CA - Mader Group: Expanding A Highly Profitable Business Model

2023-10-23 06:39:10 ET

Summary

- Mader Group has an asset-light business model with high returns on capital which are reinvested into the business.

- Recently started an international expansion into North America (164% revenue growth in FY23), where the addressable market is huge, and increased its scope of services.

- The company is still led by its founder and an experienced management team with strong skin in the game.

- In a conservative scenario, the stock is 23% undervalued, while presenting a potential 53% upside in a base-case scenario.

Note: All currencies are denominated in AUD unless otherwise stated. The Australian fiscal year goes from 1st July to 30th June.

Investment Thesis

Mader Group (MADGF)( ASX:MAD ) is the largest supplier of contract labor for the maintenance of heavy mobile equipment in Australia that is replicating its proven business model in the U.S. and Canada, while rapidly expanding its scope of services. It has an asset-light business model with high returns on invested capital ((ROIC)) and is reinvesting over 80% of its free cash flow ((FCF)) into the business.

Mader covers a market niche that can't be filled by smaller operators and Original Equipment Manufacturers (OEM), who can't match the quality and price because of the economics of the industry. Although its clients operate in a cyclical industry, the company has already proven its defensive business model in a commodity downcycle. Mader is still led by its founder and an experienced management team, which owns over 76% of the shares. Despite the recent increase in price and valuation, there is a lot of room for future growth and the stock is undervalued, since Mader can compound its high ROIC over many years.

Company Overview

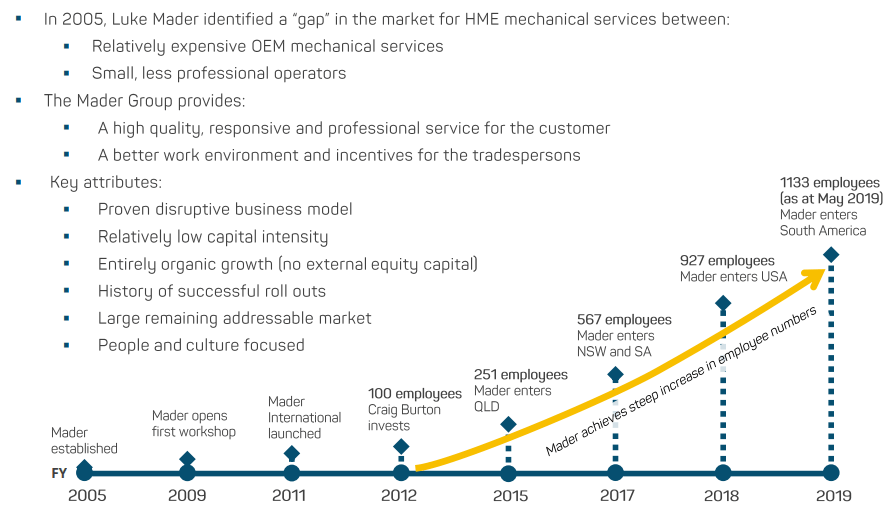

The company was founded by Luke Mader, who in the early 2000s was working as a heavy-duty mechanic for a large OEM and observed a market inefficiency. The way OEMs serves its clients is slow and unfriendly, only covering the equipment maintenance during the warranty period, which is significantly lower compared to the machine's life.

Also, most mining and energy operations involve equipment from different providers , but OEMs would only repair their own, meaning that clients need to increase their maintenance outreach efforts to repair their fleets.

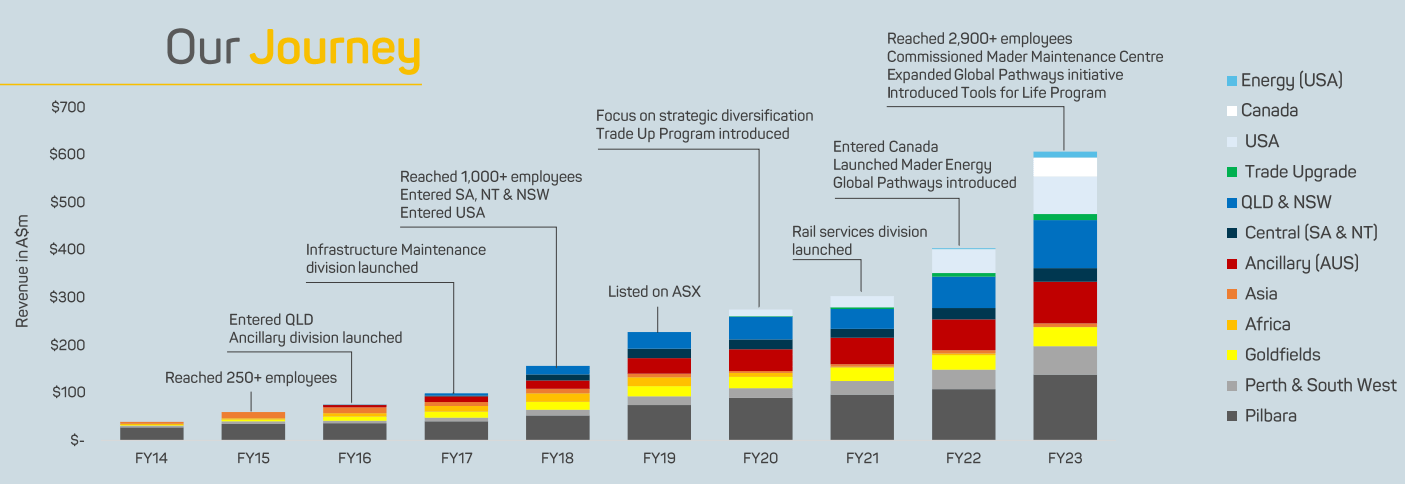

Luke Mader saw the opportunity to provide a better service at a lower cost than the OEMs, and in 2005 left his job and founded the company with one utility in Western Australia. Before going public in 2019, revenues have been growing at 48% CAGR.

