LEV - Lion Electric: High Risk But Attractive Price Level

2023-07-17 10:46:29 ET

Summary

- LEV is facing challenges due to global supply chain issues and inflationary pressures, impacting its profitability and liquidity.

- Still strong secular EV tailwinds, particularly in North America, supported by government policies promoting lower carbon transportation options.

- At $2.1 per share today, the price level is attractive. I rate the stock a buy.

Lion Electric ( LEV ) is a Canadian-based manufacturer of electric commercial vehicles, primarily known for its production of electric buses and trucks. The company was founded in 2008 by Marc Bédard and is headquartered in Saint-Jérôme, Quebec, Canada.

LEV went public in 2020 and traded at around ~$9.7 on the opening day. The stock would then reach an all-time high of ~$33, though it has gradually declined since then. YTD alone, it has mostly been trading sideways within the $2 range.

I give LEV an overweight rating. Despite the high risk, there seems to be an interesting speculative buy opportunity today. My target price model suggests that LEV may see a ~27% upside in FY 2023.

Risk

LEV remains a high-risk opportunity. The continuing global supply chain issues and inflationary environment have been creating challenges for LEV since 2021 when it went public.

{kind=link}

Despite revenue more than doubling for two consecutive years in 2021 and 2022, gross and operating losses have significantly widened. Gross margin was -10% in 2022, and though the figure improved to -4% in Q1, operating loss continued to increase quite meaningfully in Q1 as selling and administrative expenses rose by 9% and 18% consecutively.

LEV is also exposed to cyclical risk as an EV manufacturer focusing on a niche electric school bus market. As suggested by its annual report , LEV's sales are mainly driven by electric school buses, where the buying decision is affected by the school calendar. During COVID-19 in 2020, for instance, the temporary closure of schools caused LEV's revenue to decline by ~24%.

All of these challenges have suggested that LEV is a highly macro-sensitive business. It is unfortunate that the overall macro situation has probably not changed significantly since last year. Border States' report in June suggests that while the supply chain issues may soften in 2023, some lead time challenges persist in electrical utilities such as wiring devices, which are relevant EV components.

mining.com

However, the unfavorable battery cell price outlook poses a more pressing risk. Batteries are the most expensive and most important component of an EV, and as seen in a recently-published article by mining.com , the average cell price rose for the first time in May, suggesting that we may not be seeing supply chain stability just yet in the near term.

