LUGDF - Lundin Gold: Another Blowout Quarter

2023-08-22 13:24:04 ET

Summary

- Lundin Gold has revised its FY2023 guidance higher, increasing its gold production outlook and lowering its cost guidance.

- Meanwhile, the company continues to strength its balance sheet with a record quarter of free cash flow generation, giving it the flexibility to diversify (M&A) and ramp up exploration.

- In this update, I'll dig into the recent results and the valuation and see whether the stock is offering a low risk buy point after its ~20% correction.

Just over six weeks ago, I wrote on Lundin Gold (LUGDF), noting that while the company had released more blowout production results from its Fruta del Norte Mine and was tracking ahead of guidance, the stock did not offer enough of a margin of safety to justify paying up for the stock above US$12.30. This was because the stock was trading at one of the highest P/NAV multiple sector-wide despite being a single-asset producer (higher-risk), and while the company deserved a premium given its incredible operational execution, multiples were trending lower sector-wide and the company had a softer H2 on deck with H1 much stronger because of the benefit of front-end weighted production and modest sustaining capital spend.

Earlier this month, Lundin Gold released its Q2 financial results and while the solid performance was not surprising given the pre-released production figures, the company surprised the market with a material FY2023 guidance revision, increasing its outlook to 450,000 to 485,000 ounces of gold (450,000 ounce guidance midpoint previously) while also lowering its cost guidance. This has placed the company in rare air among its peer group that had a tough H1 overall, with a major strike, illegal blockades, and wildfires/power outages that impacted production for Canadian miners. Let's take a look at Lundin's results below and whether the recent correction has built in enough margin of safety.

All figures are in United States Dollars unless otherwise noted.

