CRM - Lessons From The Australian Mining Boom For Technology Investors

Summary

- Technology's strong growth over the last decade, and sudden collapse, are reminiscent of the Australian mining boom.

- There are several lessons to be learned from the Australian mining boom and bust, which can provide a helpful framework for technology investors.

- Profitability and efficiency across the technology sector will increase, which creates an attractive opportunity to invest in market-leading technology businesses with a long runway for growth.

Editor's note: Seeking Alpha is proud to welcome Fuji Kapital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

The technology sector has seen tremendous growth over the last few years. However, recently markets have gone from an extended period of techmania to suddenly experiencing a severe bout of techphobia . As a result, a lot of capital has fled the sector with many tech stocks down 60% to 90% from their (inflated) peaks. The unprofitable or low-margin technology businesses have been hit the hardest, as investors sold companies that were burning cash and perceived as speculative or marginal.

This strong period of growth and ensuing collapse in the sector is reminiscent of the Australian mining boom, which can serve as a helpful case study for investors. I'll share some observations from the Australian mining boom and some of the lessons that can be learnt from the period.

The Australian mining boom (2004-2014)

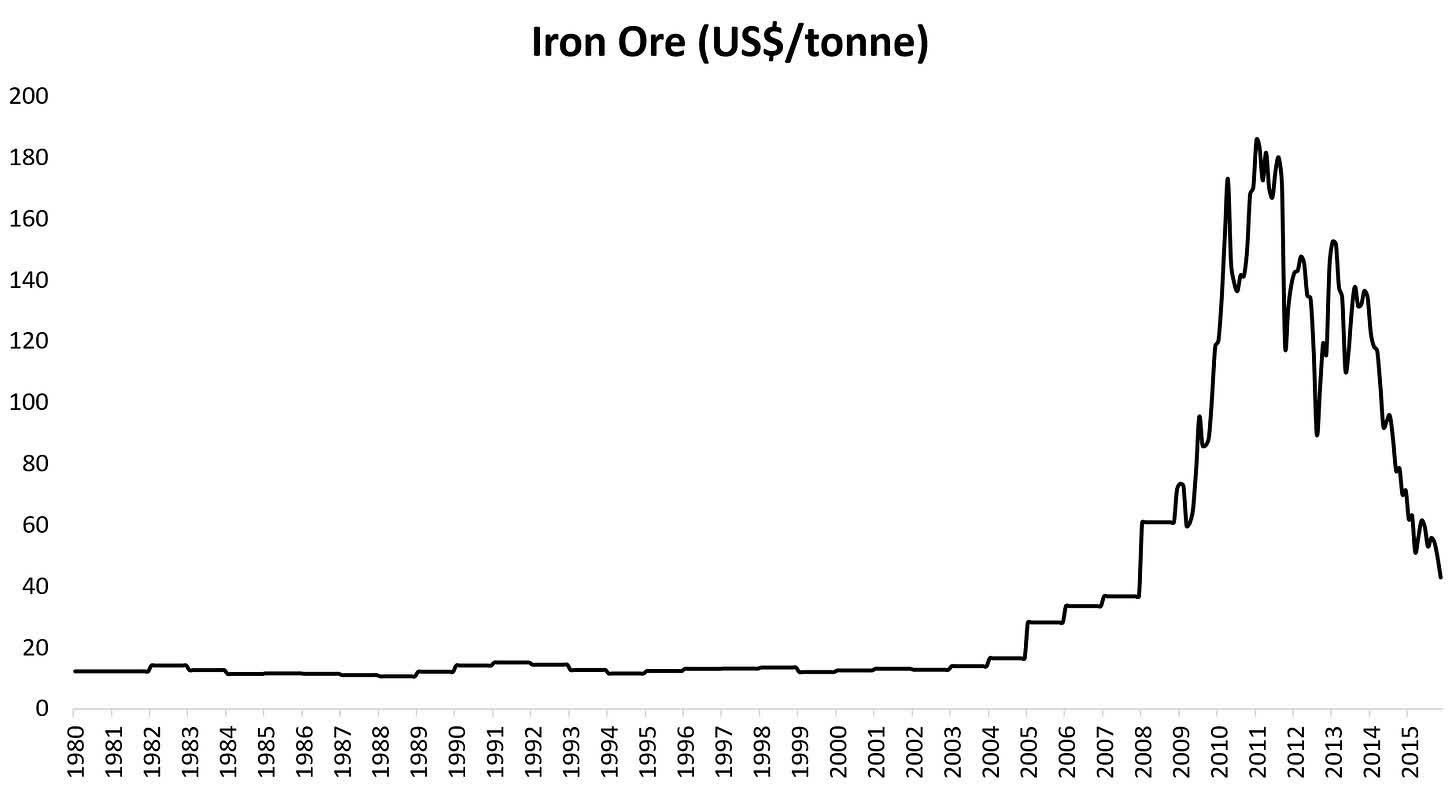

Iron ore was a boring commodity after the 1970s mining boom. It wasn't keeping up with inflation and its price remained consistently below US$20/t. This all changed in 2004 when demand from China and other emerging economies drove up the price of commodities like iron ore and coal. Over a period of 8 years the iron ore price increased 13x off its pre-boom levels. It was an extraordinary time to be in the iron ore business - everyone was making money - all you had to do was shovel dirt onto a ship and you would get $180-200 per tonne.

