MGNX - MacroGenics: Uncertain Revenue Casts A Pall

Summary

- MacroGenics' one approved therapy is a dud.

- Its pipeline is mediocre.

- MacroGenics has a secret sauce that moderates its deficits, however its longer-term prospects are highly uncertain. .

This is my first look at MacroGenics ( MGNX ). At first I thought with its $325.20 million market cap that it was ridiculously overvalued. As I investigated it further, I moderated my concerns.

In this article I explain the situation.

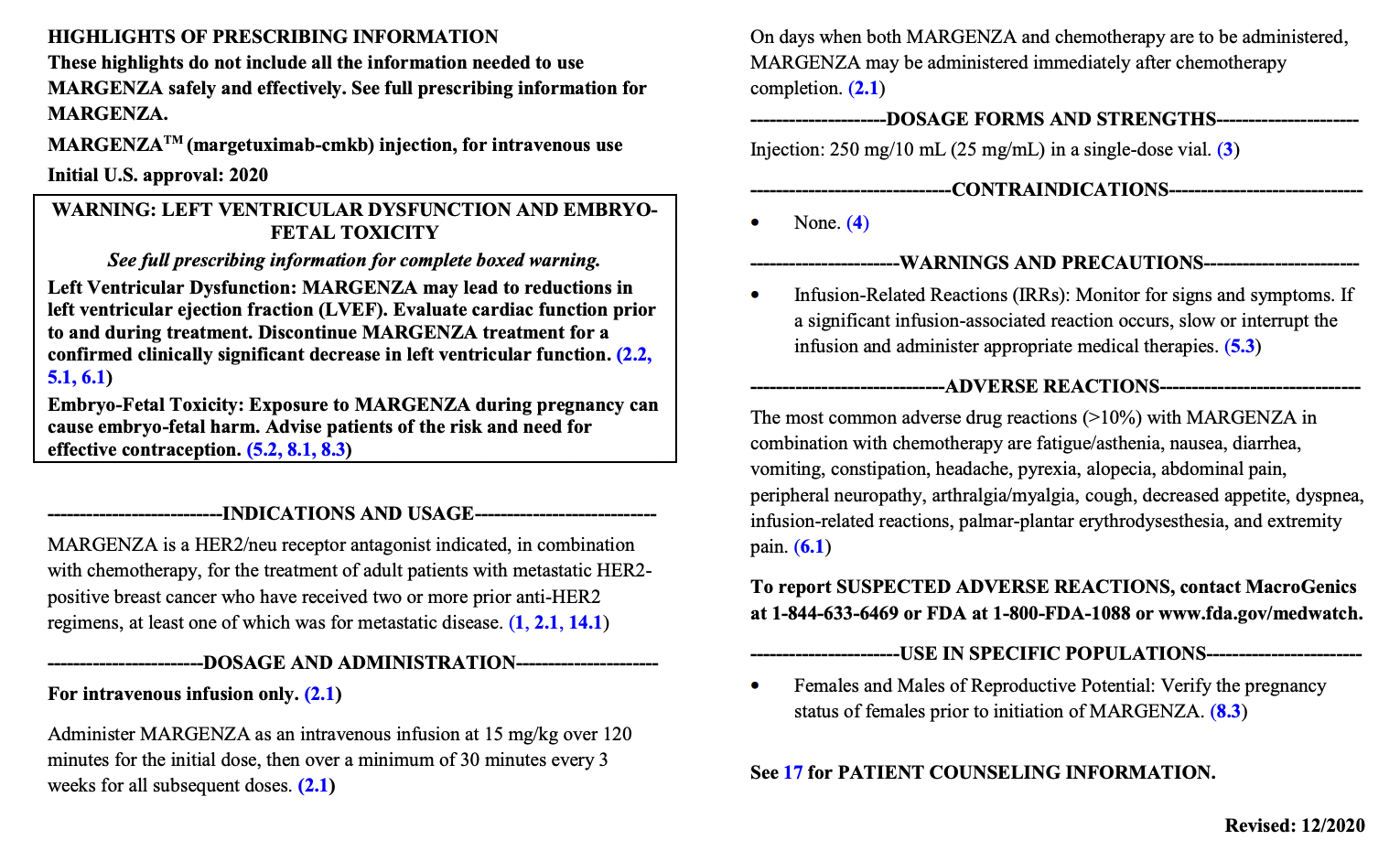

Founded in 2000, MacroGenics snared an FDA approval for its MARGENZA in 2020

In 12/2020 MacroGenics announced that the FDA approved its MARGENZA (margetuximab-cmkb) HER2 inhibitor in treatment of third line breast cancer. The approval was based on safety and efficacy results from the pivotal Phase 3 SOPHIA trial ( NCT02492711 ), a trial initiated in 2015.

Its FDA label reads:

{kind=link}

accessdata.fda.gov

In its release announcing MARGENZA's approval, MacroGenics promised availability on 03/2021. At a very early stage, during MacroGenics' Q4, 2020 earnings call it tempered expectations for MARGENZA stating:

...we have modest expectations for MARGENZA sales, given competitive realities that have taken place in the HER2 positive breast cancer market including multiple new approvals, which is great for patients.