{kind=link}

Production & Sales

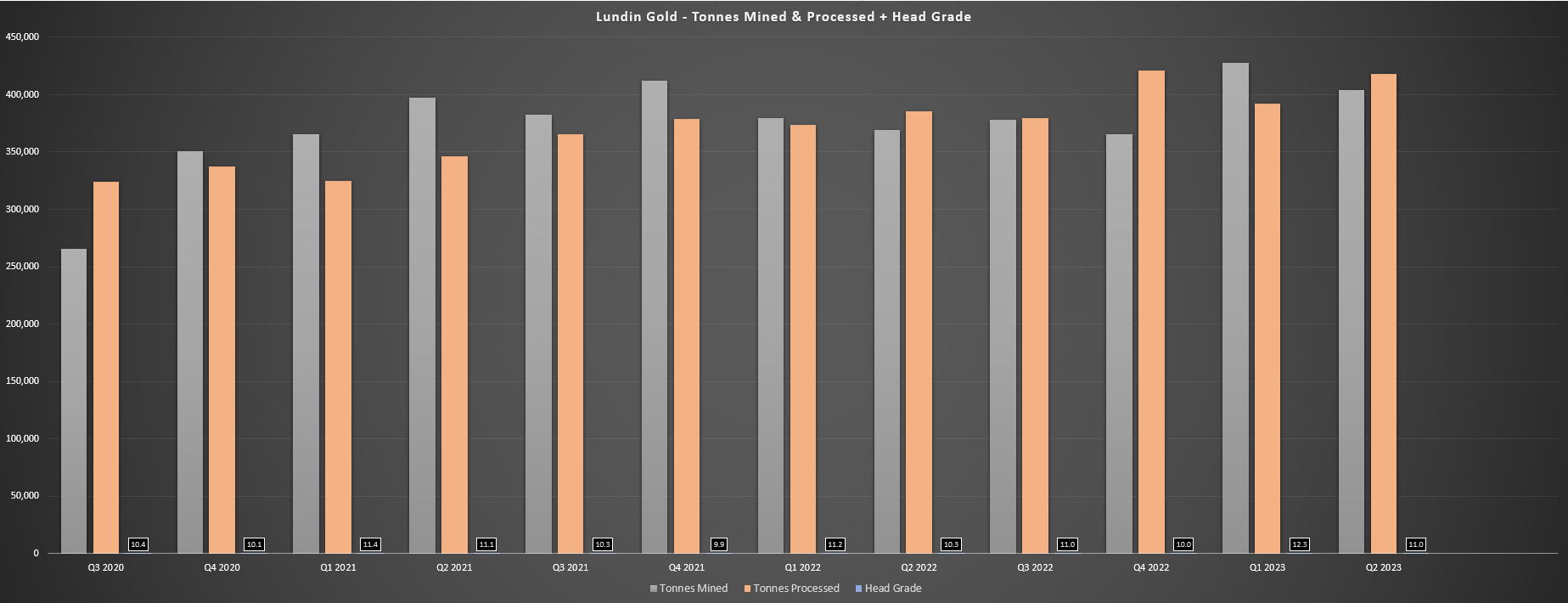

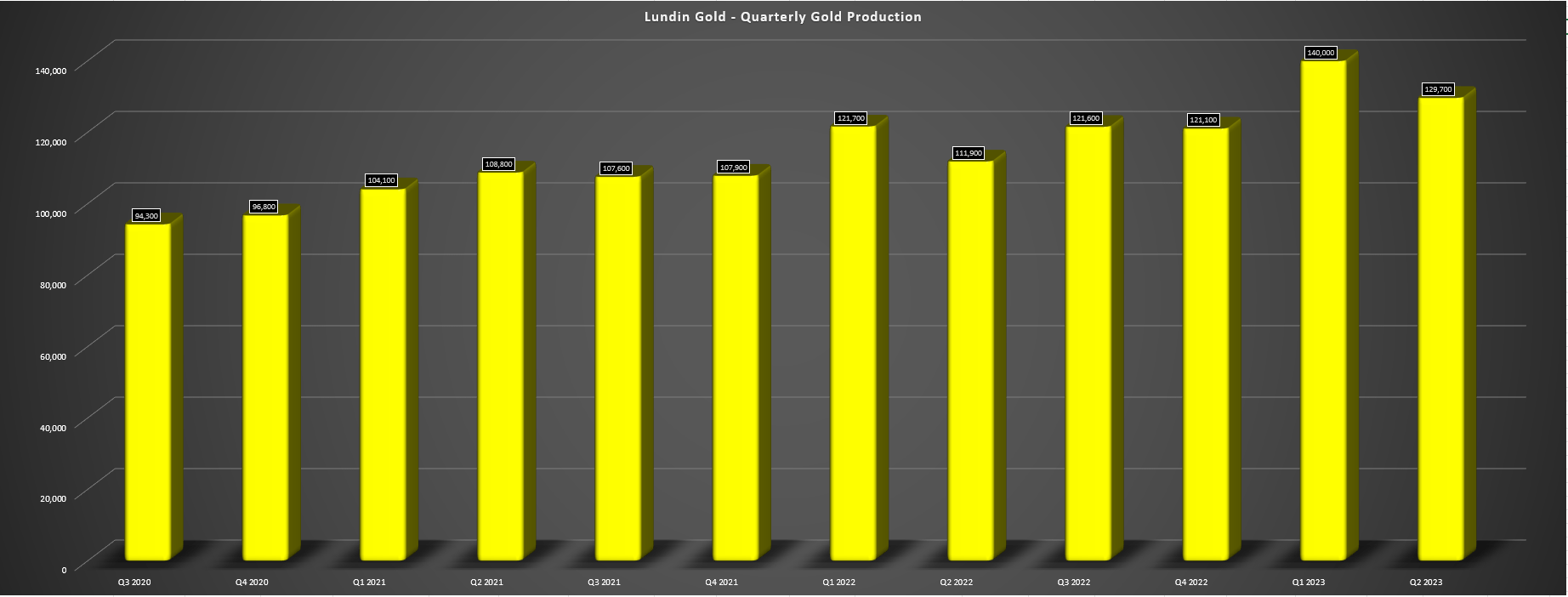

Lundin Gold released its Q2 results earlier this month, reporting quarterly production of ~129,700 ounces of gold, a 16% increase from the year-ago period. The increased production was driven by higher throughput and grades with the benefit of high-grade stockpiles from Q1 topping up the plant, evidenced by ~418,400 tonnes processed at 11.0 grams per tonne of gold, up from ~385,700 tonnes in Q2 2022 at 10.3 grams per tonne of gold. In fact, head grades in the quarter came in 33% above reserve grades of 8.7 grams per tonne of gold, which not surprisingly led to a monster quarter from an operational and financial standpoint.

