BCS - Lloyds Banking: Positioned Well Long Term With Risks

2023-05-04 05:14:26 ET

Summary

- Lloyds Banking Group plc provides a range of banking and financial services in the United Kingdom.

- Revenue growth is poised to improve as LBG expands its services and interest rates remain high.

- LBG's assets remain resilient and diversified, reducing the risk of liquidity concerns. Q1 results suggest a small uptick in credit issues but profits continue to grow.

- Markets and Management are fearful that performance will decline in FY23, representing a short-term risk for long-term upside.

- LBG stock is attractive relative to its peers, so we rate a buy.

Investment thesis

Our current investment thesis is:

- LBG is a healthy European bank with high-quality assets.

- Product expansion looks smart and has the potential to improve returns.

- Near-term gains are high due to interest rates, allowing for heightened distributions.

- LBG performs relatively well compared to its UK peers, and its valuation implies upside.

Company description

Lloyds Banking Group plc (LYG) provides a range of banking and financial services in the United Kingdom. It operates through three segments:

- Retail - offers a range of financial service products, including current accounts, savings, and mortgages to personal and small business customers.

- Commercial Banking - provides lending, transactional banking, working capital management, risk management, and debt financing services to small and medium-sized entities, corporates, and institutions.

- Insurance, Pensions, and Investments - offers insurance, investment, and pension management products and services.

The company offers its products and services under the Lloyds Bank, Halifax, Bank of Scotland, and Scottish Widows brands.

Share price

LBG's share price has struggled in the last decade, with post-GFC legislation making trading conditions in Europe far more difficult. Further, the business did not come out unscathed, with a disastrous organized merger with HBOS (A GFC strategy that involved combining bad banks with good banks).

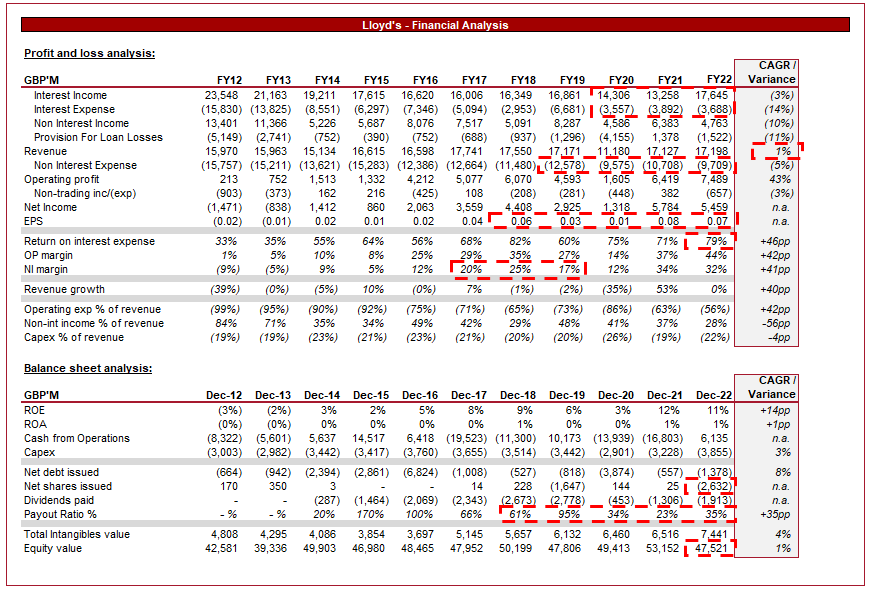

Financial analysis

LBG Financial performance (Tikr Terminal)

{kind=link}

Presented above is LBG's financial performance for the last decade.

LBG is one of the big 4 banks in the UK, alongside HSBC ( HSBC ), Barclays ( BCS ), and NatWest ( NWG ). We have covered all 3 stocks, assigning a buy rating to each.

Commercial profile

Introduction

LBG's revenue has grown at a CAGR of 1% in the last decade, with the recent 5 years being relatively flat. This covers two different monetary policy periods. For most of the decade, European banks have struggled with their recovery due to record-low interest rates, reducing the ability to generate returns. Commercial banks borrow short to lend long, at the rates we were seeing, lending activity was lucrative. LBG is the biggest mortgage lender in the UK (And the second largest for Credit Cards ), giving it significant exposure to this underperformance. Unlike HSBC and Barclays, LBG does not have any material investment banking operations, relying on interest to generate returns.

In the last 2 years, we have seen a change in monetary policy.

Economic considerations

Inflationary pressure has taken hold in the UK, driven by an extended period of relaxed monetary policy, supply chain issues, and the aftermath of the pandemic. In response to this, we have seen the Bank of England (BoE) incrementally raise rates across most of 2022.

This has worked to slow inflation, but as the graph above illustrates, inflation is stubborn. Rate hikes have likely not peaked, as the BOE remains focused on bringing this down. Our view is that rates will not begin falling until Q1-24 in the UK. We will now briefly summarize the impact current conditions have on consumers and businesses, LBG's clients.