{kind=link}

Mader Group IPO Presentation, 2019

However, the major opportunity for Mader has been its expansion into North America, which is currently driving its high growth rates and is still in the early phase.

Mader commenced its operations in the U.S. in 2018 and in 2022 it expanded to Canada. North America is already generating over 20% of total revenues with a 164% revenue growth during FY2023.

{kind=link}

Mader Group FY2023 Results Presentation

The company has not only expanded its markets but also the number of services, improving its competitive advantage and becoming a one-stop shop for heavy equipment maintenance. Currently, it provides the following services:

- In-field support for mining and energy

- Infrastructure maintenance

- Rapid response teams

- Rail services

- Road transport maintenance

- Dig and drill support

- Electrical services

- Power generation and marine support

- Boilmaking, line-boring, and machine washing

- Fixed plant planning and management

- Specialized tool hire

IPO

After many years of success, in 2019 Luke Mader and Craig Burton, a venture capital investor who entered the company in 2012 with a 25% stake , decided to become a publicly traded company on the Australian Securities Exchange ((ASX)).

Mader didn't raise any funds with the IPO but it allowed Luke Mader and Craig Burton to lock some of its gains, broaden the company's shareholder base, and increase the level of employee ownership. They release 25% of the company at AUD 1 per share, offering a 10% discount for employees, who subscribed to 3.26% of the total offering . After the IPO, Luke Mader continued controlling the company with a 56.6% stake and hasn't sold any shares since then.

{kind=link}

ASX

Business Model

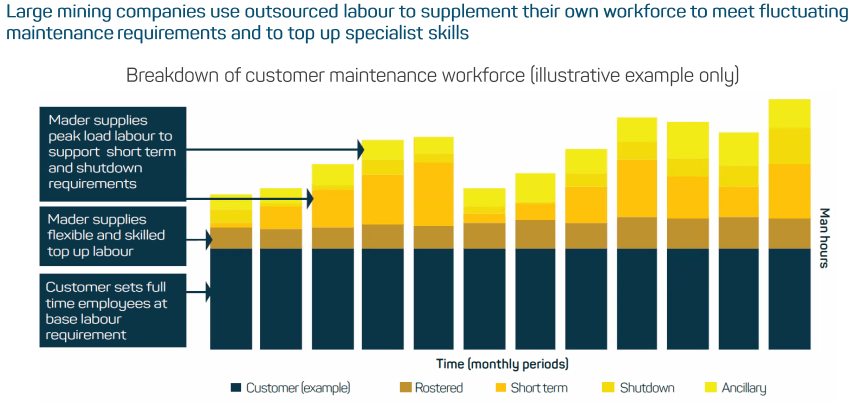

By providing a wide range of services globally, the company makes its clients' lives easier, since most of them are large mining and energy companies with operations around the world using expensive equipment from different suppliers. While the warranty covers between one and five years, the useful life is longer and most of the repairs happen after the warranty period. Since Mader can relocate its workforce depending on its client's needs, it provides great value to improve efficiency and staff reduction in mining and energy companies.

1) Asset-Light Business

Mader Group's clients operate in an asset-intensive industry with high maintenance Capex, but the company provides its services through an asset-light business model.

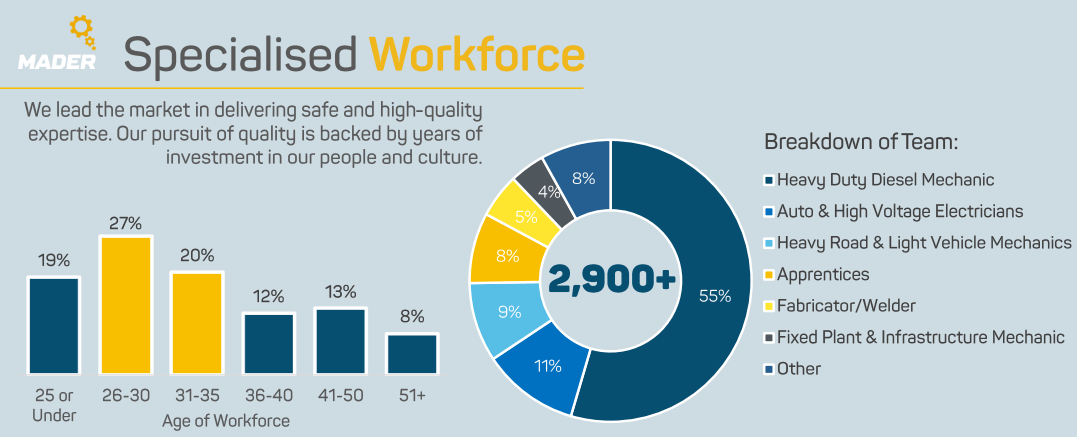

The balance of the company is simple, it owns +1,100 support vehicles throughout the world and employs +2,900 skilled technicians who provide heavy equipment maintenance, allowing its clients to outsource part of the staff while improving operational performance.

