LYV - Live Nation Still Has Room To Run

2023-06-19 23:58:20 ET

Summary

- Live Nation Entertainment's revenue growth remains strong, with Q1 2023 revenue up 73% and operating income up 5.3 times compared to pre-pandemic levels.

- Despite recent spikes, the company's valuation is still reasonable, with price/forward earnings and price/cash flow ratios below historical levels.

- Although facing long-term uncertainties due to regulatory issues and potential changes in the ticketing industry, Live Nation's short-term future looks bright as it benefits from pent-up demand for live events.

Business Overview:

Live Nation Entertainment (LYV) is the world's largest promoter of live entertainment and ticket seller. Ticketmaster, the main platform of Live Nation Entertainment, provides ticket sales, ticket resale services, promoting, marketing, and distribution services globally.

Live Nation Entertainment has three main segments. Its Concerts segment accounts for about 75% of revenue, its Ticketing segment accounts for approximately 20% of revenues, and its sponsorship & Advertising accounts for 5% of revenues.

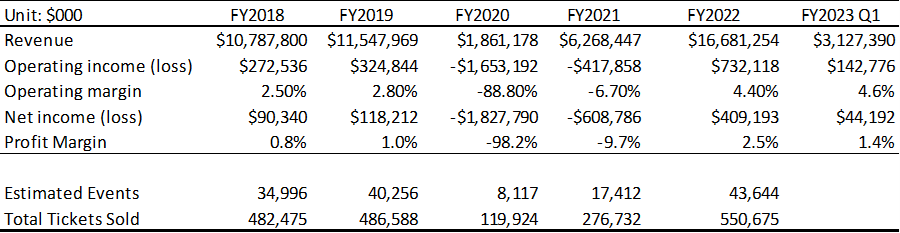

Revenue growth is still healthy.

Not surprisingly, Live Nation experienced significant business slowdown during the pandemic period (2020-2021). The year-over-year growth for FY 2022 was extremely strong due to the low base in 2021 and strong economic recovery. Thus, I compared Live Nation’s 2022 performance with its pre-pandemic period. Compared to FY 2019, Live Nation’s 2022 revenue growth rate was 44.5%, mainly due to the changing consumption patterns in the US, from goods consumption to service (especially traveling) and experience consumption.

{kind=link}

In Q1 2023, Live Nation’s revenue was up 73% and operating income was up 5.3 times. The trend of strong growth is continuing. In addition, operating margin and profit margin are lower than the 2022 level but still well above the pre-pandemic period.

Summer and fall are usually the strong seasons for live events. I expect the revenue growth rate would slightly decline from Q1 due to the high base effect. However, the healthy profit margin is likely to continue given the weakening inflation.

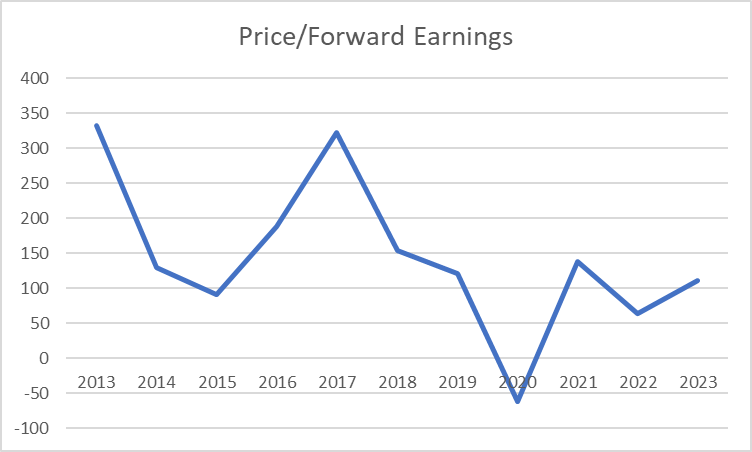

Valuation is still reasonable.

{kind=link}

Excluding the pandemic period, current valuation is well below the historical valuation. Price/forward earnings ratio currently is higher than 2022 but is below most of the pre-pandemic period.

{kind=link}

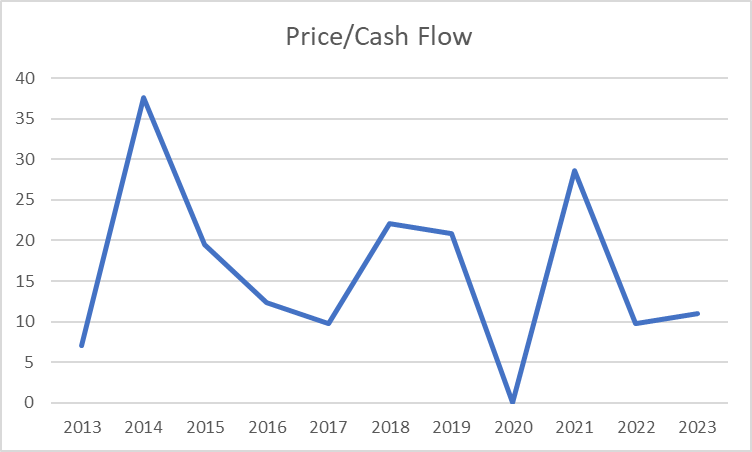

Price/cash flow ratio is also near the historical low, excluding the pandemic period. Thus, Live Nation is “cheap” compared to its own history.

The stock is not "cheap", but despite the recent spike, its valuation is still reasonable.

Monopoly position is safe for now, though long-term uncertainty remains.

Live Nation currently accounts for about 70%-80% of the concert ticketing market after the Taylor Swift ticket-sales debacle in November of 2022 . Its monopoly position is under scrutiny of the regulators. The regulatory issues facing Live Nation are two-fold: the DOJ investigation and the proposed legislative bills.

Given the strong anti-trust policy trends of the current administration, it is very likely that the DOJ investigation would conclude that Live Nation violated terms of their 2010 settlement that required Ticketmaster to license its ticketing software and divest some ticketing assets. If so, I also expect that DOJ and Live Nation would go to court to litigate. Thus, it is a potential long-term problem for shareholders of Live Nation.

Multiple legislative bills were proposed to change the practice of ticketing industry’s practice. Those bills mainly aimed to change two things: the company's exclusive arrangements with venues and/or transparency of ticket prices. Between these two targets, transparency of ticket prices is the low-hanging fruit. It is easier to achieve and its impacts on Live Nation’s revenue and profit should be modest in the long term. Live Nation has already announced that it will adopt total transparency on ticket pricing starting September.

Live Nation’s exclusive arrangements with venues have a much bigger impact on the company’s business. However, it is more difficult to change through legislation. The reason is that contract payments made by Live Nation to venues are a very important stable revenue stream to venue owners. Ending this practice may cause venues to raise prices even more on consumers to compensate the loss of this revenue stream.

DOJ investigation and the threats to end exclusive contracts with venues brought long-term uncertainties to Live Nation’s business model. By now, the market is already fully aware of those risks.

Conclusion:

Although Live Nation faces long-term uncertainties, its short-term future is bright. The summer season of live performance is here and Live Nation is still benefiting from pent-up demand for live events due to the huge backlog. Strong revenue and profits from the second and the third quarters in FY 2023, combined with the still reasonable valuation, should provide tailwinds to stock prices.

For further details see:

Live Nation Still Has Room To Run