CA - Laurentian Bank: Preferreds Offer An Interesting Setup Into Reset

2023-12-28 11:00:00 ET

Summary

- Laurentian Bank has replaced its CEO and named a new Chair of the Board following a major IT outage.

- The bank's profitability metrics are the worst among Canadian banks.

- The failed sale rubbed salt into the wounds and the bank was the worst performer amongst peers for 2023.

- Despite its challenges, there may be deep value in Laurentian Bank, with potential for significant returns if it improves its performance even marginally.

The drama at Laurentian Bank of Canada ( LB:CA ) does not seem to end. The eighth largest of the Canadian banks by size, Laurentian was once known as one of the most conservative bastions of the Canadian banking system. But it has lost its footing over the last few years as the stodgy old ways have had competitors digging into the bank's previously well-defended territories. The bank's primary metrics of profitability, return on tangible equity, and efficiency ratio are the worst among the Canadian banks we cover. The closest to this performance has been Canadian Western Bank ( CWB:CA ), and even that stands head and shoulders over Laurentian. Tired of disappointing legions of investors, the bank did a "strategic review". Many took that as a sign that the bank could be sold as a whole. That did not happen, and Laurentian stock cratered to new lows. The chart below should show when the two announcements happened.

The selloff was made worse as the company also announced that it had suffered a major outage during a planned maintenance event.

Laurentian Bank has replaced its CEO and named a new chair of the board, following a major IT outage last week.

Eric Provost was named president and chief executive of Canada's seventh largest lender on Monday, replacing Rania Llewellyn.

Provost was most recently Laurentian's group head of personal and commercial banking.

The bank also said director Michael Boychuk has been appointed chair of its board of directors, replacing Michael Mueller, who has resigned from the board.

"We have experienced challenges recently and the board is confident that Eric will successfully focus the organization on our customer experience and operational effectiveness," Boychuk said in a statement.

"Eric's appointment as CEO follows his exceptional performance leading our commercial banking business and was part of our formal succession planning process."

The moves come after the bank experienced an outage on its mainframe last week during a planned IT maintenance update.

Laurentian said it suffered a mainframe outage last week during a planned IT maintenance update. "At all times customer data and financial information remained secure," the bank said Monday.

Source: CBC

Our Take

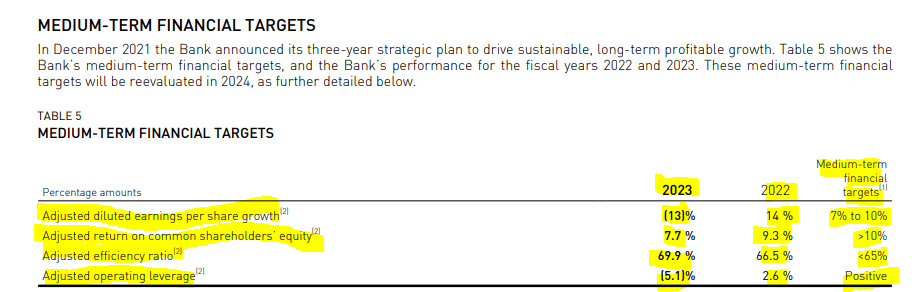

Laurentian Bank has a profitability problem. By that, we mean that it cannot make a lot of money off its assets. We are not remotely suggesting the bank is not profitable. One way to see the issues is by looking at the bank's medium-term targets relative to where it came in 2023 (Laurentian is done with 2023 as it has an October year-end).

Laurentian Q4-2023 Financials.

{kind=link}

All 4 missed, and some by a landslide. Keep in mind that the adjusted efficiency number is counterintuitive. It is a ratio of non-interest expense to revenues and hence higher, is worse.

But the banks have not done too badly in terms of navigating the credit cycles. Below, you can see the provision for credit losses relative to the Big 6 banks in Canada. The outperformance in 2020 is really what it is all about. When things break, Laurentian's risk-averse model comes through.

