ACTV - Liquidity Is Staving Off The Bear

Summary

- Risk assets have performed admirably since October 2022.

- Since October, the Bank of Japan has been intervening in financial markets to support the yen and JGBs.

- $545 billion of Fed balance sheet reduction has been compensated by reductions of the Treasury General Account.

- Until the debt ceiling is raised, the TGA can inject liquidity for the next three months, over the Fed's $95B balance sheet reduction cap.

- Elevated liquidity could prop up equities for H1 2022.

It has been 140 days since the S&P 500 marked a new low. The market declined for 282 days into that low compared to the average bear market which is around 290 days. This could mean that the bear market in equities is over.

My macro and fundamentals view is that no, the bear market is not over. Over the past few months, financial conditions have loosened. This is contrary to the Fed's objectives. Clearly, liquidity in financial markets has improved, thus supporting risk assets. Whether these sources of liquidity are temporary or not will have a significant influence on equities and investor portfolios.

Central Bank of Japan Supporting the JGB

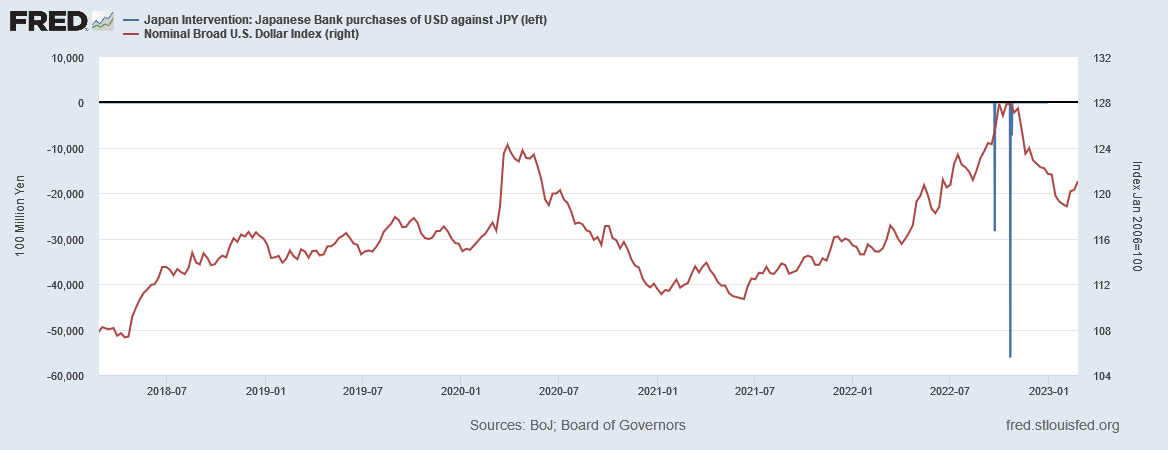

On September 22, 2022 the Bank of Japan intervened in the forex markets by selling USD and buying Yen to support the Japanese currency. Initially this seemed to slow the depreciation of the Yen against the USD. But on October 21, 2022 the BOJ intervened more than twice the size they did in September. This coincided with the U.S. dollar index putting in a top.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

In December 2022, the BOJ raised its JGB rate target from 25 basis points to 50. This caused the Yen to rally sharply against the USD. But since then the BOJ has had difficulty maintaining the rate cap. The BOJ has been buying upwards of 100% of some JGB issuance and lending a record amount of those bonds. Recently, the BOJ holdings of JGBs has increased to over 50% of total assets. This has led to a sharp increase in BOJ lending to banks to finance additional purchases of JGBs.

The Daily Shot (used with permission)

The result of this currency chaos is that the BOJ has sharply reversed its balance sheet reduction. The expansion of the BOJ balance sheet has been outpacing the reduction to the Fed's balance sheet since the start of the year. Below is the combination of the BOJ and Federal Reserve balance sheets (blue) compared to the S&P 500 (red). The combined balance sheet is nearly unchanged since, you guessed it, October.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