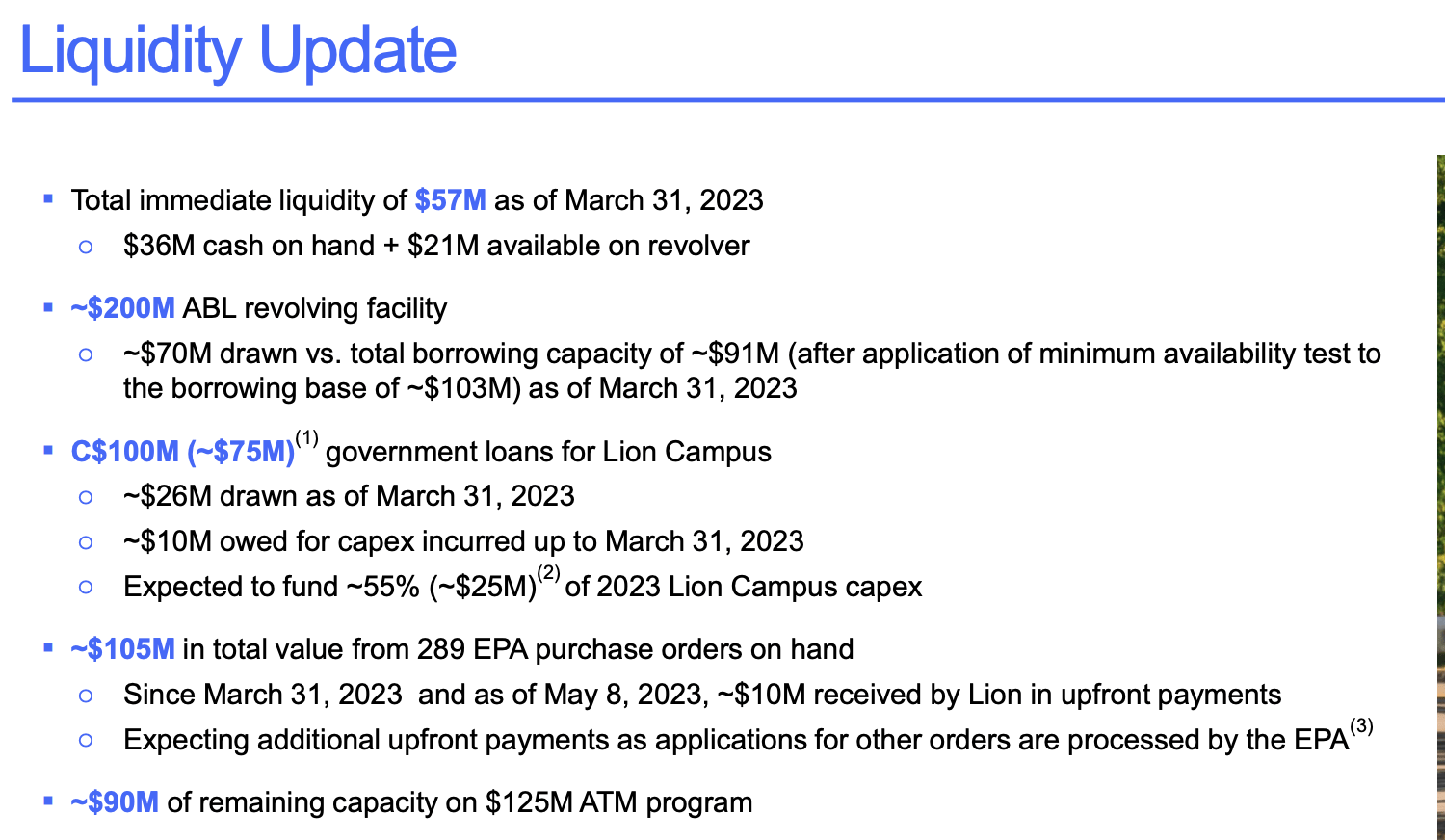

Finally, one of my bigger concerns about LEV today would be its liquidity. I have noticed how the challenging situations over the past few years may have impacted not only LEV's profitability but also its cash situation. Since LEV has not been a cash-flow-positive company, its cash position has been on a gradual decline since it went public.

{kind=link}

In just over two years, LEV's cash and cash equivalent/CCE went from over $360 million to $36 million, as of Q1 . Including the $21 million from the revolving facility, immediate liquidity stood at only $57 million in Q1. LEV has access to other sources of liquidity, though they also come at a price. LEV may continue to dilute shareholders, for instance, as it aims to secure additional up to $90 million of liquidity through its ATM program .

Catalyst

LEV will continue benefiting from the secular EV adoption tailwind globally, primarily in its core markets in North America. The demand outlook continues to be solid, due to the supporting government policies to boost the adoption of lower-carbon transport options.

{kind=link}

In the US, the EPA school bus electrification rebate program is just one of many possible growth opportunities for LEV. Under the EPA program , schools will be awarded up to 100% subsidies for purchasing electric buses. The total funding is $5 billion over 5 years, and LEV already participated in the first round of the program, securing 289 purchase orders worth $105 million. The figure alone represents at least a 75% increase from LEV's last year's annual revenue.

I expect more states and countries to launch similar programs in the future, opening up more opportunities for LEV to expand its market share in both Canada and US. I believe that LEV is in a good position to capture these opportunities as a leading player in the space. Capacity-wise, LEV today can deliver at least 220 vehicles per quarter, as opposed to just 40 two years ago.

However, it is important for LEV to serve these demands while maintaining a decent bottom line. One way to do this is by bringing BOM/Bill of Materials down across the value chain to improve production efficiencies and achieve economies of scale. I think that LEV may have the right idea to address that gap, as it already prepares a battery production facility with an annual capacity of 1.7 GWh. Longer term, I expect such vertical integration to lower battery and overhead costs, effectively improving LEV's profitability and cash flow generation.

Valuation/Pricing

My target price for LEV is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 target price model:

- Bull scenario (50% probability) assumptions - LEV to finish FY 2023 with ~$295 million of revenue, a ~111% growth YoY, the midpoint of the market's estimate . I would expect LEV to maintain today's P/S of 2.7x as it completes the rest of the EPA order, collects more payment, and ramps up battery production successfully by year's end.

- Bear scenario (50% probability) assumptions - LEV to finish FY 2023 with ~$223.9 million of revenue, a ~60% growth YoY, missing the market's estimate by a meaningful margin. While 60% is a highly desirable growth rate for most companies, I believe that LEV will need to deliver higher growth to compensate for the weaker profitability and cash flow outlook and also given its positioning. I would expect LEV to see P/S contraction to 2x from 2.7x today.

Author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of ~$2.8 per share. Since LEV has been trading between $2-$2.2 most recently, my target price model suggests that there may be at least ~27% upside at year's end. Overall, I rate LEV a buy at the current level. However, given the high risk, I think that there are a few ways to look at the opportunity.

More conservative investors may want to reassess the opportunity at the end of FY 2023 when there is more clarity on LEV's overall situation. Alternatively, more bullish investors may buy the shares today, given the potential near-term price upside, strong secular tailwind, and LEV's strong market leadership. Finally, some opportunistic investors may see LEV as a speculative buy, considering the sideway price action since the beginning of the year where the stock has been trading between $1.7-$2.5 YTD. At $2.1 today, LEV is still trading closer to the bottom and seems like an interesting buy opportunity.

Conclusion

LEV is facing significant challenges due to global supply chain issues and inflationary pressures since going public in 2021. These factors have impacted LEV's profitability and liquidity, raising concerns about its financial situation. However, LEV is poised to benefit from the increasing global adoption of EVs, particularly in its core markets within North America. The demand for EVs has been strong, supported by government policies promoting lower-carbon transportation options. Despite the challenges, LEV's stock price is currently trading at a relatively low level of $2.1, presenting an intriguing buying opportunity. Taking into account the potential for growth in the EV market, I recommend considering LEV as a buy at its current valuation.

For further details see:

Lion Electric: High Risk, But Attractive Price Level