LYV - Live Nation Entertainment: Explaining Its 7.1% FCF Yield And Why There's No Upside

2023-06-21 03:17:30 ET

Summary

- Live Nation is the largest facilitator of live entertainment worldwide, operating in three segments: Concerts, Ticketing, and Sponsorship & Advertising.

- The company connected 670 million fans in 48 countries in 2022, hosting over 43,600 concerts for over 7,800 artists and selling over 550 million tickets.

- After about 31% increase year-to-date, valuation is a major concern, as Live Nation continues to dilute shareholders and struggle to generate steady GAAP profits.

- Trading at a 122 forward GAAP P/E multiple, the current valuation leaves no room for upside. However, 2023 results should continue to impress, and justify a Hold rating, rather than a Sell.

Live Nation Entertainment ( LYV ) has seen its stock rise by 31% year-to-date, amid a historical year for live concerts. As a monopoly in its industry, Live Nation is one of the biggest beneficiaries of the immense demand for live shows.

While results in 2023 should strongly impress, I question the company's ability to generate steady GAAP net income in the mid-term. Trading at a 122.2 forward GAAP P/E multiple, and constantly diluting shareholders, I see no room for upside at current levels, and rate the stock a Hold (or a borderline Sell).

Company Overview

Live Nation is the largest facilitator of live entertainment worldwide. The company operates under three reportable segments - Concerts; Ticketing; and Sponsorship & Advertising. And, the business model is simple - make no profits from Concerts, but make a lot of profits from ticketing and ads by leveraging the company's positioning in concerts.

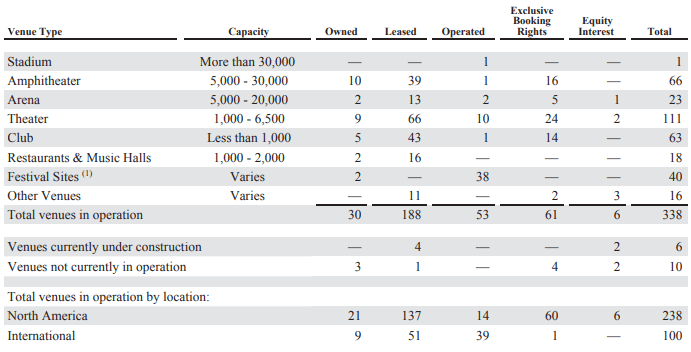

In 2022, Live Nation connected 670 million fans in 48 countries across its concert and ticketing platforms and hosted over 43,600 concerts for over 7,800 artists. LYV has significant influence in 338 venues globally and manages more than 410 artists. Through Ticketmaster, the company is also the leading live entertainment ticketing sales and marketing company, selling over 550 million tickets in 2022.

The following table summarizes the venues Live Nation has relations with, by type and capacity, as of December 31, 2022:

Live Nation Entertainment 2022 Annual Report (10-K)

{kind=link}

Concerts

The Concerts segment includes the global promotion, production, and operation of live music events, through owned, operated, and rented venues. In 2022, the Concerts segment generated $13.5B in revenues, which is 80.9% of total group sales. Concerts occur all year round, although there is some seasonality, with the second and third quarters typically being the strongest quarters of the year, as outdoor festivals and shows primarily occur from May through October.

As a promoter, LYV earns revenue from selling tickets and ancillary services, of which it pays artists a fixed guaranteed amount and/or a percentage of ticket sales or event profits. As an operator, LYV generates revenues from the sale of concessions (the right to sell merchandise, food, and beverages in the venue), parking, premium seating, and other relevant services.

Created and calculated by the author using data from Live Nation Entertainment financial reports

Concert revenues are at an all-time high, as pent-up demand caused by the pandemic is being met with mega tours. Notably, the EBITDA margin of this segment is extremely low, coming in at 0.5% for 2022. Pre-pandemic, the segment's EBITDA margins were in the 1.5%-2.0% range. Clearly, the Concert segment's goal is to drive the other two segments, which are the profit makers for the company.

Ticketing

The Ticketing segment acts as a ticket agency that sells tickets for events on behalf of its clients and retains a portion of the service charge as its fee. In 2022, Ticketing generated $2.2B in revenues, which is 13.4% of total group sales. Live Nation sells tickets for its own events as well as third parties across multiple live event categories, including sports, concerts, museums, theaters, and clubs. The company also facilitates resale platforms through which fans can resell or buy their tickets safely.