{kind=link}

Mader Group IPO Presentation, 2019

Vehicles are depreciated at 20-30% annually, but the useful life is longer and significant portion of their fleet that is depreciated is still in operation.

{kind=link}

Mader Group FY2023 Results Presentation

Mader generates its revenue by charging hourly rates per tradesperson depending on the service and speed required by its customers, typically under a service agreement. The term of the agreements ranges between 1 and 5 years with an option for the customer to terminate on a short notice period ranging from 1 to 3 months.

2) Workforce and Culture

Mader's operations rely heavily upon its people, and it has always maintained a strong focus on culture by providing continuous development while compensating fairly its employees.

In 2019, they introduced the Mader Trade Upgrade Program to upskill its mechanics, and reached over 200 graduates this year. Justin Nuich, the CEO of the company commented :

We're training up new talent. Most of these are very dedicated and loyal people that will continue with the Mader Group for years to come, which is fantastic to see.

Furthermore, the Global Pathways program gives its employees the opportunity work in other countries, while the Three Gears program connects its people through adventurous experiences. This strategy is highly profitable in the long term, especially in a business model where employees are the ones on the ground maintaining relationships with the clients. Mader has won multiple employee awards in Australia and received positive reviews, averaging 4 stars on Seek, surpassing the 3.5 industry average .

{kind=link}

Seek

The group operates through autonomous divisions, each with separate P&L accounts. Divisions are assessed based on profit, safety, and staff retention metrics. Each unit has managers, administrative and field staff, comprising the majority of their workforce. The company has around 100 office staff, 220 technicians in the U.S. , 200 in Canada, and approximately 2,500 in Australia.

{kind=link}

Mader Group FY2023 Results Presentation

Australian companies have a strong culture for work safety and Mader Group has consistently reduced injury frequency rates, improving from 9.1 per million hours worked in 2016 to 3.91 by FY2023 .

3) Top-Tier Clients

Its client base is mainly top-tier companies in the resource and energy industries such as BHP Group Ltd. ( BHP ), Rio Tinto ( RIO ) or Fortescue Metals Group ( OTCQX:FSUMF ).

The company services over 530 locations for its 380 customers, creating long-standing and recurring relationships to meet its maintenance and repair needs.

Customer concentration has been reducing as the company grows and expands into new sectors such as infrastructure maintenance, energy (oil and gas), transport, and rail.

Only one customer generated over 10% of revenue during 2023, and I suspect BHP is the biggest client, since they have operations with many of its divisions.

In its resource and minerals division, clients are mainly in the iron ore industry (44.8%), gold (22.9%), and coal mining (13.2%).

From a geographical perspective, Mader still generating most of its revenue in Australia (77%), but North America has been growing at a faster pace while other regions (Indonesia, Philippines , Papua New Guinea, Zambia, and Mongolia) have been decreasing.

Author (Data from Annual Reports)

4) Competitive advantage

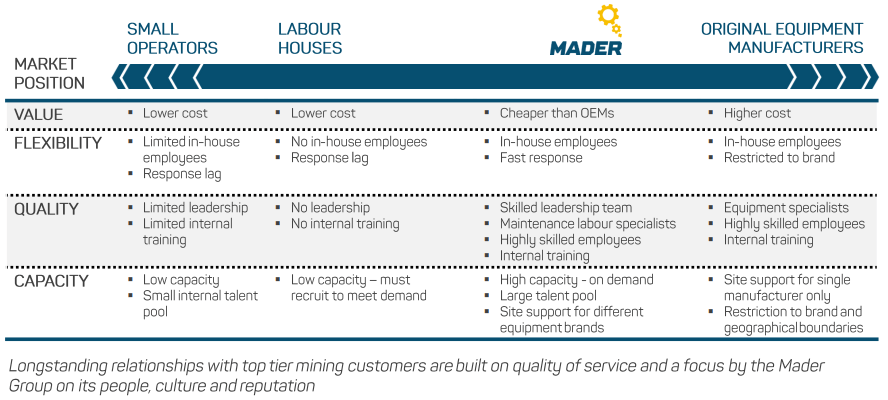

Mader's competitive advantage arises from its unique global business model. They are able to provide a quality service for a lower price than OEMs and dealers, delivering the service rapidly when needed because of their skilled in-house technicians. OEMs make most of their profits from machine sales and spare parts, while maintenance is a burden they have to carry during the warranty period. Smaller operators and labor houses can't compete with Mader thanks to its size, proven track record, and one-stop shop of services. As the company expands geographically and by service offerings, its competitive advantage increases.

{kind=link}

Mader Group IPO Presentation, 2019

In the Australian landscape, there are some smaller competitors, but as the management commented ( H1 2022 Earnings Call ) the situation in North America is different:

The Aussie market, I guess it's quite mature, and we see some smaller competitors doing similar sorts of things. What we probably see less of in the US is this top of business model. It tends to be more OEM dealers and local businesses,, but just in regional areas, supporting local towns.

There are no listed companies providing a similar service. Its closes counterpart in Australia is Premium Mechanical Group , which started its operations in 2006 on the West Coast and employs around 200 people . Other companies such as Santrix Diesel or Superservice are significantly smaller and lack ability to provide extensive services. In the U.S., L&H Industrial , though substantial with 450 employees, covers field services as just one aspect, also engaging in equipment design and manufacturing.