Household Balance Sheets Remain Elevated

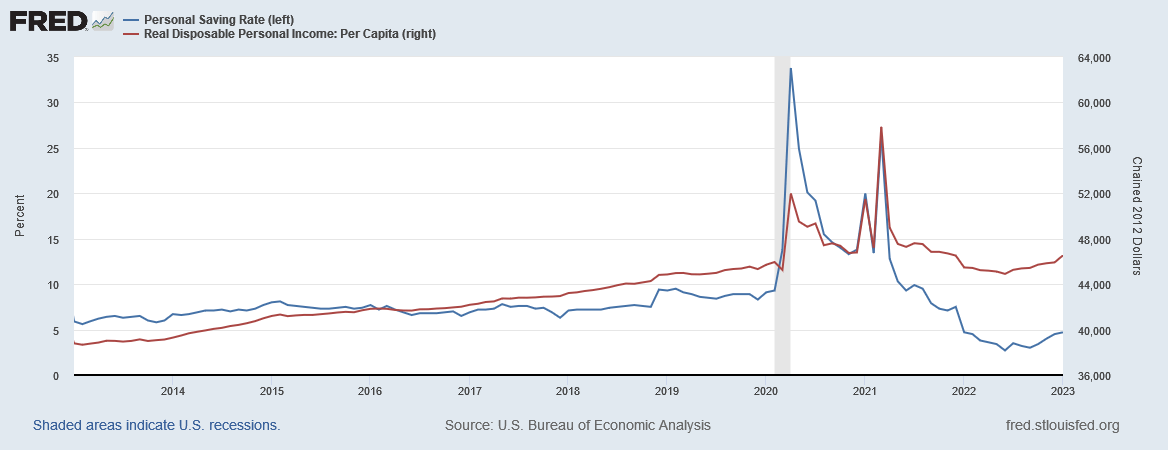

The fiscal stimulus of 2020-2021 has yet to abate in the sense of returning to pre-2020 trends. In those two years following the start of the pandemic the personal saving rate surged higher. Consumers were increasing savings as a result of several windfalls:

- Receiving money from PPP loans, stimulus checks, child tax credits.

- Deferring payments on rent, mortgages, and student loans.

- Reduced spending due to involuntary spending cuts, especially to travel and services.

The saving rate has since declined sharply from a peak of 33.8% in April 2020 to 4.7% in January 2023. The average saving rate before 2020 was 7-9%. The savings rate began to rise in September 2022 at 3%, likely a consequence of lower energy costs.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

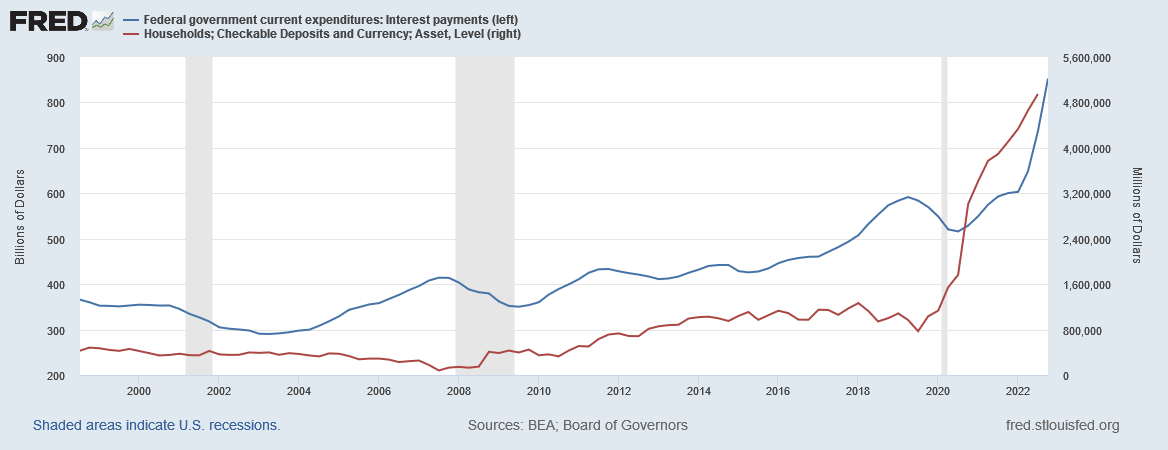

Although the saving rate has declined, the total checkable deposits held by U.S. households continued to rise through Q3 2022 nearly reaching $5 trillion. Simultaneously, the rise in short term interest rates by the Federal Reserve has resulted in a surge in interest payments, particularly those paid out to Treasury bonds and bills. Thus, U.S. households are receiving sizeable income on their large checkable deposits. Financial conditions for households, as an aggregate, are certainly loose. Note that these conditions apply mostly to upper income households.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

