SPY - Littelfuse: Our Top Stock Idea For 2024

2023-12-07 06:14:30 ET

Summary

- Littelfuse has faced headwinds and underperformed the S&P 500 index this year but has a history of impressive growth and is expected to deliver above-average growth in the long term.

- The company has been impacted by a challenging macroeconomic environment, with declining revenue and a forecasted decline in growth for the fourth quarter.

- Despite these challenges, LFUS has reduced inventory, generated significant free cash flow, and is well-positioned in growing sectors such as alternative energy and transportation. It also has a diversified customer base and a history of successful M&A growth.

- The company is trading with a significant margin of safety to our fair value estimate.

Littelfuse ( LFUS ) continues facing headwinds, and this has reduced investor interest in the shares. In 2023 it has trailed the S&P 500 index ( SP500 ) ( SPY ) by more than 10%, which is not typical for Littelfuse. The company has a history of rapid growth through a combination of organic growth and M&A. Its sales have a 15-year CAGR of 11% and its earnings per share 17%. This is a very impressive record, and we believe the company can continue to deliver above-average growth for many more years.

The company has been facing a challenging macroeconomic environment, with channel de-stocking and pockets of end-market softness. As a result, last quarter's revenue was down 8% compared to the previous year. The company is guiding for growth to deteriorate even more in the fourth quarter, guiding for a year-over-year decline of roughly 13%.

On the positive side, the company has already reduced its inventory by $66 million so far this year, helping it generate more than $250 million in free cash flow year to date. It is also forecasting a return to growth during 2024.

We believe investors are missing the forest for the trees, given that Littelfuse has significant structural tailwinds that should keep it growing in the long term. It is seeing increasing content and share gains in industrial, transportation & electronics applications. In general, it is well positioned to serve long-term structural growth themes, with exposure to rapidly growing sectors such as alternative energy, energy storage, power conversion, eMobility, data center, and cloud.

Something else we believe investors are missing is that Littelfuse has very little customer concentration risk, given that it serves more than 100,000 unique customers. It is also unlikely to be replaced once it gets a design win, as many products using its components have long-term product life cycles, and it is expensive to re-design and go through validation and testing again. Littelfuse believes it can deliver between 5% and 7% in organic growth, with additional growth coming from strategic M&A. The company is seeing particularly strong growth in its transportation segment, with double-digit growth in passenger vehicles, where it has reached ~$7 in content per vehicle. Littelfuse is also benefiting from EVs and EV-charging infrastructure growth, where it has secured design wins for both low and high-voltage applications, including EV battery management systems and inverter applications. It reported seeing very strong growth in its medical business as well.

Littelfuse is diversified, with roughly a third of its revenue coming from each of its three segments: electronics, industrial, and transportation. The company is expanding geographically, increasingly targeting markets such as Japan, Korea, and India.

Financials

The graph below shows the impressive growth in sales and earnings per share that the company has delivered over the past 15 years. The company has passed some of the increased earnings to shareholders, with twelve years of growing dividends, which have increased with a 12% CAGR since inception.

Littelfuse Investor Presentation

The company suffers from some cyclicality, but the trend overall has been towards higher sales and earnings. To counteract this cyclicality, Littelfuse tries to maintain a flexible cost structure to help drive improved profitability through cycles.

