CA - Levi Strauss & Co: What To Watch Out For When Management Reports Q3 Earnings

2023-10-03 08:00:00 ET

Summary

- Analysts have low expectations for Levi Strauss & Co.'s financial results for the third quarter, with a predicted increase in sales but a significant drop in earnings per share.

- Management has revised down their expectations for the company's performance for the year, leading to pessimism among investors.

- Levi Strauss' second-quarter results were negatively impacted by a decline in revenue and an increase in selling, general, and administrative costs, but management attributes this mostly to one-time events.

- Shares don't look all that appealing at forward pricing, but when this pain passes, LEVI shares should be attractively priced.

In the next couple of days, the management team at apparel company Levi Strauss & Co. ( LEVI ) is expected to announce financial results covering the third quarter of the company's 2023 fiscal year. Earlier this year, management reduced guidance , both on the top and bottom lines, for the year as a whole. And in the second quarter specifically, the company faced some significant challenges. Because of this, market participants will likely use the third quarter as a litmus test to see the extent to which management's guidance can be trusted from this point on. On a forward basis, the new guidance makes the stock not exactly the cheapest. But with the problems the company is facing representing more of a blip on the radar than a paradigm shift, I believe that the long-term outlook for the company is still positive enough to warrant a degree of optimism.

Analysts have low expectations of Levi Strauss' Q3 Results

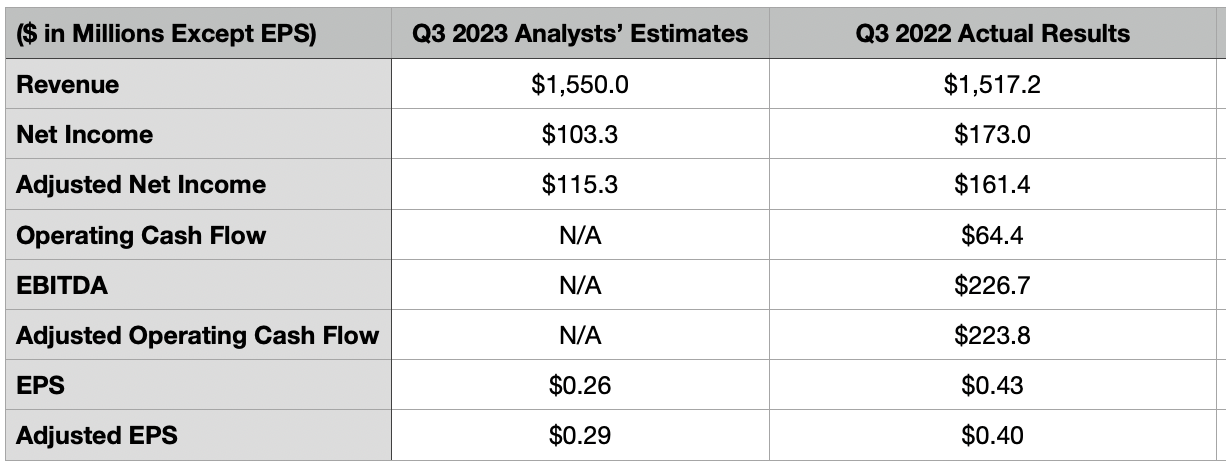

After the market closes on October 5th, the management team at Levi Strauss will be releasing financial results covering the third quarter of the company's 2023 fiscal year. Right now, analysts are not exactly optimistic about the company and its prospects. The expectation for revenue is actually quite positive, with sales forecasted to be $1.55 billion. If this comes to fruition, it would translate to an increase of 2.2% compared to the $1.52 billion the company reported in the third quarter of 2022.

{kind=link}

The bottom line, however, is a different story entirely. At present, analysts anticipate earnings per share of $0.26, with adjusted earnings per share coming in at $0.29. Should this come to fruition, it would translate to a material drop compared to the $0.43 per share in earnings the company reported last year and the $0.40 per share we generated on an adjusted basis. Put another way, analysts believe that net income will fall from $173 million last year to $103.3 million this year, while adjusted profits will fall from $161.4 million to $115.3 million. No guidance has been given when it came to other profitability metrics. But for context, operating cash flow in the third quarter of last year was $64.4 million. If we adjust for changes in working capital, it is substantially higher at $223.8 million. Meanwhile, EBITDA for the enterprise totaled $226.7 million.

A great deal of pessimism centered around the company likely comes from the fact that management has revised lower their expectations for how the company should perform for this year as a whole. Prior guidance called for revenue to grow by between 1.5% and 3% year over year. The upper end of that range has now been pushed down to 2.5%. That on its own is not a big deal. But what is a big deal is the fact that the profit per share guidance has been slashed from between $1.30 and $1.40 to between $1.10 and $1.20. Last year, earnings per share totaled $1.50. So we are looking at a rather sizable decline compared to 2022.

