CA - Lundin Mining: Difficult Near-Term Outlook For Copper Strong Headwinds For Shares (Rating Downgrade)

2023-11-03 06:03:22 ET

Summary

- Lundin Mining Corporation's recommendation rating has been downgraded to "Sell" due to a weakened near-term outlook for copper prices.

- The risk of an economic recession and lower demand for copper are expected to negatively impact the company's stock price.

- Investors may want to consider selling shares and taking profits before a potential sharp decline in the stock price.

A Sell Rating for Lundin Mining Corporation

This analysis downgrades the recommendation rating on Lundin Mining Corporation shares (LUNMF) ( LUN:CA ) to "Sell" from the previous rating of "Hold" as the near-term outlook for copper prices has weakened due to the risk of an economic recession expected to weigh heavily on demand for the red metal.

It was previously rated Hold for the following reason: It was believed that the mere concerns about the recessionary effects of a restrictive interest rate policy could provide an opportunity to expand positions in Lundin. Lower valuations for Lundin Mining shares would have been possible as investors expected the Fed's hawkish stance to be quite damaging to copper demand.

But at the same time, there was also a consensus on financial platforms that a soft landing was the most likely scenario, which would have kept the worst consequences for the economy and markets at bay while the Fed fulfilled its inflation mission.

Therefore, it was recommended to wait for lower valuations to strengthen the position as Lundin's mining operations can benefit from the significant growth potential of copper as a key metal for electrification projects, but these are now generally postponed due to high financing costs.

With Copper's Near-Term Outlook Looking Bleaker, Investors May Want to Consider Taking Profits Now

Unfortunately, conditions have deteriorated dramatically since then, as the erosion of US household purchasing power affects consumption and investment, while Israel's unexpected Gaza crisis has exacerbated the situation, meaning the downside risks are now much greater than just a few weeks ago.

Copper is used in many everyday products. Therefore, subdued consumption and postponement of business investments will translate into lower demand for the red metal, negatively impacting the price per pound.

In such a scenario, there is no prospect of a copper price recovery, but a sustained decline that would cause the market price of Lundin Mining shares to fall has a strong chance instead. A shock to the US economy could also halve the stock's market price, as it did, for example, after the outbreak of the COVID-19-induced pandemic in March 2020.

Some may argue that the shock the cycle may experience this time is economic in nature and therefore has a different impact on the market price of securities than the disruption caused by the COVID-19-induced health crisis. But in the wake of the 2008 financial crisis, an example of an economic shock instead, Lunding Mining's share price fell below $1.

Although the 2008 financial crisis could not have as immediate an impact on copper demand as what is about to emerge now as a downturn in the business cycle, the headwinds in the copper markets were still felt strongly, plunging Lundin Mining Corporation's stock price into depression.

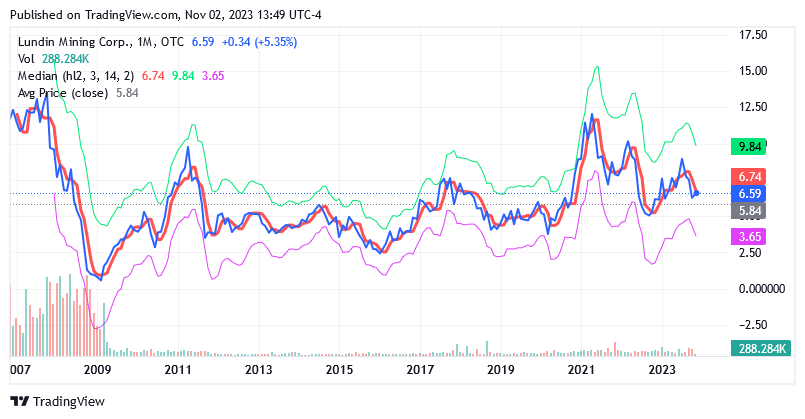

While the share price of $6.59 is currently not low compared to the median price of $6.74 and compared to the average price of $5.84 calculated over the last 17 years, there are headwinds in the home stretch to deal with, and these appear to be quite strong.

{kind=link}

Therefore, retail investors should consider the opportunity to take some profit from their investment in Lundin Mining Corporation shares before a sharp decline sets in.

