AMZN - Magnificent 7 Growth Stock Valuations Irrationally Disconnected From Interest Rates

2023-08-04 06:02:49 ET

Summary

- Long-term interest rates are back near their 2022 highs, while mega cap growth stocks have defied interest rates and risen significantly.

- Rates are at risk of going higher following the Fitch downgrade of US Treasuries and should exert a gravitational pull downward on stock valuations.

- Earnings and growth estimates for most of the top 7 mega cap growth companies have either decreased or not improved much since November 2022.

- The MGK ETF should be avoided, along with its top stocks, until about half of the run-up since the bottom has been retraced.

Defying Gravity

Warren Buffett ( BRK.A ) ( BRK.B ) has stated that interest rates act like gravity on asset prices. In that 2019 interview, he noted that this applies equally well to stocks as it does to bonds. Both types of assets effectively have "coupons". In the case of bonds, the coupon is literally a fixed interest payment paid regularly until maturity. With stocks, Buffett said "It's the same sort of thing. It has a bunch of coupons; they just haven't printed the numbers on them yet." The challenge for investors is estimating the present value of these "coupons", or future earnings. Doing this requires a discount rate, which is simply a way to quantify the time value of money. The further out into the future an earnings stream occurs, the less it is worth today. Just as with bonds, higher interest rates lower the present value. This is the gravity that Buffett was talking about.

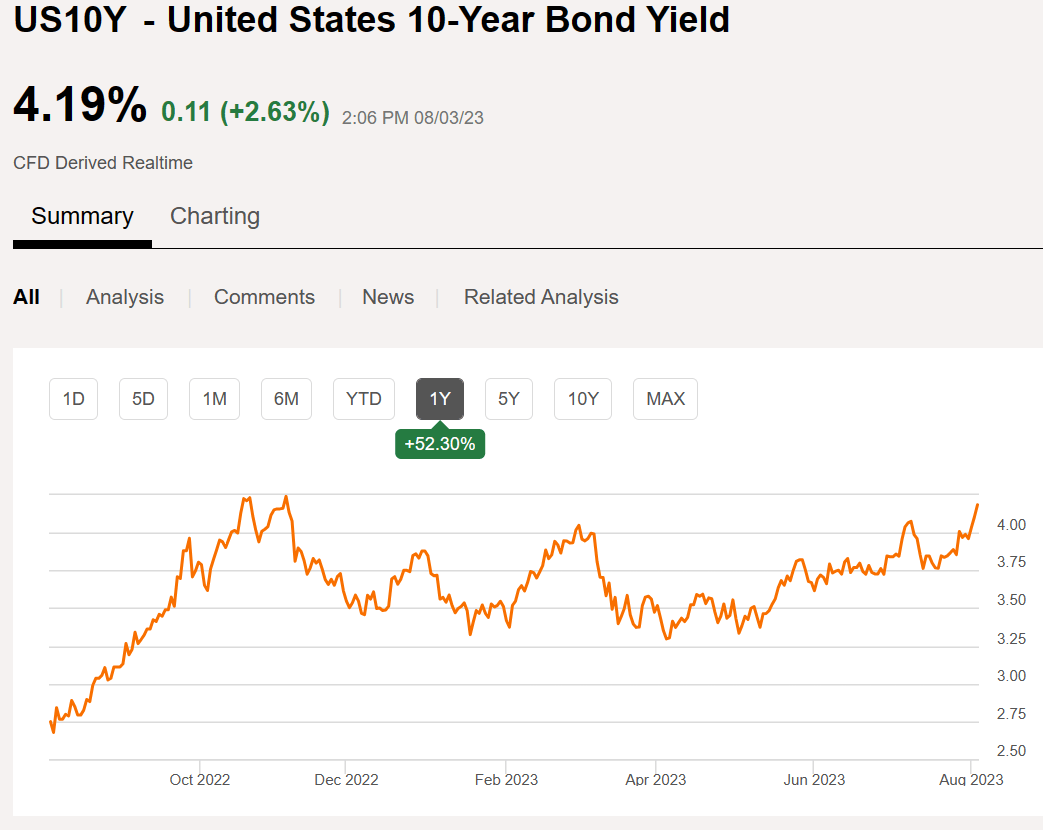

Most people reading this article are already familiar with the above concept, but it's worth mentioning in light of market action over the past 9 months. Long term interest rates as measured by the 10-year US Treasury note ( US10Y ) are back near the highs they reached in 4Q 2022.

