CTLT - Laughing Water Capital Q4 2022 Letter

Summary

- Laughing Water Capital is a concentrated, long-biased investment partnership open to accredited investors.

- For the fourth quarter of 2022, an investment in Class A shares of Laughing Water Capital, net of all fees and expenses, returned approximately 4.0% vs 7.6% and 6.2% for the SP500TR and R2000 respectively.

- I think right now is the time we should all be thinking about when we will add to our investments.

- There is a ton of evidence to suggest that accepting volatility rather than attempting to avoid it is the best path to investment riches.

Dear Partners,

For the fourth quarter of 2022, an investment in Class A shares of Laughing Water Capital (“LWC”) net of all fees and expenses returned approximately 4.0% vs 7.6% and 6.2% for the SP500TR and R2000 respectively. For the full year, LWC returned approximately -31.7%, vs. -18.1% and -20.4% for the SP500TR and R2000 respectively. Since inception, LWC has returned approximately 209% vs 132.3% and 86.6% for the SP500TR and R2000 respectively. As always, I remind you to please see your individual statements as results may vary based on timing, class, and fund.

To state the obvious, this was a tough year both for the markets broadly, and our portfolio specifically. During periods of uncertainty, investor time horizons tend to shrink considerably as people prefer to pay a premium for the illusion of certainty rather than receive a discount for embracing uncertainty. As a reminder, the core of our strategy is that I deliberately embrace uncertainty, and then spend most of my time attempting to separate uncertainty from risk.

I am not reinventing the wheel with this approach.

I am simply walking in the footsteps of most of history’s most successful public market equity investors. I walk this path confident that the key to outsized returns over reasonable periods of time is finding ways to benefit from the dual forces of increased earnings power and improved perception. Quite simply, it is difficult to benefit from improving perception if one focuses on investments that are already loved, and thus expensive.

Key to making this approach work is investing with a 3 to 5+ year view, which history has shown is a distinct competitive advantage; assuming you can survive 3 to 5 year periods. As you know, our partnership has been specifically constructed to protect this competitive advantage. However, deliberately embracing uncertainty at a time when the world craves certainty above all else leaves us susceptible to mark to market risk, which I believe is mostly where we find ourselves today. The other contributor to our poor performance in 2022 has been mistakes of commission by yours truly. Unfortunately, this will always be the case. As the largest individual investor in the funds, and as the individual with the largest percentage of their net worth invested in the funds, I feel this poor performance more than anyone, and I assure you: it stinks.

However, I sleep well at night and remain excited for the future because all of recorded history is on our side. None of today’s scary headlines can convince me that focusing on good businesses led by good people, and valuing them based on a normalized multiple of normalized earnings is not the best path to investment riches. At present, I believe that our collection of businesses is unusually well primed to both improve their earnings power dramatically over the next few years, and benefit from exceptionally large changes to perception over that period. While nothing is guaranteed except for additional bumps in the road along the way, this combination should result in returns that more than compensate us for the recent drawdown. For this reason, my family and I continue to have almost all of our net worth invested in our strategy right alongside you. Our interests are aligned.

Edge, Where Are We Now, Portfolio Review

“the test of a first-rate intelligence is the ability to hold two opposed ideas in the mind at the same time, and still retain the ability to function”

~F. Scott Fitzgerald

Broadly speaking, I think there are four types of edge when it comes to investing: informational, structural, analytical, and behavioral. In my view, at present it is the last one that is most important.

Broadly speaking, I think there are three factors that should drive our high-level investment decision making: valuation, sentiment, and macro. In my view, it is the last one that is least important.

As I have written in past letters, for a variety of evolutionary and biological reasons people tend to be hardwired in a way that prevents them from realizing the full potential of their investments. Perhaps the best-known example of this comes from Peter Lynch’s Magellan Fund, which compounded at ~30% a year during Lynch’s 14 year tenure, while the average investor reportedly lost money.

If you pay attention to the financial press (I suggest you don’t), you are aware that the pundits are eagerly saying that “stocks” are not cheap these days, and there are storm clouds on the horizon. However, they do not mention which stocks they are talking about. The fact is that if you look past the SP500, which is what most people think of when they hear “stocks,” then the story is dramatically different, (and much less interesting if you are in the business of collecting eyeballs and clicks).