Market and Drivers

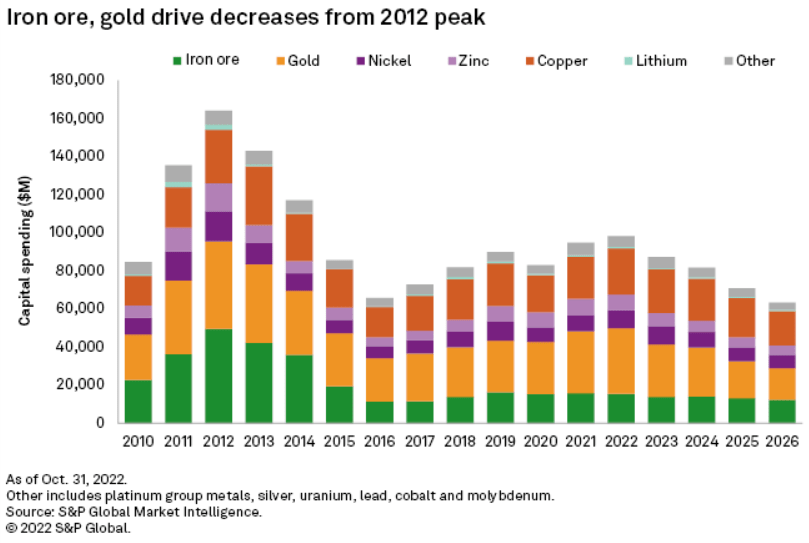

The market is driven by production growth in commodities, capital expenditure on new equipment, and the demand for maintenance labor and outsourcing. Mining companies operate in a cyclical industry, but the maintenance services are stable and can even profit in a commodity downcycle where in-house staff is reduced. Also, if capital expenditure on new mining equipment decrease, the older equipment will require higher maintenance.

Mader has benefited from the last downcycle in commodities, increasing its revenues from AUD 25.2 million to AUD 99.3 million between 2012 and 2017.

{kind=link}

S&P Global Market Intelligence.

The total addressable market ((TAM)) has been growing as the company expands geographically and enters new industries.

Mader Group FY2023 Results Presentation

In Australia, the core business continues to grow at 35% while infrastructure is growing at 57% annually. In North America, the company has just started its journey and is only in 3% of the addressable mines, presenting a massive growth opportunity.

Mader has also entered the energy industry in 2022 delivering maintenance in natural gas compressor stations. This vertical is in its early phase and has been launched as an organic start-up, but it could represent a huge opportunity. For the upcoming years, the market will be driven by the energy transition and critical minerals , such as lithium, cobalt, or nickel, used in batteries, electric vehicles, and solar and wind generation. I don't expect Mader's market to be disrupted soon and the way mining operations are conducted shouldn't change.

Financials

Mader Group's unique business model combined with its expansion strategy has allowed to company to enjoy a strong financial position.

1) Increasing Income

Revenues have been growing over the years, and the number of employees increased from about 20 technicians in 2009 to over 2,900 in July 2023. Equipped vehicles also increased since Mader is using on average one vehicle for every 2-3 technicians.

Author (Data From IPO Prospectus and Annual Reports)

Revenue per employee has been growing and the company is generating AUD 210,000 in revenue per employee annually. Revenues are recognized when the services are rendered, and on average, customers have a 45 to 60-day payment structure.

2) Margins

The most significant cost in the Mader Group's business is labor cost, which represents ?73% of total costs. In Australia, the company is paying up to AUD 80 per hour to auto electricians and heavy-duty diesel mechanics, which would add up to AUD 160,000 annually. In North America, operating margins are higher and salaries for the same job are USD ?45 per hour (AUD 70).

Comparing what the company is paying in salaries with revenue per employee (AUD 210,000), I obtain a 23% gross margin in Australia and 30% in North America. This adds up to what the company reported in FY2023 with EBITDA margins of 12% in Australia and 17.5% in North America.

Administrative staff, office rental, insurance, depreciation of furniture, computers, and software, represent about 14.4% of costs, while interest expenses are less than 1%, since it is using its FCF to expand. Net income margins have been improving over the years, increasing from 4.3% in 2017 to the current 6.3%, and this trend should continue.

The North American region provides some better margins for us. So as that continues to scale and grow at the rates we've seen, that impact on the Group margin should flow through. (Justin Nuich, FY2022 Earnings Call )

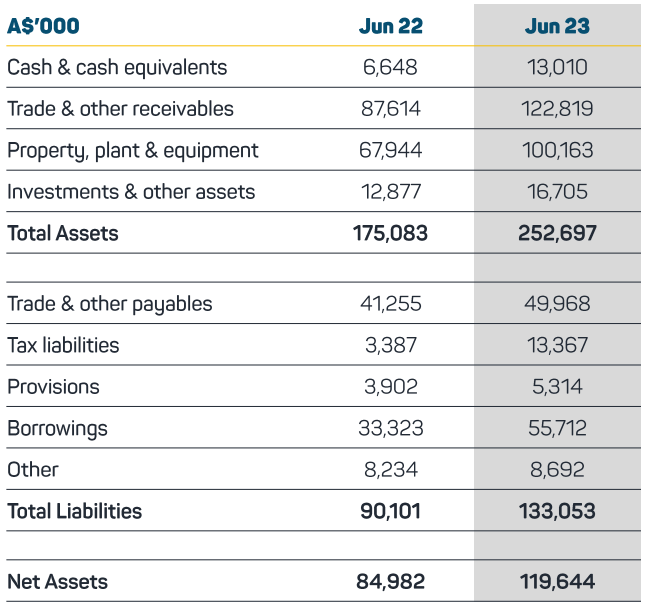

3) Balance sheet

Mader's balance sheet is straightforward, which allows investors to keep track of the company without looking for hidden notes in the annual reports.

