LLY - Lantheus Stock: Looking To Add After SPLASH's Belly-Flop

2023-12-20 08:30:00 ET

Summary

- Point Biopharma and Lantheus Holdings released positive topline results for their radioligand therapy in patients with metastatic castration-resistant prostate cancer.

- The SPLASH trial met its primary endpoint, showing a progression-free survival benefit compared to the control group.

- Both companies experienced a drop in stock prices despite the positive results, but the author remains bullish on Lantheus.

Point Biopharma (PNT) and Lantheus Holdings (LNTH) released topline results for their radioligand therapy (Lu-PNT2002) in patients with metastatic castration-resistant prostate cancer who had progressed following androgen receptor pathway inhibitor ((ARPI)) treatment. The SPLASH trial met its primary endpoint, revealing a progression-free survival compared to the control group, while overall survival ((OS)) results were deemed immature with a favorable hazard ratio ((HR)). In addition, the data showed favorable safety and tolerability with a small percentage of patients discontinuing due to adverse events. Despite these outcomes, Both Lantheus' and Point's stock prices dropped by double-digit percentages during the trading sessions as investors came to grips with PNT2002 falling short of Novartis' (NVS) Pluvicto.

Although I do agree that the data did fall short of the market's expectations, I still believe there is enough here to keep the program moving forward. Moreover, this program is not a major component of my LNTH bull thesis, so the market's reaction to the data is a bit overblown in my opinion. As a result, I am looking to add to LNTH if this unjustified sell-off brings the ticker down to my Buy Threshold.

I intend to provide some background on Lantheus and the SPLASH program. In addition, I take a look at the recent SPLASH data readout and present my views on the data. Finally, I reveal how this data has impacted my LTNH bullish outlooks as well as my plans for attempting to take advantage of this unwarranted move in the share price.

Background on Lantheus

Lantheus Holdings is a leader in diagnostic imaging, AI solutions, and radiopharmaceuticals, and has been a key player in the medical imaging industry. With a focus on innovation, Lantheus is venturing into the realm of oncology with strategic partnerships, positioning itself for substantial growth.

Lantheus is particularly active in the prostate cancer imaging and treatment market, where it offers PYLARIFY, a leading PSMA PET Imaging Agent. PYLARIFY boasts high detection rates of metastatic disease, non-limitation by lymph node size, and visualization of bone metastases.

Lantheus also operates in the ultrasound enhancing agent (UEA) market with DEFINITY, aiming to improve echocardiogram diagnostic quality. It holds a substantial share of the U.S. market and sees opportunities to address suboptimal echocardiograms.

Additionally, the company is involved in the Technetium-99m (Tc-99m) Generator market with TechneLite, a critical component in various medical imaging studies, particularly in cardiac studies.

Lantheus is committed to leveraging technology and innovation, such as AI analysis for PET/CT scans, to enhance clinical decision-making and deliver better patient outcomes.

The company's overall strategy includes sustaining double-digit growth, diversifying its portfolio, and achieving leadership in the markets where it competes. In fact, in 2022, Lantheus reported revenues of $935M, with a 28% 5-year revenue CAGR.

The SPLASH Program

On November 14, 2022, Lantheus announced a strategic collaboration and exclusive license agreements with POINT Biopharma for the commercialization of PNT2002 and PNT2003. Point Biopharma, specializes in radiopharmaceuticals for cancer treatment. The ARPI SPLASH program is a joint initiative with Lantheus that targets the androgen receptor pathway using Point's PNT2002, a 177Lu-based PSMA-targeted radiopharmaceutical therapy developed for mCRPC, particularly those resistant to standard therapies. The collaboration leverages the expertise of both companies, combining diagnostic imaging capabilities with advanced radiopharmaceutical development. Lantheus holds exclusive worldwide commercialization rights (excluding certain Asian territories), and the FDA granted Fast Track designation in April of this year for mCRPC.

The financial terms of the collaboration include a substantial upfront payment for Point, potential regulatory and commercial milestones, royalties on net sales, and sublicense proceeds. For SPLASH's PNT2002, the deal includes milestone-based structures, with an upfront payment of $250M and potential additional milestones upon U.S. regulatory approval and commercial marks. The collaboration also includes the allocation of net sublicense proceeds if Lantheus chooses to sublicense the rights.