Most of the ticketing agreements with clients create multi-year commitments, ranging from 3-5 years. In some cases, those are exclusive agreements by which Ticketmaster has the sole right to sell all the tickets for a certain client, and in other cases Ticketmaster has the right to sell a portion of the client's tickets.

Created and calculated by the author using data from Live Nation Entertainment financial reports

Looking at Ticketing, it becomes clear that most of the economics are in this segment, rather than the concerts themselves. This is one of the reasons forcing LYV to spin off its ticketing business could be catastrophic. There's a clear alignment between Concert revenues and Ticketing, as the company generally uses its own platforms to distribute tickets for its concerts. Thus, we can see that the Ticketing segment saw all-time highs in 2022 as well, but in this segment, it's not only the revenues. EBITDA totaled $733M, reflecting a 32.8% margin, which is a record for the company as well.

Sponsorship & Advertising

The Sponsorship & Advertising segment provides sponsors with the ability to reach customers through Live Nation's concert, festival, venue, and ticketing assets. This segment generates revenues from selling ads on the company's websites and venues, as well as producing exclusive events for specific brands and clients. In 2022, Sponsorship & Advertising generated $968.1M in revenues, which is 5.8% of total group sales.

Created and calculated by the author using data from Live Nation Entertainment financial reports

Just like ticketing, the Sponsorship & Advertising segment leverages the momentum in Concerts to achieve all-time highs in revenues and EBITDA. However, the segment's margins are yet to reach pre-pandemic levels, as direct costs as a percentage of sales increased significantly.

A Monopoly In A Fast-Growing, Resilient Industry

The first way to tell if a company is a monopoly is to see how much it talks up the competition in its industry. Just like Microsoft is experiencing "intense" competition in office productivity and Visa and Mastercard are experiencing "intense" competition in payments, Live Nation claims "competition in the live entertainment industry is intense".

The competition is so intense, that poor Live Nation controls only 70% of the ticketing and live venues market . To put it simply, Live Nation is responsible for more than 90% of the most successful tours in the world, with names like Taylor Swift, Beyoncé, Harry Styles, Bruno Mars, Guns N' Roses, and Coldplay. No company in the world is even remotely close to challenging Live Nation's presence in this category, and this category is growing fast.

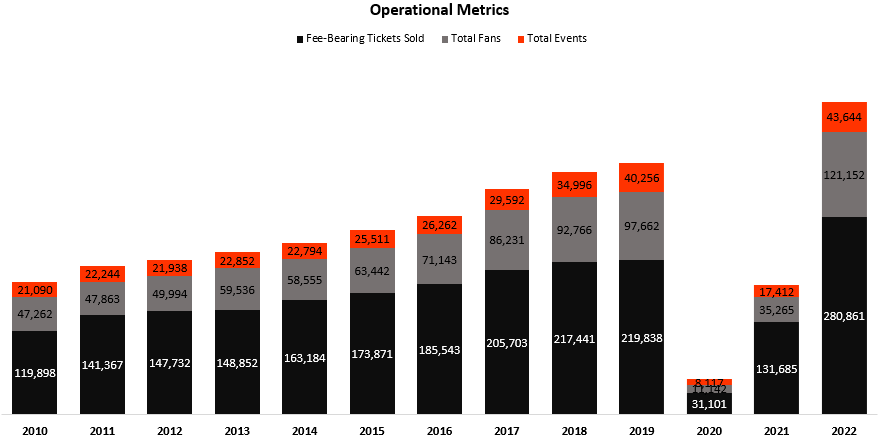

Show attendance in 2022 was up 24% from 2019, and Live Nation sees an even larger pipeline for 2023. Live shows are one of the most resilient categories in discretionary spending, with people willing to give up restaurants, travel, and apparel before they would be willing to miss an opportunity to see their favorite artist performing live.

Created by the author using data from Live Nation Entertainment financial reports (10-K); Numbers in thousands except Total Events.

{kind=link}

And as we can see, operationally, the live entertainment business is booming and has been growing sequentially, excluding pandemic-affected years. Since 2010, Live Nation has seen its total events, total fans, and total fee-bearing tickets sold, growing by a CAGR of 6.3%, 8.2%, and 7.4%, respectively.