M&A

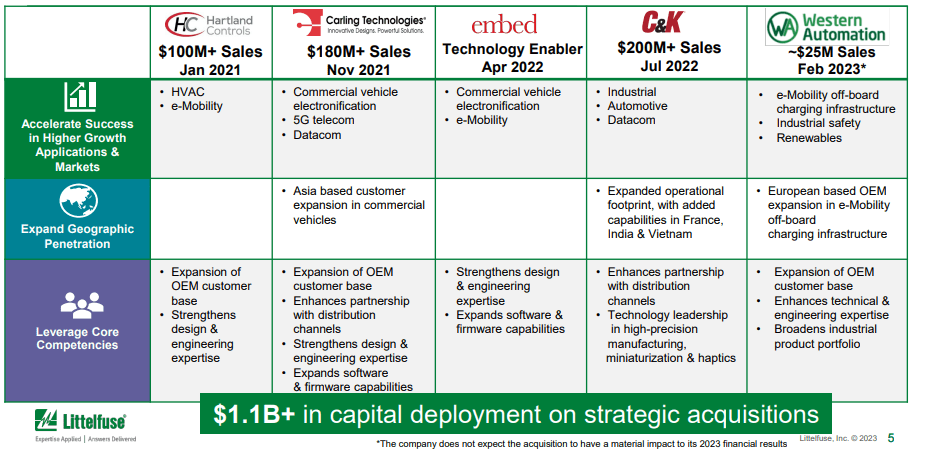

Littelfuse has a history of successful M&A growth, where they tend to do small to medium-sized acquisitions that benefit from Littelfuse's distribution network, or that leverage some other of its core competencies.

{kind=link}

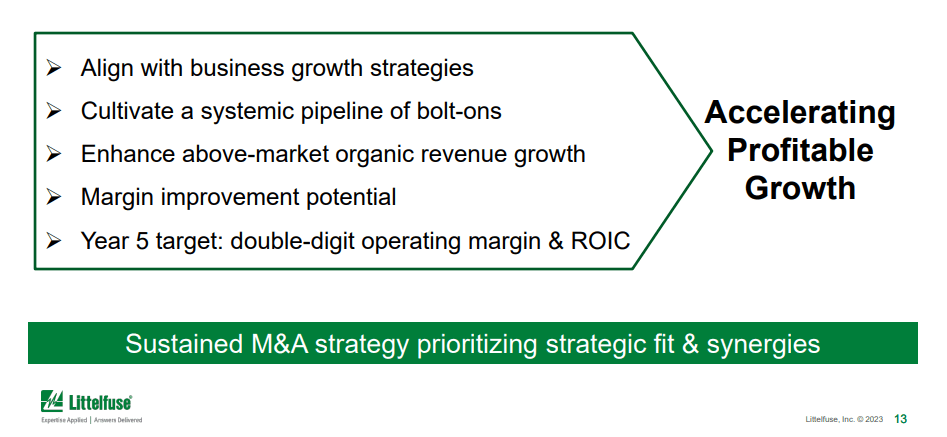

They have proven to be disciplined with their acquisitions, and look for opportunities that align with their business growth strategies. They tend to be bolt-on acquisitions with margin improvement potential, with a five-year target of reaching double-digit operation margin and ROIC. It is in part thanks to this M&A strategy that the company has been able to sustain double-digit sales growth for so long.

{kind=link}

Balance Sheet

While total long-term debt has been increasing, leverage remains quite manageable. At the end of last quarter, net debt to EBITDA stood at ~1.4x. The company has significant amounts of cash and short-term investments, providing ample capacity for organic and inorganic growth investments.

Outlook

Looking forward, the company expects inventory de-stocking to continue into next year. Once inventory levels stabilize, Littelfuse expects to return to normalized order rates and a return to growth during 2024.

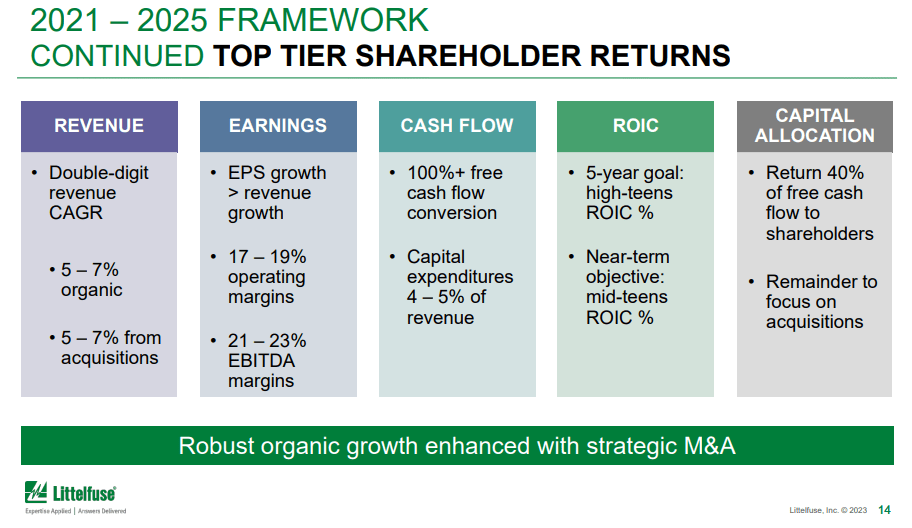

Its 2021-2025 investor framework guides for double-digit revenue growth, earnings growth above revenue growth, free cash flow conversion above earnings, ROIC in the high teens, and for the company to return ~40% of free cash flow to shareholders through dividends and buybacks, with the remainder used to help finance acquisitions.