The collaboration aligns with Lantheus' long-term strategy and business development criteria, focusing on diversifying its portfolio with late-stage assets, and high-growth, high-margin products that leverage core capabilities. Considering that prostate cancer is the second most common cancer in men in the U.S., the company stands to greatly benefit from a potential approval.

SPLASH Data

The topline results from the global Phase III SPLASH study, evaluating the efficacy and safety of 177Lu-PNT2002 in mCRPC patients who have progressed on an ARPI. The data revealed that the SPLASH trial hit its primary endpoint with a median radiographic progression-free survival (rPFS) of 9.5 months whereas the control group only had 6 months. This marked a statistically significant 29% decrease in the risk of radiographic progression or death. The interim OS results were deemed immature , with a hazard ratio of 1.11. Furthermore, PNT2002 showed an advantageous safety profile, with lower rates of treatment-emergent adverse events (TEAEs), leading to a lesser discontinuation rate compared to the ARPI group.

The companies anticipate additional data in 2024 before a potential NDA submission to the FDA.

SPLASH Crash?

Although I do concede the PFS results were considered "inferior" to Novartis' Pluvicto (lutetium Lu 177 vipivotide tetraxetan), I am still bullish on the SPLASH program due to the trial hitting its primary endpoint, revealing a progression-free survival with a 29% cut in the risk of radiographic progression or death. Plus, we don't have all the data yet with the OS still being immature, yet, the HR was still 1.11. In addition, I will reiterate the favorable safety, with only 1.9% of patients discontinuing the trial due to adverse events. The well-tolerated nature of the radiopharmaceutical presents a positive outlook for patients facing disease progression after ARPIs, potentially offering a new avenue for effective treatment. I think the FDA will have to consider the potential positive improvements with solid efficacy with a great safety profile and has the potential to carve a niche in the market, providing a competitive edge for both Lantheus and Point Biopharma. In addition, Novartis has had to halt patients due to a supply shortage of Pluvicto, so there might be a market share to claim.

Moreover, the recent developments in the landscape of mCRPC treatment have taken a significant turn with the strategic acquisition offer from Eli Lilly ( LLY ) to acquire all of Point's shares for $12.50 per share, totaling an estimated $1.4B. This deal underscores the interest in radiopharmaceuticals and the sustained vigilance by Big Pharma for acquiring cutting-edge cancer therapeutics.

Considering these points, I believe the program still has the prospects to produce marks to get them through the FDA and possibly differentiate them from existing therapies. In addition, Eli Lilly's proposed acquisition of Point Biopharma at a premium valuation supports the pursuit of radiopharmaceuticals.

However, we have to concede that Pluvicto's data does present as superior to PNT2002, therefore, the market opportunity for PNT2002 may be limited in mCRPC. So, I would say PNT2002 might not fail in the clinic… but it might fail on the market.

Still Bullish On LNTH Stock

I must admit the SPLASH data is a legitimate setback for Lantheus due to their expectation that this collaboration will diversify its revenue streams, support long-term cash flow generation, and contribute to its overall growth strategy. The company's strong operational and commercial capabilities demonstrated through past successes, position it well to capture significant opportunities in the radiopharmaceutical market that do not hinge on PNT2002.

In fact, the company recently reported strong Q3 numbers that revealed robust financial performance and operational success. The company's total revenue hit $319.9M, marking a notable 33.7% increase compared to the same period last year. Net sales demonstrated strong growth, reaching $215.4M with a remarkable 49.9% year-over-year increase. The success was particularly driven by the continued demand for PYLARIFY, Lantheus' leading PSMA PET imaging agent, solidifying its position as the top-ordered agent in the market. In addition, they reported an expanded adjusted net income margin of 32.2%, which led to an adjusted EPS of $1.47 and the company upgrading their 2023 guidance. Furthermore, Lantheus finished Q3 with $615.7M in cash and cash equivalents.

