PUBM - Magnite: Strong Cash Flows Will Matter Eventually

2023-11-27 12:50:44 ET

Summary

- Magnite's Q3 results showed mixed performance, with decelerating growth and improved profitability.

- Despite improving cash flows, weak guidance and macro challenges have prevented Magnite's share price from increasing.

- While there are reasons to be concerned about Magnite's business long-term, the company's valuation more than accounts for this.

Magnite’s ( MGNI ) third quarter results were mixed, with growth decelerating and profitability improving. Concerningly, Magnite gave weak guidance and management commentary suggested the macro environment remains challenging. Uncertainty and soft growth have prevented Magnite’s stock from moving higher, even with free cash flow generation improving significantly. I previously highlighted these issues and suggested that the tenuous competitive position of SSPs reduced the attractiveness of investing in Magnite, despite its low valuation. Magnite’s stock continues to look inexpensive for investors with a longer investment horizon, but the macro environment and uncertainty regarding long-term competitive positioning are substantial risks.

Market

Magnite reported fairly flat revenue YoY in the third quarter and suggested that the start of Q4 was soft, which was attributed to the macro environment. Magnite's DV+ business has been performing reasonably well, although this has been offset by CTV weakness.

Despite near term headwinds, it is obviously still early days for programmatic CTV advertising. Marquee publishers are just beginning to ramp ad supported streaming, causing inventory to be scarce . As a result, publishers are preferring to sell programmatic deals through their direct sales teams. While publishers are using Magnite’s technology to do this, programmatic direct carries a lower take rate. Buyers are eventually expected to purchase the majority of their CTV programmatically, using advanced data targeting, which should lead to greater ad spend and higher take rates for Magnite.

PubMatic’s ( PUBM ) guidance and commentary was more positive than most adtech peers. On its third quarter earnings call, PubMatic suggested that monetized impression growth has been solid, although this has been more than offset by weak CPMs. Market conditions reportedly improved through the third quarter and PubMatic's revenue increased around 5% YoY in October. Omnichannel video revenues were down approximately 4% YoY in the third quarter due to a soft July and CTV revenue declined 3% YoY. As a percent of total revenue, omnichannel video revenues increased to 33%. Display revenues were 67% of total revenue and declined 4% YoY.

The Trade Desk ( TTD ) reported reasonably strong results in the third quarter, but gave soft guidance and commentary which spooked investors. In particular, The Trade Desk suggested that spending by some advertisers (auto, electronics, M&E) was weak in October . Spending had reportedly stabilized by November though, and The Trade Desk remains optimistic about 2024. The Trade Desk’s view of CTV appears to be broadly similar to Magnite. CTV advertising is increasing but much of this isn’t biddable programmatic yet. Ultimately The Trade Desk expects CTV to catch up with consumer viewing behavior and for most CTV ad spend to be programmatic.

Roku's ( ROKU ) third quarter platform revenue growth was primarily the result of content distribution (subscriber growth and subscription price increases) and video advertising, offset by lower media and entertainment promotional spend. Video ads reportedly began to recover in the third quarter and Roku expects this strength to carry over into the fourth quarter. Unsurprisingly, video advertising on Roku is outperforming the overall ad market and the linear ad market in the US. The macro environment is still causing Roku to be cautious though. Ad verticals like CPG and health and wellness continue to improve, while verticals like financial services and M&E remain challenged. The fourth quarter also faces a difficult comparable period due to strong content distribution and M&E revenue in 2022.

Magnite

While Magnite has a large opportunity ahead of it, particularly in CTV, there are questions around competitive positioning and the value proposition of SSPs. Investors only need to look at how Magnite's business has been buffeted by technology changes in the past to understand some of the vulnerabilities.

CTV could have dynamics which are more favorable for SSPs though. For example, there is a limited number of CTV publishers and premium CTV inventory is relatively scarce, potentially providing the supply side with more bargaining power. Magnite also believes its CTV solutions are far stickier than the typical SSP model.

While Magnite's CTV business performance may currently look anemic, CPMs and a publisher preference for direct sales are causing revenue growth to trail ad spend. For example, Magnite’s CTV ad spend growth is over 20% indicating that the company is gaining market share. Magnite’s high take rate managed service business has also faced headwinds. Magnite expects CTV revenue growth to converge with ad spend growth over time as the mix shift stabilizes.

Supply path optimization is also an important trend for Magnite. Its ClearLine self-service solution enables agencies to purchase video inventory directly. Magnite believes this product will help unlock linear budgets and efficiently shift them to programmatic CTV. The market is likely to transition to biddable programmatic over time due to buyside pressures, but this is potentially an important transitory solution.