The impact on consumers is a "double-whammy". Inflationary has been reducing real incomes as pay rises across many industries fail to keep pace. This is contributing to consumers dipping into savings, as well as reducing discretionary spending and increasing borrowing. Further, a secondary impact is from the risen rates. Borrowing costs also rapidly rise, further deteriorating take-home pay.

The nuance with the UK, which will likely mean the impact is greater, is due to the high home ownership in the country. The majority of fixed-rate mortgages in the country (c.57%) will need to be renewed in 2023 (or will revert to the base rate). British consumers generally fix for a short period (2-5 years), as a means of locking in at lower and lower rates. For this reason, most of the 57% are locked in at <2% and are facing rates in the region of 4-6%. To illustrate this, if a consumer borrowed £270k 5 years ago and locked in at 1.5% for 25 years, their monthly payment (repayment & interest) would be £1,080. This increases to £1.35/£1.5k at 5.5% (20/25 years). This is a substantial increase.

Businesses are facing slowing demand from consumers, as well as rising input costs. Further, with rates rising, it is more difficult to raise debt at attractive levels, deterring spending.

Interest income

Despite the bearish economic outlook, this has been good for LBG. The rising rates have allowed the bank to substantially improve its lending returns, with its interest payments on deposits remaining relatively fixed. In FY22, its return on interest expense increased to 79%, which is the second-highest level in the decade. The most recent rate hike was in Mar23 , implying returns will continue to increase throughout the year, especially if our forecast rate-change timeline occurs.

ECL (Expected Credit Loss)

The offsetting factor during rate hikes is an increase in bad loans. Due to the squeeze on consumers and businesses, current economic conditions are usually conduits to default.

In the most recent quarter, we have seen an increased number of loans face difficulty, potentially reflecting an end of resilience in the market. Although it is too early to suggest we will see a jump in impairments, LBG is quick to highlight that levels remain well below Q1/2-20.

Arrear payments and overdraft usage (Lloyds)

The good news for LBG is that we think the business has a quality portfolio of assets. The average LTV of the mortgage portfolio is 42%, with 93% of the portfolio <80%. This will reduce the payment impact on consumers and increases the property value-to-loan delta in the case of foreclosure. Further, 90% of SME lending is secured, with >75% of commercial exposure at an investment-grade level. Finally, regarding commercial real estate, the average LTV is 44%, with >95% with a LTV of <70%.

The key concern is how the retail (consumers) segment develops. It is LBG's biggest exposure and has the potential to deteriorate between quarters with little warning.

LBG's deposits (LBG)

Commercial conclusion

Overall, our expectation is for LBG to perform extremely well over the coming years (before debt provisions). Its large loan book is structured well and the higher rates will allow the business to earn outsized returns. Although we are expecting rates to begin their descent in 2024, it will not be a rapid decline. Further, there will be questions about where it declines to. The key to this all will be how the ECL develops. So far, the provision is in line with FY19 but already elevated well beyond FY14-FY18.

Long-term prospects

Looking long term, LBG's growth prospects will come from an expansion of services in the UK. Being in a leading position for retail banking is fantastic, but it limits the company's ability to grow organically, with anti-trust threats stopping inorganic methods.

Management is considering creating a tiered system for its services, targeting high-wealth individuals with a premier service. This is an opportunity for LBG to expand into an area underserved by commercial banks, with only HSBC having a significant product offering. Wealthy Britons are mainly covered by "boutique" firms, such as Coutts (Owned by NatWest), Julius Baer, and others. The key will be to quickly expand beyond this and gain market share in wealth management, as this partners perfectly with HNW clients and is more lucrative. Again, outside of HSBC, this is a fragmented market supported by boutiques.

Further, LBG is also investing in insurance services, another segment that allows the business to utilize its financial services expertise. This has been accelerated through the acquisition of Cavendish Online and has the opportunity to create an all-weather portion of revenue.

Finally, LBG has created a home rental business . According to the FT , the objective is to own 10k residential properties by 2025, with a longer-term target of 50,000 by 2030, making LBG one of the UK’s largest landlords. This has the potential to generate an estimated ROA of 6% , substantially higher than its current level.

Margin

Margin improvement has been materially driven by the increased return from lending activities. This being said, it is worth noting that Management (And former head António Horta-Osório) have done well to "clean up" the bank following the GFC.

Operating expenses as a % of revenue declined from >(90)% to low (70)s. The factors contributing to this are a reduction in geographical footprint as banking increasingly becomes digital, greater operational efficiencies with headcount reduction and the elimination of loss-making and low-profitability departments.