{kind=link}

Mader Group FY2023 Results Presentation

Current assets are mainly receivables, getting paid at 45 to 60 days, while non-current assets are mainly vehicles (86%), depreciated over 4 years on average. On the liabilities side, trade & other payables are expenses related to day-to-day operations, inventory, and tools supply. It is a non-bearing interest liability and is paid at 30 days on average.

Mader has AUD 55.71 million in debt at a 7% interest rate on average, of which only 14% is on floating interest rates. Net debt is low and stands at 0.71x EBITDA.

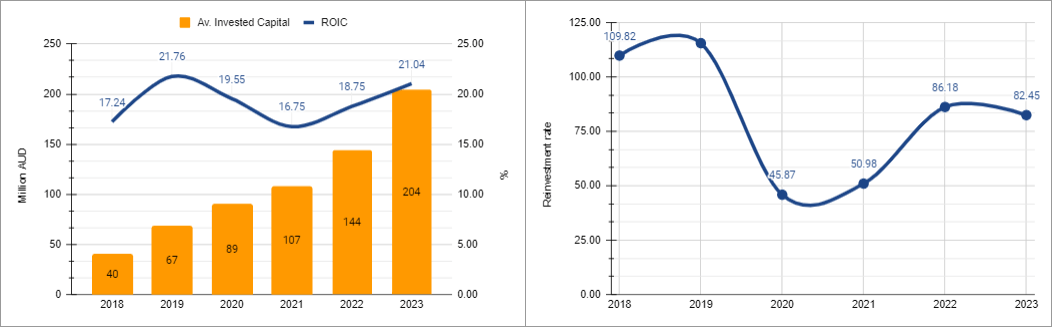

4) Returns on Capital

This asset-light business model has allowed Mader to generate high ROIC over many years while reinvesting its profits back into the business.

{kind=link}

Author (Data from IPO Prospectus and Annual Reports)

On average, it has reinvest over 80% of its cash from operations into expanding the business and increased the number of vehicles from 400 in 2019 to the current 1,100. Its ROIC has kept north of 19%. This is already impressive performance, but I believe in the upcoming years returns should increase even more because of depreciation accounting.

So yes, the depreciable life is a lot shorter than the whole useful life of that vehicle. So there would be a significant portion of our fleet that is fully depreciated, but still in operation. (Justin Nuich, FY2021 Earnings Call )

Once Mader reduces growth rates, Capex should decrease as a percentage of sales. Also, the company is entering new verticals that require less Capex , such as infrastructure maintenance and rail.

5) Capital Allocation

Capital allocation has been focused on growing into new markets and entering new industries, and I expect this trend to continue for many years ahead. Mader has not made any significant acquisitions and this demonstrates how strongly management believes in its own business.

Trying to buy something and then change culture and turn it into something that we want, you could spend just as much time in any you doing that, then you could doing an organic startup. So we did end up doing an organic style. (Justin Nuich, H12022 Earnings Call).

To expand in North America, which currently generates AUD 132.2M in revenues, the CFO of the company moved with his family for a couple of years to the U.S., and in one year it was already profitable. Later on, Mader expanded to Canada by opening another start-up, and in less than two years they are already in 5 provinces. Since Mader can expand organically using its FCF and doesn't require to deploy large amounts of capital to grow, it has been paying 35% of its earning in dividends.

6) Taxes

Most of the revenue has been generated in Australia until recent years and effective tax rate for Mader has been at 30%. In the U.S. and Canada effective tax rates are lower, and since revenues are increasing faster and are expected to represent a higher percentage, the effective tax rate will be below 28%.

