AMZN - Macerich: A Broken Clock Is Still Right Twice A Day

2023-03-23 05:52:29 ET

Summary

- Macerich is a REIT operating in the mall space that only narrowly managed to stay afloat during the pandemic by repeatedly lowering its dividend and materially diluting its stockholders.

- It's a tragic tale of a truly disappointed shareholder base, that has been through two painful equity-eroding periods and has had more than one chance to be disappointed in management.

- However, past misgivings have forced the management's hand into redefining their strategy and optimizing their asset portfolio in a way that could materially benefit shareholders over the long term.

- Macerich is displaying the potential to become a true contrarian underdog turnaround story, currently being valued at a very attractive 5.26x P/FFO while offering a 7.24% dividend yield.

- Similar to the concept of a broken clock that still tells the accurate time twice a day, the time might have finally come for Macerich to step up and deliver a compelling value-accretive strategy.

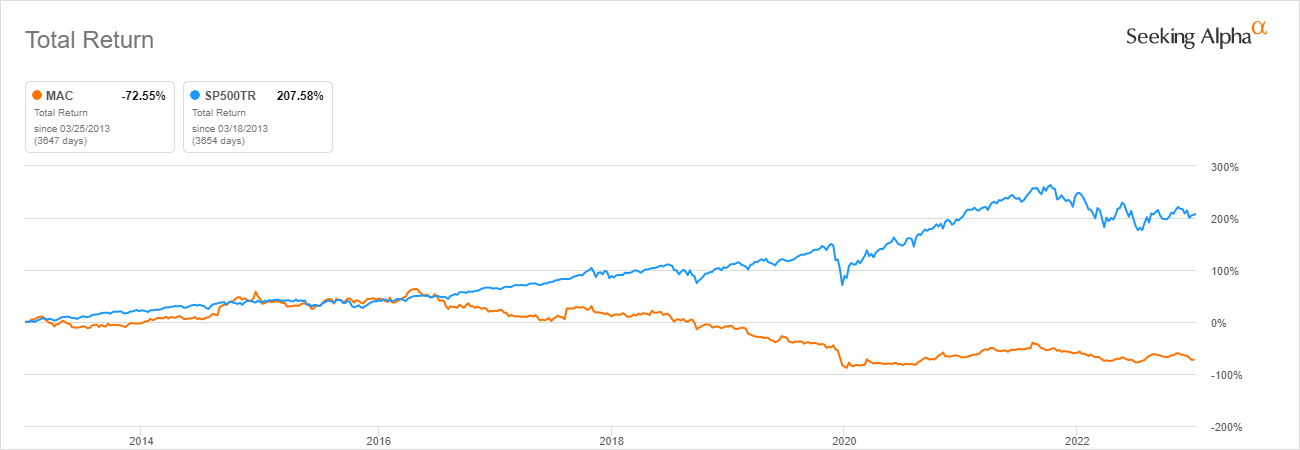

The Macerich Company ( MAC ) is a Real Estate Investment Trust operating in the mall space that only narrowly survived the pandemic after repeatedly lowering its dividend and materially diluting its stockholders in a desperate attempt for the REIT to stay afloat. After the initial post-pandemic recovery period, the company's stock saw another major selloff, losing almost 36% of its market value in the last year while lagging behind the S&P 500 ( SPY ) by a wide margin. In fact, looking back at the past decade for MAC, shareholders have been on a wild ride as the company has indeed been through both thick and thin. They have survived two very painful equity-eroding periods in the past decade alone, while those shareholders hanging on since the IPO have had more than one chance to be tragically disappointed in management and its lack of vision.

The 10-year chart does a fine job of demonstrating this equity destruction process. One might forgive you if the pitch doesn't sound all that convincing at this point. Still, what if we were to say that the past misgivings have forced the management's hand into redefying their strategy and optimizing their asset portfolio in a way that is set to materially benefit shareholders over the long term? Furthermore, what if we were to say that the market has beaten down the stock to the point where Macerich is trading at a 5.26x P/FFO while offering a 7.24% dividend yield? Well, this tragic tale likely created better value opportunities in the REIT space, and the recent price weakness over the past couple of weeks has only served to further emphasize the fact.