{kind=link}

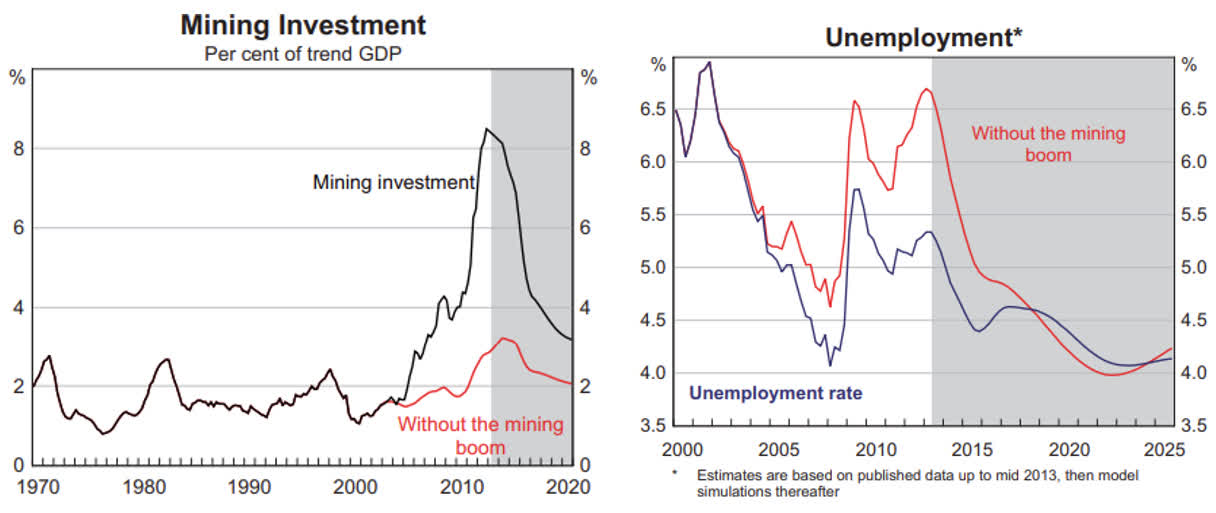

The boom in commodity prices resulted in a flood of capital to the mining sector as companies rushed to increase production in order to meet this newfound demand. Plenty of marginal/moonshot projects became economic and secured funding. According to the Reserve Bank of Australia ((RBA)), investment spending by the mining sector increased from 2% of GDP to 8% of GDP during the boom. There was also an increased demand for labor, leading to a tight labor market. The RBA estimates that the boom lowered Australia's unemployment rate by 1.25 percentage points, significantly softening the impact of the GFC on Australia's economy.

{kind=link}

The mining boom was an incredible period for Australia and mining companies. A key feature of the mining boom was the significant expansion in the cost bases of companies . During the boom times, cost bases expanded across the board as companies competed for talent and spent aggressively on growth initiatives. Efficiency took a back seat.

Fortescue Metals Group (FSUMF) presents a good case study on "bull market costs" and how organizations can get fat during the good times. It also presents a good framework on the amount of cost savings that can be extracted once management are incentivized to identify efficiencies, which results in a permanent increase in profitability.

Fortescue Metals Group - the new force in iron ore

Fortescue was a fast-growing iron ore miner that quickly became the fourth-largest producer of iron ore. They also had a pretty inflated cost base, with their cost per tonne one of the highest out of the major iron ore producers.

