of Point at a >80% premium to last traded price may imply that the market has under-appreciated the radioligand opportunity, and the market does not seem to have priced in the potential blockbuster (>$1bn revenues per annum) opportunity in play for Lantheus should PNT-2002 be approved, given its current low P/S and P/E ratios. Were PNT-2003 also to be approved, we may want to consider adding $2 - $3bn to Lantheus' current market cap valuation of $4.63bn over the long term.

Based on all of the above, and acknowledging that there are significant risks associated with this investment thesis (I would encourage all readers to complete their own due diligence, or share thoughts in the comments section below), my view is that the market - even after the stellar gains made by Lantheus stock since January 2022 - continues to undervalue this innovative company and the impressive way - after a slow start to life as a listed company - it has grown organically, and inorganically via smart deal-making. Lantheus remains a buy, for me.

For further details see:

Lantheus: Fast-Growing Radiotherapeutics Specialist Can Benefit From Lilly's POINT Biopharma Takeover