Macerich vs S&P500 10-Year Total Return (Seeking Alpha)

{kind=link}

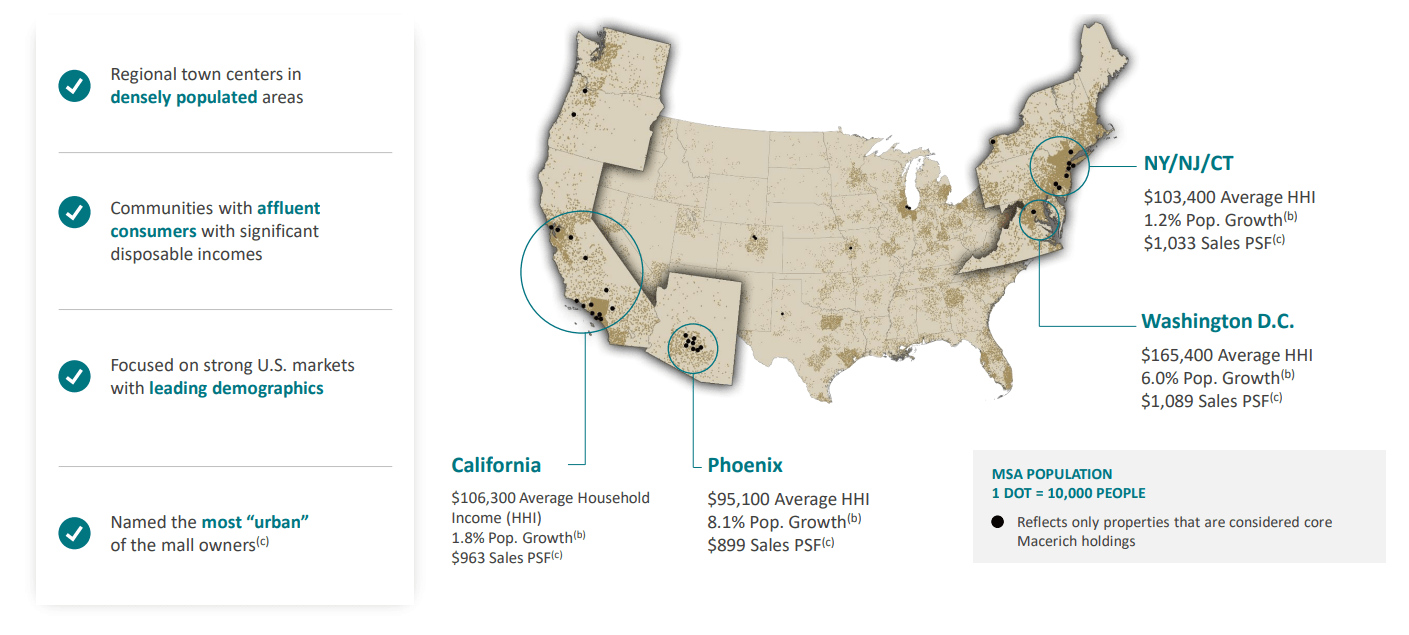

Today, the company is well known as a "Class A" mall operator with a respectable portfolio of assets, but things looked much different back in the day. Currently, the REIT owns 44 premium mall locations ranging from one end of the coast to another, as well as five community/power shopping centers, one office property, and one redevelopment property.

In terms of total figures, we are discussing 47 million square feet of the gross leasable area owned and operated by Macerich. Prior to the great financial crisis, MAC's portfolio of malls was significantly more diversified in terms of quality. The REIT has successfully repositioned its portfolio over the past decade by selling lower-quality assets and acquiring new Class A malls or buying its partners out of joint ventures.

Regional Portfolio Diversification (Investor Day 2022 Presentation)

{kind=link}

This has allowed the company to generate more tenant sales, occupancy levels, and ultimately higher rent. Macerich still finds itself in the later stages of the portfolio optimization process, trying to achieve accretive moves through various redevelopment , acquisition, and asset sale opportunities. However, the mall REIT space began to be particularly negatively impacted by rising e-commerce challenges as many of their long-term customers were forced to redefine their market strategy.

Consumers taking their business online threaten the weakest links in the tenant's lineup, as the likes of Amazon ( AMZN ) and other online competitors rapidly eat up market share. Even the healthy and resilient tenants are ultimately forced to redefine their approach and possibly be much more selective in choosing where they wish to deploy their brick-and-mortar presence.