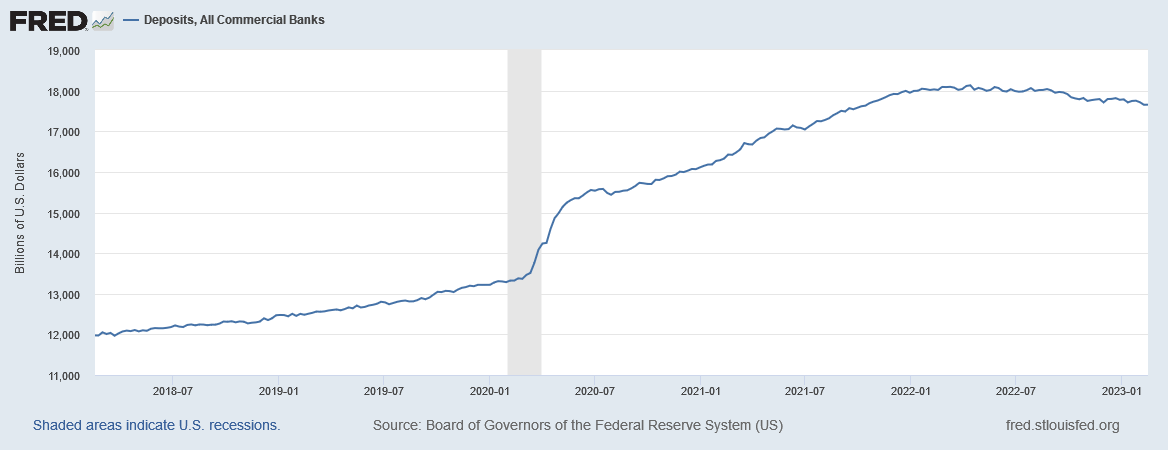

Overall, commercial bank deposits are lower year-over-year. This suggests that liquidity conditions have been tightening. I interpret this to mean that the underlying liquidity trend is in decline.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

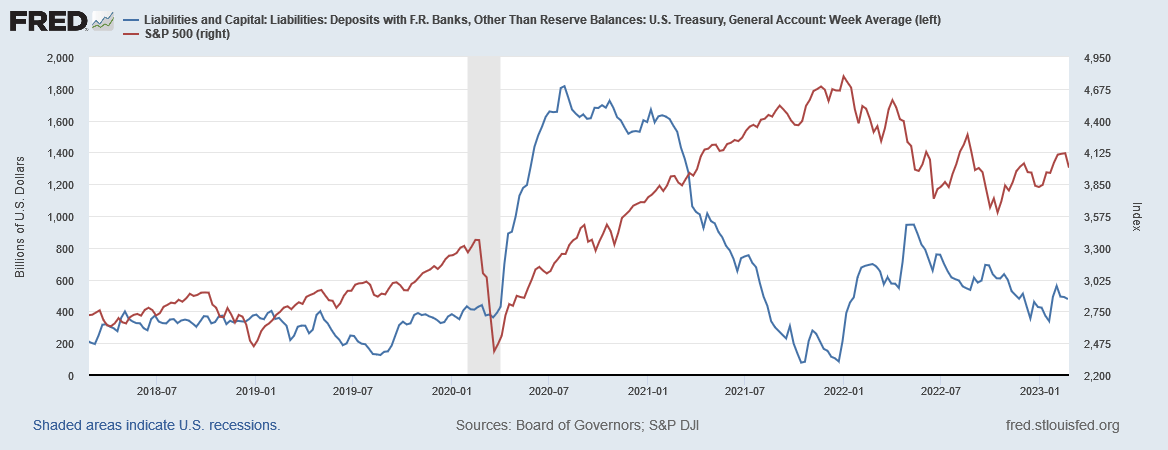

Treasury General Account and Debt Ceiling

The U.S. Federal Debt Ceiling is due to be raised in 2023. It is expected that until Congress passes a higher debt ceiling the U.S. Treasury will need to use funds from Treasury General Account (TGA) to fund the U.S. government without new issuance of debt. The TGA has about $350 billion and this is expected to last until June.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

Reductions in the TGA loosen financial conditions because the balance of the TGA is a liability on the Fed's balance sheet. When the federal government spends the funds from the TGA without new debt issuance, that money enters into the economy through entitlement programs, such as social security and Medicare, government salaries and other spending. The funds are deposited at banks which can then be used as collateral for lending.