Lundin Gold - Quarterly Tonnes Mined, Tonnes Processed & Feed Grade (Company Filings, Author's Chart)

{kind=link}

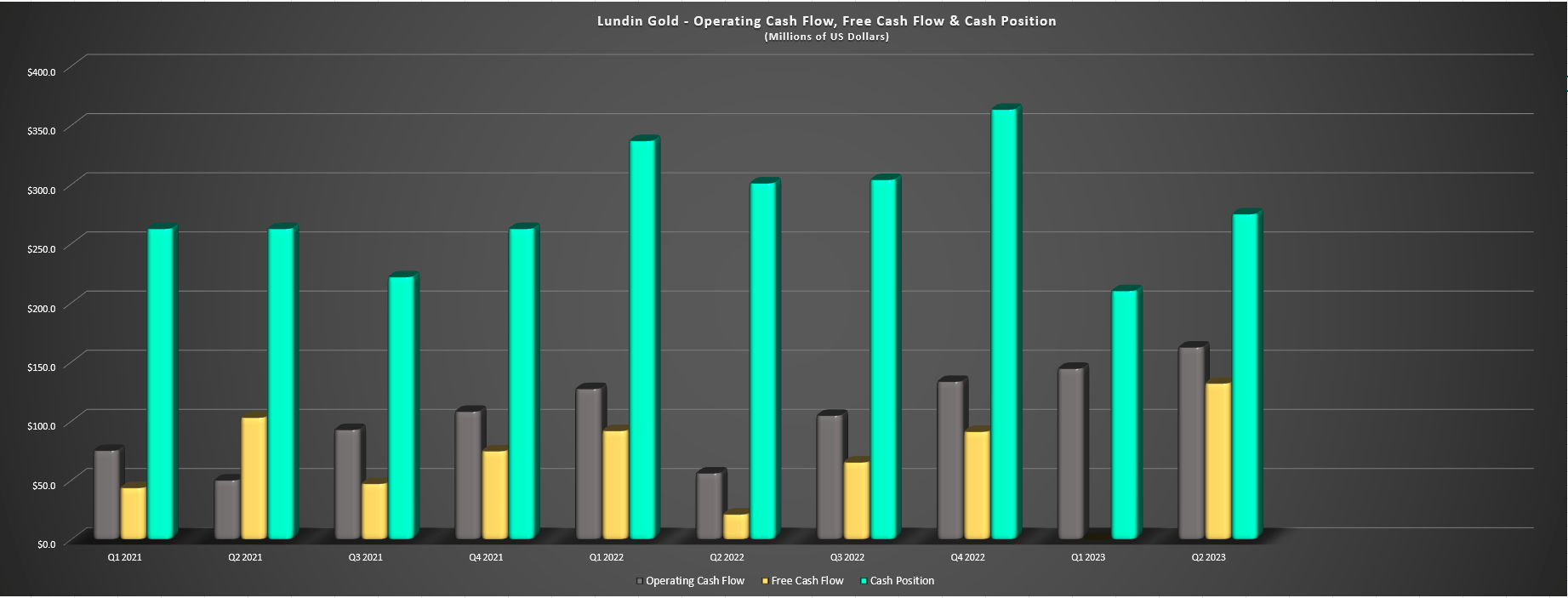

Digging into the chart below, we can see that this was the second best quarter for the company since beginning production at Fruta del Norte in 2019, and it's pushed year-to-date production to ~269,400 ounces of gold, tracking well ahead of the initial guidance midpoint of ~450,000 ounces. This prompted the company to raise its guidance to 450,000 to 485,000 ounces (~468,000 ounce mid-point), which has also positively impacted its cost guidance, which was revised to $845/oz at the mid-point, ~37% below the estimated industry average of ~$1,360/oz in FY2023. Meanwhile, revenue soared to ~$243.9 million (+37% year-over-year) because of higher sales volumes and the near-record average realized gold price, while operating cash flow improved to $162.4 million and free cash flow surged to a record of $131.9 million (~54.1% free cash flow margin).