This is exactly why Macerich stands out from its competitors in the public and private markets. Their strategic portfolio shift is a well-tailored response to the growing challenges that the e-commerce revolution poses for the mall REIT space as well as the overall brick-and-mortar retail concept. It places pressure on retail operators and forces them to redefine their approach and bring forward a new omnichannel retail strategy. As sales dollars slowly move online, this pressure first and foremost threatens the lower quality end of the portfolio, usually defined as the "Class B" and "Class C" mall properties with less prestigious and frequently traveled square footage. This is the point where we circle back to what we believe is Macerich's winning strategy for the upcoming decade. High-quality, prestigious "Class A" malls are those that are most likely to prove meaningful resilience to these growing challenges.

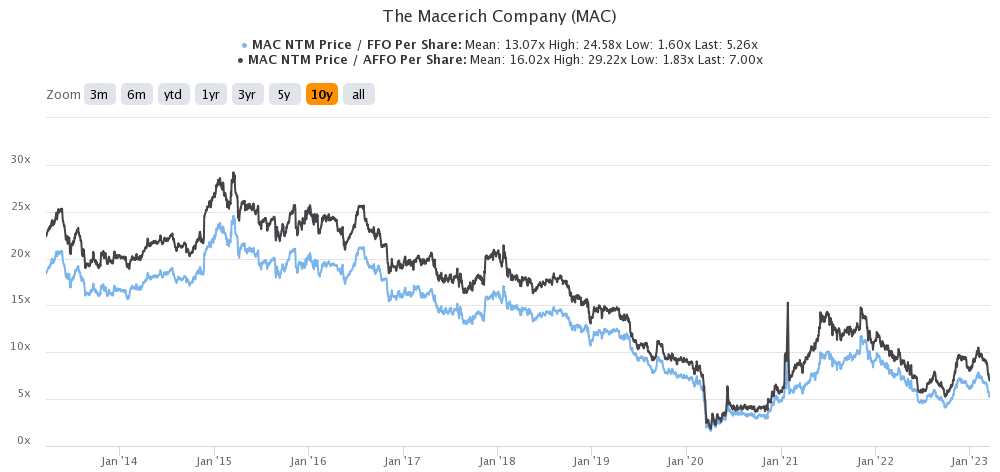

Valuation and its peers

In our view, the market seems to be missing out on this potential and keeps valuing the REIT through the lens of its previous blunders and mistakes, missing some clear signs that Macerich could be setting itself up to outperform in the upcoming decade. The market currently values Macerich at a 5.26x P/FFO with a roughly 9% implied cap rate given the current share price of $9.40. The REIT currently also offers a dividend yield of 7.24%, marking an under-pressure, but still low 39% FFO payout ratio. On paper, the pure value offering makes for a compelling argument, but the story is somewhat more complex.

Macerich 10-year P/FFO and P/AFFO Decay (TIKR Terminal)

{kind=link}

The story of how this attractive valuation came to be in the first place is somewhat tragic and mostly originates from a deeply disappointed shareholder base that has been betrayed by management time and time again. It is best told by drawing a direct comparison to Simon Property Group ( SPG ), which is a much more popular and well-respected competitor. SPG closed its initial public offering in December of 1993 at a price of $22.25 per share, while the shares of the REIT can be purchased today in the open market at around $107.12 per share.

On the other end, Macerich had its IPO a year later at a price of $19.75, but the REIT is trading under $10 per share today. Simon Property Group has had much more success, to say the least, in terms of adequately rewarding its shareholders throughout the years. One might not be surprised by the fact that the market is willing to assign a premium to the rival, valuing the REIT at 9.30x P/FFO with a similar dividend yield of 6.70%, but a much higher FFO payout rate.

From where we stand, the company seems to be sitting at very compressed valuations, with its upside potential being omnidirectional. The REIT could potentially benefit from a multiple expansion in line with other publicly listed counterparts, a slightly improved macroeconomic environment would do wonders by itself, but there is also the chance for the market to reevaluate its position on M-REITs somewhere down the line.