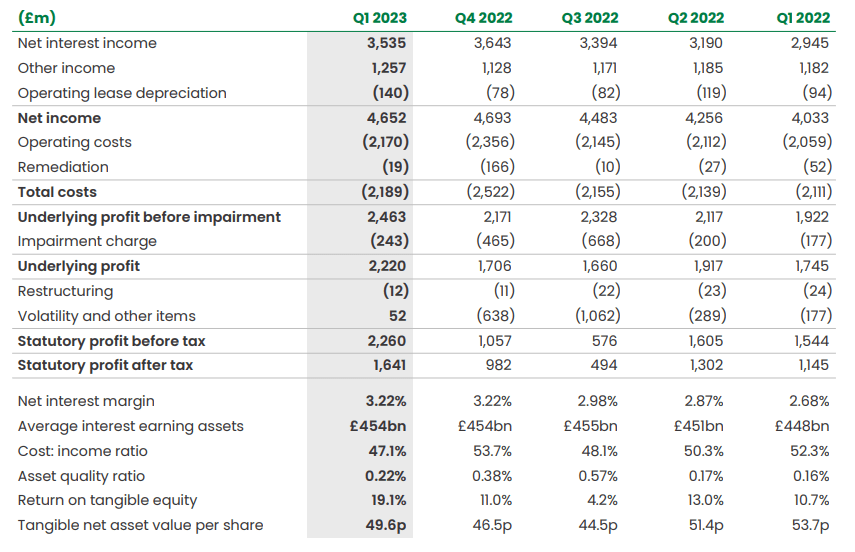

Q1 results

{kind=link}

LBG has recently announced its Q1 results. Revenues have increased substantially Y/Y, beating analyst estimates with interest income continuing to drive profitability. This is not a unique result, HSBC, Barclays, and NatWest posted outstanding results. The question then becomes, why did the share price decline?

Lending has only marginally increased, with mortgages and SMBs down. These are two segments that are of higher risk and reflect a continued weakening in the market, with demand down. Further, consumer deposits have declined, which suggests they are forced to access savings and are shopping around for higher rates. These are near-term bearish indicators.

Lending and deposit change (LBG)

Further, the company's net position is a slight decline in deposits, which reduces its long-term earnings potential. Markets are likely pricing in a continued decline in the coming quarters.

Deposit change (LBG)

The biggest concern is that ECLs continue to suggest uncertain market conditions, worrying investors for the coming quarters.

Outlook

The strong returns in Q1 have not tempted LBG to guide growth in the coming year. In line with its peers, the bank is expecting a flat year. Our view is that this is continued conservatism from the British Banks. All evidence currently suggests an outperformance is highly likely, even if ECL begins ticking up. We see no reality where rates fall before 3.5% in 2023, which means interest income will remain strong.

The issue with this guidance is that it scares markets. We are not surprised to see the stock down despite the beat when LBG (and the other banks) are essentially telling markets to be scared of the coming quarters.

Peer analysis

Profitability (Seeking Alpha)

Comparing LBG to the other UK banks, it performs relatively well. The business is more profitable than both Barclays and NatWest and only below HSBC. With a substantial Asian presence and scale benefit, HSBC is superior. Efficiency-wise, the delta increases from Barclays/NW and closes to HSBC.

Valuation

Valuation (Tikr Terminal)

LBG is currently trading at a slight premium to all businesses on an earnings basis, but below HSBC on other metrics. The issue we find with looking at P/E is that these banks tend to regularly incur one-off charges, distorting the underlying performance value (although given the regularity, some may say it's part of the normal course of business). LBG, HSBC, and Barclays incurred £0.7m, £2m, and £1.1m below the line respectively in the LTM. Further, our view is that all 3 banks remain a buy, implying their valuations are undervalued.

Our view is that a 1.8x sales multiple is creeping toward the top-end valuation of the business, but does leave value on the table, especially because we expect the strong performance to continue into FY23. LBG can reach closer to 2x, with the substantial cash generated in FY23 going toward buybacks/dividends, as well as funding expansion. This implies an upside of 14%. Analysts are currently guiding £7.2bn PBT (4% growth), with a target upside of 35% ( Source: Seeking Alpha ). Although the upside looks rich to us, the profit guidance looks reasonable.

Key risks with our thesis

The risks to our current thesis are:

- Material changes in UK economic conditions (This is a catch-all risk). Including but not limited to a recession being triggered, a material increase in defaults, and/or a rise in unemployment.

- Larger than expected decline in deposits, pressuring Management to increase the interest paid.

Final thoughts

LBG is a solid banking choice for investors. The company's assets are high quality and the business has scope for services expansion in the coming years. In the near term, we expect the business to continue earning outsized returns through FY23, resulting in estimate beats until Management boosts guidance, which has the potential to cause price action.

The key and continuing risk (and what is stopping Management from increasing guidance now) is ECL. Credit analysis of LBG's books suggest there was a mild weakening in the last 3 months, which could develop further or remain at its level. Our view is that this still means asymmetric returns. If defaults increase and the company comes in down/flat, you are still buying a solid bank with long-term upside. If the company beats and the UK economy remains resilient enough to escape this period, the share price will likely rally in the short term.

LBG is the last to report of the big 4 and so investors would be wise to keep a keen eye on the other 3.

For further details see:

Lloyds Banking: Positioned Well Long Term With Risks