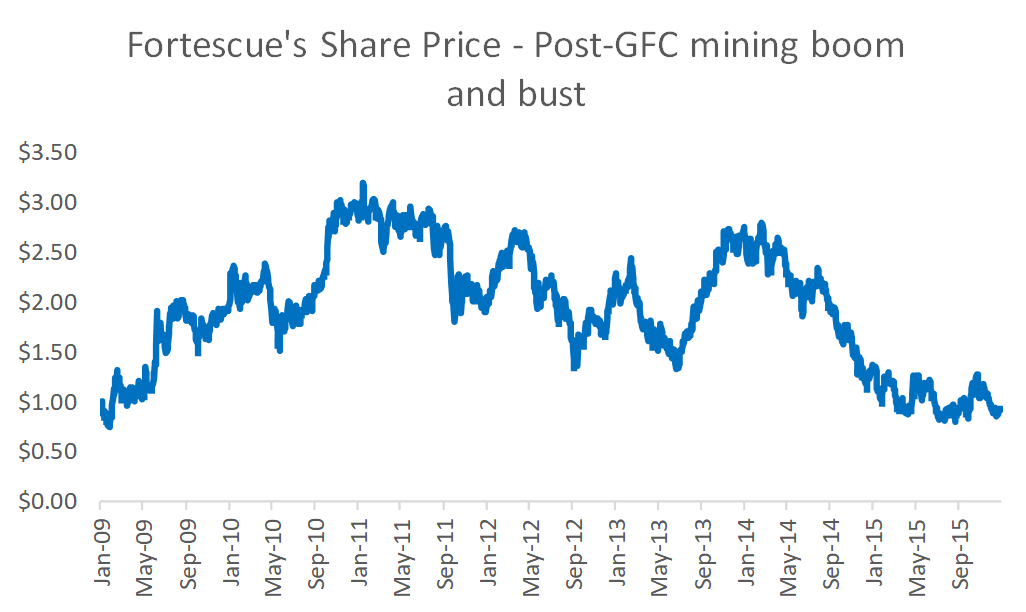

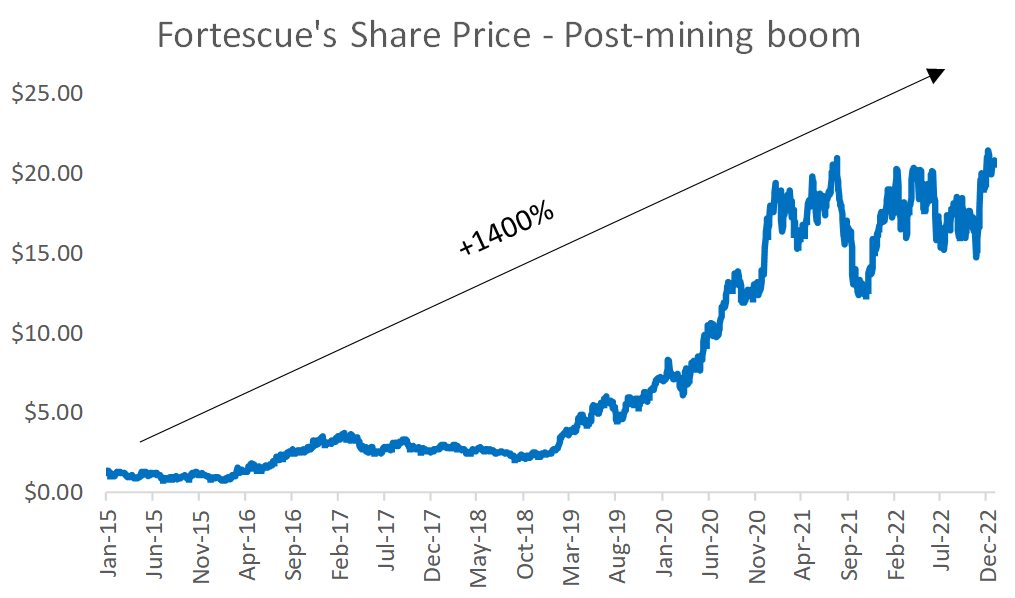

While the market was hot and commodity prices remained elevated, Fortescue's inflated cost base (and large debt balance) was not a major concern. Over this period, Fortescue's share price increased 3.6x off its 2009 levels.