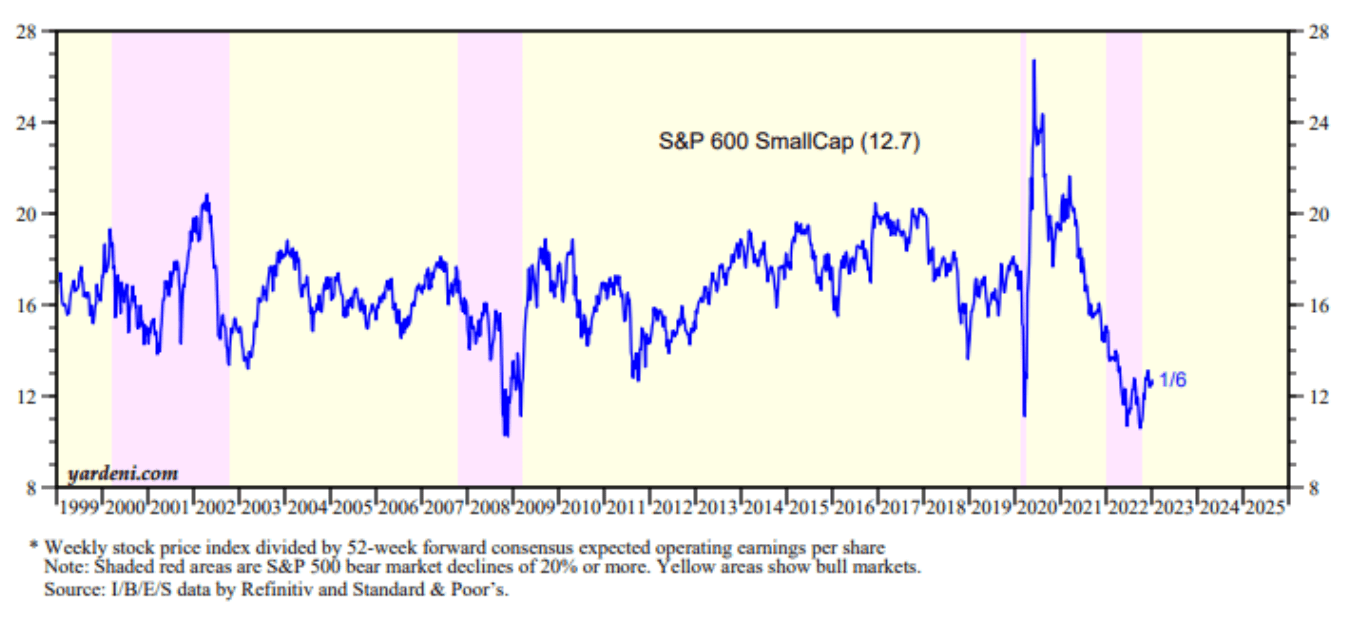

While at present “stocks” might not be cheap relative to history, there are a lot of cheap stocks out there. Specifically, small cap stocks, where I spend most of my time, are at historically low valuation levels, having only been cheaper over the last 2+ decades on a forward earnings basis during the Great Financial Crisis and in the depths of Covid. As a reminder, at those times people were convinced that the entire global financial system would collapse and a decimation of the global population was on the horizon.

{kind=link}

As always, I do not know what will come next with macro, and it is entirely possible that rates continue to tick up, inflation continues to tick up, and that we face a recession. However, the second derivative of rate moves has already declined, inflation is already declining, and most importantly, valuation levels suggest that small cap stocks are already pricing in a severe recession. I believe this backdrop is very exciting for our long term and small cap focused strategy: the odds for success appear to be heavily tilted in our favor.

The problem however is that during difficult periods, correlations tend to go to one. It is entirely possible that weak economic data and/or earnings revisions drag down the SP500 to levels where it too is historically cheap, and small cap stocks move down in tandem, despite the fact that they are already historically cheap. Thus I think it is possible that we are in a period where bulls and bears may both be right, and one’s timeframe will be all that matters. This comes down to behavior.

The fact is that while in difficult periods correlations may go to one, they do not stay there. At some point, despite all of the macro noise, earnings power will be the North Star. If we wait until this is obvious, it will be too late.

The bet we are making is that for the companies in our portfolio, earnings power will be significantly higher and perception will be significantly better a few years from now, regardless of what happens next month or next quarter with macro. My analysis is typically focused on some very specific temporary problem or transition or opportunity that is unique to each company that we own. If on the whole our properly incentivized management partners are able to solve their unique problems and/or successfully transition their businesses, then the intermediate term future will be completely different than the near- term diagnosis, and we will be richly rewarded for our patience, despite some inevitable errors along the way.

It must be noted however that this bet says very little about the path our stocks will take from now until their intermediate term success. Our collection of businesses is not completely immune to economic cycles, and even if I am ultimately proved correct in my belief that their cyclicality is less than the market believes and/or already reflected in their prices, over shorter periods of time stock prices will be determined by mob rule. This is always the case.

It has been said that the key to successful investing is being comfortable holding 2 conflicting ideas in your head at once. This is because if you wait for everything to appear perfect, you will pay a steep price for the privilege and likely wind up disappointed. This is true at the company level, as well as at the macro level. Right now we must be comfortable with the idea that the near term macro conditions may be challenging, but the intermediate and long term rewards should be substantial.

The key is to stay focused on the idea that the world will be somewhat normal at some point in the next 3-5 years, and own businesses whose unique circumstances will allow them to do well enough in non- normal periods. In this regard I think we are very well positioned.

Top 5 Disclosed Holdings

Below you will find brief summaries of how I believe earnings power and perception will change at our top 5 investments over the next few years. I have included more detailed descriptions in the appendix to this letter. There are a few things to note.

First, I believe that each of these investments has a “heads we make a little, tails we make a lot” dynamic.

They are leaders in their respective niches, beneficiaries of strong secular tailwinds, and well positioned to excel in the years to come. Second, the potential upside is eye-popping, to the point I fear sharing my honest analysis may come across as promotional. I assure you, that is not my intent. Rather, I am hoping to illustrate why I think it is worth being invested with a 3 to 5 year view instead of focusing entirely on inflation data and interest rates. Third, while each of these investments has their own idiosyncratic opportunities to benefit from improving perception in the years to come, all of them should benefit from a broad re-rating as the world inevitably moves past the recession fears that currently weigh on small cap stocks. Fourth, as a reminder, we want to have different kinds of bets, not just in terms of sector, but also in terms of how earnings power will improve, and how perception will change over time. This means that some of our investments are cheap on current normalized earnings, while some must navigate near term problems and opportunities for their full potential to be realized. Importantly, in all cases I expect that each of these businesses will look very different in a few years than they do today by simply stepping over low hurdles, and there is a clear path toward significant free cash flow. In my estimation the market has not yet fully realized their potential.

API Group ( APG ) – APG is the world’s leading provider of Life Safety services, which can be thought of as our fire safety business. Earnings will improve organically through continuing to take share from mom & pop players, widening margins through route density and scale, improving business mix by pruning less profitable operations, and improving operations at a recently acquired (and previously neglected) European business.