PubMatic has a comparable solution (Activate) which it has been developing over the past 18 months. Activate enables buyers to execute no-bid direct deals on CTV and premium video inventory through PubMatic’s platform. Activate was launched in May and provides SPO for premium CTV and online video inventory, which represents a 65 billion USD TAM expansion for PubMatic. In the first six months, PubMatic has built a pipeline of over 50 advertisers, agencies and campaigns. Activate was recently launched in the Asia Pacific region. Total activity from SPO deals grew to 45% in the third quarter, partly aided by Activate.

While Magnite is a potential beneficiary of supply path optimization, it also faces the threat of disintermediation from companies like The Trade Desk. Magnite has stated that so far it has only seen increased spend from The Trade Desk post-OpenPath though.

SPO also means that Magnite must be able to supply buyers with data. In support of this, Magnite recently partnered with Attain , to provide agencies buying video supply through ClearLine with purchase data. Magnite has stated that it plans on expanding Attain data availability beyond ClearLine soon though. Magnite is not alone in this endeavor, with PubMatic recently launching a self-service ad platform for commerce media and Criteo developing a new SSP dedicated to commerce. While SSPs do not have access to proprietary purchase data, they can provide value by helping provide advertisers access to consistent data.

Financial Analysis

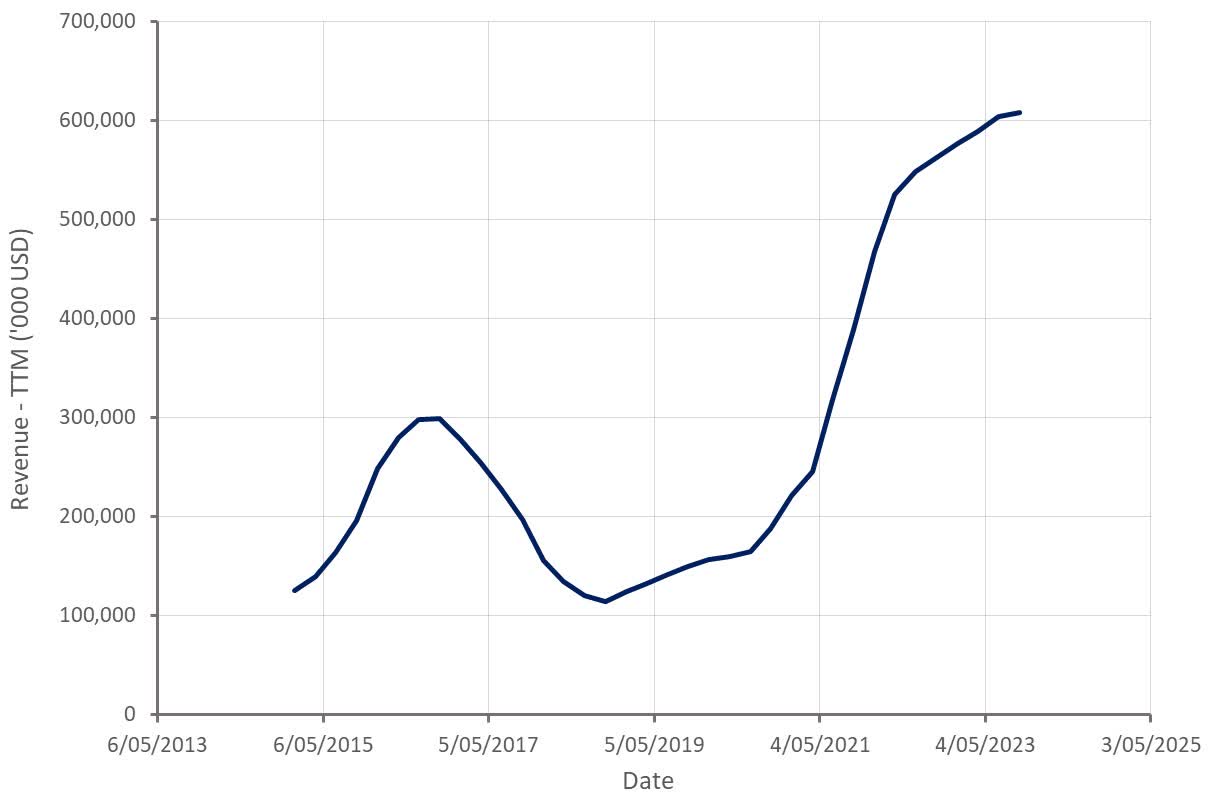

Magnite’s revenue increased 3% YoY in the third quarter to 150 million USD. CTV contribution ex-TAC was down 6% YoY while DV+ contribution ex-TAC increased 12%. CTV contribution ex-TAC was negatively impacted by expected softness in managed service and by mix shift. A difficult comparable period in 2022 due to political spending also created a 3% headwind.