{kind=link}

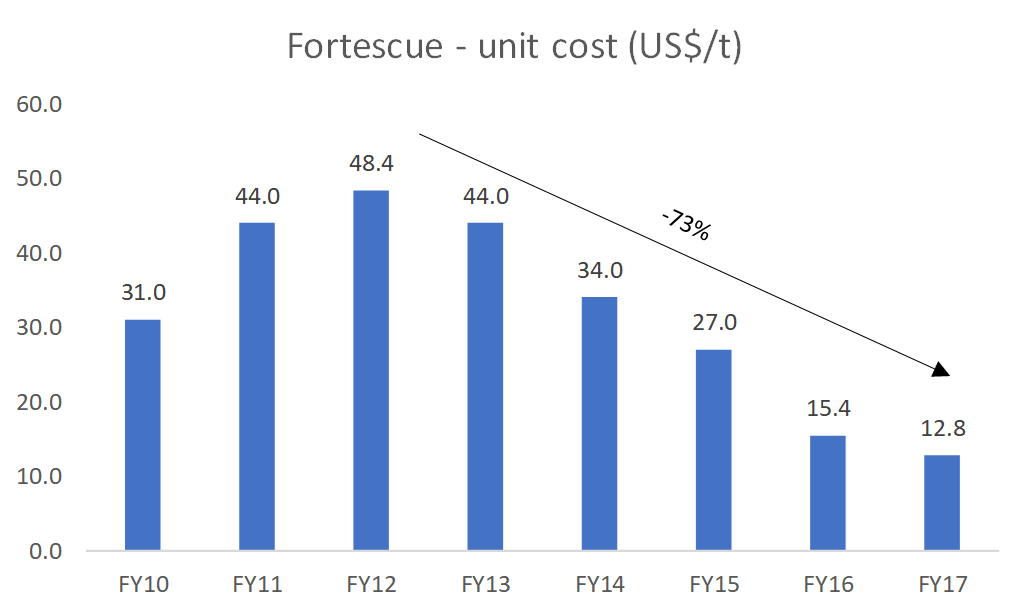

However, as soon as the iron ore price started to fall in 2014, Fortescue came under huge pressure and its share price declined by more than 70%. Some were even speculating whether the business would go into administration. It was during this period when Fortescue's management rolled up their sleeves and went to work on their cost base. As a result, Fortescue were able to reduce their cash costs from US$48/t to US$13/t .

{kind=link}

The collapse in the iron ore price caused Fortescue to forensically look at their cost base - something they never had to do before. The fact that a fixed unit cost, process intensive business was able to identify permanent unit cost savings of ~70% is incredible, and it's a great reminder of how easy it is for organizations to get fat during the good times.

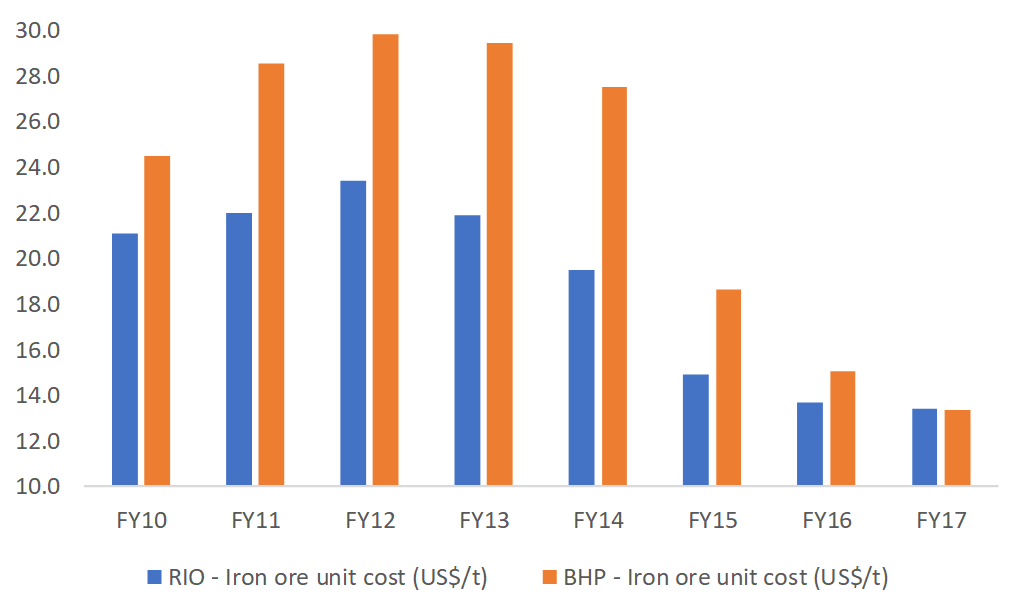

It's worth noting that it wasn't just the high-growth, marginal producers like Fortescue that got fat during the boom periods. Even the well-oiled major producers were forced to realize tremendous cost savings. Over the same period, Rio Tinto (RTPPF) and BHP Group (BHP) reduced their unit costs by 43% and 55%. This is further evidence that there were a lot of cyclical "bull market costs" floating around in the sector.

{kind=link}

The mining boom's parallels with the tech sector

Many of the dynamics that we saw during the mining boom are similar to what we've seen in the tech sector over the last few years.

Growth was the key driver of value

During the mining boom the whole industry was focused on growth.

