LYV - Live Nation: Ticketmaster Breakup Improbable But Exposes Vulnerabilities

2023-08-11 17:13:47 ET

Summary

- Live Nation is the largest facilitator of live entertainment worldwide, operating in three segments: Concerts, Ticketing, and Sponsorship & Advertising.

- The company is on pace for a record year after it connected 670M fans in 48 countries, hosted 43,600 concerts for 7,800 artists, and sold 550 million tickets in 2022.

- Regulatory pressures and a Ticketmaster breakup possibility are weighing on the stock, sending it into a sharp dip of more than 13% from its July peak.

- I find a Ticketmaster breakup highly improbable, as the company's entire business model relies on the business, and even before a breakup, it is struggling to generate profits.

- I rate the stock a Hold, as I expect growth deceleration and continued struggles to generate GAAP profits, both of which are not currently reflected in the valuation and consensus estimates.

Live Nation Entertainment ( LYV ) saw its stock rise by 45% to reach its 2023 peak leading up to its second-quarter results, amid a record year for live concerts.

Following the earnings release, the stock experienced a sharp decline, but it wasn't because of the company's results, rather, it was a Politico article stating the Ticketmaster business could face new legal threats as soon as this fall, which could potentially lead to a breakup of the company.

As a monopoly in its industry, Live Nation is one of the biggest beneficiaries of the immense demand for live shows. That being said, its model requires owning both the ticket-selling business and the concert-producing segment, as the majority of the economics are captured in the ticket-selling process.

For that reason, I find a breakup highly unlikely. However, I believe the dependency between the segments exposes important vulnerabilities that investors should not overlook.

I reiterate Live Nation as a Hold and estimate the company will struggle to provide market-beating returns on a steady basis in the long term.

Background

In June, I wrote my first article about Live Nation Entertainment, ' Explaining Its 7.1% FCF Yield And Why There's No Upside ', where I dove into the company's business model, operating segments, growth prospects, and risks, as well as described my investment thesis.

In a nutshell, I believe the company's business model is great as long as it's able to generate growth, as the company enjoys a favorable cash cycle. However, the live shows business is cyclical, and after a record year for live shows with the world's most successful artists touring, I expect significant growth deceleration in 2024. This will expose the vulnerability of the company's business model, and result in a decrease in net income.

Let's briefly go over the second quarter numbers before analyzing the implications of a Ticketmaster breakup.

Second Quarter Review

Revenues grew 27.0% to $5.6 billion, an all-time second-quarter record for the company. Gross profit was $1.5 billion, reflecting a 26.0% margin, a 30 bps decrease from the prior year period, caused primarily due to a change in mix, as Concerts revenue was higher in the quarter.

Operating profit was $386 million, and operating margin was 6.9%, a similar 30 bps decline, which is entirely attributed to the decrease in gross margin. Net income was $294 million, reflecting a 5.2% margin, up 100 bps, primarily due to significantly higher interest income.

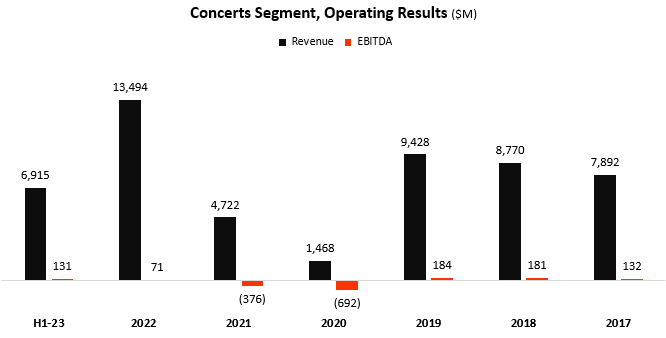

Concerts

Created and calculated by the author using data from Live Nation Entertainment financial reports

{kind=link}

Concerts revenue increased 44% to $6.9 billion during the first half of 2023 as compared to the same period of the prior year, primarily due to more shows and festivals in Europe and the United States as well as the Asia Pacific market, which was largely closed during the first half of 2022. Concerts had incremental revenue of $299.1 million during the period from acquisitions and new venues.

Concerts EBITDA grew more than 5x and reached $131 million, due to revenue growth and a 140 bps margin expansion derived from operational improvements in SG&A.