Perception will change as the stink of formerly being a SPAC wears off, and as the market realizes that with much of revenue tied to statutorily mandated work, the ability to easily flex labor costs, and favorable working capital dynamics during downturns, this business is more resilient than it gets credit for.

As revenue grows organically 6-7% a year, and margins widen through increased efficiency and density, I believe EBITDA will grow by ~60% over the next 3-4 years, which suggests APG currently trades at ~6x the FCF the Company will generate, assuming conversion of preferred shares. Additional upside is possible, perhaps even likely, as there is a long track record of successful bolt on M&A, and a very capable sponsor group will seek to maximize upside through creative capital allocation. As perception improves and revenue mix moves increasingly toward statutorily required work, I believe this business could ultimately trade at 20x FCF, which would imply ~200% upside.

Avid Bioservices ( CDMO ) – Avid is our large molecule contract drug manufacturing business. The industry has historically been capacity constrained, and the Company is primed to more than double capacity over the next few quarters. Avid’s long tenured regulatory track record is a distinct competitive advantage vs. upstarts that may also seek to add capacity, and it is likely that Avid is adding new capacity at the request of customers. As this new capacity is filled in the not-too-distant future, the Company will benefit from significant operating leverage, which will drive earnings power.

Perception should change as Avid fills its new capacity and develops into a free cash flow machine.

If CDMO is able to fill their new capacity, they should be able to generate somewhere around $120M in steady state FCF, assuming conversion of convertible debt and utilization of substantial NOLs. This implies CDMO currently trades at ~7x intermediate term FCF. It would not surprise me to see fast growing, recession resistant cash flows valued at 20x, suggesting ~200% upside is possible. This may prove conservative as the Company will retain significant strategic optionality at that time.

Hilton Grand Vacations ( HGV ) – HGV combines the impossible to replicate Hilton brand with a nearly impossible to replicate portfolio of vacation properties into the Hilton time share business. HGV has 25+ years of cohort data that suggests that for every $1 a customer spends, they will spend an additional $1.10 as their tenure matures. Thus, the maturation of the existing owner base alone should drive earnings power higher with time. However, the real prize will come from the recent acquisition of Diamond Resorts. In brief, I expect that layering the Hilton brand and best practices over the Diamond business will greatly improve earnings.

Perception will change as the market appreciates the benefits that will come from the Diamond merger and realizes that with ~70% of revenue either recurring or highly predictable and 30% of revenue tied to a flexible cost structure, this business is much more resilient than it appears.

If I am correct on how I think earnings power and perception will evolve in the years to come, HGV currently trades at ~6x normalized FCF looking out 2 years. This will likely prove conservative as the share count is likely to shrink as the Company continues to aggressively repurchase their own shares. I believe the multiple can easily double from 6x, and mid-teens is not out of reach as the market comes to appreciate the resilience of the business. Further upside is likely beyond the next 2 years as the Company finalizes the integration of Diamond Resorts, and sells through a $12B inventory position. Ultimately, I believe there is a path toward 300-400% upside in the not-too-distant future.

Thryv, Inc ( THRY ) – Thryv is the “growthiest” of our investments. The Company is using its legacy Yellow Pages business as the base from which to launch a SAAS product that greatly improves operations for small and medium businesses. While this SAAS business could currently be profitable, a highly incentivized and experienced management team is instead steering cash flow back into growth. SMBs are way behind the curve when it comes to moving their operations to the cloud, and as this inevitable change takes place, Thryv will realize considerable growth and operating leverage, which will drive earnings power.

Perception will change as cash flow from the declining Yellow Pages business improves the Company’s balance sheet, and as the software business reaches scale and begins to gush cash. Additionally, THRY is still mostly unknown on Wall Street as it came public through a direct listing and screens as a marketing company, not a software company.

Management has laid out a plan to reach $200M in EBITDA from their SAAS business in 5 years. If they are successful, assuming that the Yellow Pages business is run off suggests that THRY currently trades ~4.5x EBITDA looking out ~5 years. Slower growing SMB software providers trade north of 20x, suggesting that THRY could be up more than 400%. Additional upside is possible as in five years the Company will still only be scratching the surface of a massive secular trend.

Vistry Group PLC ( BVHMF ) – Vistry is our UK homebuilder that recently acquired our previous investment in Countryside Partnerships, to become the largest player in affordable housing in the UK. While at present there are concerns around housing affordability, the UK faces a chronic shortage of housing, and we have already seen actions from both the government and lenders to keep people on the property ladder. Vistry has a clear plan to increase the amount of houses it can deliver while improving margins and earnings power. The real gem however is the Company’s asset light, recession resilient Partnerships business, which focuses on affordable housing. This business should be able to grow double digits and gush free cash flow.

Perception will change – and already is changing – as concerns around affordability fade, and as the market comes to appreciate the resilience of the Partnerships business, which should shortly comprise more than 50% of revenue. Additionally, management has already stated that if the market does not reward them for the Partnerships business, they will take steps to spin it off in a few years.

If I am correct on how I think earnings power and perception will change in the years to come, Vistry can generate GBP 450M in normalized after tax profits from just the Partnerships business looking out 3-4 years. This suggests a multiple of 5x after tax earnings, giving no value to the traditional homebuilding business. 10-14x would be more appropriate for a traditional homebuilder, but would likely be conservative for Vistry given the defensive nature of the Partnerships business. At 18x, the Partnerships business alone would be worth ~250% more than current share prices. Surely the traditional business is worth something as well. Additional upside is probable as the Company will likely soon become an aggressive buyer of its own shares.

