META - LVS Advisory Q3 2023 Letter

2023-10-19 05:45:00 ET

Summary

- LVS Advisory is a boutique investment firm focused on providing active investment management services for individuals, families, and institutions. LVS Advisory LLC is a Registered Investment Adviser based in New York City.

- The Defensive Portfolio gained 4.4% in the first nine months of 2023, while the Growth Portfolio declined 2.4%.

- The S&P 500 may not be representative of the overall stock market, as most financial assets are flat to down for the year.

- A small number of large tech companies, known as the 'Magnificent 7', are driving the market's returns, while the rest of the market is struggling.

Dear Investors,

For the first nine months of 2023, the Defensive Portfolio gained 4.4% (net of all fees and expenses) and the Growth Portfolio declined 2.4% (net).

| Investment Results |

| Full Year 2019 |

| Full Year 2020 |

| Full Year 2021 |

| Full Year 2022 |

| YTD 2023 |

| Since Inception 1 |

| LVS Defensive Portfolio (net of fees) |

| 7.0% |

| 13.2% |

| 9.1% |

| 3.8% |

| 4.4% |

| 43.2% |

| Benchmark: High-Yield Bond Index |

| 13.4% |

| 5.0% |

| 4.0% |

| (11.4%) |

| 5.0% |

| 15.2% |

| LVS Growth Portfolio (net of fees) |

| - |

| 61.8% |

| 16.1% |

| (35.8%) |

| (2.4%) |

| 17.7% |

| Benchmark: S&P 500 Total Return Index |

| - |

| 18.4% |

| 28.7% |

| (18.1%) |

| 13.1% |

| 41.1% |

| Note: investment performance is presented net of all fees and expenses. Investment results are as of September 30, 2023. (1) LVS Defensive was incepted on January 1, 2019. LVS Growth was incepted on January 1, 2020. |

Are We Still In A Bear Market?