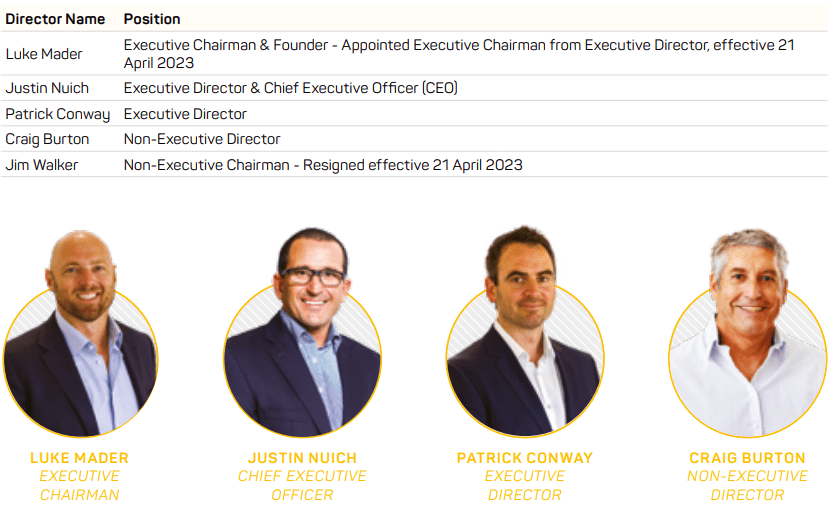

Management

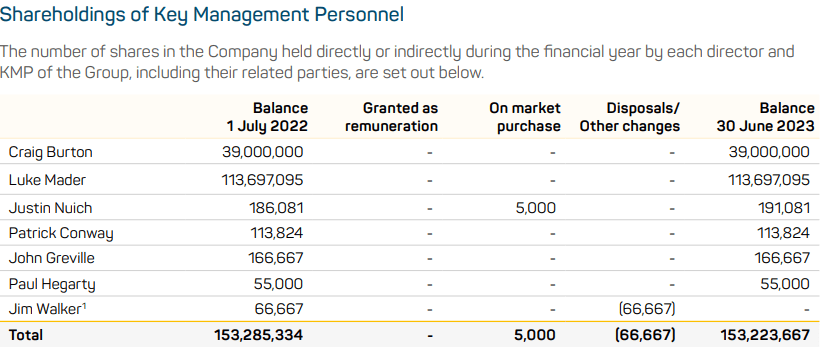

The company continues to be run by its founder Luke Mader (42), who acts as Executive Chairman and owns 56.8% of the shares valued at AUD 668 million (USD 422 million), while receiving received a salary of AUD 233,241. He started working as a tradesperson at CAT and transitioned into a marketing role at Caterpillar. In the early stages of Mader, he has been in the fields, so he really understands the business.

{kind=link}

Mader Group FY2023 Annual Report

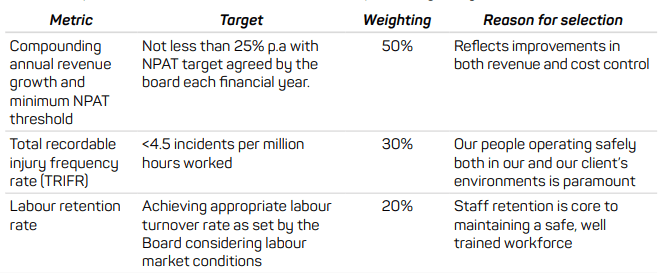

The other major shareholder and early investor Craig Burton, owns 19.5% of Mader and receives AUD 66,300 for his responsibilities at the Audit and Risk Committee and the Nomination and Remuneration Committee. The CEO of the company since January 2021 is Justin Nuich, who previously worked at Fortescue Metals Group Ltd. ( OTCQX:FSUMF ), Mineral Resources Ltd. ( OTCPK:MALRF ), and BHP Group Ltd. ( BHP ). He invested over AUD 1M in Mader since the IPO, despite having 2,25M performance rights and 1M share appreciation rights that will be exercisable on June 2024 and June 2026, which I believe is really positive.

Performance rights are vesting in 2024 if net profit after taxes (NPAT) is over AUD 40 million, and AUD 60 million in 2026..

{kind=link}

Mader Group FY2023 Annual Report

The compensation structure aligns management with shareholders' interests by incentivizing revenue growth without compromising margins, ensuring a minimum NPAT. Former CEO Patrick Conway, now Director of Emerging Businesses joined the company in 2014, while the current CFO Paul Hegarty was appointed in 2020. The COO, John Greville, has been with Luke Mader from the beginning. They know every little detail about the day-to-day of its employees and how the business works from top to bottom, and I believe this combination of talent could explain the success of Mader.

{kind=link}

Mader Group FY2023 Annual Report

The management combined holds 76.6% of the total outstanding shares.

Expected growth

Mader has been growing faster than its competitors and smaller operators which shows the management's ambition and ability to execute its strategy successfully. The main question is if the company still has room to grow, and I believe there is way more growth ahead.

First, its expansion into North America has just started and the addressable market is at least three times bigger than Australia. The number of vehicles and personnel is just about one-fifth when compared to Australia, and I expect this market to represent over 50% of Mader's revenues over the years.

Secondly, the number of services and industries has also increased and Mader just entered the energy market, which could be huge.

Our primary growth drivers include the energy market, in which we have entered the industry delivering maintenance and natural gas compressor stations. This entry point is just the tip of the iceberg with several stages of the upstream and midstream sectors also requiring equipment support. (Justin Nuich, FY2023 Earnings Call)

The replicable business model has already proved it can successfully create profitable and fast-growing start-ups, and Mader is enjoying some tailwinds since the U.S. wants to reduce its reliance on imports of critical minerals and energy, increasing the activity in the region.

Finally, I expect increasing margins as taxes go down, North America represents a higher percentage of revenues, and depreciation reduces.