As mentioned previously, I have provided more information on the above positions in an appendix to this letter. Again, I realize the potential returns that I have outlined above may seem too good to be true. Rather than focusing on the potential returns, I suggest focusing on the margin of safety. In the event that my view of the unknown future is wrong, I think the valuations are such that we will still generate acceptable returns. The key takeaways should be that our businesses are operating in cockroach type niches with secular tailwinds. Looking out a few years from now people will still need fire safety, the world will still be increasingly relying on biologic drugs, people will still go on vacation, small businesses will still be transitioning their operations to the cloud, and the UK will still be severely under-housed. I believe our businesses are well positioned to benefit from each of these unstoppable trends, and each of our businesses will be significantly stronger a few years from now. Importantly, I believe we are paying low prices too.

Comments on Select Investments

Lifecore Biomedical, Inc. ( LFCR ) – Until recently known as Landec, Inc., in November Lifecore underwent a name change to reflect the fact that the business will soon be a pureplay Contract Drug Manufacturing Organization focused on fill-finish of injectable drugs. There is a lack of capacity in this arena, and a 4 to5 year lead time to add additional capacity, which in my view gives LFCR’s assets tremendous strategic value. Standing in the way of pureplay status is the Company’s continued ownership of a processed avocado business which they have been trying to sell for more than a year. The sale process has clearly been disappointing and dragged on longer than I hoped, likely due to extreme inflation in avocado prices in 2022, which made it difficult to pass on costs, and then a closing of credit markets. The failure to sell the avocado business in a timely manner led to the Company completing a capital raise through a convertible preferred equity in early January. The convertible preferred security will likely lead to dilution which necessarily reduces my estimate of per share equity value, but at the same time the event path has been considerably de-risked.

Cannabis Basket - It is hard to describe our cannabis basket as anything other than a disaster to date. The original thesis was predicated on the idea that this investment would be uncorrelated to interest rates and recession fears, and would instead benefit from secular growth and an easing of the regulatory environment. In essence, it was supposed to act as a hedge of sorts. I continue to think that uncorrelated investments can benefit our portfolio, but uncorrelated and wrong does us no good.

Aimia Inc ( AIM:CA) – Aimia started the year trading at a discount to the cash that would soon hit its balance sheet, giving no value to other investments, some of which I think will prove quite valuable with time. Owning this cash box at a discount was also supposed to act as a hedge of sorts, and it also did not work as intended. Rather, the discount to cash went from reasonable to giant, proving once again that the market can do whatever it wants over shorter periods of time.

New LPs and Add-on Investments

Over the last few letters I have tried to stress the idea of “cheap enough,” as a means to combat the temptation to try to time the bottom of the market’s current downturn. As a founding principle of LWC, I never want to be in a position where I am selling an investment in our partnership. Rather, I want it to be bought by like-minded individuals who have an innate understanding of the benefits that can come from our differentiated approach to investing.

That being said, I think right now is the time we should all be thinking about when we will add to our investments (not just in LWC). This is not me drawing a line in the sand. This is me saying that attempting to call the bottom of any market down turn is a fool’s errand, and dollar cost averaging is a very effective strategy. I suggest coming up with a plan around either timing or broad market levels that will spur you to action when appropriate. Personally, I will be having a liquidity event tied to my primary residence near the end of Q1, and I intend to add to my investment in LWC.

I am not the only one deploying capital despite the current macro backdrop.

In recent months, out of our 10 largest investments, there has been insider buying and/or stock repurchases by properly incentivized management teams at all of them except for one. I assure you, these insiders and management partners do not have a crystal ball, but I believe they view the odds of future success as very favorable. I strongly agree.

Administrative Matters: K1s and Annual Audit

The team at Spicer Jeffries is hard at work on our year end audit and K1s, and I expect that the necessary documents will be available well before Tax Day. The funds ended the year in a realized loss position, so I expect that taxes should be somewhere between de minimis and non-existent, although I cannot guarantee that at this time, and tax obligations may vary based on the timing of individual cash flows.

Looking Forward

As always, near term market action is unknown and unknowable. What seems clear however is that just about everyone is expecting cuts to earnings estimates and a recession of unknown depth and duration. What is harder to know is if the fact that just about everyone is expecting these things to happen will have an impact on whether or not they actually happen, or whether or not they negatively impact stock prices. These are questions without reliable answers, and the track record of those who try to predict these things is horrible.

As investors we have to make a choice. We can try to navigate every unknowable bump in the road, or we can except the bumps and stay focused on the destination. I am firmly committed to the latter option as there is a ton of evidence to suggest that accepting volatility rather than attempting to avoid it is the best path to investment riches. I am well aware that almost everything I have written about the businesses we own in this letter and others is grounded in a sort of naïve optimism.

I am also well aware that naïve optimism is undefeated over reasonable periods of time.

What we must get comfortable with is that period between now and then, because despite what I think are reasonable paths toward fantastic returns, I promise you those returns will not come in a straight line. Despite the macro uncertainty, I can say that with small cap stocks at historically cheap levels, and with what I believe to be an exceptional group of businesses in our portfolio, I think that the odds of success over intermediate and longer-term periods appear to be heavily tilted in our favor.

Please let me know if you have any questions,

Matthew Sweeney,

CFA Managing Partner, Laughing Water Capital

Appendix: More on Our Top 5 Disclosed Holdings

API Group ( APG )

APG was first introduced in the Q2 2020 letter, and we have owned it as a small position since that time. More recently APG became a large position as I added shares following a near 50% decline in price earlier this year. The business has two segments, both of which are recession resistant. Safety Services (70% of revenue) which focuses on fire prevention services, and Specialty Services (30% of revenue) which primarily works with utility and telecom customers. In brief, fire prevention is still mandated by law regardless of the economy, and utilities and telecom continue to operate regardless of the economy.