{kind=link}

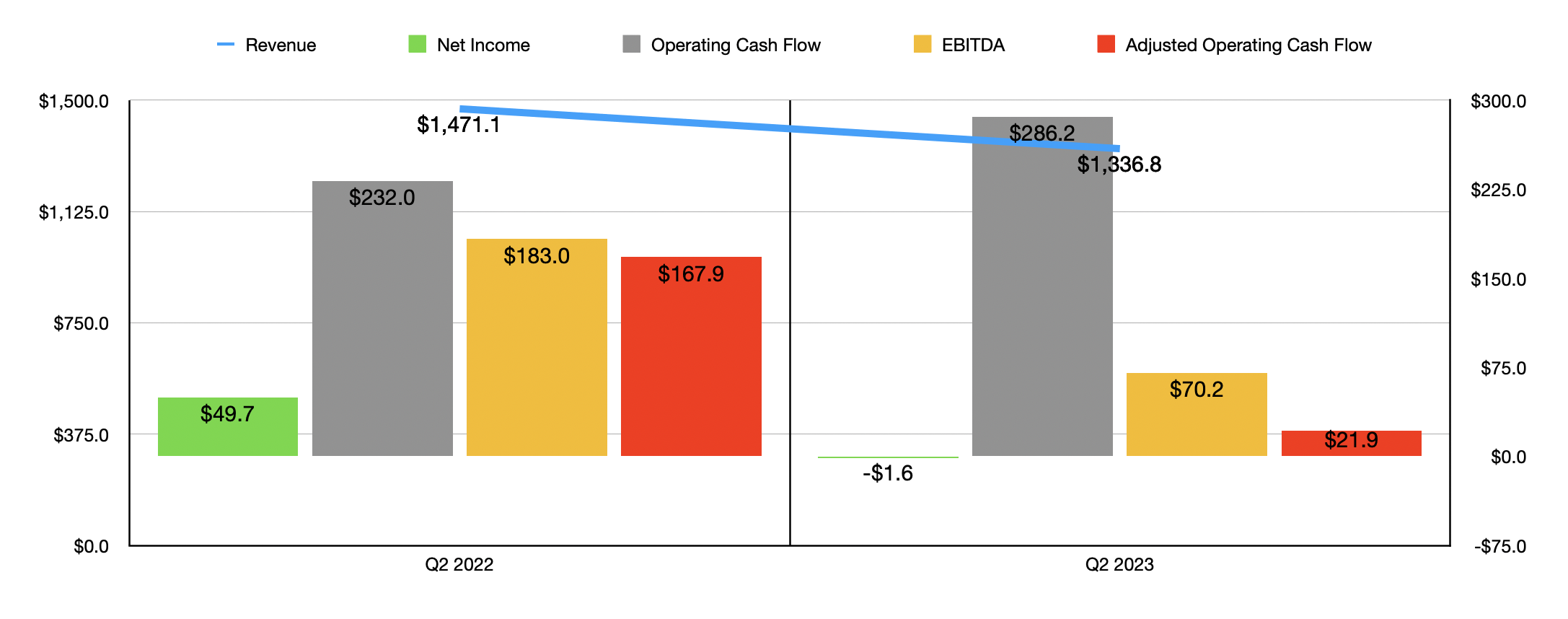

This downgrade for the company came after management reported a rather painful second quarter this year. Revenue for that time totaled $1.34 billion. That's a whopping 9.1% drop compared to what the company saw in the second quarter of the 2022 fiscal year. It may seem odd at first glance to expect the third quarter to be so radically different than the second quarter was. But according to management, the decline in the second quarter was truly a one-time event. You see, while the company did claim that US wholesale revenue was down year over year because of softened demand, the largest reason for the weakness involved a change in timing of wholesale shipments thanks to the company's new ERP system being implemented. At the same time that this weakness occurred, the company noted growth in both its direct to consumer and international operations.

The drop in sales brought with it a significant decline in profits. Net income plunged from $49.7 million to negative $1.6 million. Obviously, the decline in revenue played a role in this. However, the company also suffered from a surge in its selling, general, and administrative costs from 52.9% of sales to 57.9%. That increase was thanks to a combination of factors that included higher costs because of the increase in sales of its direct-to-consumer operations, higher labor costs, and foreign currency fluctuations. Increased spending on media, aimed at promoting the company's 150th anniversary of its 501 jean, was also a factor.

