TSLA - Lyft: 30% Market Share 3% Market Cap

2023-11-06 02:58:41 ET

Summary

- Lyft has lost its ground to Uber in recent years, as Uber expanded more aggressively, making it the market leader in ride-hailing.

- The Company's market share in the ridesharing industry remains strong, and active riders continue to grow, despite losing market share.

- LYFT's valuation is substantially compressed in comparison to competitors, which could attract an acquisition offer.

Lyft ( LYFT ) has been a terrible investment, shedding nearly 90% of its value since debuting on the stock market in March 2019. Despite a post-pandemic recovery in growth, Lyft hasn't been able to keep pace with its main competitor, Uber ( UBER ). In a bold move to halt its losses, Lyft's leadership saw a shakeup , signaling a clear recognition that the company is in dire need of a new strategy.

In a pivotal change, co-founders and long-standing leaders CEO Logan Green and President John Zimmer resigned. They've been at the helm since Lyft's inception, 16 years ago. In an unexpected turn, the board has chosen Lyft's own director David Risher to fill their shoes. Risher was an early player at Microsoft and moved to Amazon (AMZN) in 1996 as the 37th employee. At Amazon, founder Jeff Bezos entrusted him with the ambitious task of broadening the company's scope beyond just selling books.

Lyft's new management is poised to face the formidable challenge of reversing the company's decline in market share relative to Uber while steering the focus towards achieving profitability-a task complicated by Lyft's struggle to scale effectively. Nonetheless, should the new leadership succeed in overcoming these hurdles, there is potential for Lyft's significantly undervalued stock to mirror the ascent experienced by Uber last year, possibly leading to a substantial rebound.