Laurentian Q2-2023 Presentation

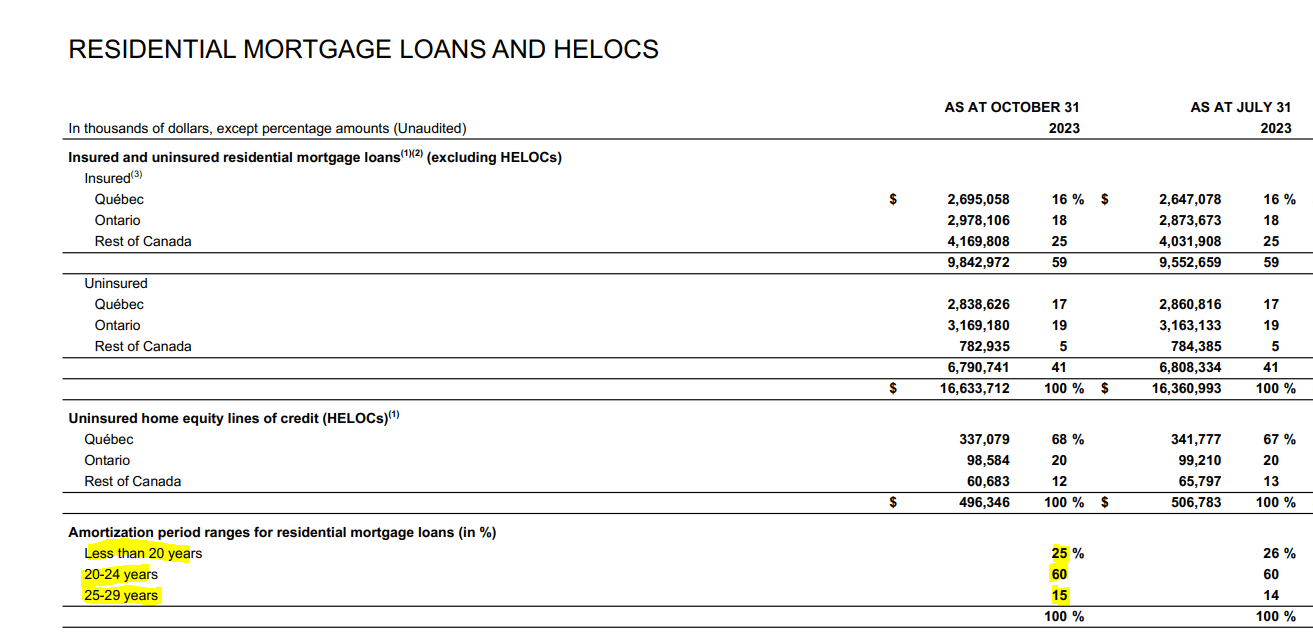

Another metric here is the amortization of residential mortgages. 85% amortize in under 24 years. 15% are in the 24-29 year range.

Laurentian Q4-2023 Financials.

{kind=link}

Now let's look at the Big 6. The Toronto-Dominion Bank ( TD:CA ) and Royal Bank of Canada ( RY:CA ), both have 23% amortizing over more than 35 years. Canadian Imperial Bank of Commerce ( CM:CA ) outdoes those two on that front with 25%. Bank of Montreal ( BMO:CA ), which likely changes its slogan to " Forever Isn't Long Enough ", has 30% in that category. Only The Bank of Nova Scotia ( BNS ) and National Bank of Canada ( NA:CA ) are as conservative as Laurentian.

Hanif Bayat On X

Laurentian's CET1 ratio is also solid and approaching 10%. But that ratio is nowhere near as high as the Big 6 (12.5%-14.6% range), which are systemically important banks. That is by design as Laurentian is not required to maintain the very high CET1 ratios that the other six have to. That ratio differential could be part of the reason the complete sale did not happen. Even if you got past the monopoly clauses, one of the larger banks absorbing Laurentian would likely have to dump a lot of the (relatively) riskier assets to keep the CET1 numbers where they need to be.

But there is some deep value here, even if Laurentian does not actually sell itself over the next 5 years. Of course, the long-suffering investors will argue otherwise but just look at the change in stock price over the last 18 years versus the change in tangible book value per share.

That creates excruciating pain for anyone who was long, but an opportunity for those betting on even mediocre outcomes. If you assume that Laurentian gets pretty much anything right and trades at CWB's multiple in 5 years, your returns look pretty spectacular.

You start off with the 7% dividend yield and your tangible book value expands to about $65 at the end of 5 years, even assuming very modest earnings. If Laurentian trades at 0.9X tangible book value, the stock price would more than double. That is an over 20% compounded return. The worst case here is likely to be the bank continues to deliver poor returns and valuation (price to tangible book) remains right around here. Even in that case, you likely make 10% a year from dividends and a slightly higher stock price.

Verdict

We bought a little and are ready to punt on the bank, delivering a modicum of efficiency. The new CEO has his work cut out for him, but the sentiment and valuation offer a good chance to deliver from here. For those wanting a more conservative betting mechanism, we would suggest you look at Laurentian Bank of Canada PFD SHS SER 13 ( LB.PR.H:CA ). Those preferred shares yield 7.15% and reset by June 1, 2024 at a Government of Canada 5-year bond yield plus 2.55%. With the GOC-5 at 3.2%, we are looking at a reset of 5.75% on par, and that works to almost 10% on the current price of $14.40. We expect the GOC-5 to rise into this timeframe, and hence the reset could prove to be even better.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Laurentian Bank: Preferreds Offer An Interesting Setup Into Reset