Management has laid out a clear path toward earnings power improvement in the years to come. First, the industry is fragmented with many mom-and-pop players, and APG has been able to grow organically 6-7% a year for decades through a branch led model focused on providing better service, which in some ways is tied to scale. Management has indicated they are confident they can continue this cadence, which is likely conservative as industry rag Engineering News Record has predicted that fire safety should grow 9%, and recent growth has far exceeded the 6-7% estimate. Second, since the financial crisis the business has been focusing more and more on recurring services and inspection work, which is more predictable, and higher margin. Importantly, incremental margins tied to route density are significantly higher than run rate margins. Lastly, about a year ago APG acquired European fire and security assets ( CHUBB ) from Carrier Group ( CARR ). These businesses were an afterthought for CARR, which is primarily focused on HVAC. At a recent Investor Day, management detailed the opportunity to improve operations at these formerly neglected assets.

Putting it all together, management has outlined a plan that if successful should see normalized EBITDA and FCF grow by ~60% in the not-too-distant future. These estimates however are based solely on organic growth, and give no credit for intelligent capital allocation. This should be conservative as APG has a long and impressive track record of growth through acquisitions, and Co-Chairs Martin Franklin and James Lillie have a long track record of fantastic capital allocation and creative capital structure management.

In addition to a reasonable path toward earnings power improvement, perception is very likely to improve in the years to come. First, the Company flexed their balance sheet to acquire Chubb, but leverage should come down one turn per year as the Company executes. This deleveraging will accrete to the equity. Second, the taint associated with being a post SPAC equity will fade with time. Third, at present the SPAC sponsors have an unusual compensation scheme whereby they are paid on performance of common shares through a preferred equity structure that results in dilution. This arrangement clearly aligns the sponsors with equity holders, but is confusing to some investors and off-putting to others. In either case, it will be eliminated in 2026, making the story cleaner. Fourth, the sell side has been critical of the recent Chubb acquisition, but in my view this criticism is focused on the rearview mirror. The windshield should become more clear with time. As the Company executes, I do not think it is unreasonable to think that APG can trade at 16x EBITDA or 20x FCF, in line with other Engineering & Construction firms that in my view service less desirable end markets.

Taken together, I believe the combination of reasonable growth, widening margins, and improving perception can lead to a stock in the low $50s in a few years, assuming that management does not do anything smart. However, given the combination of skin in the game and a world class track record of capital allocation by the Co-chairs, this would be a very poor assumption. I think it is very likely that instead of sitting idly, they will be attempting to realize value in every way possible, with some combination of larger scale M&A, tax-efficiently spinning or selling the Specialty Services business, and returning capital via buybacks all representing reasonable paths forward. If things do not unfold as I hope, I think we will still do well over time. I would note that recent insider buying suggests that I am not alone in my optimism.

Avid Bioservices ( CDMO )

Avid, our large molecule, small batch, domestic Contract Drug Manufacturing Organization, should be familiar as CDMO was a meaningful position in the portfolio for several years before I reduced it late in 2021. Following a steep decline in price, I re-purchased shares earlier this year, and for a few months I looked brilliant as shares quickly rallied. However, more recently shares retreated once again. The decline was sparked by cautious comments out of Sartorius AG ( SRT.GR ), a provider of picks and shovels to the biologic CDMO industry, and the decline was made worse by a guidance cut by Catalent ( CTLT ), a larger CDMO with a focus on biologics. Avid Bio was thrown out with the bathwater, and when CDMO reported that backlog “only” grew 23% in fiscal Q2’23, shares fell further despite the fact that CDMO actually raised guidance.

In my view, this recent sell off is just noise.

Reading past the headlines from SRT.GR and CTLT reveals that weakness at both of these companies is mostly tied to the rolling off of Covid vaccine manufacturing, centered in Europe, and/or related to divisions other than biologics. Of course, CDMO does not have European exposure, has zero Covid business, and is not exposed to other verticals such as OTC health supplements that are more directly tied to consumer spending.

As for CDMO’s “disappointing” backlog growth, over the years that we have owned CDMO backlog has been consistently lumpy on a quarterly basis, and the Company has consistently outperformed over longer periods of time. Management took pains to note that a few days difference in timing can result in big swings to backlog, and further noted that in the past when new capacity came online, backlog jumped higher almost in lockstep.

I am reading tea leaves here, but with an additional $100M of capacity coming online in calendar Q1’23 (vs fiscal ’23 guidance of $150M in revenue), it is at least curious that management would remind investors that in the past capacity expansion has led directly to jumps in backlog. An additional ~$150M of capacity should come online in the summer of 2023. Moving past tea leaves and on to facts, the Company also noted that Process Development revenues grew 74% YoY and 37% sequentially.

In my view, while backlog should not be completely ignored, the real leading indicator in this business is Process Development. Process Development is essentially when a customer comes and says, 'lets run some super small batches to make sure we have the process down, and when we know that the process is sound, we will start to run bigger batches.' In fact, according to management, Process Development revenue is typically ~15% of the total amount a customer will spend with CDMO, which again suggests that CDMO’s new capacity will be filled rather quickly.

Regardless of quarterly lumpiness, earnings power at CDMO is highly likely to improve in the intermediate term. As mentioned above, revenue capacity should be somewhere around $400M by summer of 2023. This increased capacity is intended to meet huge secular tailwinds as drug development is increasingly focused on large molecules, with more than 5,500 biologics awaiting FDA approval at present. Further confidence can be gained by recognizing that historically industry capacity has not been added on spec. Rather, capacity is typically added when existing and potential customers ask for it based on their own pipelines. Examining the pipelines of CDMO’s existing customers such as Halozyme ( HALO ) seems to suggest that this fact pattern has been playing out at CDMO.