{kind=link}

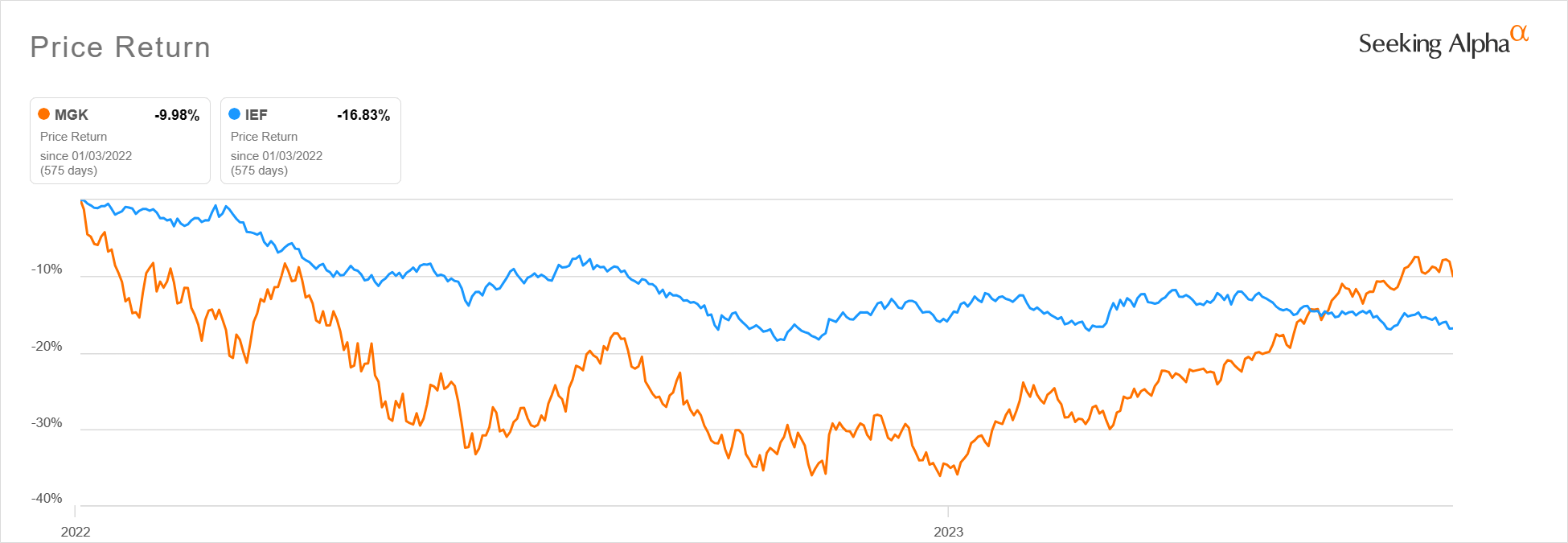

Over the same period, mega cap growth stocks, as measured by the Vanguard Mega Cap Growth Index Fund ETF ( MGK ) have completely defied interest rates and rocketed higher. MGK moved in parallel with bond prices for most of 2022 but have been completely uncoupled so far this year. Here is MGK compared with the iShares 7-10 Year US Treasury ETF ( IEF ).

{kind=link}

Other things being equal, MGK would be back down near the lows reached in 4Q 2022, not 40% higher. Of course, other things are never equal. If earnings estimates have improved considerably, or growth prospects are better, higher valuations would be justified. As I will show below, that is not the case for most of the big components of MGK. The only component of the valuation equation that has changed considerably is the risk premium. On average, the difference between the average earnings yield of the top 7 mega cap companies and the 10-year Treasury yield has declined 2 full percentage points, from +0.7% nine months ago to -1.3% today.

The Magnificent Seven

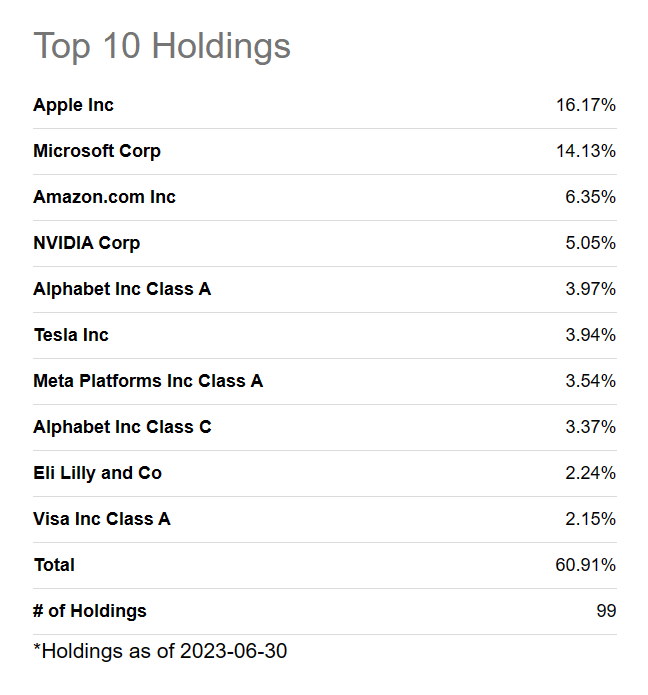

The top 7 mega cap growth companies (8 stocks thanks to Google's two share classes) make of 56.5% of MGK. As a reminder these include Apple ( AAPL ), Microsoft ( MSFT ), Amazon ( AMZN ), NVIDIA ( NVDA ), Alphabet ( GOOG ) ( GOOGL ), Tesla ( TSLA ), and Meta Platforms ( META ).