{kind=link}

Investors and analysts are wondering when the current down cycle will end, with an analyst basically asking during the Q&A session of the most recent earnings call whether next quarter will mark the bottom in terms of margins for the business. Below we include what CFO Meenal Sethna replied.

So what I would say is, and we've talked in the past, for us, sales volume tends to be a pretty large driver for us in terms of margin profile as you look quarter-over-quarter, especially when you have near-term trends that are going on. So the case of the fourth quarter, as I mentioned in my prepared comments, with the sequential sales decline that we have, really the margin -- expected margin decline, and I'm not going to comment on the exact margin here. But the expected margin decline really is a function of that sales volume.

As I take a step back and think about our overall margin expectations for '23 compared to past cycles, we get reminded a lot of times of what life is like in '08, '09, where our margin profile was sub-10%. And even during the pandemic period, the 2019 cycle, that '19 to '20 period, our margins finished off at about 14.5% or so. And so our expectation is, with all the work that we've done in the past few years from an execution perspective, from a pricing perspective, portfolio diversification, I expect that we will finish better than that margin profile for 2023.

Valuation

We believe there are a few other companies that are indirectly benefiting from the shift towards electrification and electronification.

This can be through exposure to the renewable energy sector, EVs, smart buildings, etc. These include Rockwell Automation ( ROK ), ABB ( OTCPK:ABBNY ), Schneider Electric ( OTCPK:SBGSY ), and Nidec ( OTCPK:NJDCY ). We believe Littelfuse can grow faster than most of them, yet it is trading with the lowest EV/EBITDA ratio.

While the company expects to return to growth next year, analysts believe the recovery is a little further away. On average they see FY24 looking very similar to FY23, and growth returning until FY25. We think that unless the US economy enters a recession, it will probably be the company that is proven correct.

SeekingAlpha

Our estimate for the net present value of future earnings is roughly $300. With shares currently trading at ~$240, this implies a close to 20% margin of safety to fair value when using a 10% discount rate. Morningstar ( MORN ) seems to agree, with their analyst estimating fair value at $310.

| EPS |

| Discounted @ 10% |

| FY 24E |

| 11.79 |

| 10.72 |

| FY 25E |

| 15.05 |

| 12.44 |

| FY 26E |

| 16.71 |

| 12.55 |

| FY 27E |

| 18.54 |

| 12.67 |

| FY 28E |

| 20.58 |

| 12.78 |

| FY 29E |

| 22.85 |

| 12.90 |

| FY 30E |

| 25.36 |

| 13.01 |

| FY 31E |

| 28.15 |

| 13.13 |

| FY 32E |

| 31.25 |

| 13.25 |

| FY 33E |

| 34.68 |

| 13.37 |

| FY 34E |

| 38.50 |

| 13.49 |

| Terminal Value @ 3% terminal growth |

| 495.48 |

| 157.87 |

| NPV |

| $298.19 |

Risks

We believe Littelfuse to be a below-average risk company, thanks to its wide end-market diversification, strong balance sheet, and track record of profitable operations. Still, some of its end markets are sensitive to macroeconomic conditions. The company has historically experienced some cyclicality in its sales and earnings, and it is currently experiencing a down cycle. Should the US economy enter a recession next year, sales could decline even more, and this would probably result in an even lower share price.

Conclusion

Headwinds have continued for Littelfuse, and this has resulted in underperformance this year when compared to the S&P 500 index. We believe, however, that investors are too focused on the short to medium term, and are missing the long-term opportunity that shares offer at current prices. We believe Littelfuse shares to be trading below their fair value, and at a lower valuation compared to companies exposed to similar end-markets. This is why we are maintaining our 'Strong Buy' rating, and making it our top idea for next year.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Littelfuse: Our Top Stock Idea For 2024