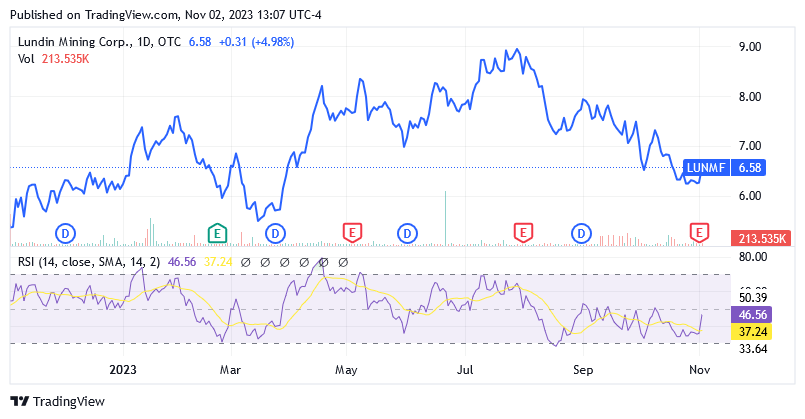

Shares of LUNMF stock were trading at $6.58 apiece as of this writing, giving it a market cap of $4.83 billion. Shares are trading below the 200-day simple moving average of $7.33 and below the 50-day simple moving average of $7.11.

However, due to the gloomy outlook for copper, the main commodity produced and traded by Lundin Mining, the fact that shares are trading lower than technical trends does not imply a different rating than a Sell rating suggested by this analysis.

{kind=link}

Furthermore, a 14-day relative strength indicator of 46.56x, which is still far from the oversold level, suggests that there is plenty of room for shares to fall sharply from current levels under the negative pressure of the "higher for longer" interest rate policy of the Fed.

{kind=link}

And then readers should also note that there is a possibility of another Fed rate hike before the end of this year or early 2024, which would increase unfavorable macroeconomic and geopolitical conditions for this stock.

The same considerations are applied to the stock traded on the Toronto Stock Exchange.

Shares of Lundin Mining Corporation under the LUN:CA symbol are trading at CA$9.00 apiece as of this writing, below the 200- and 50-day simple moving averages of CA$9.88, and CA$9.71, respectively. Shares are also trading below the middle point of CA$ 9.575 in the 52-week range of CA$ 7.22 to CA$ 11.93. The stock has a market cap of CA$ 6.70 billion.

The stock under the symbol LUN:CA has a 14-day Relative Strength Indicator of 46.

About Lundin Mining Corporation in the Third Quarter of 2023

As a base metal producer based in Toronto, Canada, Lundin Mining Corporation has a diversified portfolio from a geographic perspective, with mineral operations located in Latin America, the United States, Portugal, and Sweden, but also from a commodity perspective. In addition to copper, the company also processes zinc, nickel, and gold.

However, copper is the main source of income for Lundin Mining, and following the acquisition of 51% of SCM Minera Lumina Copper Chile in July 2023, Lundin's mineral holdings in the world's largest copper producer Chile are now also responsible for the development of Caserones open pit copper mine and molybdenum mine, so that approximately 75% of the company's total red metal production consists of Chilean copper.

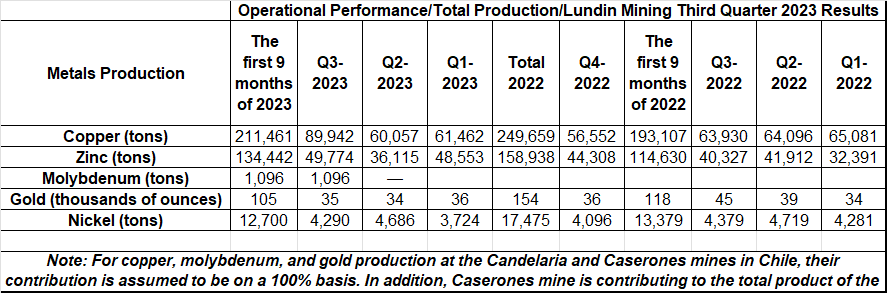

For the third quarter of 2023, the results of which the company announced after regular market hours on Wednesday, November 1, 2023, Lunding Mining's production was as follows.

Copper production on a consolidated basis was 89,942 tonnes of the metal, which the company said was a "new quarterly record". As well a record was quarterly zinc production of 49,774 tonnes, while nickel and gold production totaled 4,290 tonnes and 35,000 ounces, respectively.

Based on average market prices in the third quarter of 2023, the production of copper accounts for three-quarters of total revenue, while molybdenum, zinc, gold, and nickel together account for the remaining 25%.

Copper production, which stood at 211,461 tonnes in the first nine months of 2023, increased by 9.5% year-on-year, but it includes the Caserones mine that started contributing to the company's total production since its acquisition in July 2023.

Source of data: Lundin Mining Corporation Q3-2023 Earnings Report

{kind=link}

Copper production in the third quarter of 2023 was 49.8% higher sequentially and 40.7% higher year-over-year. However, these growth rates were influenced by the inclusion of Caserones production from mid-July 2023.