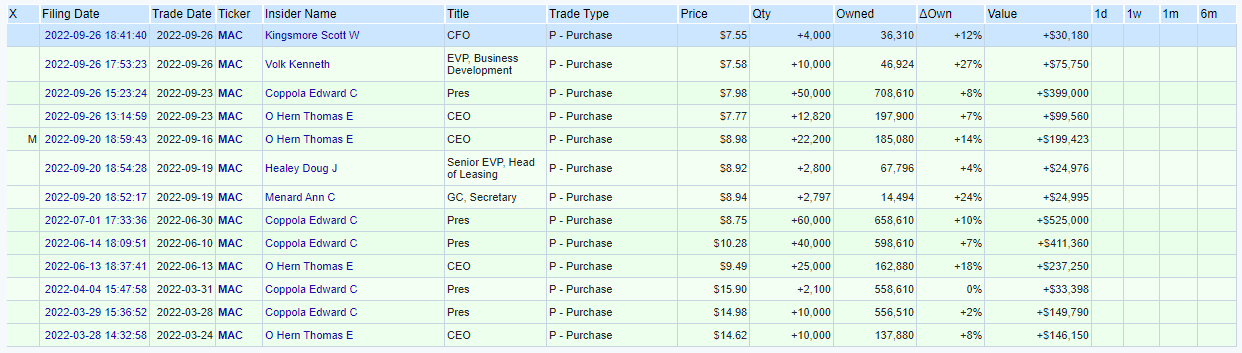

Insiders signaling confidence

With the price weakness in the following couple of weeks, Macerich is getting back into what we consider to be deep-value territory and quite a good deal. A similar sentiment was shared by management as well, which seemed to be willing to execute material insider purchases last year when the stock price was trading in about the same range.

Insiders like president Edward Coppola and CEO Thomas O'Hern bought more than $2 million worth of MAC shares in the open market in the $7.55-$8.98 range. This was the second time that insiders backed the declining share price, having done so in the pandemic era when the shares even traded in the low single digits. For what it's worth, the insiders are the same group of executives that have rejected a takeover offer by Simon Property Group at $95 per share, a close to 20% premium to what Macerich traded in the day.

Insider Activity (OpenInsider)

{kind=link}

Not everyone is on board

The market has punished MAC over and over again, which is very much warranted for a good portion of the time. Even today, a clear path toward redemption is not visible, as there are still several risks and uncertainties surrounding the business. The REIT is mainly held back by its high leverage profile, which has slowly evolved into increasing difficulty given the degrading macroeconomic environment.

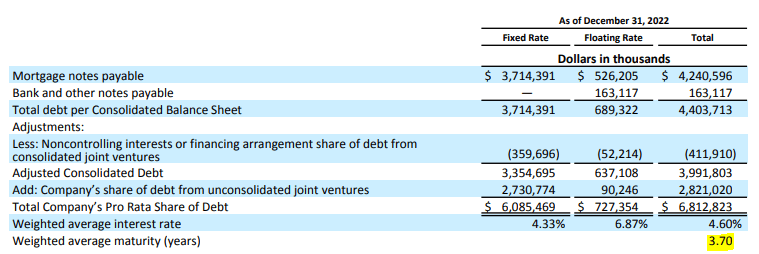

It is currently leveraged at 8.8x net debt/EBITDA, with an average weighted debt maturity of just 3.6 years. This ties up any access to cash over the next couple of years, preventing the company from materially rewarding its shareholders. Directly tied into this problem, management also indicated its willingness to further dilute shareholders during last year's Investor Day conference , openly discussing raising capital in order to service some of its debt obligations.

Debt Summary (Supplemental Information - Q4 '23)

{kind=link}

They did however state that they are unwilling to consider a capital raise as long as the REIT remains priced at these levels. The company has in no doubt executed an impressive recovery, bringing its sales, traffic, and occupancy close to pre-pandemic levels. However, even operationally, things are not as good as they would seem. While, for example, occupancy rates have been rising and are expected to gradually continue to recover over the next couple of years, this success came at a cost of re-leasing spreads which have turned negative over the past couple of quarters.

In summary, short-term headwinds mainly associated with the high leverage profile combined with long-term structural degradation of the mall business make for a fairly solid short thesis. The sum of these points, among others encouraged bears to build up a 5-10% short float, indicating a clear lack of consensus on the future of Macerich. Still, this sort of lack of consensus is exactly what brings good opportunities up front, and we believe even if we are dealing with higher levels of uncertainty, the REIT is priced at attractive enough levels to warrant more serious consideration.

Closing arguments

Similar to the concept of a broken clock that still tells the accurate time twice a day, our interest in the REIT follows somewhat of the same principle. We are not pursuing anything more than to state that the hour for Macerich to rise and shine might finally have come around and that investors who are laser-focused on its prior subpar execution might be missing out on an extraordinary deal to be made. From our point of view, Macerich's stock price remains undervalued by a significant margin when compared to both its peers and the value of its assets, as the market fails to properly price the REIT's successful post-pandemic recovery, strong operating performance, as well as the overall strengths and resilience of their portfolio.

For further details see:

Macerich: A Broken Clock Is Still Right Twice A Day