{kind=link}

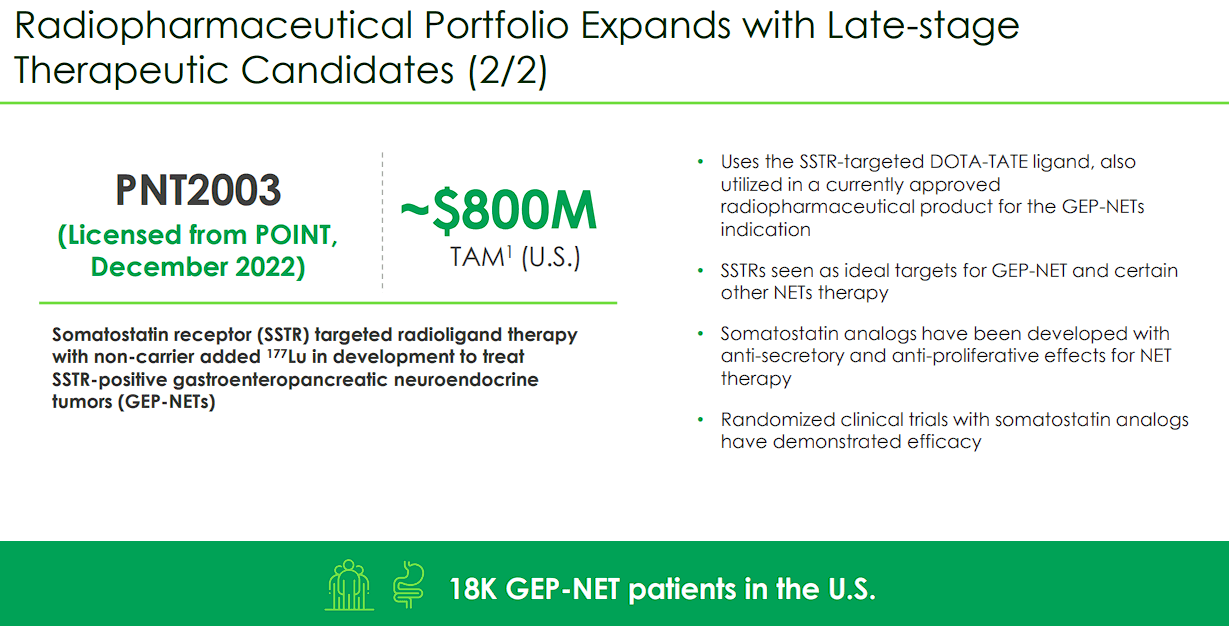

I should also make note that Lantheus still has other pipeline developments, including the Fast Track Designation granted for MK-6240, a novel PET imaging agent for Alzheimer's disease. Lantheus also has their other Point candidate, PNT2003, which has a ~$800M total addressable market.

{kind=link}

These advancements underscore the company's commitment to innovation and future growth opportunities.

Considering these points, I still believe Lantheus is a leader in the radiopharmaceutical industry, with strong product demand, successful pipeline progress, and effective financial management contributing to a promising outlook for future growth and innovation. Yes, the recent PNT2002 does damage their growth potential and the company might be on the hook for additional milestone payments. However, I am not convinced LNTH's value has been heavily dependent on this program.

Keep in mind, Lantheus and Point Biopharma announced this collaboration program in November of 2022 and the ticker was trading around the same range as it is today ($55-$60). Before the announcement, LNTH had hit nearly $90 per share and responded well to reports about PYLARIFY's performance. Moreover, Lantheus has plenty of partnerships and pipeline programs to extract growth in the coming years.

So, I don't see how this program is critical to Lantheus in the near term or the long term if the market was willing to bid the share price substantially higher before we knew about Point Biopharma collaboration. Of course, any setback hurts… but some analysts are making this data readout seem like Lantheus is dead in the water and this was the entire bull thesis.