Concerts operating loss was $6 million, compared to a loss of $112 million in H1-22. As we can see, even at its peak, the Concerts segment operates at a loss, which we'll discuss in further detail later.

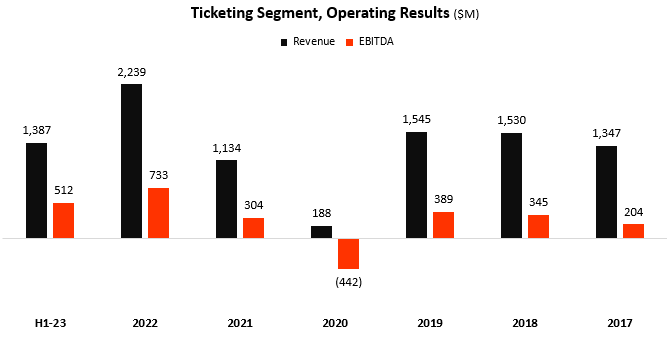

Ticketing

Created and calculated by the author using data from Live Nation Entertainment financial reports

{kind=link}

Ticketing revenue increased 31% to $1.4 billion during the first half of 2023 as compared to the same period of the prior year, primarily due to higher primary and secondary sales volumes driven by more events on sale, and upward pricing momentum due to higher demand and artist mix.

Ticketing EBITDA grew 31% and reached $512 million, due to revenue growth and a slight margin contraction.

While Concerts operate at a loss, Ticketing achieved a 33.1% operating margin in the first half of the year, compared to 31.6% in H1-22.

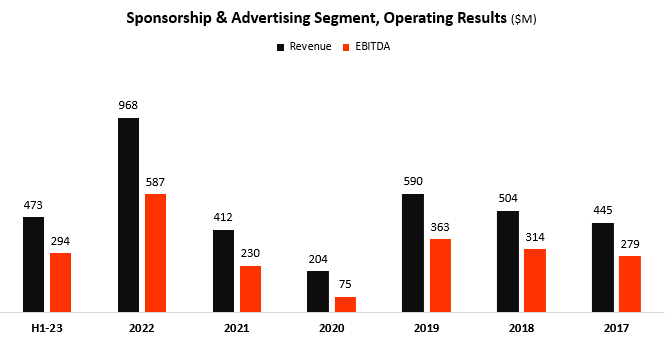

Sponsorship & Advertising

Created and calculated by the author using data from Live Nation Entertainment financial reports

{kind=link}

Sponsorship & Advertising revenue increased 25% to $473 million during the first half of 2023 as compared to the same period of the prior year, primarily due to new venue sponsorships and increased activity in international markets.

Sponsorship EBITDA grew 20% and reached $294 million, as revenue growth was partially offset by a 234 bps margin contraction resulting from higher artist expenses.

Sponsorship & Advertising operating profit was $251 million, reflecting a 53.2% operating margin, compared to 60.1% in H1-22.

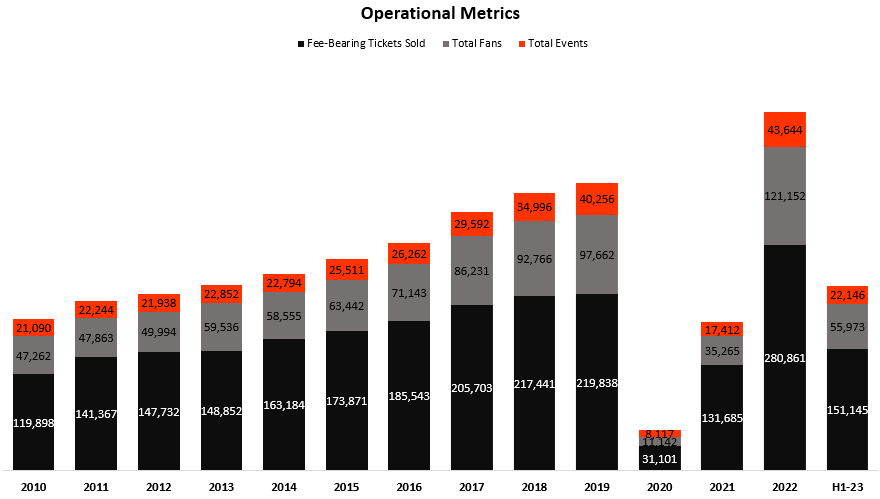

Operational Performance

Created by the author using data from Live Nation Entertainment financial reports (10-K); Numbers in thousands except Total Events.