"For about a decade, if you were in this industry, what was important was spending your investment quickly so you could get your production out as quickly as possible," Former BHP Chairman Jacques Nasser

This has also been the case in the technology sector. Anyone following the sector would be aware that growth has been the key measure to judge a technology company's performance, with less focus on efficiency or unit economics. (Note: I still believe organic growth is one of the most important qualities of any business; however, this has to come with attractive unit economics) .

Capital flooded the sector

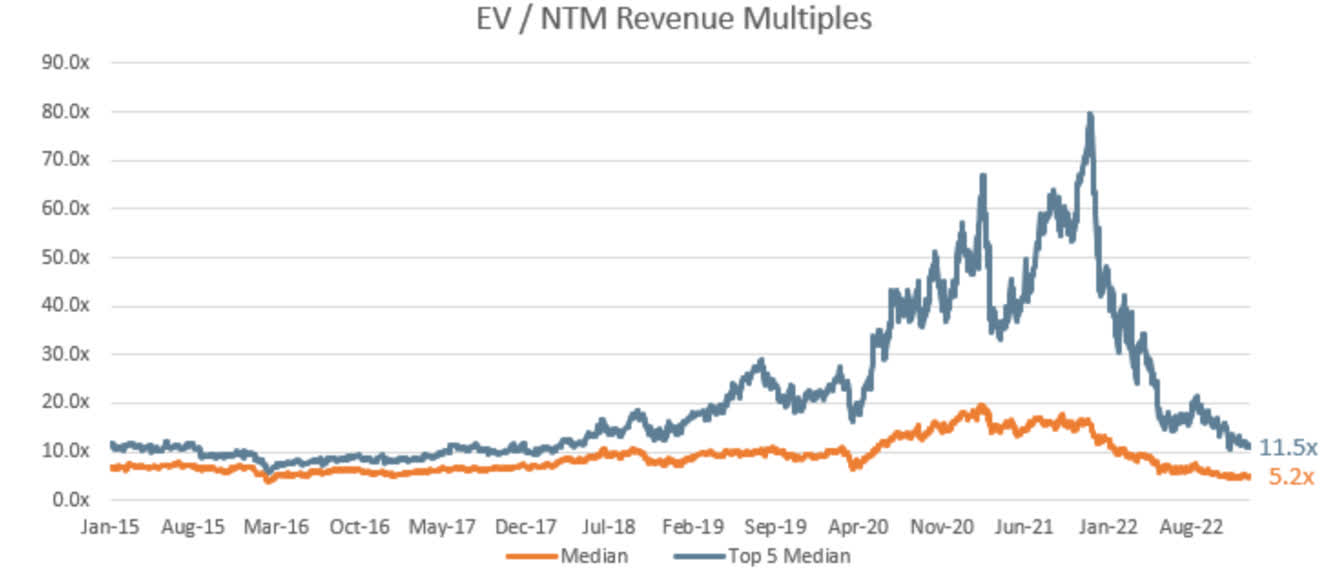

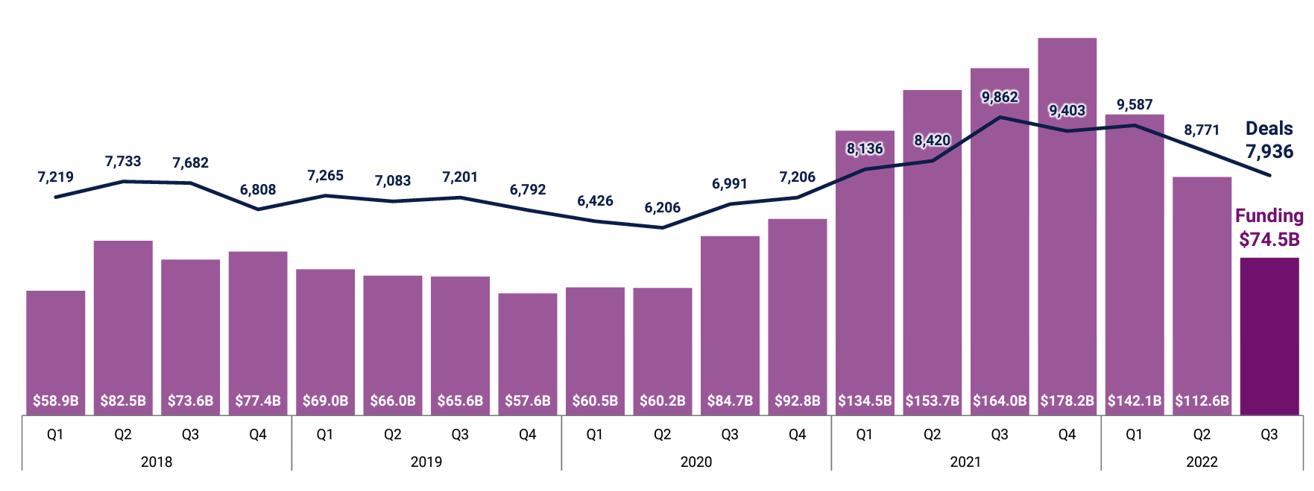

Technology valuations got pretty ridiculous in 2021, as the chart below shows. Several large hypergrowth SaaS companies were trading on EV / Sales multiples in excess of 70x whilst also burning cash. In private markets, deals and funding exploded from late 2020 and into 2021.

{kind=link}

{kind=link}

Moonshot projects securing significant funding

"It is another common feature of bull markets that as a mania progresses, the quality of stocks that attract speculation declines - a rising tide floats all ships, even the most unseaworthy" - Edward Chancellor. Devil Take the Hindmost .

During the mining boom, super marginal projects with high costs and in remote/risky regions attracted funding . This has also been the case in the technology sector. Meta's $10b binge on the metaverse is a perfect example of this dynamic. While I have an Oculus Quest and like the product, its use case is super niche and mass market adoption of this technology is still questionable. For the world's largest social media platform to bet 30-40% of its free cash flow on such an adjacent and moonshot endeavor is pretty extraordinary, and probably would not have happened in a non-boom environment.

