WBD - Longleaf Partners Global Fund Q2 2023 Commentary

2023-07-20 04:02:00 ET

Summary

- Longleaf Partners Funds is a suite of mutual funds and UCITS funds that Southeastern Asset Management, the investment advisor to the Longleaf Partners Funds, created in 1987 as a way for Southeastern employees to invest alongside their clients.

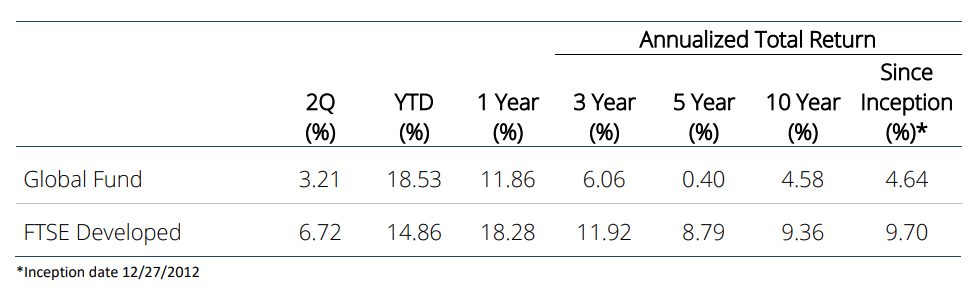

- Longleaf Partners Global Fund added 3.21% in the second quarter, taking year-to-date returns to 18.53% for the first half.

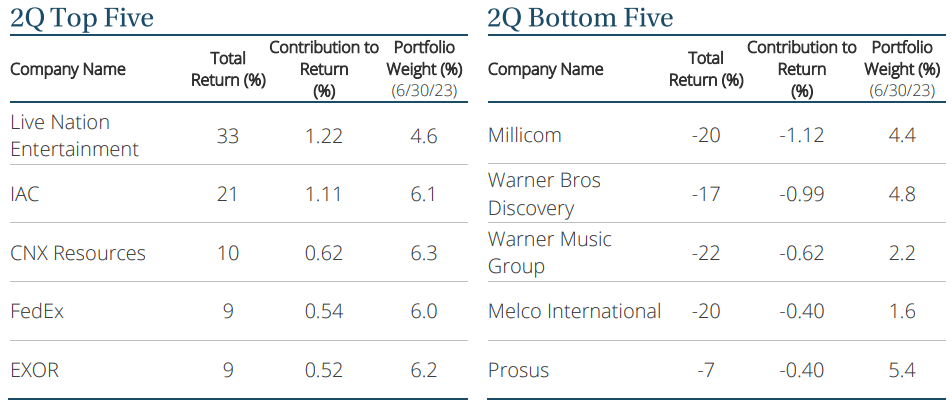

- Live Nation Entertainment, a new purchase this year, was the top contributor in the quarter and a top performer for the first half.

{kind=link}

| Returns reflect reinvested capital gains and dividends but not the deduction of taxes an investor would pay on distributions or share redemptions. Performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting southeasternasset.com. The prospectus expense ratio before waivers is 1.33%. The expense ratio is subject to a fee waiver to the extent the Fund’s normal operating expenses (excluding interest, taxes, brokerage commissions and extraordinary expenses) exceed 1.15% of average net assets per year. |

Longleaf Partners Global Fund added 3.21% in the second quarter, taking year-to-date ((YTD)) returns to 18.53% for the first half. While the portfolio’s lack of exposure to Information Technology and relative overweight to Consumer Discretionary weighed on relative results in the quarter, the Fund outperformed the FTSE Developed Index in the first half in an environment that strongly favored growth.

The central macro theme in the second quarter and for the first half was the reemergence of a handful of mega-cap growth stocks driving the market. These stocks dominated markets over the last decade but suffered an initial collapse of over 30% from January 2022 to the Nasdaq’s recent low point in October 2022, before rallying over 40% in the last six months. The market rarely moves down (or up) in a straight line, as we have learned through multiple previous cycles. This reminds us of the early stages of the dot-com bubble, when the Nasdaq fell over 35% from March 2000 highs before temporarily rebounding 36% in 2Q 2000, only to drop a further 80% over the subsequent 25 months, as shown in the charts below.

{kind=link}

While every period is different, we believe the mega-cap tech darlings are similarly primed today for a more precipitous decline in the face of peak margins on top of increased competition and regulation.

However, the Fund’s ability to produce strong relative results is not predicated on a market correction. We continue to see solid operational results across our portfolio holdings, translating into positive stock performance for many. Our management partners are on offense with strong balance sheets and pricing power, allowing them to grow and recognize value in more challenging market environments.