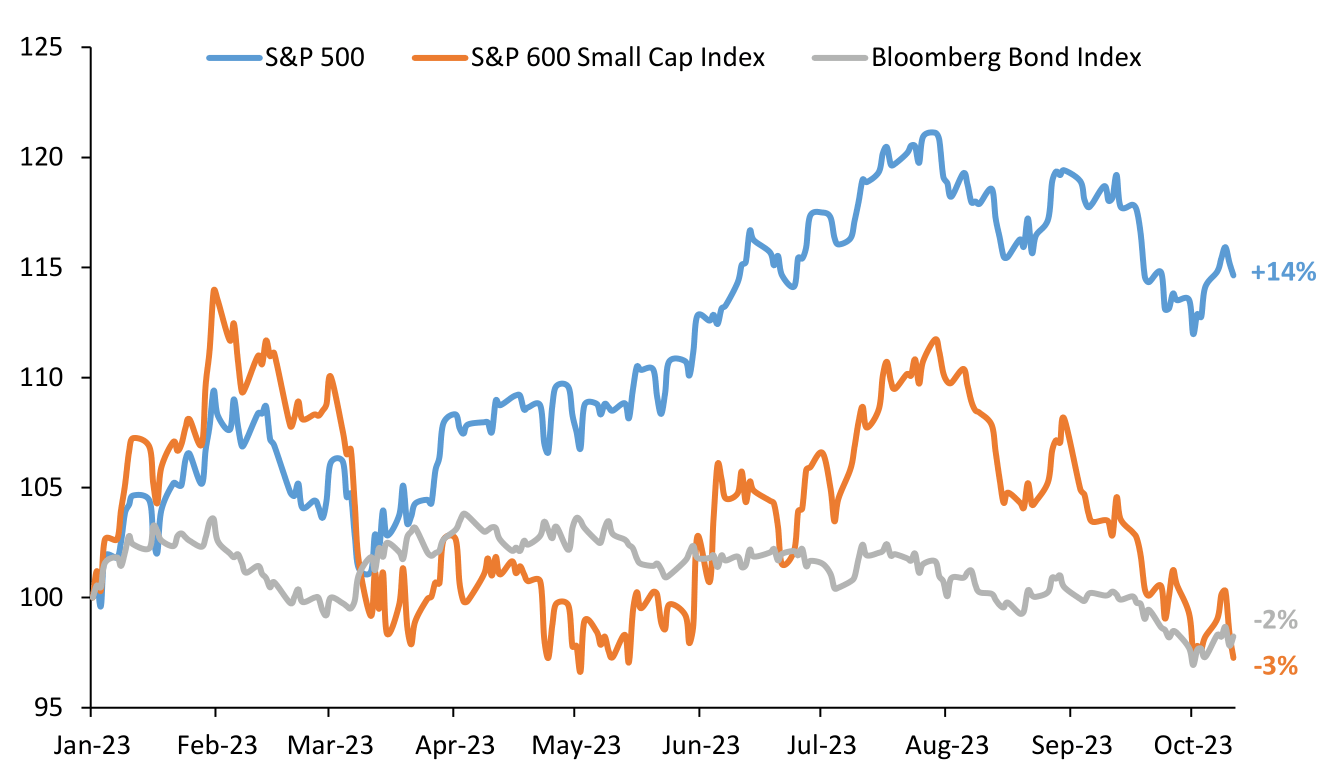

I have been reflecting on why the current investment environment feels so bleak despite the S&P 500 ( SP500 , SPX ) showing a positive return for the year. After some analysis, I concluded that the S&P 500 may not be the most representative index for stocks in 2023. Most financial assets are actually flat to down so far on the year. To illustrate, the chart below shows that while the S&P 500 is up 14% (as of 10/13/23), the benchmark small cap index is down 3%, and the benchmark bond index is down 2%.

{kind=link}

This is true of most asset classes I have looked up recently. US mid-cap stocks are flat for the year. European stocks are only modestly positive. Emerging market stocks are down. Most bond funds are down this year. Financial markets historian Niall Ferguson even noted that this is the worst bond market rout in 150 years.

More interesting is that the average stock in the S&P 500 itself is roughly flat so far in 2023, despite the index being up 14%! This can be observed by comparing the S&P 500 index to the equal-weighted version of the index.

{kind=link}

Why is this happening?

Boiling it down, a small number of companies with outsized weights in the S&P 500 are driving the entire market’s returns for the year. The financial press has picked up on this small group of companies and has named them the ‘Magnificent 7’.

The Magnificent 7 stocks are Apple ( AAPL ), Microsoft ( MSFT ), Google ( GOOG , GOOGL ), Amazon ( AMZN ), Nvidia ( NVDA ), META , and Tesla ( TSLA ). The obvious commonality is that this group is 100% made up of large technology companies.

I could get into why these large tech companies have appreciated but I think it is more revealing to ask why the rest of the market hasn’t participated. I believe most companies are still digesting the impacts of high inflation which has translated into higher input costs (raw materials, labor, and cost of capital) resulting in lower margins. Furthermore, when speaking with business leaders, most cite a cautious outlook, and many have curtailed investments in expansionary projects.

Investors have taken the cue and reduced their estimates for what companies will likely earn . According to Refinitiv , earnings per share for the S&P 500 is expected to grow just 2.3% in 2023, the lowest growth rate since 2020. A lack of earnings growth for public companies has directly translated into flat share price performance.

On the other hand, most of the large tech companies have benefited from increased investments in artificial intelligence, and investors seem quite eager to pay higher valuation multiples for the perceived quality and safety of these select companies.

Investing implications

To answer the question: yes, we are still in a bear market for most financial assets. I believe this is a good thing for investors today because it creates an attractive entry point for long-term owners.

The broader market did participate in the stock market rally during the first half of 2023 when it was believed that inflation was easing and an economic soft landing was achievable. Then the market gave it all back in Q3 on the reassessment that inflation would remain high and that the economy could soften.

If we have learned one lesson from the past two years, it is that attempting to predict the timing and magnitude of economic recessions is a futile exercise. It is more important to recognize that many stocks are attractive today relative to what they will earn through the cycle. Buying these assets when they are on sale will result in satisfactory investment returns. There is no need to overthink it.

A rising risk with index investing

The dynamic above also highlights a rising risk with investing in the S&P 500 index. If a small number of stocks can prop up the index returns, then a small number of stocks can also ruin the index returns. The S&P 500 is increasingly becoming reliant on a handful of large technology companies. If these companies on average were to underperform for whatever reason, then investors would be better off investing in other areas of the market.