Significant expansion in cost bases

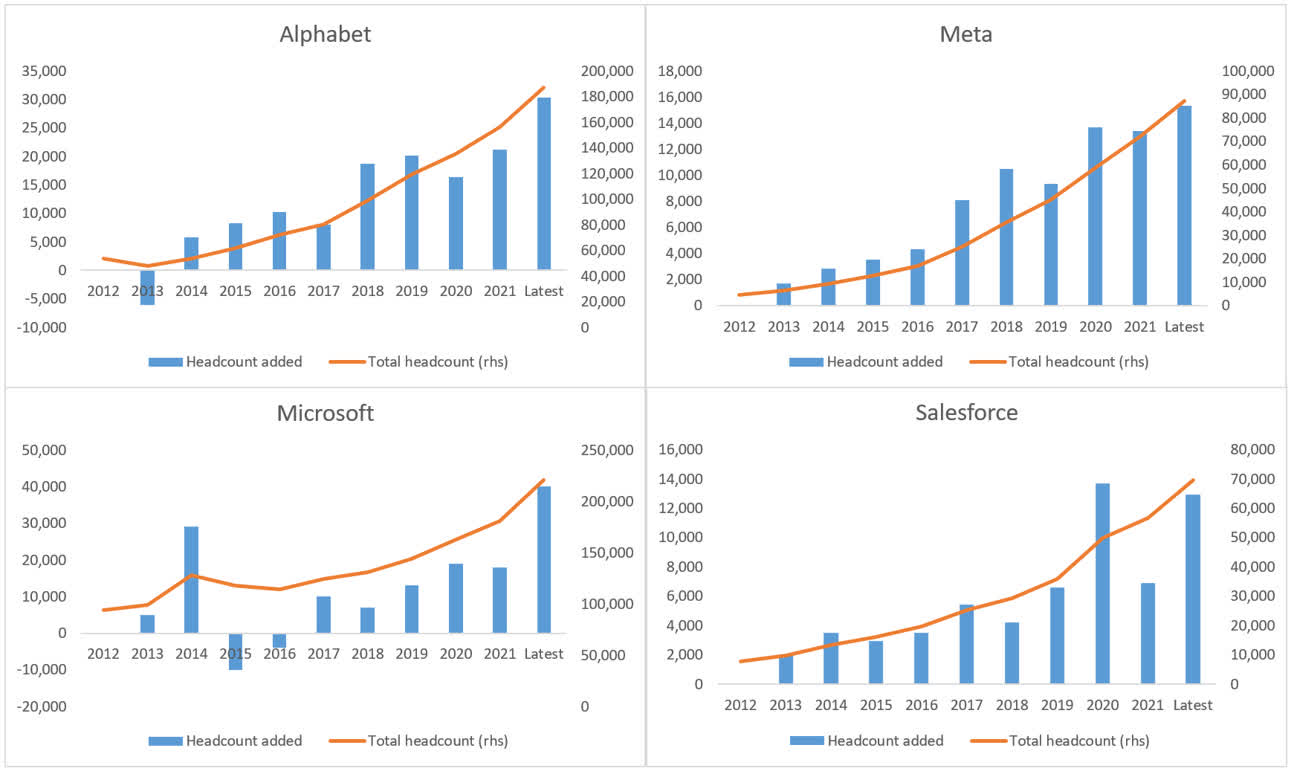

These charts below summarize the story. Over the last few years the world's largest software and internet companies had increased headcount at record levels. If we focus on Alphabet and Meta: during COVID they both entered a period which could be described as almost perfect operating environments . The whole world was indoors and went online; most of the developed world received free money from governments; and every business needed to spend on Search (Google (GOOG)) and Social (Facebook (META) & Instagram) to reach those online customers. Did Alphabet and Meta really need to increase headcount at record levels in order to capture those COVID-boom advertising dollars? It is obvious that they didn't. During the boom times companies just get fat. It is easy to get complacent when things are going so well, and if you have high incremental gross margins!

{kind=link}

Anecdotally, there's plenty of evidence of excess in the start-up, small-tech and "web3" space as well. Coinbase was paying $1 million for engineers while their Chief Product Officer also secured a +$600 million payday after less than 2 years of joining!

The downturn will drive technology companies to discover efficiencies

Just like the Australian mining companies during the boom, many tech businesses have gotten fat over the last few years. Fundamentally, when you think of software it's still one of the best business models with zero/minimal incremental cost to serve, super scalable products and recurring revenue. They should be extremely profitable . However, because most technology businesses have been focused on growth and reinvesting free cash flow in pursuit of more growth, the super high margin nature of technology business models has not always been evident .

The fall in commodity prices after the mining boom forced mining companies to discover significant efficiencies within their businesses. Similarly, this current downturn in technology valuations will force technology companies to identify efficiencies within their businesses, which should lead to a significant improvement in profitability across the technology sector.