We encourage you to watch our video with Portfolio Managers Ross Glotzbach and Staley Cates for a more detailed review of the quarter.

Contribution To Return

{kind=link}

- Live Nation ( LYV ) - Live Nation Entertainment, a new purchase this year, was the top contributor in the quarter and a top performer for the first half. We had the opportunity to buy Live Nation on the back of the well-publicized controversy faced by Ticketmaster after the botched Taylor Swift tour pre-sale event in November, which lead to short-term fan and political pressure. The industry continues to have great demand tailwinds for the long term. Even after a strong 2022, concerts further accelerated in 2023, driving the positive stock price performance in the quarter. We have prior knowledge of Live Nation from our time owning various Liberty Media entities and are encouraged on future capital allocation that Liberty is still on the case as a 30%+ owner.

- IAC ( IAC ) - Digital holding company IAC was a top contributor in the quarter and in the first half, after having been among the largest detractors in 2022. Underlying holding MGM ( MGM ) has continued to deliver great results, reporting double-digit profit growth while being one of our largest share repurchasers. Controlled companies Angi ( ANGI ) and Dotdash Meredith have stabilized following positive management changes at Angi and further business integration at Dotdash Meredith. Angi reported year-over-year (YOY) revenue declines but positive YOY operating cash flow (OCF). Dotdash reiterated guidance for the second half with expected growth in revenues and OCF as it rolls off more challenging 2021 YOY comparables. IAC bought back more shares in the quarter than it has in many years, while also buying more Turo shares at good prices, and it still has net cash at the parent level.

- Millicom ([[TIGO]], [[MICCF]]) - Latin American wireless and cable company Millicom was the top detractor in the quarter but remains a meaningful positive contributor for the year. The company announced a disappointing quarter of organic revenue and EBITDA declines driven by its Guatemala business. In June, Millicom confirmed it had ended potential takeover discussions with private equity company Apollo Global, which the market had rewarded in the first quarter and disliked in the last month. We were not counting on an Apollo buyout as an outcome, and our appraisal was not impacted by the news. Much more compellingly, French billionaire Xavier Niel, founder of French broadband Internet provider Iliad, grew his stake to almost 25% in the quarter and said in a public statement, “We remain fully convinced that Millicom’s potential is untapped and under-utilized, particularly when it comes to hidden infrastructure and asset value. We have a clear view on how opportunities can be unlocked, and are ready to bring our industrial experience, passion, and perspectives to the Millicom board.” While we have been disappointed in certain operational missteps and capital allocation decisions at the company, we think that Niel’s positive presence will make the future different than the recent past.

- Warner Bros. Discovery ( WBD ) - Media conglomerate Warner Bros. Discovery was a top detractor in the quarter but remained a top contributor for the first half. After a strong first quarter, the stock price faltered in the face of near-term uncertainty around the re-launch of streaming service Max. Additionally, the big budget movie The Flash has not been a success. Finally, there was well-publicized drama around CNN management, with CNN CEO Chris Licht leaving the company after only one year, which we believe was a positive resolution. The company remains dramatically undervalued today, and management continues to make positive operational progress to drive free cash flow ((FCF)) growth. We believe this company has seen the worst so will be less leveraged and more strategically positioned in the quarters and years to come. Its underlying holdings are high-quality businesses that will drive FCF per share growth while also being attractive acquisition candidates.

Portfolio Activity

Portfolio activity was higher than usual in the first half with ten new positions, five exits, and multiple active trims and additions throughout the year in the face of increased market volatility and team productivity. We initiated four new positions in the second quarter - one in a US Health Care company that we are still building and will discuss in more detail next quarter. We also started buying a new investment post-quarter that gets most of its value from Asia. Our other year-to-date purchases range from French testing laboratories company Eurofins Scientific ( ERFSF ), which services the pharmaceutical, food, environmental, agriscience, and consumer products industries but is currently lapping some temporary headwinds; to consumer staples company Kellogg ( K ), which plans to spin off its eponymous cereal business (which accounts for less than 20% of our appraisal value) to focus on its high-quality and growing snacks business; to Entertainment company Live Nation, discussed in more detail above; to toy company Hasbro ( HAS ), which we have followed as a direct competitor to existing holding Mattel ( MAT ) and finally had the opportunity to purchase at a discount; to a combined holding in Fiserv ( FI ) and Fidelity National Information Services ( FIS ), purchased in the wake of the first quarter banking crisis; to Fortune Brands ( FBIN ), a large conglomerate that has strategically slimmed down to a high-quality owner of plumbing and other housing-related businesses.