To be clear, I cannot tell you with any certainty how long it will take to fill CDMO’s new capacity. While I believe they have a distinct competitive advantage due to their impressive and long-standing regulatory track record, they are not the only industry participant adding capacity. Additionally, it is possible or perhaps even likely that a more difficult fundraising environment will slow the cadence of work from development stage biopharma companies. However, when this capacity is filled CDMO should be able to generate somewhere around $120M in steady state FCF, versus a current market cap of ~$850M.

As the Company grows into its new footprint, perception should re-rate dramatically higher as the Company will be more predictable, have wider margins, and generate cash rather than consume cash. Further, the Company will maintain tremendous strategic optionality. They could choose to expand further organically, they could become an acquiror, they would be an attractive target for larger players, or they could return capital to shareholders. This optionality will likely lead to a higher multiple for CDMO, but if we assume 20x steady state FCF is conservatively the right multiple for a fast growing, recession resilient business, then shares would trade ~200% higher than they do at present. Whether it takes 3 years or 5 years to reach that point, we should be happy either way. If I am wrong, and CDMO falls short of filling their pending capacity additions, the margin of safety is wide enough that we should still do ok.

Hilton Grand Vacations ( HGV )

HGV is the Hilton branded time share business that was spun off from Hilton Hotels in 2017. I first introduced HGV to LPs at the 2022 LWC LP meeting as a business that is often perceived as cyclical, yet is nowhere near as cyclical as one would expect. For a more detailed discussion of HGV, I would refer you to the t r a n s c r i p t .

At present, HGV trades at a bit more than 8x my estimate of 2022 normalized FCF, which suggests the market believes that HGV is subject to a cyclical downturn and/or overearning due to a post Covid bounce. It is of course impossible to completely rule out these risks, but in my view they are unfounded. As for the cyclical risk, I believe HGV gets tossed into the same bucket as hotels, but in actuality 50% of EBITDA is recurring in nature, another 20% is highly predictable, and the last 30% is tied to a flexible cost structure. Additionally, the timeshare industry grew through every recession prior the Great Financial Crisis, and HGV revenue only declined 3% through the GFC. This of course does not guarantee there won’t be bumps in the road as we move forward. However, even if the Company is presently over earning, looking outa few years, earnings power is likely to be substantially higher than it is today.

First, the Company has 25 years of cohort data that demonstrates that members upgrade their spend very predictably over time as they add on more time, or utilize larger units. This suggests that members that joined over the last few years alone will drive earnings power higher as they mature. Additionally, at present HGV is in an enviable inventory position, with ~$12B in the pipeline.

Most exciting, HGV recently acquired Diamond Resorts, and is presently re-branding Diamond operations under the Hilton umbrella. While there are obvious cost savings tied to reducing duplicate functions, the real prize in this merger will be the improvements tied to overlaying HGV’s best in class sales practices on Diamond’s properties, as well as applying the benefits of the Hilton brand to the Diamond properties. Quite simply, Hilton is the #1 brand globally for hotel travel, which makes acquiring customers for HGV much easier and cheaper. Ask yourself this. If you were considering purchasing a time share, who would you trust more? Hilton, or Diamond?

There are other more tangible benefits as well. For example, in the time share business unused inventory is typically made available to the public. For Diamond, this has historically meant spending a fortune on Google keywords to advertise the inventory, and as a result Diamond has run their rental business at a loss. In contrast, when HGV has unused inventory, they simply make it available to the 139 million members of Hilton’s Loyalty program, which allows them to realize a nice profit. Applying HGV’s historic margin in Rental to Diamond’s historic revenue in Rental suggests well more than $100M of EBITDA can be un-locked by HGV in Rental alone.

To be fair, the Diamond transaction is not without risk. Most notably, Diamond’s customers have a slightly lower FICO score and lower average income than HGV customers, and these customers were underwritten by Diamond, not HGV, all of which suggest that these customers may be more susceptible in an economic downturn. Thus far however, there is no sign of softness in travel demand, with companies from American Express to Delta commenting that they expect travel to remain strong. It also may be worth noting that Blue Green Vacations ( BVH ), an industry player with even lower quality customers and brand than Diamond, recently attempted to repurchase ~23% of their existing equity through a tender offer. Considering that BVH is ~40% owned by insiders, this suggests that they are not worried by macro concerns in the near term.

Returning to how earnings power is likely to improve on a per share basis, there are early signs that HGV might become a “cannibal,” and aggressively shrink its share count in the years to come. From the Company’s 2017 debut as a public company until the 2021 purchase of Diamond Resorts which involved issuing equity, HGV shrank its share count by 13%. In early 2022 the company resumed this pattern with a $500M repurchase authorization, of which $290M still remains. I think the right mental model for this investment might be similar to Eddie Lampert with AutoZone in the early 2000s, which generated fantastic returns for investors. Every year, the top line can grow a bit, margins can widen a bit allowing EBITDA to grow a bit more, and the increased EBITDA can support a bit more debt, and the excess cash can be used to retire shares. Key to this potential path forward is the fact that HGV is currently under-levered, primed for significant increases in earnings power, engaged in capital efficient development, and trading at a low multiple.

If HGV does develop into a cannibal, this will likely contribute to a change in perception, which will eventually drive a re-rating of the stock. However, even without the cannibal angle, perception of HGV stock should improve on several levels in the years to come. Most obviously, at some point the market will move past cyclical fears, and shares will re-rate higher. I view this as a “when,” not an “if.” Additionally, I believe there is a chance that the entire industry is awarded with a higher “normal” multiple over time. First, with time and through normal cycles the market is likely to figure out that these businesses are not as cyclical as they appear at first glance. I think this is especially true as the Company has yet to face a non-Covid recession in the age of Instagram, which has placed a premium on travel and experiences, which theoretically will allow the industry to hold up better during downturns than it has historically.