Attributable copper production by region: Overall, there are weaknesses in key operating parameters

In terms of attributable production, as Lundin Mining owns 80% of the Candelaria mine and 51% of the Caserones mine, Chilean copper totaled approximately 44,978 tonnes in Q3-2023, including some tonnes of Caserones' pre-acquisition production.

Candelaria's lower grades impacting its Q3-2023 production year-over-year were offset by its and Caserones' higher throughput and by Caserones' higher recoveries.

Brazilian copper production from the 100% owned Chapada mine was 12,286 tonnes of copper, which was lower year over year due to a combination of lower throughput and grades.

Lundin Mining Corporation's fully owned Eagle Mine, an underground nickel-copper mine in the Upper Peninsula of Michigan, USA, produced 3,245 tonnes of copper, but it was impacted by lower planned grades and therefore the third quarter output went down year-on-year.

Lundin Mining Corporation's 100% Neves-Corvo mine, an underground copper-zinc mine in Castro Verde, Portugal, produced 9,016 tonnes of copper in the third quarter of 2023, up year-on-year, as the mine benefited from higher throughput, ore grade, and recovery rates.

Lundin Mining Corporation's 100% owned zinc/lead/copper/silver Zinkgruvan underground mine in Sweden produced 1,299 tonnes of copper in the third quarter of 2023, below the prior-year figure due to lower throughput.

Secondary production is also affected by the same problems with lower grades and throughput, mainly, causing this negative development on an annual basis:

· first nine months' gold fell 11% and third quarter gold fell 22.2%.

· first nine months' nickel fell 5.1% and third quarter nickel fell 2%.

Instead, the production of zinc increased by 17.3% and 23.4% in the first 9 months and the first quarter of activities, respectively, but the improvement is the result of the expansion of mining and processing operations in Portugal.

The costs are rising:

Lower grades and lower throughput rates are having a negative impact on production and cash costs, which increased on a year-over-year basis. Negative trends in costs were also observed in the previous quarter , when Caserones was not part yet of the company's portfolio:

· year-over-year production costs increased 44.5% to $615.1 million in Q3-2013.

· year-over-year cash costs increased 46.6% to $401.4 million in Q3-2013.

· year-over-year production costs increased 18.80% to $1.44 billion in the first 9M-2023.

· year-over-year cash costs increased 28.2% to $993.81 million in the first 9M-2023.

The price of copper, which along with sales volumes drives at least ¾ of the company's profitability, rose 8.2% year-over-year to average $3.7936 per pound in the third quarter of 2023 but declined year-over-year by 5.2% to an average of $3.9025 for the first 9 months of 2023.

The price of copper: a key factor for Lundin Mining's profitability

Caserones has undoubtedly delivered an excellent performance, but without the year-on-year improvement in copper prices in Q3 2023, the positive dent observed in profitability - as measured by the adjusted EBITDA measure - from Q2-2022 to Q2-2023 could hardly be achieved, also because the cost pressure was quite significant.

Source of data: Lundin Mining Corporation Q3-2023 Earnings Report

The development of the copper price is fundamental to the profitability of Lundin Mining Corporation. So , despite the Caserones volumes in the third quarter of 2023, the EBITDA margin in the first nine months of 2023 is still lower than the previous year, which was due to the lack of positive support from the copper price, as this, instead, weakened.

Higher realized copper prices enabled a revival in free cash flow performance, resulting in an inflow of $71.1 million in the third quarter of 2023, following an outflow of $163.2 million in the third quarter of 2022. In the first nine months instead, the partial Caserones' contribution failed to prevent a free cash outflow of $47.7 million in 2023 compared to an inflow of $158.3 million in 2022.

The 9-month trend is certainly influenced by expansionary capital spending, for which $234.8 million was allocated in 2023, up from $126.5 million in 2022, although it has to be said that even with a budget of the same amount the free cash inflow would still have been 60% lower than in the 9 months of 2022.

The financial condition

The company is going through a very challenging period and has a balance sheet that is heavily leveraged, with cash and cash equivalents at $357.3 million and debt at $1,516.2 million as of September 30, 2023.

This balance sheet situation increases the risk associated with investing in Lundin Mining stock, as the stock has an Altman Z-Score of 1.62 (scroll down to the Risk section on this page of Seeking Alpha ) and is currently potentially at risk of bankruptcy within a few years. The reader must also be aware of this.

This balance sheet shows that the company still pays a quarterly cash dividend of CA$0.090 per common share, but objectively the low amount paid and the volatility to which the payment is exposed do not make the dividend the reason why Lundin shares Mining are traded on the stock exchanges.