Therefore, we will hold off providing sales guidance until MARGENZA is on the market and we have a better sense of uptake by oncologists.

During this call MacroGenics also reminded investors it was working to minimize launch expenses. It partnered the initial five years of the MARGENZA launch with EVERSANA , a pioneer of next-generation commercial services.

In its 22 slide 01/09/2023 Corporate Update Presentation (the " Presentation ") MacroGenics gives MARGENZA short shrift including the following:

- A panel in its "partnered program" slide 5 listing its US commercialization EVERSANA deal with equal cost sharing;

- Slide 17 a billboard side listing MARGENZA as its first approved therapy, showing its container graphics and its approved indication;

- slide 19 showing a headline "MARGENZA FDA Approval Based on Progression-Free Survival Results of SOPHIA Improved PFS vs. Herceptin®, both with chemotherapy, in pretreated HER2+ metastatic breast cancer" above two panels captioned "efficacy" and "safety";

- slide 19 repeating and amplifying safety information from slide 18.

Slide 21, MacroGenics all important financial overview slide set out below, contains no mention of MARGENZA. Nor does the Presentation mention MARGENZA's revenues elsewhere. To find that I had to repair to its Q3, 2022 earnings press release . It reports Q3, 2022 quarterly MARGENZA revenues of $4.4 million compared to $3.6 million for the quarter ended September 30, 2021.