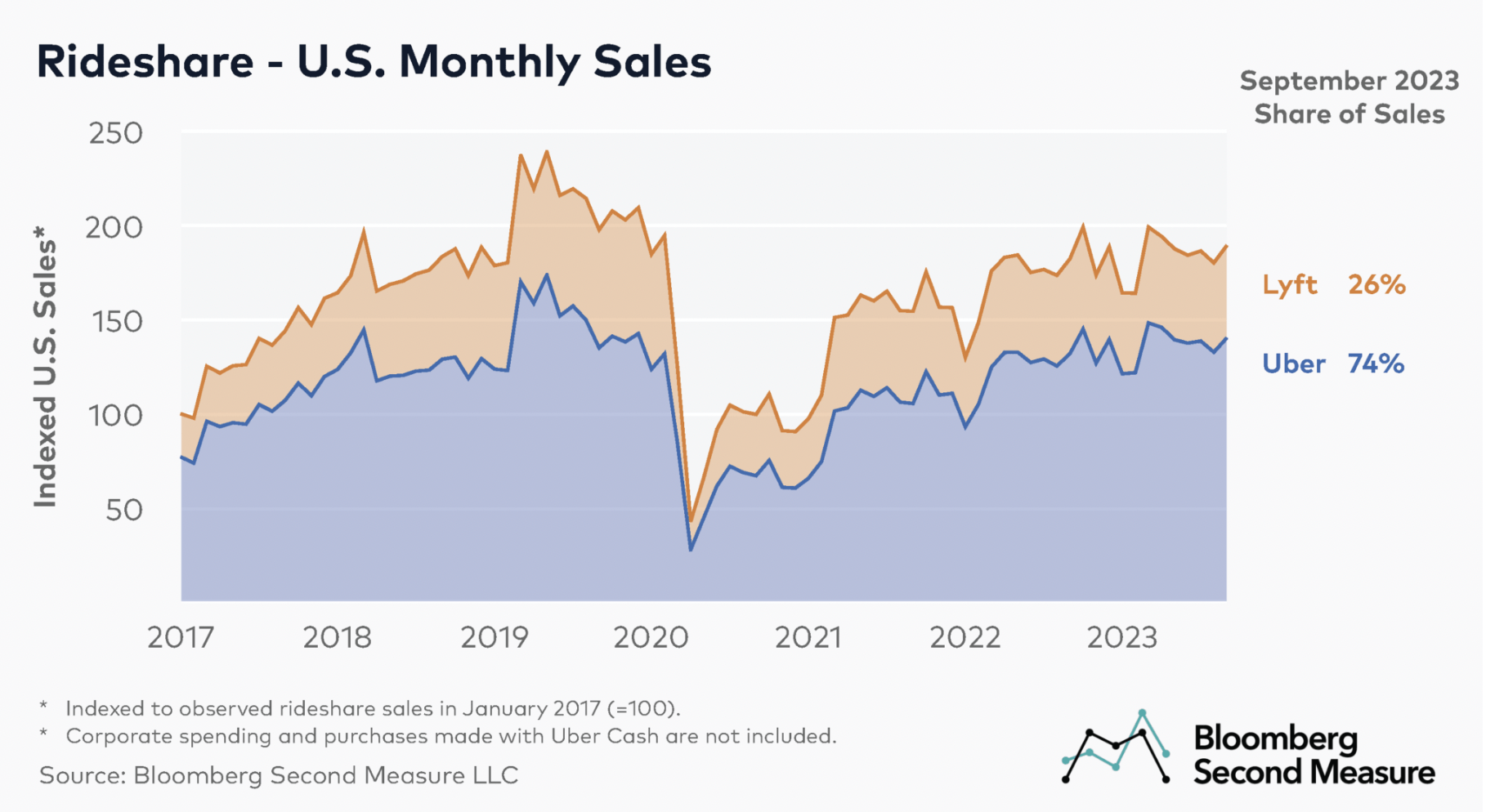

Market-Share Remains Strong

{kind=link}

Lyft's post-pandemic recovery in the ridesharing market has been rocky, but the company still maintains a considerable portion of the overall market. During Q2 2023, market leader Uber posted booking growth of 16%, while trips during the quarter grew 22%. This compares to Lyft's 18% growth in rideshare rides or 8.8% growth in active riders. However, that growth was offset by lower overall revenue per active rider (-5%) as the growth in active riders pulled down the average. In the U.S., Uber and Lyft are still a duopoly in the ridesharing market, although Uber is much more diversified in terms of offerings, as well as geographically. Its food-delivery business also took off in recent years, having grown to over $10 billion in 2022.