Table 1: Magnite Contribution ex-TAC Growth (source: Created by author using data from Magnite)

Revenue in the US declined roughly 2% YoY in the third quarter compared to 22% growth internationally. International strength was attributed to the DV+ business and new publisher wins. Travel was the strongest performing vertical, while retail, financial services, and media and entertainment were areas of weakness.

Contribution ex-TAX is expected to be 158-162 million USD in the fourth quarter, roughly a 2% increase YoY. CTV contribution ex-TAC is expected to be 61-63 million USD (~4% YoY decline) and DV+ contribution ex-TAC is expected to be 97-99 million USD (~7% YoY increase). While political spend in 2022 creates roughly a 6% headwind, guidance is still soft.

For 2024, contribution ex-TAC growth is expected to grow in the high single digits, with CTV expected to outpace DV+. Magnite has stated that guidance reflects macro uncertainty, particularly related to the conflict in the Middle East.

Figure 1: Magnite Revenue (source: Created by author using data from Magnite)

{kind=link}

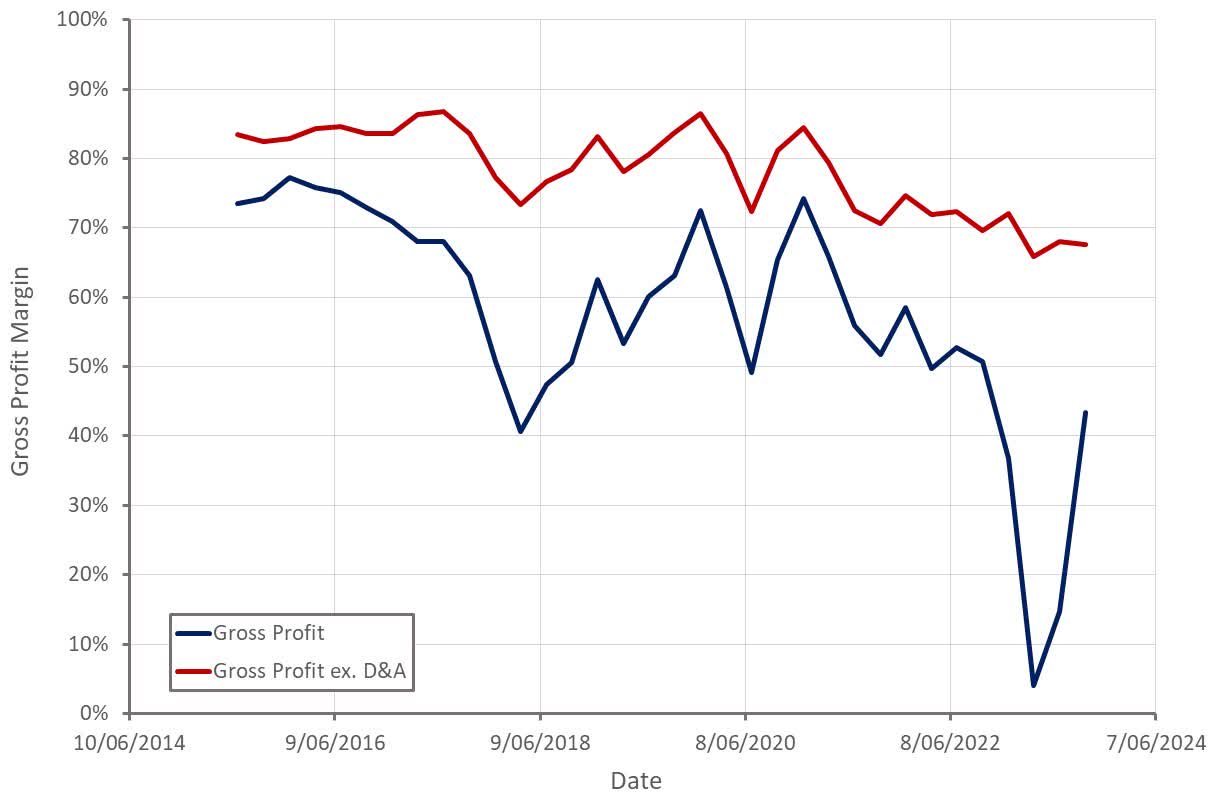

The recent decline in gross profit margins has primarily been the result of an accelerated amortization of intangible assets related to prior acquisitions. This process is now approaching an end though, causing gross profit margins to rebound sharply. Underlying profitability continues to deteriorate, likely driven by shifts in revenue mix and CPM weakness. Assuming Magnite can drive economies of scale with its infrastructure and CPMs stabilize or improve, gross profit margins should rebound in time. This is something that PubMatic is already expecting to occur in the fourth quarter of 2023.