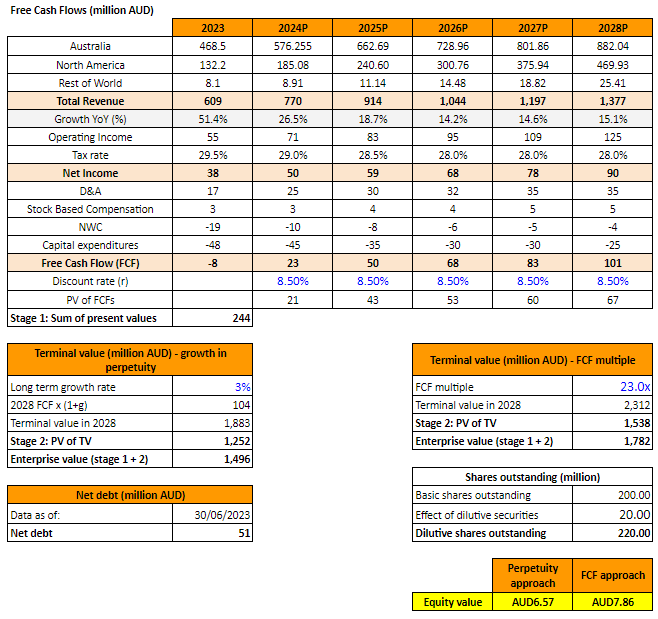

The management set up a goal to achieve AUD 1 billion in revenues during FY2026, which would represent a 20% CAGR, but I expect them to reach it earlier, since they have long history of conservative guidance. During FY2023 they upgraded its guidance two times and ended up exceeding the last guidance. For FY2024, revenues are expected at least AUD 770 million with NPAT at AUD 50 million. I assume an increase of 22% in Australia, 40% in North America, and 10% in the rest of the world.

The increase in Australia and North America I believe is conservative given the recent growth and the opportunities ahead. Although the rest of the world segment won't change significantly the outcome, it was significantly affected by COVID-19 related travel restrictions and over the years it could grow at least to pre-pandemic levels (AUD 27 million). Since the IPO, shares have remained at 200 million and if the maximum number under the incentives program were exercised, it would increase to 211,48 million. Until 2028, I don't expect them to increase over 220 million.

{kind=link}

Author

I used an 8.5% discount rate, based on its low debt at 7% and assumed a 3% long-term growth rate, based on inflation. With a 23x last twelve months FCF, I get an average fair price of AUD 7.22, presenting a 23% discount. In a more optimistic scenario, with revenue growth declining over the next years to a rate of 15% in Australia and 25% in North America for 2028, higher net working capital ((NWK)) and 7% net income margins, my fair price is over AUD 9 (USD 5.7), representing a 53% potential upside.