According to management, this trend should continue, as the company is targeting double-digit adjusted operating income growth for the foreseeable future.

Growth Strategy

Looking at the linear growth of the company's metrics, it's hard to challenge the notion that demand for live events is constantly growing. For 2023, management expects a record number of fans, a record number of tickets sold at 600 million, and double-digit adjusted operating income growth in Sponsorship & Advertising, which is coming off a year of all-time highs.

With social media, it's hard to miss the fact that 2023 is the year of mega tours. Taylor Swift, Beyoncé, Harry Styles, and other renowned names are currently touring, filling stadium after stadium. When everything seems so bright, there's always the fear of becoming too complacent.

One important thing to take in mind is that most of Live Nation's business is non-recurring and somewhat cyclical in nature. Considering the fact the world's most successful artists are currently on tour, we have to consider the possibility of down years in the near term, as artists usually go on tour once every few years. However, when we exclude the Covid years, we see a clear linear trend since 2010.

This linear trend can be partially explained by the fact that some of the company's business is recurring, like live sports ticketing or annual festivals. Yet, live music concerts are a very significant portion of the company's business. Focusing on the live music business, there are two notable drivers for the linear growth we're seeing.

First, there's organic growth, which is a result of a growing number of stadium-filling artists, a growing demand for live shows, and steady price increases made by Live Nation (just think how much you paid for a concert ticket 5 years ago compared to now).

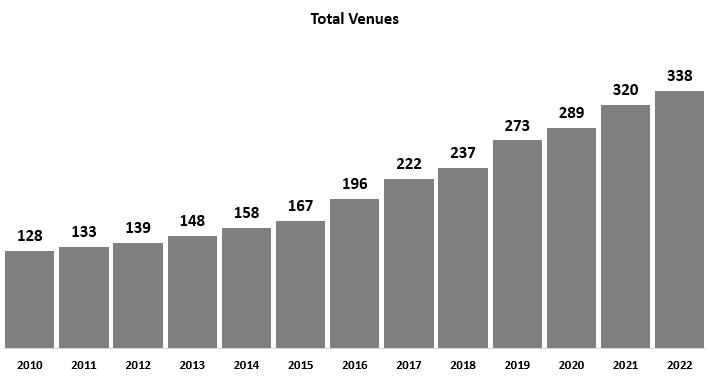

Second, there's geographic expansion. One of the most important drivers of growth for Live Nation is its ability to constantly expand its influence into more and more venues. While there's a growing total number of venues in the world, LYV has been able to maintain its control over its most important venues and grow the number of them.

Created by the author using data from Live Nation Entertainment financial reports (10-K)

{kind=link}

As we can see, the total number of operated venues has been growing steadily for the last 15 years, with an 8.4% CAGR. According to management, new venues are expected to welcome 3 million additional fans in 2023, hosting 1,000 shows.

Growth Projections

I expect 2023 to be a record year for the company, whereas growth in 2024 should decelerate, or even turn negative. However, over the long term, I expect Live Nation to continue to grow revenues at a high-single-digit to low-double-digit pace.

We think '24 into forward, you kind of look at what we historically have delivered. We've been a high single industry growth business and a high single-digit revenue AOI business year after year for many years. And we look going forward, we think we're back to being a great strong growth business year-over-year off this foundation of business.

--- Michael Rapino, President & CEO, Q1-23 Earnings Call

Regarding margins, Live Nation's cost inputs are limiting its ability to provide margin expansion. Management is clearly recognizing that and is focused on absolute dollar growth.

We don't assess over margins because, for instance, this year, we expect to be having a great stadium and arena year, as you could tell by the numbers we already gave for that's inherently going to be a lower-margin business than one of our amputate customers. We're still going to pursue that business, still a great business, but it impacts technically the margin, while generating cash profitability.