{kind=link}

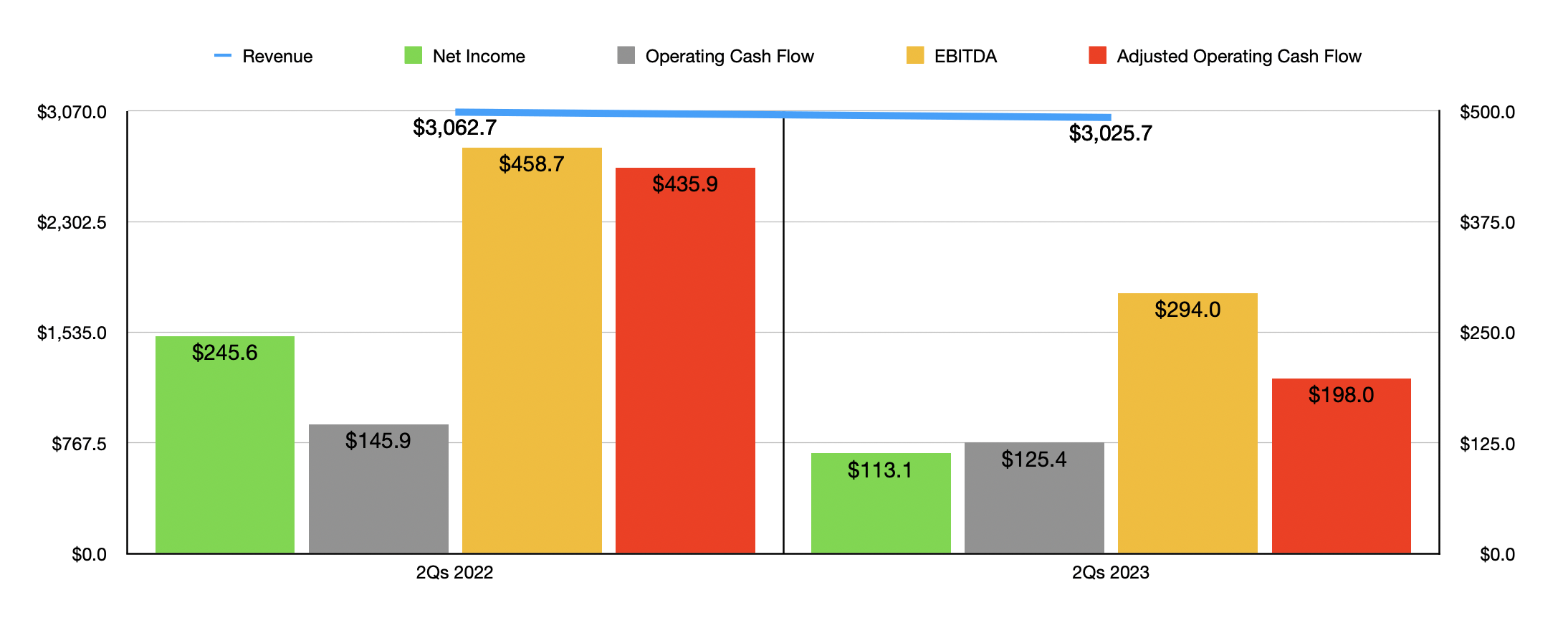

Other profitability metrics largely followed suit. Operating cash flow did increase from $232 million to $286.2 million. But if we adjust for changes in working capital, we get a decline from $167.9 million to $21.9 million. Meanwhile, EBITDA for the enterprise fell from $183 million to $70.2 million. As you can see in the chart above, financial results for the first half of the year as a whole were not as bad as the second quarter on its own. There definitely was a decline in some areas. But what this supports is the idea that the second quarter was just particularly painful for the company.