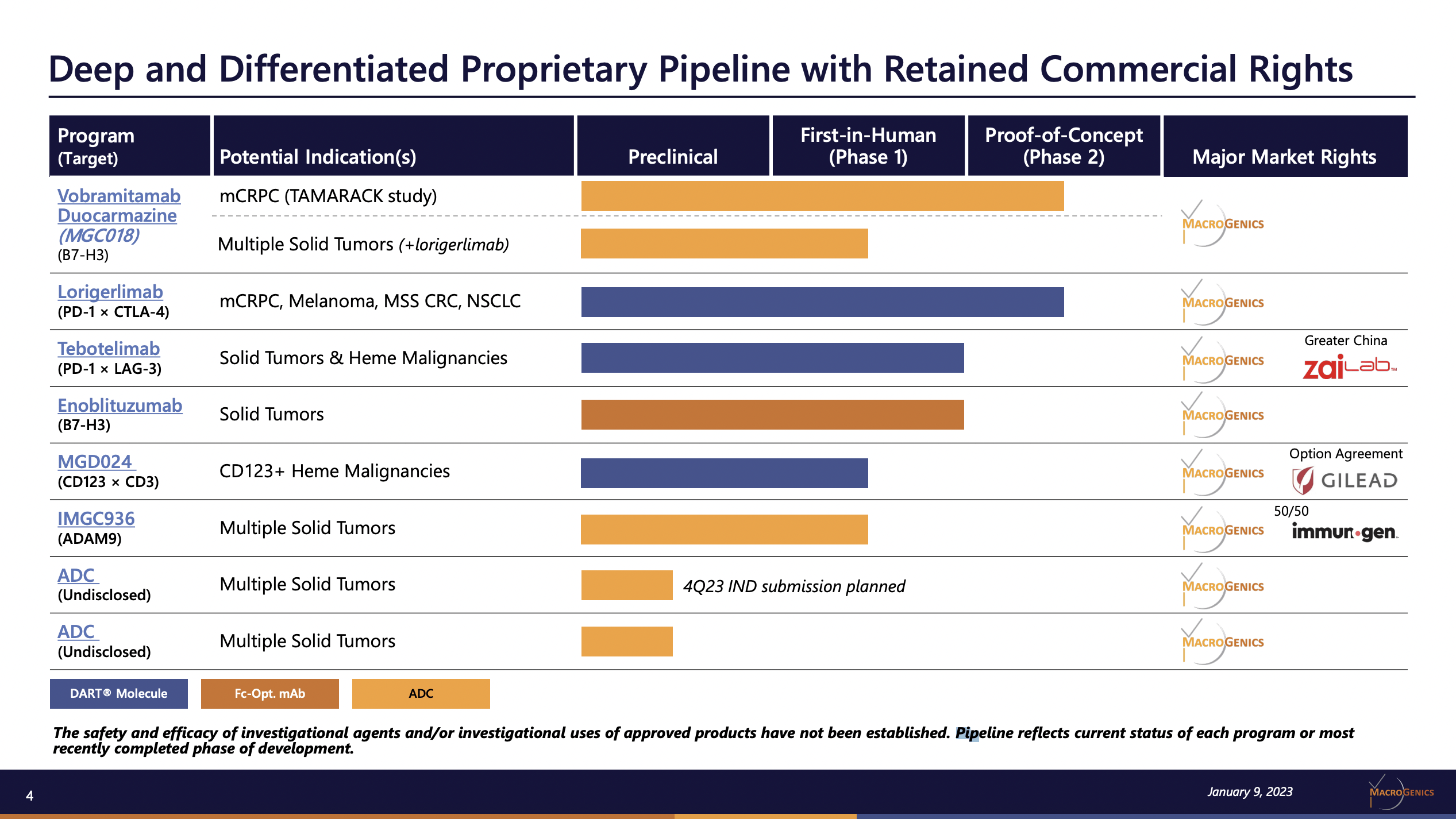

MacroGenics' pipeline is tilted towards early phase therapies

The heading to MacroGenics' Presentation pipeline slide below strikes me as quite an overstatement; you be the judge:

{kind=link}

ir.macrogenics.com

Does a pipeline with six therapies in clinical trials, two in phase 2 and none beyond, qualify as "deep and differentiated?".

Sticking with the slide, vobramitamab duocarmazine (MGC018) (TAMARACK study) and Lorigerlimab (PD-1 × CTLA-4) are its most advanced therapies. The clinicaltrials.gov brief summary of the TAMARACK study ( NCT05551117 ) lists it as a phase 2/3 study. The study start date is 11/2022; the study completion date is 12/2026. Accordingly it is just beginning with a long way to go.

During the Call, they gave MGC018 a snappy new name in prostate cancer, "vobramitamabduocarmazine". They also advised that interim data from the phase 2 portion of the study was expected in 2024.