--- Joe Berchtold, President & CFO, Q1-23 Earnings Call

Valuation

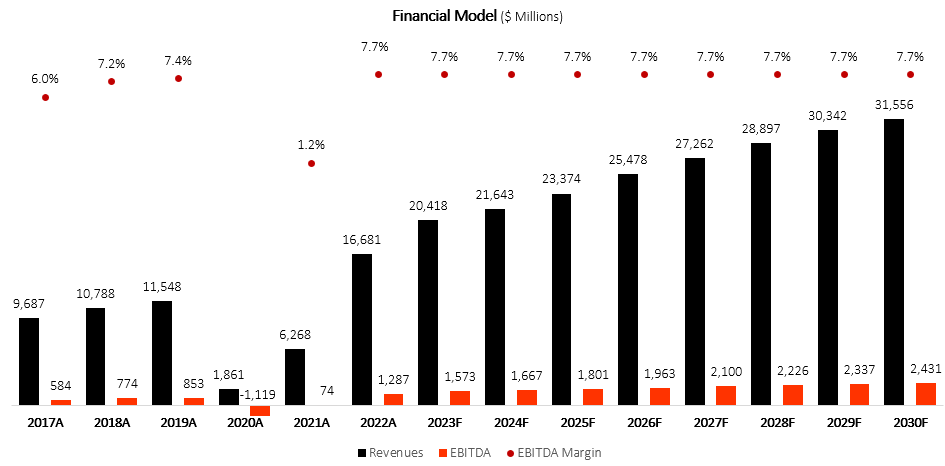

I used a discounted cash flow methodology to evaluate Live Nation's fair value. I assume the company will grow revenues at a CAGR of 6.4% between 2023-2030, based on the 7%-9% growth rate of its market, and considering 2023 being an extremely high baseline.

I project EBITDA margins to remain steady at 7.7% as the company focuses on absolute dollar growth rather than margins, and its costs are mostly connected directly to revenues.

Created and calculated by the author based on Live Nation Entertainment financial reports and the author's projections

{kind=link}

Taking a WACC of 9.5% (relatively high due to dilution) and adding LYV's net debt position, I estimate the company's fair value at $82.6 per share.

Risks - Dilution, No Net Income, No Cash Returns

In my view, Live Nation lacks emphasis on its shareholders' interests. Over the last five years, Live Nation outperformed the market by 19%, but there have been significant drawdowns along the way, and many investors are still in the red, whereas the S&P 500 index is almost fully recovered.

So, there's been outperformance, but not too impressive. Let's begin with dilution:

Since its IPO, Live Nation has been steadily diluting shareholders. Over the last 6 years, investors have been diluted by 3.5% annually. This is a questionable source to finance the company with, especially as Live Nation isn't highly leveraged, and as of last quarter, the company has zero net debt.

Created and calculated by the author using data from Live Nation Entertainment financial reports (10-K); Net Debt doesn't include lease liabilities.

One of the reasons I believe the company chooses to go the dilution route is the fact that it makes no GAAP net income, or at least not steadily. Live Nation generated positive net income to common shareholders only in four out of the last ten years, with interest payments being a major reason for the lack of GAAP profits.

Peter Lynch and Warren Buffett have been repeatedly quoted saying GAAP earnings are one of the most important metrics to observe in a company, and Live Nation's track record on that front isn't too impressive. While I do believe the company is on the right path, intra-year seasonality and the nature of its operations with deferred revenues are hurting its ability to provide steady GAAP EPS growth. As such, don't expect any dividends anytime soon.

Overall, it's clear that investors in Live Nation should focus on its free cash flows, rather than net income. However, free cash flows should be taken with caution because as soon as growth slows, FCF will quickly disappear.

Additionally, it's hard to overlook the constant dilution and inability to generate steady GAAP net income. While it does seem like the company is on track to achieve GAAP profitability in 2023, it's also important to take in mind the fact that many of the mega tours will not be continuing into 2024, and growth will definitely decelerate. The current valuation in my view is completely ignoring fundamentals, as well as the regulatory risks, and the company's underlying business model.

Conclusion

Live Nation has a monopoly in the resilient and fast-growing live entertainment industry. In 2023, the company is projected to record astounding growth and profits, as live events leave Covid-19 behind completely. However, the stock is more than pricing in the probability of record performance, and I expect that 2024 will highlight the company's somewhat cyclical nature, with significant growth deceleration.

I would rate the company a Sell, but I believe its results in 2023 will continue to impress. On the flip side, If the company stops diluting its shareholders and demonstrates an ability to generate GAAP profits steadily, I might change my view in another direction.

As the company trades at a forward GAAP P/E of 122 and shows no intention to stop diluting its shareholders, I see no shareholder upside in the foreseeable future. Thus, I rate the stock a Hold.

For further details see:

Live Nation Entertainment: Explaining Its 7.1% FCF Yield And Why There's No Upside