{kind=link}

My Plan

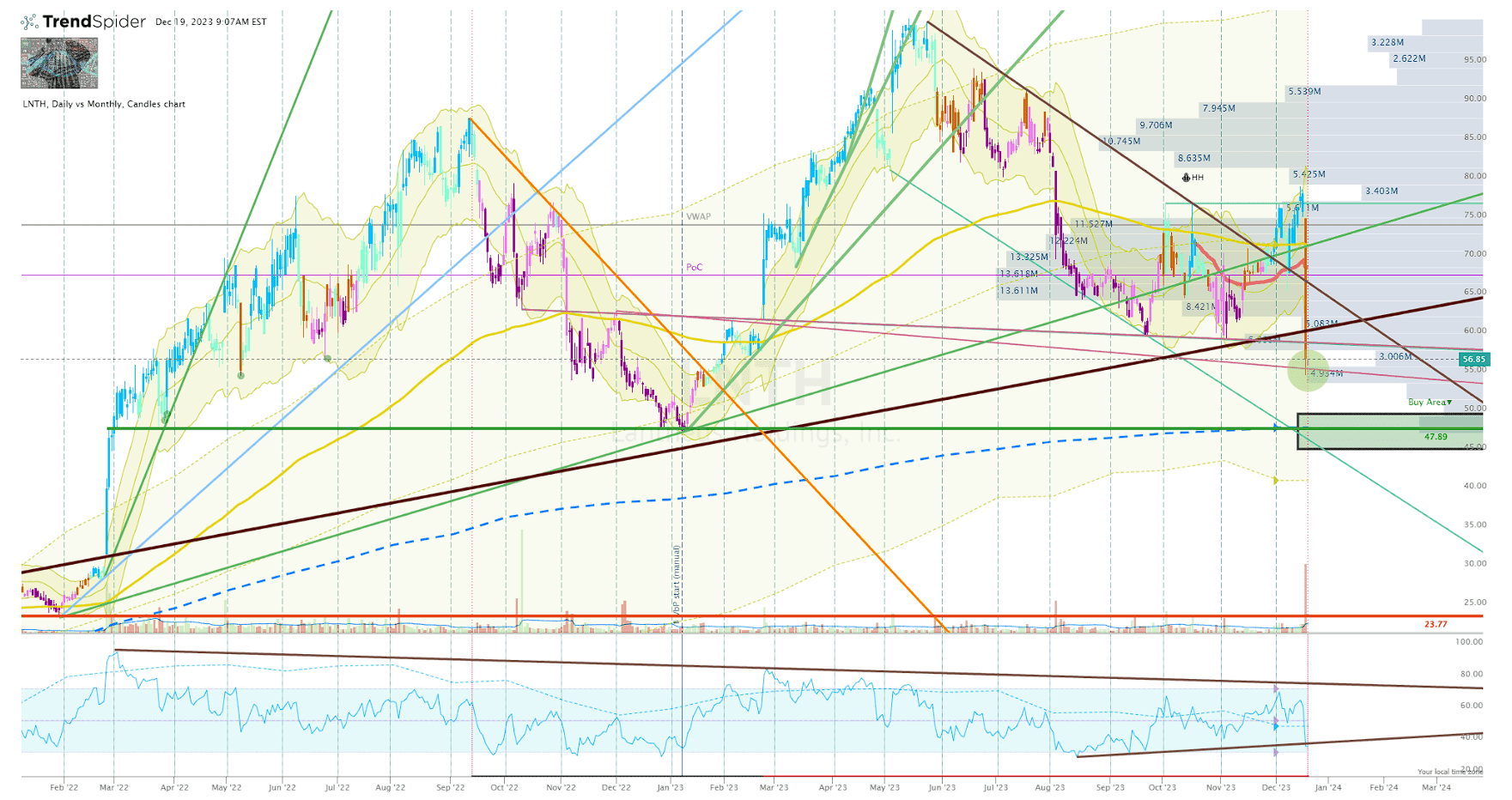

As I mentioned above, I am looking to take advantage of the market overreaction to the SPLASH data readout, which dropped LNTH from about $75 per share to $55 per share under elevated volume. Although I would consider adding to LNTH here, I like to rely on technical analysis during these times of elevated volatility due to the algorithms typically relying on set parameters and achieving their targets. Right now, LNTH is sitting on a light support level below an uptrend ray, so I am expecting another leg lower, where I will set a buy order around my Buy Threshold. However, I am not going to commit to an oversized share size due to my LNTH position being in a "House Money" status, and I don't want to remove that designation on a ticker that is experiencing strong selling pressure.

{kind=link}

If that buy order is filled, I will set an equal sell order at my Sell Target 1 to book profits and keep the position in a "House Money" standing.

Long-term, this data has not weakened my bullish sentiment and I will keep LNTH in the Compounding Healthcare "Bioreactor" growth portfolio with a conviction rating of 4 out of 5.

For further details see:

Lantheus Stock: Looking To Add After SPLASH's Belly-Flop