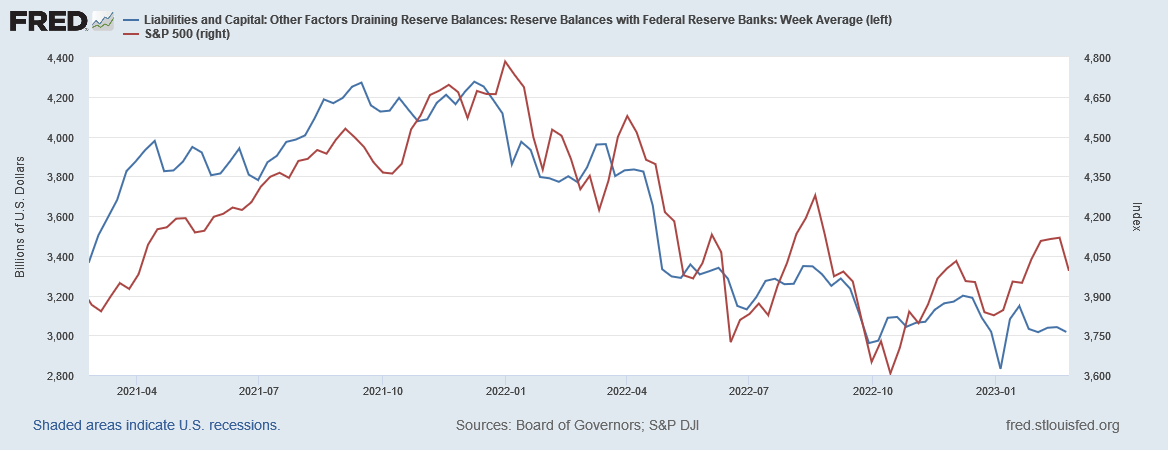

Since September, reserve balances with Federal Reserve Banks have been largely unchanged, supporting the notion that financial liquidity and financial conditions have been looser during this period. Equities may be stretched here relative to the liquidity level indicated by reserve bank balances, if it were not for other sources of liquidity.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

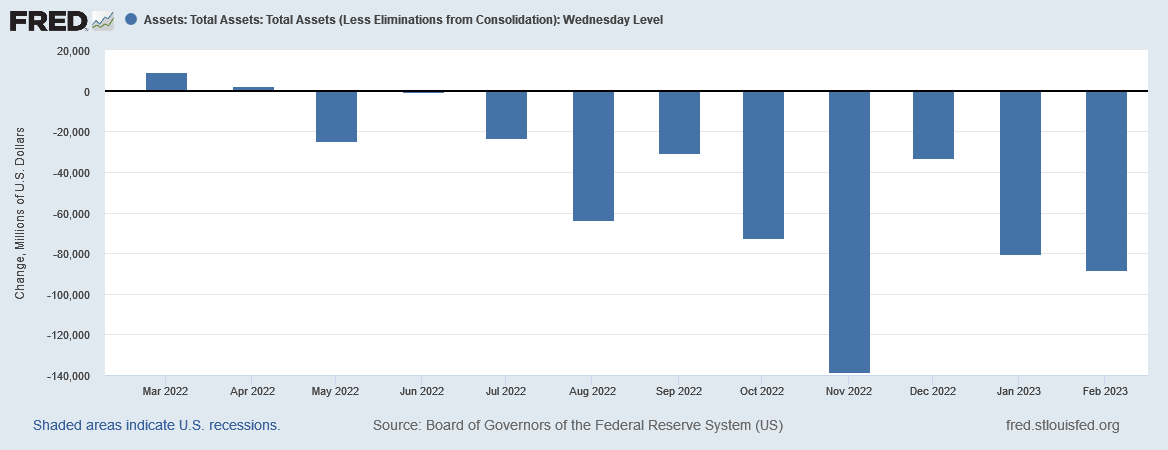

It would seem that this increase in liquidity is in contrast to higher interest rates set by the Federal Reserve in addition to the $545 billion runoff of the Fed's balance sheet over the last year. These policies should tighten financial conditions and reduce overall liquidity. Although inconsistent, the Fed has been successful in reducing its balance sheet each month since June 2022. However, they have not always been able to reach their monthly reduction cap of $95 billion . Since last May, the reduction in the TGA has closely compensated for the reduction of the Fed's balance sheet and this trend could easily continue for Q2 2023.

Federal Reserve Economic Data | FRED | St. Louis Fed

{kind=link}

Summary

Liquidity matters.

Financial markets, and certainly risk assets, are contingent upon the availability of financial liquidity. Something changed in October 2022 which resulted in a significant rally in risk assets. The U.S. dollar began its current decline in October, a sign of increased liquidity. The Bank of Japan intervened in currency markets in late 2022 to preserve the Yen. Now, they continue to expand their balance sheet to stabilize their bond market.

Liquidity provided by the BOJ and spending of the Treasury General Account has been more than offsetting the quantitative tightening of the Federal Reserve by reducing its balance sheet. This trend has the potential to continue for another quarter. At the same time, U.S. households continue to be cash-rich.

The Federal Reserve has more work to do if they want to tighten financial conditions and reduce liquidity. The outcome will decide if the current rally in equities is a new bull market or if the bear market resumes. In the meantime, I expect that equity markets could remain range-bound for the next few months as liquidity staves off the bear market and worsening economic conditions keep a lid on upside. To invest for these conditions, my portfolio is net neutral on equities and I am using strategies to hedge against a flat market including selling volatility and the JPMorgan Equity Premium Income ETF ( JEPI ).

For further details see:

Liquidity Is Staving Off The Bear