{kind=link}

Operational growth was broad-based, as total events grew 15.0% to 22,146, total fans grew 25.1% to nearly 56 million, and fee-bearing tickets sold grew 22.4% to over 123 million. As we can see, the company is on pace to achieve all-time highs in all three metrics, as the record year for live shows continues.

Regulatory Pressures Increasing

In my previous article, I discussed Live Nation's monopolistic hold on the live shows industry:

The first way to tell if a company is a monopoly is to see how much it talks up the competition in its industry. Just like Microsoft is experiencing "intense" competition in office productivity and Visa and Mastercard are experiencing "intense" competition in payments, Live Nation claims "competition in the live entertainment industry is intense".

The competition is so intense, that poor Live Nation controls only 70% of the ticketing and live venues market . To put it simply, Live Nation is responsible for more than 90% of the most successful tours in the world, with names like Taylor Swift, Beyoncé, Harry Styles, Bruno Mars, Guns N' Roses, and Coldplay. No company in the world is even remotely close to challenging Live Nation's presence in this category, and this category is growing fast.

Live Nation Entertainment and Ticketmaster specifically have been under regulatory scrutiny ever since they completed the merger back in 2010. After major crushes during the sale of Taylor Swift concert tickets, regulators' and fans' criticism increased, claiming it's a demonstration of a low-quality service that's only able to maintain its success through the abuse of its monopolistic power.

Supposedly, through ownership and exclusive deals with the world's most important venues, artists are forced to use Live Nation's services. Live Nation then allegedly forces those artists and venues to use its ticketing service, Ticketmaster. According to claims, those Ticketmaster deals are either unfair in terms of price or unfair in terms of blocking other alternatives.

Regarding the price for fans, I think live show tickets are clearly mispriced, but to the low side. Tickets are sold on the secondary market for a significantly higher price, and could sometimes reach a 5x or a 10x markup. On the Artists' side of things, it's harder to say whether or not they have a claim against Live Nation's pricing actions. However, it's commonly known that artists make the majority of their profits through concerts, while other distribution forms like streaming are much less favorable economically.

Regarding the quality of service, there haven't really been major complaints lately, aside from the Taylor Swift saga. And considering the absolute mania surrounding her tour, I don't blame Ticketmaster for crushing.

All of this doesn't matter much to the DOJ, which has been very active lately in filing lawsuits with questionable merits. As we'll discuss in the following section, investor sentiment is seemingly very sensitive to the regulatory cloud that's casting a shadow over the company.

Ticketmaster Breakup Improbable

LYV shares were on a steady upward trend in the months leading to its second-quarter announcements. While the results were better than expected, they are completely overshadowed by the Politico article.

As we can see, the stock declined sharply and is now trading 13% below its July peak. As you can understand by now, I believe the chances of a Ticketmaster breakup are extremely low, as it's the only profitable business of the company, which isn't really a high-margin business anyway.

While it could be argued that if the Concerts segment wasn't a part of the entire group, it wouldn't be operating at a loss (meaning that management intentionally decides to subsidize the Ticketing segment), I believe this isn't true. Looking at the company's results prior to the Ticketmaster acquisition, it operated at a loss as well.

But, It Exposes Vulnerabilities

I believe the worst-case scenario with regard to regulatory intervention is some kind of fine. However, I believe investors are right to be scared of a breakup, because the company's entire business model relies on the cash advances it generates through selling tickets, and that's what I mean when I say the breakup threat exposes Live Nation's vulnerabilities.

As I wrote in my previous article, Live Nation struggles to generate any kind of GAAP net income. Even in a record 2023, its net income margin should stay in the low single-digit range. As market participants focus on the company's cash generation, it's important to remember the purpose of GAAP accounting and the differences between the cash flow statement and the income statement.

In essence, the income statement reflects the company's business if all expenses and revenues happened concurrently, whereas the cash flow statement reflects the actual movements of cash.