{kind=link}

These 8 stocks also make up 43.25% of the NASDAQ 100 ETF ( QQQ ) and 27.69% of the SPDR S&P 500 ETF ( SPY ).

I will be comparing 2023 and 2028 earnings estimates and the resulting implied 5-year growth rates for these stocks as they existed on 11/3/2022 and 8/2/2023. These historical values can be found on the Earnings Revisions page on Seeking Alpha for each stock.

2023 earnings estimates for the Magnificent 7 are now flat to lower than where they were in November 2022, except for NVIDIA and Meta. Tesla ( TSLA ) estimates are down considerable. As a high-end chip manufacturer, I can see NVIDIA benefitting the most from the growth in AI. In the case of Meta, the connection is a little less clear, or perhaps the estimates were too low in November because of the failure of the previous hot 2-letter acronym ((VR)) to result in tangible growth.

Author Spreadsheet

Looking at future earnings, the 2028 estimates show the same two stocks with improved estimates since November. Amazon joins Tesla, however, as a stock with significantly lower estimates.

Author Spreadsheet

From the above two charts, we can calculate the EPS growth rate for each stock. Several of these stocks have an improved growth rate. Amazon and NVIDIA are the two fastest growers, however the growth projections for these two have come down since November.

Author Spreadsheet

Looking at the averages for the overall group, 2023 EPS estimates have come up 13%, 2028 estimates have increased 23% since November. The 5-year EPS growth rate was estimated at 17.5% in November and 18.8% currently. With interest rates at about the same level, these modest improvements suggest share prices should be higher, but a 40% improvement in MGK seems excessive.

The PEG ratio (price / earnings growth) is a quick and dirty way to scale P/E to growth rate. It is not appropriate for slow growers or startups with low earnings but can be useful for established stocks with good growth rates like the Magnificent 7. What we see in most of these stocks is the share price increased far in excess of earnings while growth expectations also improved only slightly. The exception is Meta, which improved future earnings even more than the impressive improvement in current earnings, leaving the PEG ratio lower despite the more than tripling of the share price. Google is the only other name with a modest PEG ratio expansion. The others have all grown beyond 2, which is often considered an indicator of overvaluation.

Author Spreadsheet

Finally, the risk premium, or earnings yield minus 10-year Treasury yield, was positive for 4 stocks in November, with Meta and Google the best values. Currently, 5 out of the 7 are negative. Meta and Google are now only barely positive.

With long term interest rates now increasing following the Fitch downgrade of US Treasuries, the gravitational pull on asset prices should only get stronger. In the absence of more meaningful earnings estimate and growth rate increases, most mega cap growth stocks should be avoided until they are cheaper. This applies to ETFs like MGK and QQQ as well.

Investing Strategy

I would continue avoiding most of these stocks and ETFs until they retrace about 50% of the move between the November lows and current values. At that time, the valuations will be reasonable at least from a PEG viewpoint. The one exception to consider might be Google, which is practically a value stock by comparison. I liked Google back in October and would have pulled the trigger if I did not need the cash for personal reasons. If I was only going by the numbers, I would include Meta as well, but the future of social media and the company's product strategy is more questionable to me. VR has not generated much tangible benefit despite the company rename, AI strategy sill seems all over the place, and Threads is failing to take off despite all the unforced errors of X (Twitter).

If you own any of these names, consider at least trimming a portion, especially if you have tax losses from other sales to offset the gains. Also consider owning puts, either as a hedge against a current position or as a speculative play if you don't own the underlying stock. In the latter case, limit position sizes to a tiny (<1%) part of the portfolio. I tried this with QQQ puts in July and was unfortunately too early, but it only cost me the 0.25% of my portfolio that I risked. Covered calls are another strategy for current owners who are confident about the long-term prospects of their stock but would like to generate regular periodic income during a downturn. I would not short these names, simply because of the high potential losses if the market remains irrational.

Conclusion

The Magnificent 7 mega cap growth stocks which make up most of the MGK ETF have seen slightly improved earnings and growth estimates since their late 2022 bottom, but not enough to justify a 40% increase in MGK. Interest rates are now back where they were when MGK bottomed and risk increasing further since the Fitch downgrade of US Treasuries. A pullback for these stocks is now in order, especially if earnings estimates deteriorate. I suggest avoiding the group if not a current owner, and trimming or hedging if you are. A 50% retracement of the gains since the November bottom is a better level to consider owning most of these names.

For further details see:

Magnificent 7 Growth Stock Valuations Irrationally Disconnected From Interest Rates