Further, at present there is likely some ESG concern overhanging the industry, as historically the industry had multiple bad-actors at the low end, and there is a belief that people get “trapped” in time shares. That may have been true historically, and it was certainly true at the low end, but in my view there is too much reputation risk for branded players to engage in shenanigans with customers. Hilton hotels is the number one ranked hotel brand globally, and quite simply it is not worth putting that status at risk to trap people in a timeshare. Attrition at HGV runs in the low single digits, and the Company has an active inventory recapture program, which suggest that customers are both happy and able to leave when they want.

In sum, simply assuming a more normal multiple on current normalized FCF potential could lead our investment to significant upside. However, as the Diamond acquisition matures and as recent cohorts upgrade their spend, it is not hard to imagine FCF more than doubling in the years to come. A doubling in earnings power and significant multiple expansion can lead to potential multi-bagger returns with time.

Thryv Inc ( THRY )

Thryv is our fast-growing software company that is modernizing the way in which small and medium businesses operate by bringing their operations into the cloud. The Company also owns the Yellow Pages as well as other digital marketing tools which are clearly in decline. However, these businesses 1) generate gobs of cash which allows Thryv to self-fund their software efforts and 2) represent a clear competitive advantage on distribution as Thryv has a pre-existing relationship through the Yellow Pages and related with about a third of their new software customers. Another third of new customers come through referral.

A distribution advantage is rare in SAAS, and allows THRY to have lower Customer Acquisition Costs than the competition, which is especially important in SMB world due to how diffuse the potential customer base is. A lower CAC combined with internal funding in a world where access to capital has dried up puts Thryv on a different playing field than other upstarts. To be fair, SMB can be rocky in a recession, but Thryv specifically services businesses that focus on “the nasty things in life” such as plumbers, who typically do not suffer during recessions.

Earnings power will grow at Thryv through topline growth tied to huge secular tail winds and operating leverage as the Company gains scale. The vast majority of small and medium businesses have not yet moved their operations to the cloud, and are instead relying on a “system” of post-it notes, excel spread sheets, and paper filing cabinets to operate. As their competitors embrace products like Thryv – where the entire customer experience from scheduling, to estimating, to invoicing and payments, to follow-up calls, etcetera can be done through an app and text messages – more and more SMBs will be forced to adopt similar solutions, or risk losing their customers to competitors who provide a better customer experience through software. This sort of secular technological change has a strong track record of success through difficult economic periods, with the rise of online travel agencies during the recession of the early 2000s being a prime example.

At an April Investor Day, the Company laid out ambitious plans to reach $1B in revenue and $200M in EBITDA in 5 years, and $4B in revenue and $800M+ in EBITDA in 10 years. Of course, all long-term projections should be taken with a grain of salt, but zooming out suggests that the 5 year targets are reasonable, if not conservative. To reach $1B in revenues, the Company thinks they will need 150,000 customers, or more than 90,000 more than I estimate they have today. To frame that, consider that the Company believes there are 4 million American businesses and an additional 4 million international businesses that make up their Total Addressable Market. In other words, the Company is forecasting less than 2% penetration of their TAM, which is a breath of fresh air versus other SAAS companies that require “winner take all” economics to be successful.

Framed differently, 150,000 customers is ~38% of the ~400,000 existing Yellow Pages customers, or only a bit higher than the 33% of new customers that are presently coming to Thryv via the Yellow Pages. Thus, there may be a path to success here even if Thryv does not move much beyond the Yellow Pages. Of course, with more than a third of new business coming from referrals, we know that Thryv is already well beyond the Yellow Pages ecosystem.

A third way to think of reaching 150,000 customers can be seen through the eyes of the Baby Boomers. We have all heard that 10,000 Baby Boomers retire every day. What is less well known is that these Baby Boomers own an estimated 4 million small businesses, and it is estimated that 3.3 million of those businesses will change hands over the next 5-10 years i . While some of these businesses have surely already modernized their systems, what are the odds that the next generation of small business owners who were raised as digital natives will continue on with a system of sticky notes rather than modernizing the businesses’ operating procedures by embracing software?

Lastly, two of management’s key assumptions are that they will lose market share in the years to come, and that their growth will be entirely organic. Given that at present they have the best product at the lowest price point with well-defined distribution advantages, assuming a loss of market share appears conservative. Further, given that the management team here has executed more than 100 transactions in the past and competitors may struggle in a constrained funding environment, it would not surprise me to see M&A materialize as another leg of the Thryv stool in the years to come.

Perception will change in several ways in the years to come. In the immediate term, I believe it is likely that the next round of 13F filings will show that Mudrick Capital no longer owns THRY. Mudrick, a distressed debt fund that owned THRY equity as a result of the 2016 bankruptcy of Dex Media, started 2022 as the owner of approximately 50% of THRY equity, and has been a steady seller as the original bankruptcy investment has matured. Having a 50% owner liquidate their position has been a clear overhang on the stock, which I believe will be lifted shortly. Second, at present THRY screens as a marketing services company as revenues from the Yellow Pages and related businesses are significantly larger than the SAAS business. However, at some point in the next ~3 years, revenue from the SAAS business should eclipse revenue from the Yellow Pages business, allowing the combined entity to be reclassified as a software company, which should draw in an entirely new arena of potential investors. Lastly – and most importantly – at present Thryv is a sum of the parts story where analysts struggle to value a long duration tech asset combined with a declining cash cow. As the Company matures the story will be cleaned up, and the market will be able to cleanly value fast growing free cash flow generated by a best-in-class software business with tremendous tailwinds.