Lundin Gold - Quarterly Gold Production (Lundin Gold - Quarterly Gold Production - Company Filings, Author's Chart) Lundin Gold - Operating Cash Flow, Free Cash Flow & Cash Position - Company Filings, Author's Chart

{kind=link}

{kind=link}

Costs & Margins

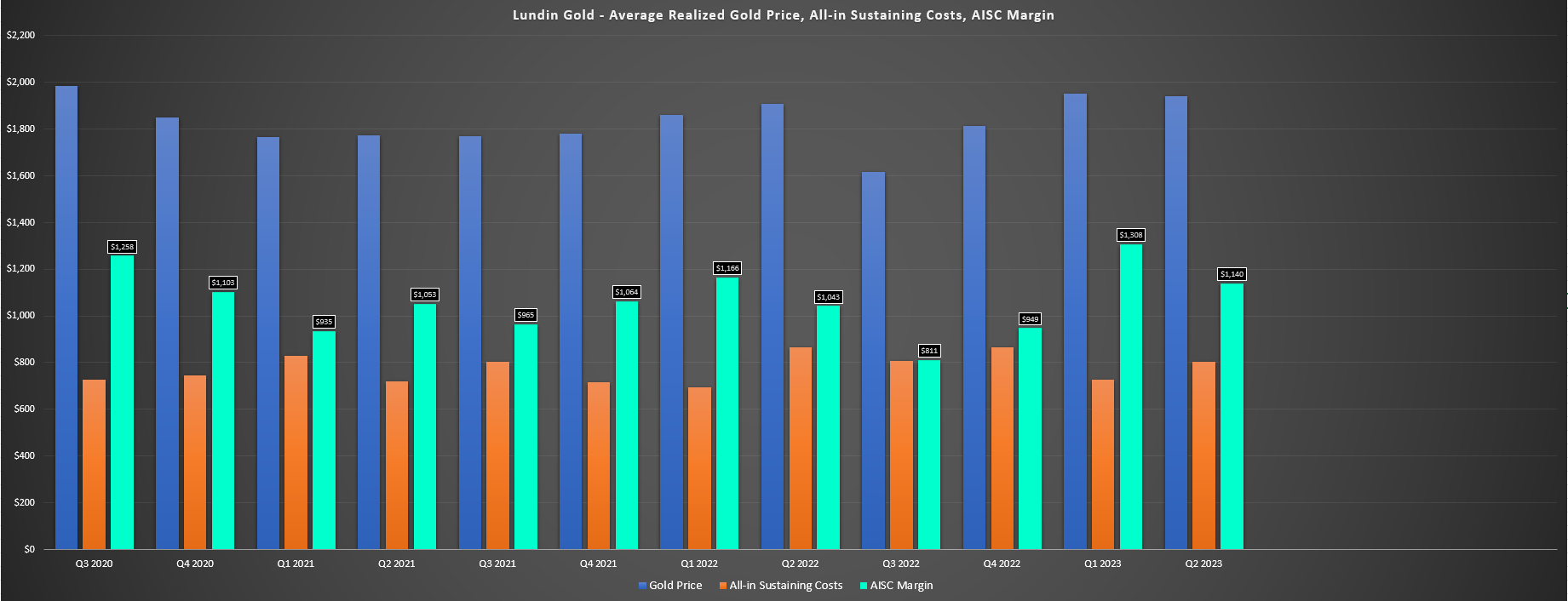

Moving over to costs and margins, Lundin Gold reported industry-leading cash costs of $644/oz and all-in sustaining costs [AISC] of $802/oz, with AISC down 7% year-over-year despite higher sustaining capital spend in the period. The lower AISC benefited from easy comps due to fewer ounces sold than produced in the year-ago period, the relatively low inflation rates in Ecuador, and the increased production volumes. These costs translated to AISC margins of $1,140/oz, up 9% year-over-year and beating my previous estimates of $1,100/oz, which assumed slightly higher sustaining capital spend and production closer to ~120,000 ounces. This solid performance has placed year-to-date AISC at $765/oz, which certainly explains why the company reeled in its AISC guidance to $820/oz to $870/oz in its Q2 results.