The Presentation included seven slides with more detailed MGC018 data including slides:

- #3, Antibody Drug Conjugates panel on slide titled "Multiple Platforms for Developing Innovative Biologics";

- #6 titled "MGC018: Antibody-Drug Conjugate with Duocarmycin-based Linker Payload" including panels setting out its Function/MoA, its Clinical Results and its Milestones;

- #7 titled "MGC018: Baseline Patient Characteristics: mCRPC Expansion Cohort";

- #8 titled"MGC018: Best Percent Change of Target Lesions in mCRPC Cohort" including notation that 4 of 16 Patients (25%) had reductions in target lesion sums from baseline of ?30% (two confirmed PRs and two unconfirmed PRs);

- #9 titled "MGC018: Best Percent Change of PSA in mCRPC Cohort" with notation that 39 Patients were evaluable for PSA response: – 21 (54%) had reductions in PSA from baseline of >50% – 24 (62%) remained on treatment;

- #10 titled "MGC018: Summary of Adverse Events"; and

- #11 titled MGC018: TAMARACK mCRPC Phase 2/3 Study Design Summary".

As for Lorigerlimab, its status is more difficult. During the Call CEO Koenig reported:

During the second quarter, we completed enrollment of the Phase I/II dose expansion study with lorigerlimab as monotherapy in cohorts of patients with microsatellite stable colorectal cancer, mCRPC, melanoma and checkpoint-naive non-small cell lung cancer.

I was not able to find any reference to such a phase I/II on clinicaltrials.gov. One trial, NCT03761017 did match the pipeline slide, but it was strictly a phase 1 study. It carries the following brief description:

This Phase 1, open-label study will characterize safety, dose-limiting toxicities (DLTs), and maximum tolerated/administered dose (MTD/MAD) of MGD019. Dose escalation will occur in a 3+3+3 design in patients with advanced solid tumors of any histology. Once the MTD/MAD is determined, a Cohort Expansion Phase will be enrolled to further characterize safety and initial anti-tumor activity in patients with specific tumor types anticipated to be sensitive to dual checkpoint blockade.

In any case the point I would make is that MARGENZA is likely to be a lone ranger in terms of approved therapies for a long time.