The Outlook: Production, Costs, CapEx, Copper Price, and Demand

Looking ahead, the company slightly increased full-year 2023 copper production guidance, the midpoint of the interval more than anything else, to 305,000 to 325,000 tons from 296,000 to 325,000 tons according to the previous range.

Cash costs for Caserones and Eagle are expected to be lower due to higher production volumes combined with higher by-product credits, but the 80% interest in Candelaria is likely to weigh on the profitability of the business through higher operating costs. And that's not exactly encouraging news, considering that Candelaria mine accounts for the majority of the company's total copper production, outstripping Caserones and Eagles combined by more than double.

Additionally, the company lowered its investment forecast for its mineral projects in Portugal and Sweden by $30 million. As with many other companies, the current environment of high borrowing costs is likely to be the reason for the decision of Lundin Mining Corporation to reduce expansionary capital expenditures.

But even with the planned reduction in CapEx for the portfolio in Portugal and Sweden, total capex in the last quarter of 2023 will be higher subsequently and compared to the quarterly average for the first nine months of 2023. That does not stimulate free cash inflow in the near term, with the potential impact on shares being felt in early 2024 when the next results are released.

Regarding copper price prospects, the valuation will be affected by the economic recession, which, according to economists and the inverted yield curve for US government bonds, will occur as early as 2024. In the sense that a downturn requires a sustained decline in consumption (almost 70% of GDP ), and this negative trend will certainly be reflected in subdued demand for copper, from which most of the products that American households use every day are made.

Economists predicting an economic recession include:

Michael Pearce , chief US economist at Oxford Economics, Chryssa Halley , chief financial officer of the US Federal National Mortgage Association (Fannie Mae), and David Rosenberg , economist at Rosenberg Research. Most recently, former US Treasury Secretary Larry Summers believes that a soft landing is unlikely, but a recession will instead come as early as 2024 as the next business cycle.

Finally, Luke Tilley , chief economist at Wilmington Trust, says the US economy is not recovering but slowing down, which will become clear to everyone, and thus he is implicitly pointing to an economic recession.

The U.S. Treasury's inverted yield curve has correctly predicted an economic downturn seven out of eight times over the past 58 years. Now it still suggests a recession as a one-year yield of 5.391% is higher than a ten-year yield of 4.665%, but under normal conditions, the opposite is instead true.

Source: GuruFocus

A significant slowdown in GDP growth could incubate under signs of faltering consumption, and China does not need copper at the moment

Non-performing loans and asset write-offs continue to rise , leaving more consumers struggling to make ends meet. That means U.S. households could soon be forced to make drastic decisions in allocating their budgets between goods and services purchases.

Also, when it comes to copper demand, the contribution of China's real estate sector, a key absorber of this base metal, is missing at the moment as the sector - a mainstay of China's faltering economy - is in major problems. The economy of the Asian country and the world's largest copper consumer is now paying an expensive bill for the financial woes of China Evergrande Group (EGRNQ) and Country Garden Holdings Company Limited (CTRYF) (CTRYY), as these major real estate companies cannot meet their offshore obligations, undermining the creditworthiness of an entire industry.

As a result of all this, demand for copper is already likely to be falling, as inventories of the red metal on the Shanghai Futures Exchange and the London Metal Exchange appear to be declining significantly.

Conclusion

In the medium to long term, Lundin Mining shares should benefit from a business poised to capitalize on the significant growth potential of copper as a key metal for electrification projects.

However, the near-term outlook has become much bleaker due to the increased risk of an economic recession, which is also gaining momentum as "higher for longer" interest rates combined with elevated core inflation weigh on consumption (or 70% of US GDP).

The deterioration in consumption could hit the demand for copper in a remarkable way because the basic metal is used in several products that people use on a daily basis. Support is also currently lacking from China, the world's largest copper consumer, due to the crisis in its main buyer, the real estate market.

Weaker demand and sluggish economic growth in China already appear to be reflected in negative momentum for copper as inventories shrink significantly. In such a situation, there is no point in increasing supply, as prices fall or remain subdued at best, and investment in future production is currently too expensive.

The darker outlook for copper in the near term will weigh on Lundin Mining's business, whose profitability is challenged by weakness in some key operating parameters and rising costs.

Shares in Lundin Mining, which are highly correlated with copper as the company's revenue depends on it for at least 75%, have a high risk of trading much lower than currently. Investors may want to consider the idea of selling some shares and taking some profit from their investment.

This stock price is cyclical, just like the commodities being traded. There will come a time to reintegrate the position in this stock for a strategy that seeks to gain exposure to the benefits of copper as a key element in the energy transition through increased electrification.

For further details see:

Lundin Mining: Difficult Near-Term Outlook For Copper, Strong Headwinds For Shares (Rating Downgrade)