Defensive Portfolio: Benefitting From An Index Rebalance

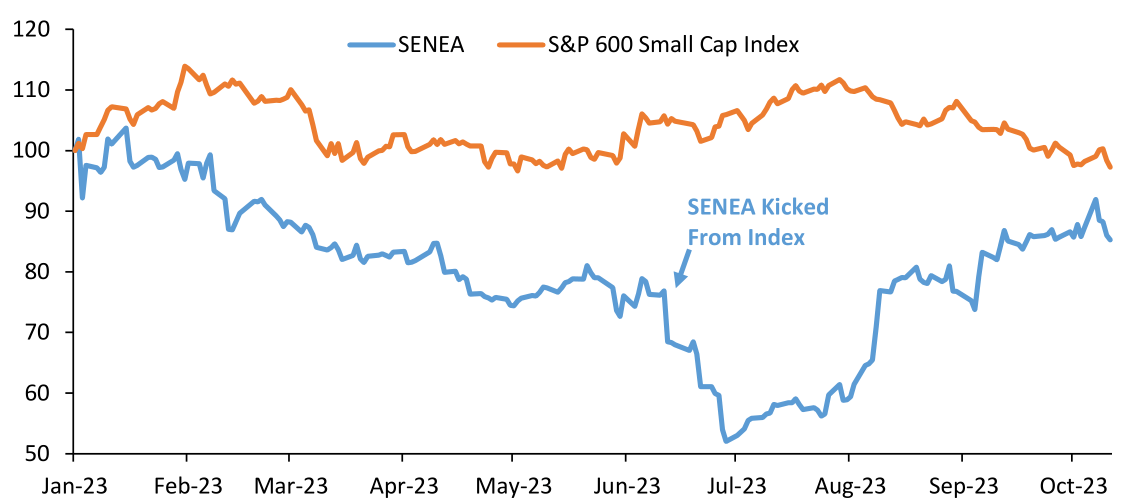

The third quarter was relatively quiet for the Defensive Portfolio. However, we did benefit from a technical trade around an index rebalance.

Seneca Foods ( SENEA ) is a consumer-packaged goods company that sells canned vegetables in the US. The opportunity to buy the stock came when it was removed from the S&P 600 index at the end of June. The stock declined by over 25% within a few weeks as many funds that track the S&P 600 became forced sellers.

{kind=link}

In addition to the index deletion, the company took a massive LIFO accounting charge obscuring the company’s reported earnings. The accounting charge relates to how Seneca values its inventory which it has historically done on a “last in, first out” basis. After adjusting for this non-cash accounting charge, Seneca’s stock was trading for just 4x cash flow and less than 1/3 of its book value. I viewed this as an extremely attractive valuation for an otherwise staid business. We purchased shares of SENEA stock in July for approximately $36.50 per share.

What happened next was equally impressive. Other participants in the market started to catch on to the value offered by Seneca. The company reported solid financial results in August and the stock quickly caught a bid. Within a month, the stock rallied 40% and we were able to sell our shares in August at a price of around $51 per share.

Seneca isn’t a bad business, but it isn’t a super high-quality business either; therefore, the plan was always to sell the stock once it appreciated back to its fair value range. The stock reverted back to the level it traded at before the index deletion, so I felt that the event-driven thesis had played out and it was time to take profits and move on.

Until next time

Thank you for your continued support and confidence.

Best regards,

Luis V. Sanchez CFA

| Disclosure: The information and statistical data contained herein have been obtained from sources, which we believe to be reliable, but in no way are warranted by us to accuracy or completeness. We do not undertake to advise you as to any change in figures or our views. This is not a solicitation of any order to buy or sell. We, any officer, or any member of their families, may have a position in and may from time to time purchase or sell any of the above mentioned or related securities. Past results are no guarantee of future results. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. These comments may also include the expression of opinions that are speculative in nature and should not be relied upon as statements of fact. LVS Advisory LLC is committed to communicating with our investment partners as candidly as possible because we believe our investors benefit from understanding our investment philosophy, investment process, stock selection methodology and investor temperament. Our views and opinions include “forward-looking statements” which may or may not be accurate over the long term. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events or otherwise. While we believe we have a reasonable basis for our appraisals and we have confidence in our opinions, actual results may differ materially from those we anticipate. The information provided in this material should not be considered a recommendation to buy, sell or hold any particular security. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

LVS Advisory Q3 2023 Letter