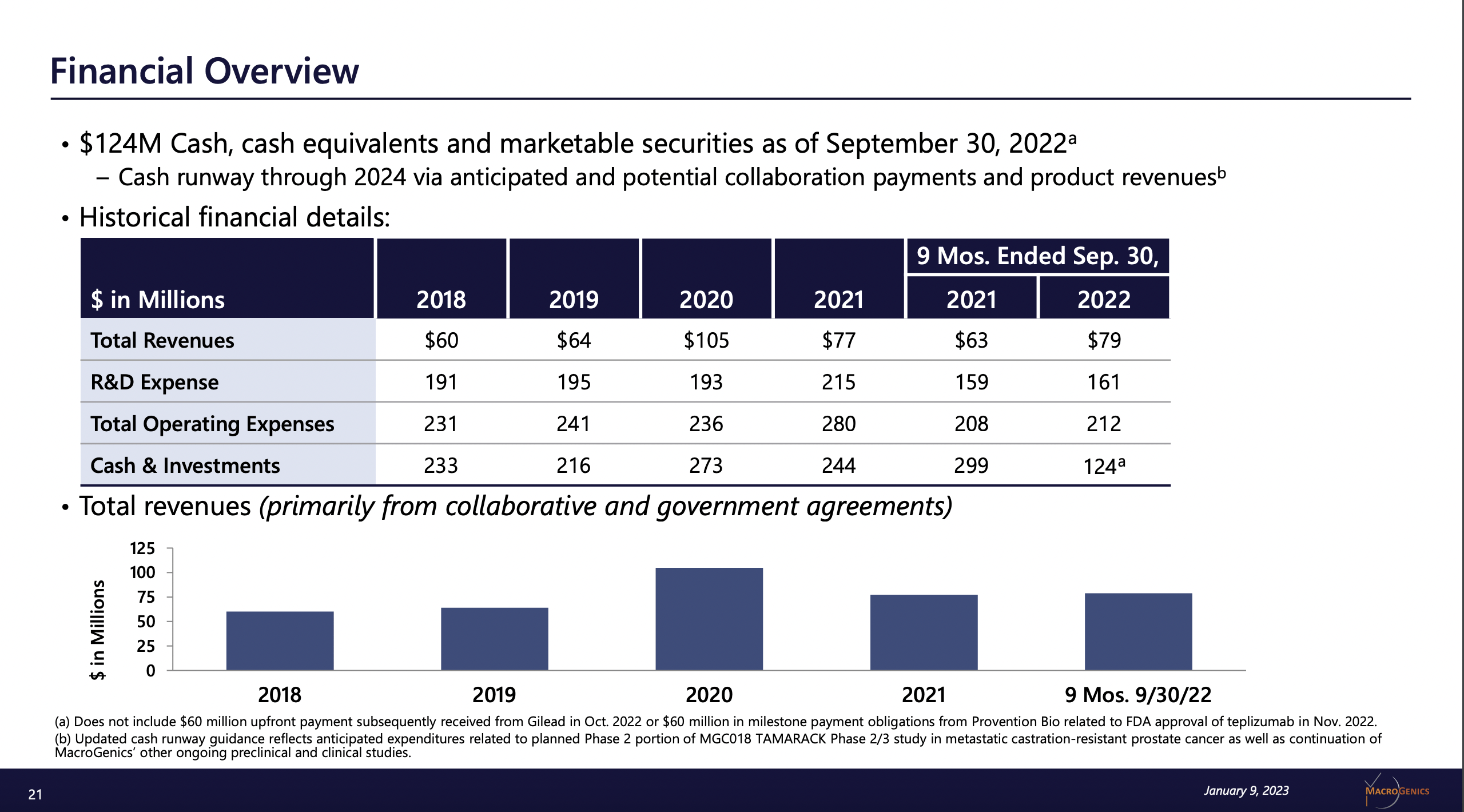

Despite its deficits in terms of product revenues, MacroGenics has ongoing revenues

The Presentation financial overview slide shows that MacroGenics has enjoyed solid, albeit lumpy, revenues over the last five years:

{kind=link}

ir.macrogenics.com

With its combined operating expenses edging up to $300 million per year MacroGenics sorely needs non dilutive revenue. Its price chart coupled with its outstanding share counts paint a concerning picture for shareholders:

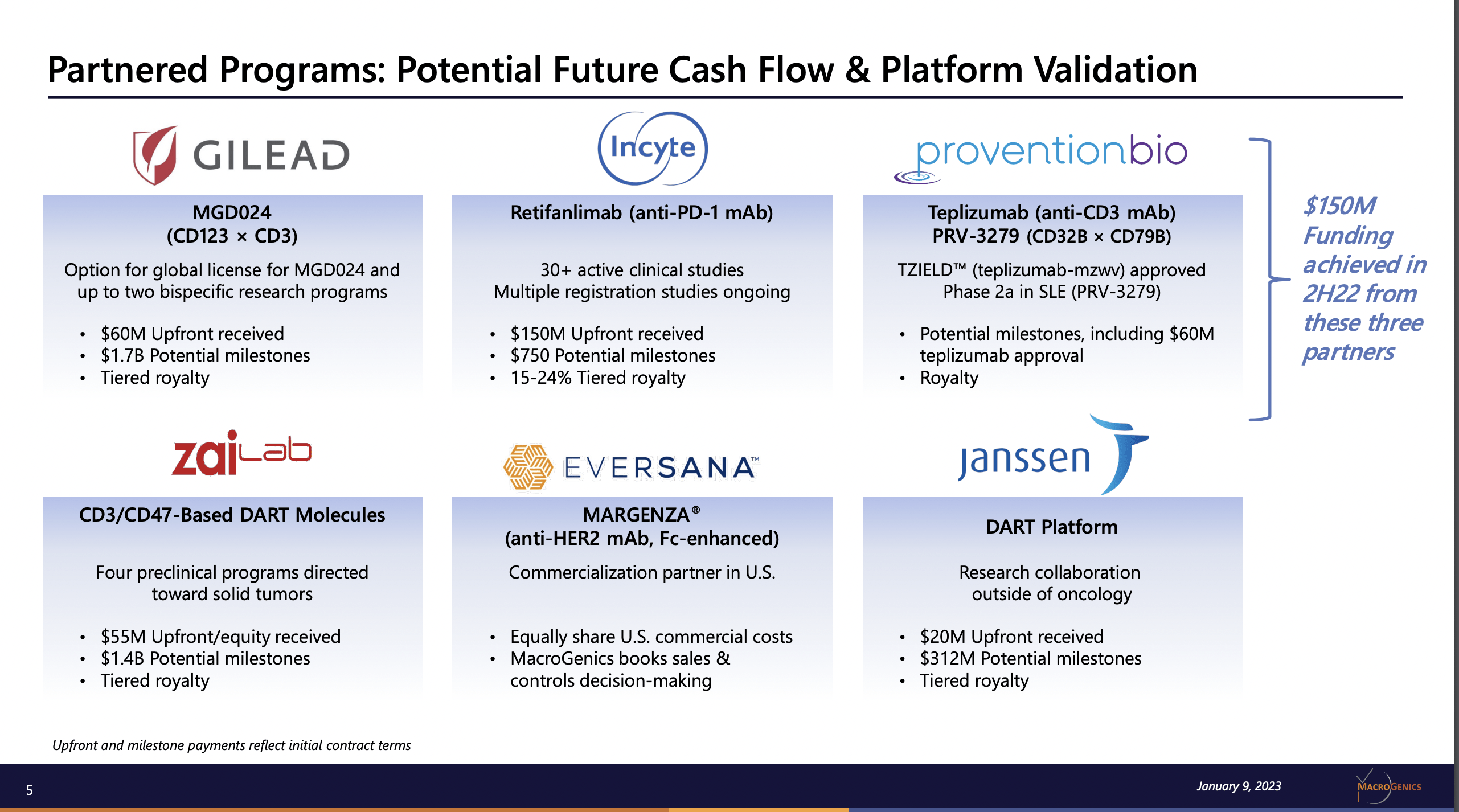

It seems certain that there will be no turnaround in the next few years based on MacroGenics' product revenues, which are minimal at best. Presentation Slide 5 lists other potential revenue sources that can offer salve to anxious MacroGenics investors:

{kind=link}

ir.microgenics.com

The three that are proving of greatest significance are its collaborations with Gilead ( GILD ), Incyte ( INCY ) and Provention BIO ( PRVB ). Gilead and MacroGenics formed a strategic alliance back in 01/2013. In 10/2022 the relationship took on a dramatic new dimension . Gilead paid MacroGenics $60 million up front with potential additional payments of $1.7 billion plus royalties on resulting product sales.

MacroGenics' deal with Incyte is multifaceted tracing back to 10/2017. I have been unable to determine how it contributed to 2H22 revenue as shown on the slide. The most recent revenues I can find from Incyte are $10 million in 02/2021 retifanlimab development milestones.

As for Provention Bio, it chipped in with $60 million in an 11/2022 milestone with FDA approval of teplizumab. This deal also calls for contingent payments totaling $225 million upon the achievement of teplizumab sales milestones as well as a single-digit royalties.

Conclusion

MacroGenics has certainly proved that its therapeutic platforms have significant value. This does not necessarily translate to investment merit. During the Call an analyst asked for clarity on how MacroGenics was setting its cash runway to 2024.

SVP and CFO Karrels responded:

We have not disclosed the specific milestones other than in aggregate that we are potentially eligible to receive from our various partnerships. ...

As I assess the situation MacroGenics is running an annual cash nut of ~$300 million. Its source to fund those expenses is an uncertain cadence of episodic milestones, with only minimal product revenues likely over the foreseeable future. This is a situation that existing investors might readily accept. It is not one that is attractive to buy into.

For further details see:

MacroGenics: Uncertain Revenue Casts A Pall