To put it simply, if I plan to sell you a hamburger for $10 two years from now, and you paid in advance today, this year's cash flow statement will show I generated $10, whereas the income statement will show nothing, as revenues and expenses are recognized only at the moment the service or product was transferred.

And here's the trick - the Ticketmaster segment provides the service and the buyer gets his ticket, thus, Ticketmaster's income statement shows profits, while it also generates cash. However, the Concerts segment doesn't provide the truly expensive service yet (producing the concert), and thus, at the consolidated level, the company generates high amounts of cash and low amounts of profits.

The problem is that at the moment people stop buying a lot of tickets in advance, because, for instance, Taylor Swift or Beyonce aren't touring next year, then, the cash flows will decrease as well, and then you're left with a company that struggles to generate real profits.

Valuation

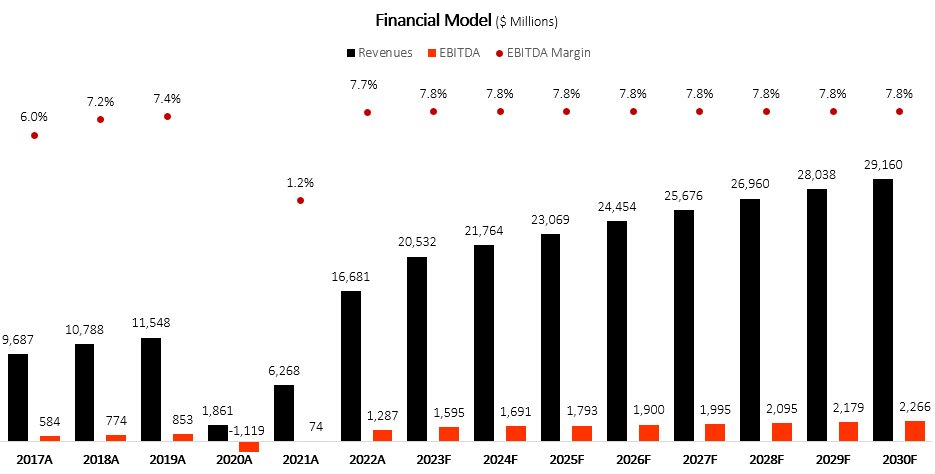

I used a discounted cash flow methodology to evaluate Live Nation's fair value. I assume the company will grow revenues at a CAGR of 5.1% between 2023-2030, based on the growth rate of its market, and considering 2023 being an extremely high baseline.

I project EBITDA margins to remain steady at 7.8% as the company focuses on absolute dollar growth rather than margins, and its costs are mostly connected directly to revenues.

Created and calculated by the author based on Live Nation Entertainment financial reports and the author's projections

{kind=link}

Taking a WACC of 9.5% (relatively high due to constant dilution) and adding Live Nation's net debt position, I estimate the company's fair value at $87.90 per share.

Back-Of-The-Envelope-Math

I want to add additional color here. Current consensus estimates expect revenues to grow approximately 6% in 2024, not too high of an expectation. However, consensus estimates for EPS show an astounding 54% growth next year.

Keep in mind, this is a company that's constantly diluting its shareholders and is struggling immensely to generate net income. I don't see a scenario where it's all of a sudden able to grow EPS in such excess of revenues. Additionally, I believe even the 6% revenue growth expectation will be tough to achieve, following a record year that combined mega-tours and high pent-up demand.

And, even if the company does achieve $1.71 EPS in 2024, it still reflects a high 50x P/E multiple, which I find too high.

Conclusion

Live Nation has a monopoly in the resilient and fast-growing live entertainment industry. The company is on pace to achieve a record 2023, driven by several mega-tours and high pent-up demand.

The stock experienced a sharp decline due to a regulatory threat to break up its Ticketing division, a move that could be devastating, as the ticketing division is the profit center of the company.

While I find a Ticketmaster breakup improbable, I believe it exposes the company's underlying vulnerabilities, which include its inability to steadily generate net income, and its somewhat cyclical nature.

I don't expect Live Nation to provide steady market-beating returns in the long term, and rate the stock a Hold.

For further details see:

Live Nation: Ticketmaster Breakup Improbable, But Exposes Vulnerabilities