{kind=link}

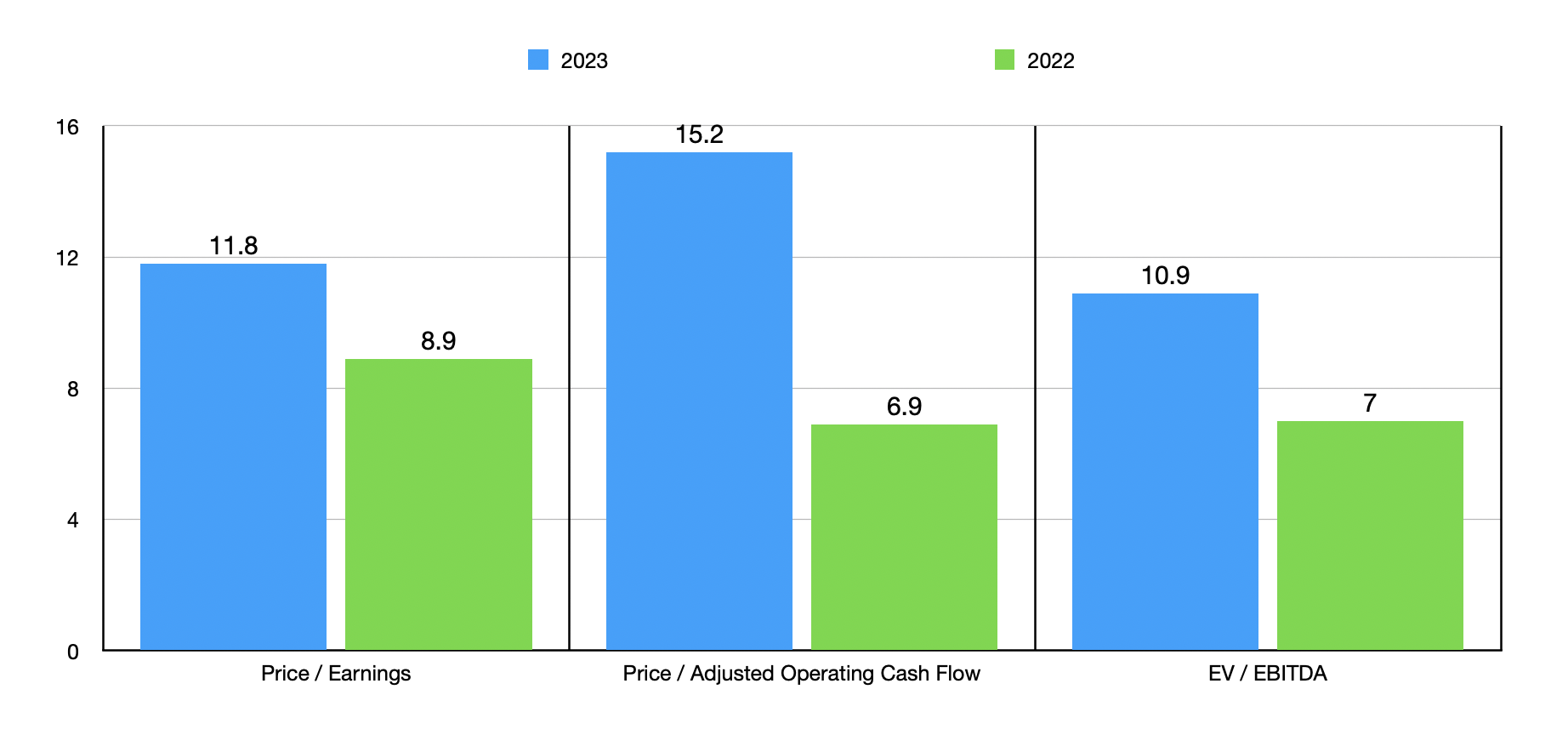

Leading up to the firm's earnings release, it would be wise to pay close attention to the aforementioned revenue and profitability metrics for the company. After all, these, combined with guidance, will go a long way toward determining how the stock performs over the next few months. If we were to assume that recent market conditions represent a new paradigm shift, the stock does not look particularly appealing. Using estimates for both adjusted operating cash flow and EBITDA, as well as management's forecast for adjusted profits, I was able to price the company as shown in the chart above. The stock does get noticeably more expensive on a forward basis than if we were to use data from 2022. In the table below, meanwhile, I compared the firm to five similar enterprises. Using both the price to earnings approach and the price to operating cash flow approach, I found that three of the five companies ended up being cheaper than our target. And when it comes to the EV to EBITDA multiple, that number increases to four.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Levi Strauss |

| 11.8 |

| 15.2 |

| 10.9 |

| G-III Apparel Group ( GIII ) |

| 4.5 |

| 5.4 |

| 6.1 |

| Capri Holdings ( CPRI ) |

| 15.1 |

| 9.9 |

| 9.1 |

| Gildan Activewear ( GIL ) |

| 10.2 |

| 19.4 |

| 8.8 |

| Delta Apparel ( DLA ) |

| 6.3 |

| 11.3 |

| 37.9 |

| Kontoor Brands ( KTB ) |

| 12.1 |

| 25.9 |

| 9.1 |

Takeaway

Heading into earnings, investors don't really have much of a reason to be optimistic. Management has already decreased guidance once and the second quarter was particularly painful. On the other hand, pain caused by some weakness on the wholesale front should be considered temporary, while the ERP issue is most certainly a one-time event. This gives me a reason to believe that, while we may see some weakness on the bottom line as analysts are forecasting, the long-term outlook for the company should still be positive. And if we assume that financial performance will eventually revert back to what it was in 2022, which I do not think is an unreasonable assumption, then the stock looks very appealing. Based on these factors, I've decided to keep the company rated a 'buy' even though shares have fallen 4.9% since I last wrote about the company compared to the 3.5% decline seen by the S&P 500.

For further details see:

Levi Strauss & Co: What To Watch Out For When Management Reports Q3 Earnings