Valuation

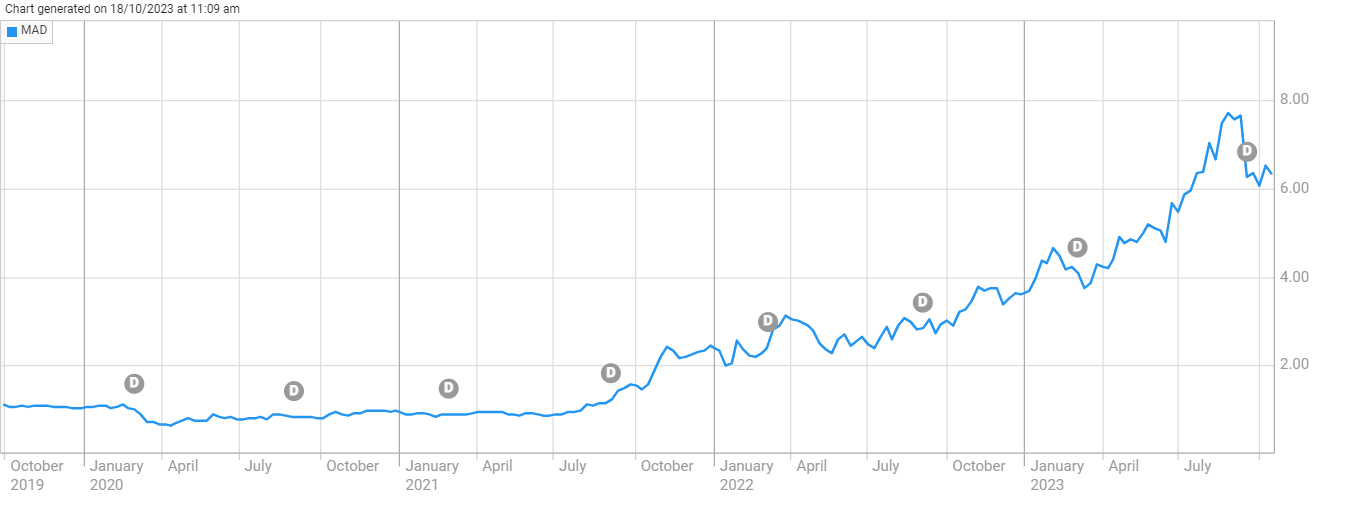

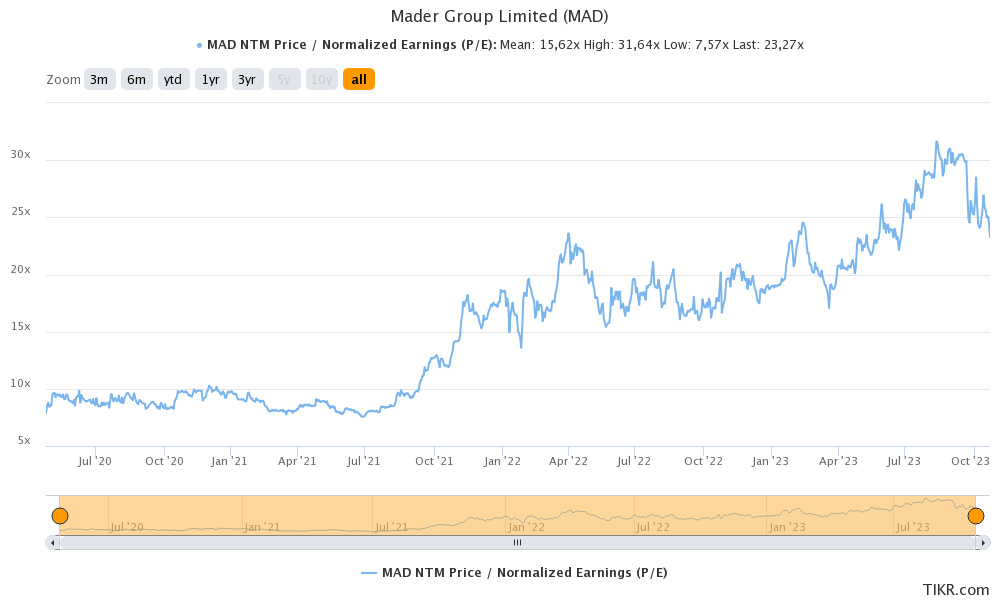

Despite the company increasing its valuation since the IPO, I still consider the stock to be undervalued given the expected growth.

{kind=link}

TIKR.com

Mader is currently at 23x next twelve months' earnings (NTM) and has been trading at a lower valuation for some time because is a relatively unknown company, trading in Australia, and with a market cap of under USD 1 billion. Given the quality of the business and the management, high ROIC, low competition, and its growth perspectives, I believe the current valuation is fair. In the conservative scenario, where I expect NPAT at AUD 90MM in 2028, even if valuation reduced to 25x LTM NPAT, the stock should be trading at AUD 10.5 (USD 6.65), providing a 14% CAGR plus dividends.

Risks

Mader is enjoying great momentum, but there are some potential risks that I consider important to track.

1) Labor Risks

The business model is highly reliant on its workforce, and I see this as the major risk over the long term. On one side, Mader could suffer shortages of skilled staff. In Australia, the labor market is tight and unemployment is low , which drives salaries up and makes it more difficult to retain skilled staff. They mitigate this risk with its strong business culture and reducing rotation through an above-market compensation salary. In North America, the company has found a more positive picture relating to staff, which has allowed it to enjoy higher margins:

The U.S. is certainly a lot easier to attract and retain staff over there. It's a different model. So people are able to sort of travel between states and do work in sort of different industries or different commodities. (Justin Nuich, 2Q 2022 Earnings Call )

On the other side, Mader could face the risk of over-hiring. This is not a risk in the short term since the company is growing faster than it is able to hire but is something to monitor when it enters into a more mature phase.

If there is a decline in demand for maintenance activities or a prolonged period of low commodity prices, they might be forced to adjust its staff. This could mean significant human capital losses given the company is investing in improving its employees' skills over years. To solve this risk, a portion of the staff is employed on a part-time or casual basis, which also gives flexibility to employees, letting them choose between different rosters .

2) Declining Demand

I don't expect to see a decline in demand soon, but any change in the trend toward outsourcing maintenance activities would have a significant effect over the long term. Mader already demonstrated its ability to perform under a commodity downcycle and benefit by recruiting employees who were laid off from mining companies, solving its long-term scarcity of skilled technicians.

On a downcycle, mining companies reduce their in-house staff and machinery acquisitions. As warranty periods expire on the current machinery, it means more revenue for Mader. In a positive scenario for mining, Mader can help by providing additional staff during work peaks, so I see it as a highly defensive business model.

3) Competition

Since Mader doesn't operate in the OEM warranty space, and small local operators can't compete from a service quality perspective, competition could come from a similar size company covering the same niche. Although smaller companies could increase in size, there are some barriers to entry such as attracting and retaining highly skilled tradespeople, business relationships, obtaining a vendor registration number from large mine owners, a track record of delivery, the ability to provide flexibility and a global network. As years go by and Mader continues increasing its presence in different regions and industries, I believe its competitive advantage becomes stronger.

4) Credit Risk

Despite the reduction in customer concentration and the geographical and service diversification, a significant proportion of the revenue comes from a group of key customers. A prolonged decline in commodity prices may lead to clients not meeting its financial obligations or terminating the relationship on a short notice period. To calculate expected credit losses, the company uses a provision matrix for trade receivables and has been reducing its collection period over the years.

Author (Data from Annual Reports)

5) Financial Risks

The two main financial risks any multinational needs to have under control are foreign currency risks and interest rate risks. Mader operates in currencies other than AUD, and to minimize the risk, management ensures both the customer contracts and recoverable costs are denominated in the same currency. Regarding interest rates, only 14% of its debt is based on floating rates, and total debt is low when compared to income, so I don't see any significant risks.

Conclusion

Mader ticks all the boxes on my checklist before investing in a business, it has high ROIC and the opportunity to reinvest in the business for many years, making it a potential compounder. The business model is scalable, the company has a huge addressable market, and is expanding geographically and by the number of services, increasing its competitive advantage. Its outstanding management with strong skin in the game knows every detail of the business and the day-to-day of its employees. Despite the significant increase in price, I consider the stock to be undervalued by 23% in a conservative scenario and by 53% on a base case scenario, assigning it a Strong Buy rating.

For further details see:

Mader Group: Expanding A Highly Profitable Business Model