So, what are the key takeaways?

Drawing on some of the learnings from the Australian mining boom, there are a few lessons that can provide some insights into how the next few years will play out.

Lesson #1 - Organizations get fat during the good times

Do not underestimate the amount of fat that gets built up within organizations during the boom times. Fortescue was a perfect example of this dynamic and the market was clearly ignorant to the quantum of "bull market costs" that were floating around in the business. In the technology sector, we've also seen an extraordinary period of growth in businesses cost bases. There has been a lot of bull market spend - remember those viral " day in the life " TikToks from tech employees? You can be certain that there ain't going to be many eucalyptus towels handed out in 2023!

We are entering a period where technology businesses will "shed their bull market fat" or "do more with less". Unit economics across the space will improve and companies will operate more efficiently - showing the true high margin nature of technology business models.

Lesson #2 - The market mechanism works

The market forces companies to change. At the end of the mining boom it was the collapse in commodity markets that forced management to change their capital allocation policies and optimize cost bases. The market had created an environment that incentivized management teams to identify structural efficiencies within their businesses.

In the tech sector, the collapse in valuations and rising cost of capital will force management to operate more efficiently. The market is the mechanism that rewards outcomes (i.e., be it outcomes related to growth, profitability and/or product) and those outcomes inform the incentives set for management. In an environment where the market permanently places a low value on revenue growth, management incentives will inevitably change to incorporate what the market wants.

"Show me the incentive, I'll show you the outcome"- Charlie Munger

And as I previously mentioned, a recurring revenue business model (i.e., don't have to acquire or dig for your revenue everyday) with +80-90% gross margins are the best models from which to extract efficiencies.