{kind=link}

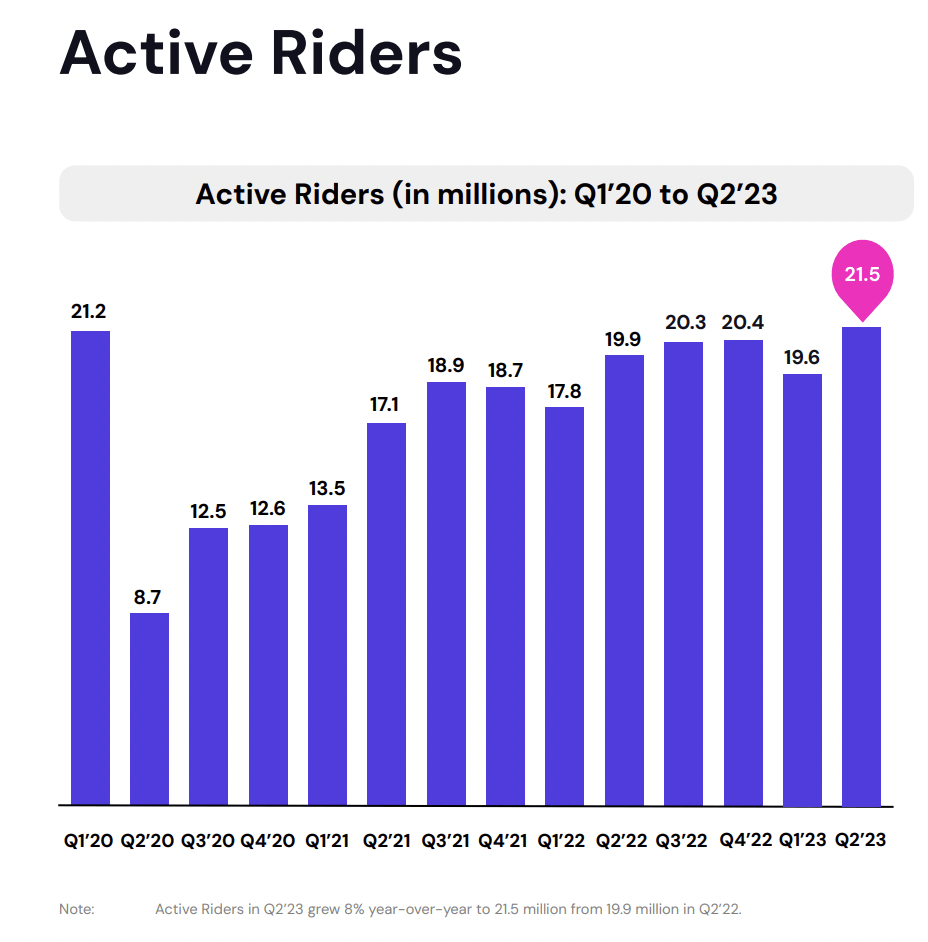

Nevertheless, Lyft's active riders continue to grow steadily, as gig-economy workers aim to diversify their income streams. In large cities during peak hours, prices and waiting times for Uber cards may increase drastically, which is why riders sometimes own both apps in order to cut waiting times or save on costs. Overall, there is very little differentiation between the two apps, in terms of functionality. The only main difference remains that Uber is more widely available, such as in smaller cities and internationally. While Uber has traditionally expanded no matter the costs, its aggressive expansion strategy could face regulatory hurdles in the future, such as the EU's new plan to reclassify drivers and couriers across the EU, which could cause Uber to cease operating in hundreds of the 3,000 cities across the EU.

While Lyft has been increasingly focusing on growing its main ridesharing business and most importantly, turning a profit doing so. However, Lyft is also investing in new mobility solutions, such as micromobility, including rented scooters and bicycles in large cities. While the business has relatively large maintenance costs, it can be profitable, as shown by competitor Lime, which is profitable for its first year, according to reports .

While there is no exact amount in terms of Lime's current valuation, estimates range anywhere from $1 billion to $10 billion. Lyft's current market cap stands at just under $4 billion and that includes its more profitable ride-hailing service. The overall growth in its micromobility section is strong, reporting double-digit growth annually.

Attractive Valuation

Lyft trades at a significant discount to Uber, which is a reflection of the difference in scale between the two companies, as well as better execution and overall growth. As mentioned before, Uber continues to grow at higher growth rates, despite generating nearly 10x as much revenue on a trailing basis. While many companies in the ride-sharing, delivery market have seen their stock prices rise, such as Uber and DoorDash ( DASH ), this has not been the case with Lyft, as negative sentiment rules.