In my view, if Management is able to achieve their 5 year targets and the market were to value THRY similarly to Paychex ( PAYX ), a more mature provider of software to small and medium businesses, shares would trade ~400% higher than they do at present. If the future does not unfold as expected, we should still do well. I would note that CEO Joe Walsh appears to share this view as he has recently purchased stock in the open market despite already owning ~7% of the equity.

Vistry Group ( BVHMF )

Our investment in Countryside Partnerships, a UK homebuilder with an asset light division, has evolved into Vistry following the November acquisition of Countryside by Vistry. I detailed the mistakes I made with Countryside a t L W C ’ s 2 0 2 2 I n v e s t o r D a y , as well as why I think the opportunity going forward is more attractive than ever. I would note that my current intermediate term optimism is at odds with UK housing market headlines, all of which are dire. However, if you read past the headlines, you will see that current weakness will likely lead to the strong getting stronger. Vistry is arguably the strongest.

The key to this investment is the Partnerships business, which is growing at double digits (completions up 17.6% in 2022) and more economically resilient than traditional housing. The Partnerships business sees Vistry partner with local housing authorities in arrangements that typically see the housing authorities contribute land, while Vistry contributes their homebuilding expertise. More than half of planned homes are typically pre-sold as affordable housing or as private rental for sale. This capital light arrangement allows Vistry to earn 40+% ROCEs, while pre-selling homes eliminates sales risk. Importantly, housing associations typically work with Homes England - a quasi-government agency tasked with funding affordable housing - to pre-fund their housing development in conjunction with 5 year plans. This reduces the impact of macro conditions on Partnership completions. As CEO Greg Fitzgerald recently commented, “Our partnerships business is extremely well placed to meet the high level [of demand] that is there. And of course, that’s countercyclical. If the market comes off, partnerships will do better than they’re currently forecasting.”

At present, Vistry is valued as a traditional homebuilder, with management even commenting that they believe they get no credit for the value of the Partnerships business. Over time, and through a cycle, perception will likely change as the resilience of the Partnerships business is demonstrated.

In my view, the Partnerships business alone should be able to generate GBP 600M of EBIT looking out a few years. The Company is in a net cash position, so we can theoretically ignore the interest payments, and then deduct taxes and reach normalized after tax earnings of GBP 450M for just the Partnerships business. At present, this suggests a multiple of ~5x earnings looking out a few years. A low double-digit multiple does not strike me as inappropriate for a traditional homebuilder, and given the superior model of the Partnerships business, a high teen or even 20x multiple may ultimately be appropriate, suggesting that ~400% upside is possible for the combined business. Additional upside is likely in the form of aggressive buybacks. Vistry was a buyer of its own shares prior to the Countryside merger, and CEO Greg Fitzgerald recently bought GBP 5M worth of stock through an entity he controls, which suggests he believes the future is bright.

Footnotesi https://www.thegoldhillgroup.com/baby-boomer-businesses-for- sale/#:~:text=Baby%20boomers%20own%20about%20two,(Source%3A%20Securian%20Financial). |

| Disclaimer: This document, which is being provided on a confidential basis, shall not constitute an offer to sell or the solicitation of any offer to buy which may only be made at the time a qualified offeree receives a confidential private offering memorandum (“CPOM”) / confidential explanatory memorandum (“CEM”), which contains important information (including investment objective, policies, risk factors, fees, tax implications and relevant qualifications), and only in those jurisdictions where permitted by law. In the case of any inconsistency between the descriptions or terms in this document and the CPOM/CEM, the CPOM/CEM shall control. These securities shall not be offered or sold in any jurisdiction in which such offer, solicitation or sale would be unlawful until the requirements of the laws of such jurisdiction have been satisfied. This document is not intended for public use or distribution. While all the information prepared in this document is believed to be accurate, Laughing Water Capital, LP and LW Capital Management, LLC make no express warranty as to the completeness or accuracy, nor can they accept responsibility for errors appearing in the document. An investment in the fund/partnership is speculative and involves a high degree of risk. Opportunities for withdrawal/redemption and transferability of interests are restricted, so investors may not have access to capital when it is needed. There is no secondary market for the interests and none is expected to develop. The portfolio is under the sole trading authority of the general partner/investment manager. A portion of the trades executed may take place on non-U.S. exchanges. Leverage may be employed in the portfolio, which can make investment performance volatile. The portfolio is concentrated, which leads to increased volatility. An investor should not make an investment, unless it is prepared to lose all or a substantial portion of its investment. The fees and expenses charged in connection with this investment may be higher than the fees and expenses of other investment alternatives and may offset profits. There is no guarantee that the investment objective will be achieved. Moreover, the past performance of the investment team should not be construed as an indicator of future performance. Any projections, market outlooks or estimates in this document are forward-looking statements and are based upon certain assumptions. Other events which were not taken into account may occur and may significantly affect the returns or performance of the fund/partnership. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. The enclosed material is confidential and not to be reproduced or redistributed in whole or in part without the prior written consent of LW Capital Management, LLC. The information in this material is only current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Any statements of opinion constitute only current opinions of Laughing Water Capital LP, which are subject to change and which Laughing Water Capital LP does not undertake to update. Due to, among other things, the volatile nature of the markets, an investment in the fund/partnership may only be suitable for certain investors. Parties should independently investigate any investment strategy or manager, and should consult with qualified investment, legal and tax professionals before making any investment. The fund/partnership is not registered under the investment company act of 1940, as amended, in reliance on an exemption there under. Interests in the fund/partnership have not been registered under the securities act of 1933, as amended, or the securities laws of any state and are being offered and sold in reliance on exemptions from the registration requirements of said act and laws. The S&P 500 and Russell 2000 are indices of US equities. They are included for informational purposes only and may not be representative of the type of investments made by the fund. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Laughing Water Capital Q4 2022 Letter