{kind=link}

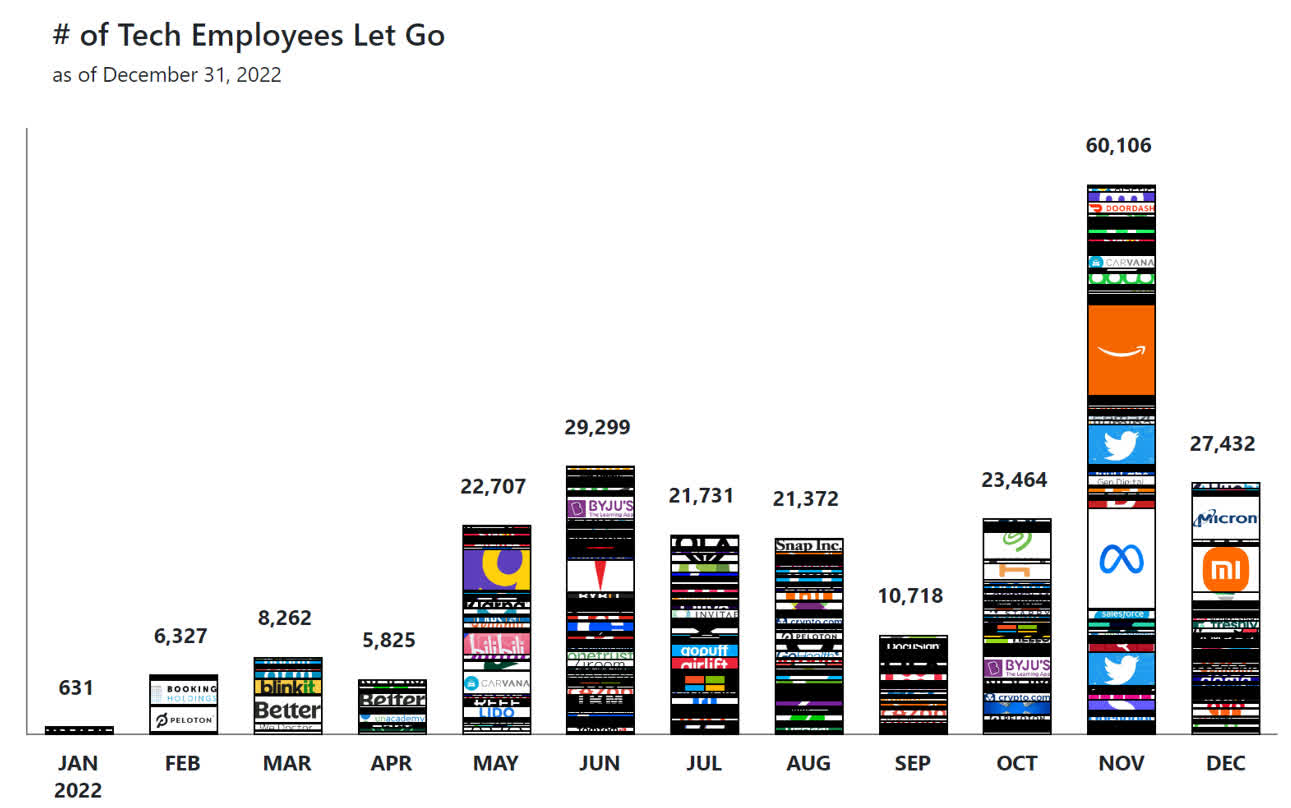

As shown in the chart above, the market mechanism has already forced a lot of unfortunate, but necessary layoffs within the sector. Even the extremely profitable businesses with no requirement for external capital are taking cues from the market (i.e., Meta cutting staff, Alphabet shutting moonshot projects like Stadia). (Note: I am not celebrating layoffs, they are painful for everyone involved) .

Lesson #3 - The recoveries can be violent

After the mining bust Fortescue was forced to structurally lower its cost base, which left it in a much stronger position to take advantage of any future increases in iron ore prices. In 2016 iron ore (surprisingly) entered another boom cycle, which - combined with Fortescue's structural improvement in unit costs - led to Fortescue's equity eventually increasing ~15x off its post-boom lows.

{kind=link}

Like Fortescue, I think the technology sector's recovery out of this downturn could be violent. I believe a permanent improvement in profitability across the technology sector plus the continued structural growth in the adoption of technology products will drive strong free cash flow generation across the sector, which will lead to higher share prices / valuations.

Furthermore, as we enter into a macroeconomic slowdown, growth will inevitably slow across the board (i.e., for all companies, not just technology companies). However, the product-led technology businesses that still have attractive structural elements to their adoption will continue to grow. Only now, these companies will be operating with a significantly improved cost base, which should allow more of this incremental revenue growth to drop through to free cash flow. In my view, a business with structural growth combined with high incremental profitability presents an attractive proposition for any investor, especially in an environment where growth is scarce.

Final Thoughts

I think we are currently in a pretty exciting period for technology investors. We have the opportunity to invest in generational growth stories at pretty attractive valuations. While many of these businesses might not show much profitability today, I think the key question investors need ask is: are these businesses structurally unprofitable or just fat?

In the same way that Fortescue - the beaten down, fat , marginal iron ore producer - delivered significant returns once it rationalized its cost base, technology companies that fix their costs bases and still maintain structural adoption dynamics will deliver significant returns to investors.

While the macroeconomic picture will get shaky, the structural trends that have been underpinning the growth of technology are still underway (i.e., companies are still digitizing workflows, adoption of the cloud is still increasing, cybersecurity is still a huge area of growth). An economic slowdown doesn't stop or reverse the structural adoption of technology - it may slow the adoption, but the end state does not change. In my view, this current market has created a great opportunity to invest in market leading technology companies that still have a long runway for growth.

For further details see:

Lessons From The Australian Mining Boom For Technology Investors