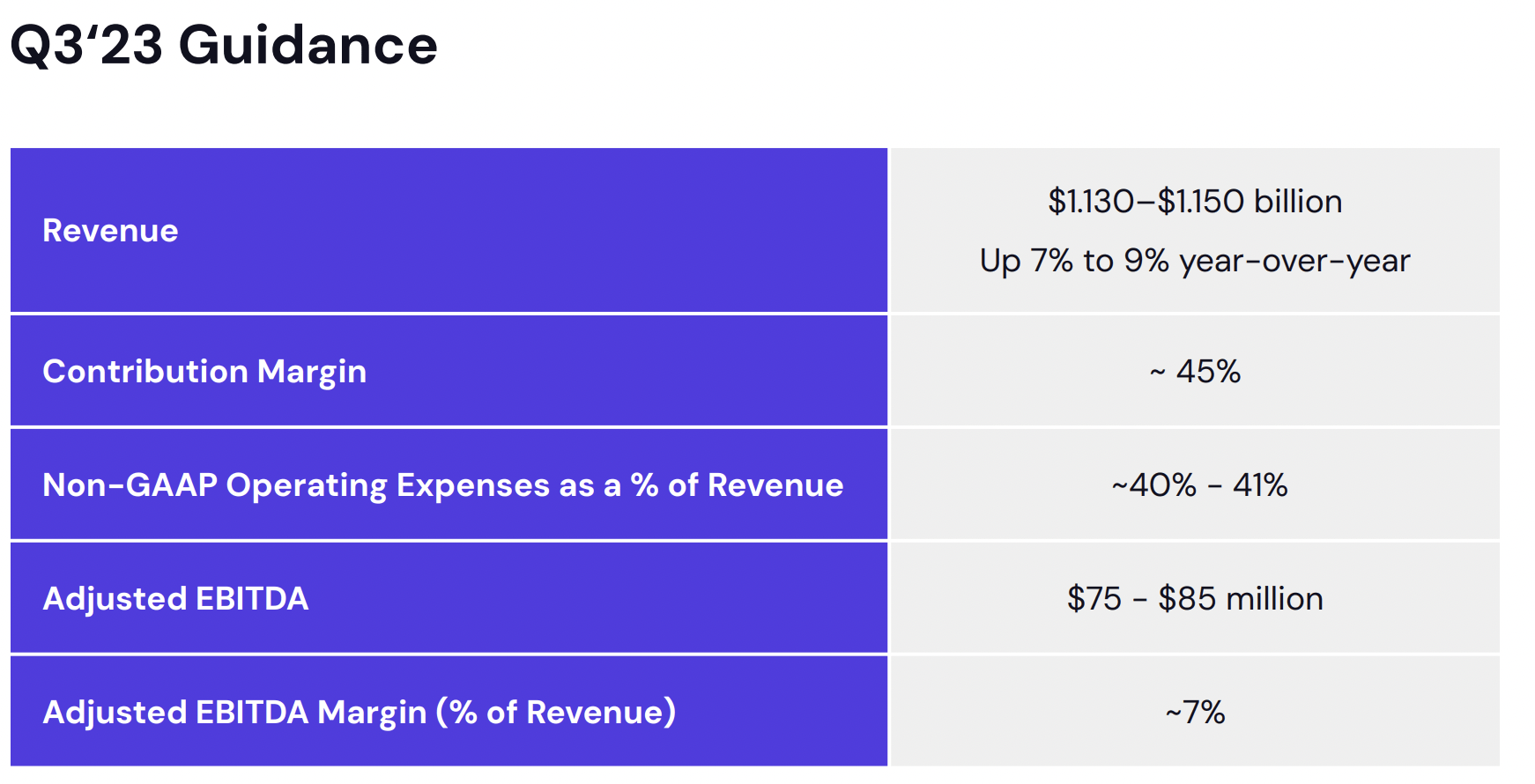

It is crucial to note that despite Lyft's missing scale, it is still a capital-light business with high gross margins. As Lyft continues to solely focus on its ride-hailing business, it is even more capital-light than Uber, yet misses the scale to turn sustainable long-term profits. However, as seen in recent quarters, Lyft is slowly steering towards profitability, achieving positive EBITDA.

{kind=link}

Lyft's overall goal of reaching $75-$85 million in EBITDA, represents a 7% margin, with just over $4 billion in TTM revenues. Lyft could potentially grow revenues to $6 billion annually, 5 years from now, which I believe is realistic. Assuming that Lyft continues to cut costs and reaches greater scale, it could achieve an EBITDA margin of 15%, translating into roughly $900 million in annual EBITDA. If its valuation and balance sheet stay roughly the same, that translates into an EV/EBITDA of 3.3x, which seems too low, considering Lyft's capital structure and low overall costs of revenue.

Despite owning roughly 30% of the total ride-hailing market in the U.S., its market cap r epresents just 3% that of all ride-hailers. Thus, it is possible, that its large network could attract buyers such as DoorDash, Tesla ( TSLA ), or Google ( GOOGL ) to get a foot into the ride-sharing industry, which is set to go autonomous in the future.

Takeaways

With strong projected growth in the ride-hailing market, Lyft is well-positioned to continue growing, despite losing ground to Uber and facing significant hurdles. After all, Lyft remains highly relevant, as seen by its growing numbers of users. Investors will closely watch its earnings call on November 8, which could serve as a catalyst for sentiment going forward.

Although Lyft's stock may seem attractively priced, notable risks remain. These include regulatory challenges, economic impacts, and most importantly, competition. These factors could hinder Lyft's already missing scale and profitability going forward. However, if Lyft can successfully address these concerns, there may be potential for upside.

For further details see:

Lyft: 30% Market Share, 3% Market Cap