Lundin Gold - AISC, AISC Margin, Gold Price - Company Filings, Author's Chart

{kind=link}

While this is certainly positive news for 2023, which is expected to be more robust than initially guided, and Lundin is now sitting with a cash balance of ~$275 million despite the full repayment of its gold prepay ($208 million) earlier this year. It is worth noting that the H2 will be much softer than H1. This is because we could see a slight dip in plant throughput in Q3 vs. Q2 because of the planned SAG mill liner change, and grades and recoveries should normalize and come in closer to 9.4 grams per tonne of gold, in line with grades in the 2022 TR, management comments that it will be processing ore from areas with less favorable geology, and not having access to high-grade stockpiles like it did last quarter. This should translate to production closer to ~220,000 ounces in H2, which would beat the top end of guidance (~490,000 ounces vs. ~485,000 ounces) but translate to a meaningful dip in H2 production vs. H1.

And while the company will still report industry-leading AISC figures as implied by its guidance, production was front-end weighted this year with back-end weighted sustaining capital, and the potential that we could see sustaining capital come in at or above the top end of FY2023 guidance ($45 million to $55 million) due to accelerated underground development. So, assuming $55 million in sustaining capital, sustaining capital of $17.6 million year-to-date is sitting at just ~32% of annual guidance, which will lead to a spike in H2 AISC. As noted, this is hardly material, as Lundin Gold will still be an ~$850/oz producer with ~55% AISC margins. Still, investors expecting a similar H2 performance to H2 2022 (~243,000 ounces at sub $840/oz) could be disappointed.

Valuation

Based on ~242 million fully diluted shares and a share price of US$11.60, Lundin Gold trades at a market cap of ~$2.78 billion and an enterprise value of ~$2.90 billion, making it the highest valued single-asset producers in the market today. However, while this might seem extreme vs. names like Victoria Gold (VITFF) and Centamin PLC (CELTF), this is mostly justified, with Fruta del Norte being near unrivaled from a grade and scale standpoint among other mines sector-wide (480,000+ ounces at sub $850/oz AISC), making it a free cash flow machine. That said, while Guerrero State, Mexico is no Loja, Ecuador, Torex Gold is one single-asset producer that will also generate significant free cash flow in FY2025 that trades at well below half of Lundin Gold's enterprise value, and is certainly becoming more attractively valued from a relative value standpoint.

Assigning a fair multiple of 1.1x P/NAV and 9.0x FY2024 cash flow estimates and using a weighted valuation of 65% assigned to P/NAV and 35% assigned to P/CF, Lundin Gold's fair value comes in at US$14.65. This fair value estimate points to a 13% upside from current levels, but I prefer to bake in a significant margin of safety for precious metals producers when starting new positions. This is because these are risky and volatile stocks with depleting assets that do not have pricing power and are at the mercy of the gold price, and while we've seen only positive surprises to date from Lundin Gold, the odd negative surprise does come along. For this reason, I require a minimum 35% discount to fair value to justify buying single-asset producers, which carry higher risk, even if they benefit from incredible ore bodies. After applying this required discount, Lundin Gold's ideal buy zone comes in at US$9.50 or lower.

Summary

Lundin Gold put up another exceptional quarter in Q2 and has continued to over-deliver on its promises with an unparalleled track record of beats and raises relative to its peers over the past couple of years, with its only peer in this regard being Orla Mining ( ORLA ), the lowest-cost gold producer sector-wide. That said, LUGDF may be a free cash flow machine, but the market has priced some of this into the stock following its significant outperformance, with it trading at ~9.0x EV/FCF estimates, a very reasonable valuation but not a valuation that offers an extreme margin of safety which is what I prefer to make new investments. So, while I see LUGDF as a Buy if it hits US$9.50 before year-end, I continue to see more attractive bets elsewhere in the sector.

For further details see:

Lundin Gold: Another Blowout Quarter