We exited second-time holding Alphabet ([[GOOG]], [[GOOGL]]) and long-term position Lumen in the quarter. After successfully owning Alphabet from 2015 to 2020, we purchased the company again in 2022 as tech stocks broadly faced weakness. Alphabet was especially punished due to fears of increased competition entering the AI space, and we felt those worries were overdone. This market narrative quickly flipped in our roughly one-year holding period with Alphabet now being viewed as a likely AI winner, and we sold the position at a gain as the share price re-rated and the market was now overlooking a worse competitive and regulatory outlook.

We sold our remaining position in Lumen, after reducing our position in the first quarter when it became clearer the new management team under CEO Kate Johnson would not pursue a strategic path to monetizing Lumen’s consumer business. At their first analyst day in early June, new management presented disappointingly weak financial targets and significant further spending without a clear path to revenue growth. Throughout our holding period, we saw bond market pricing holding up and supporting our case for the strength of Lumen’s balance sheet, but in the second quarter, this reversed with bond prices becoming overly distressed. We lowered our appraisal as our outlook for the company deteriorated, leading to a full exit in the quarter. Lumen represented a permanent capital loss for the Fund, a significant opportunity cost for the portfolio, and a disappointing long-term mistake. Lumen has reinforced the importance of limiting overweight positions in the portfolio, being cautious of leverage and value declines, and fully re-underwriting a case – and being willing to move on - when the people and/or underlying facts change.

The higher-than-average portfolio activity YTD reflects the continued improvement in our process and the productivity of the team, with the proceeds of our trims and sales going to fund new opportunities with a better margin of safety and significant potential upside.

Outlook

The Fund delivered a strong first half, despite significant relative macro headwinds, and with materially different return drivers than the index. We believe this positions the Fund to deliver differentiated future returns. The research team has been busy evaluating existing holdings and identifying new opportunities, resulting in upgrades to the portfolio. Our management teams have been similarly busy, taking steps to get the underlying value of their businesses recognized. Following a period of high-teens returns, the portfolio ended the quarter with a compelling price-to-value (P/V) ratio in the mid-60s%, indicating significant future potential upside.

Important disclosures

Before investing in any Longleaf Partners Fund, you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. For a current Prospectus and Summary Prospectus, which contain this and other important information, visit https://southeasternasset.com/account-resources. Please read the Prospectus and Summary Prospectus carefully before investing.

RISKS

The Longleaf Partners Global Fund is subject to stock market risk, meaning stocks in the Fund may fluctuate in response to developments at individual companies or due to general market and economic conditions. Also, because the Fund generally invests in 15 to 25 companies, share value could fluctuate more than if a greater number of securities were held. Investing in non-U.S. securities may entail risk due to non-US economic and political developments, exposure to non-US currencies, and different accounting and financial standards. These risks may be higher when investing in emerging markets.

The FTSE Developed Index is a market-capitalization weighted index representing the performance of large and mid-cap companies in Developed markets. The index is derived from the FTSE Global Equity Index Series ((GEIS)), which covers 98% of the world’s investable market capitalization.

P/V (“price to value”) is a calculation that compares the prices of the stocks in a portfolio to Southeastern’s appraisal of their intrinsic values. The ratio represents a single data point about a holding and should not be construed as something more. P/V does not guarantee future results, and we caution investors not to give this calculation undue weight.

“Margin of Safety” is a reference to the difference between a stock’s market price and Southeastern’s calculated appraisal value. It is not a guarantee of investment performance or returns.

Operating Cash Flow ((OCF)) measures cash generated by a company’s normal business operations.

Free Cash Flow ((FCF)) is a measure of a company’s ability to generate the cash flow necessary to maintain operations. Generally, it is calculated as operating cash flow minus capital expenditures.

EBITDA is a company’s earnings before interest, taxes, depreciation and amortization.

As of June 30, 2023, the top ten holdings for the Longleaf Partners Global Fund: CNX Resources, 6.3%; EXOR, 6.2%; IAC, 6.1%; FedEx, 6%; Prosus, 5.4%; Affiliated Managers Group, 5.3%; Undisclosed, 4.8%; Warner Bros Discovery, 4.8%; MGM Resorts, 4.6% and Live Nation, 4.6%. Fund holdings are subject to change and holdings discussions are not recommendations to buy or sell any security. Current and future holdings are subject to risk.

Funds distributed by ALPS Distributors, Inc.

LLP001444

Expires 10/31/2023

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Longleaf Partners Global Fund Q2 2023 Commentary