Figure 2: Magnite Gross Profit Margin (source: Created by author using data from Magnite)

{kind=link}

{kind=link}

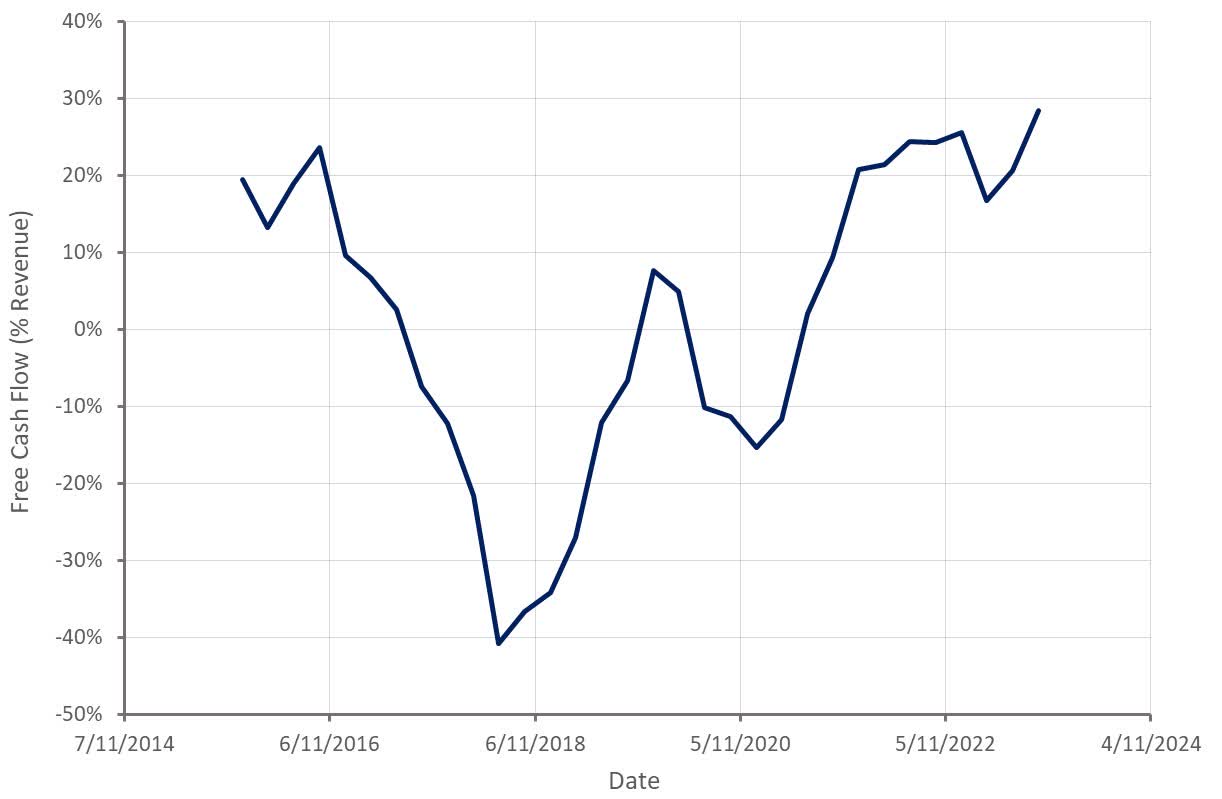

Magnite's operating expenses declined modestly YoY in the third quarter, with payroll being the primary cost driver compared to 2022. Adjusted EBITDA margin and free cash flows continue to expand on the back of cost controls and revenue growth. This improvement in profitability is yet to be reflected in Magnite's stock price, indicating an excessive focus by investors on near-term growth expectations.

Figure 4: Magnite Free Cash Flow Margin (source: Created by author using data from Magnite)

{kind=link}

Magnite is starting to generate substantial free cash flow, which is currently being directed towards strengthening the company's balance sheet. Magnite has reduced its total convertible note debt balance from 400 million USD to 275 million USD, and still has 70 million USD remaining under its current repurchase program (either common shares or convertible debt). Magnite also still has a 311 million USD cash balance, which increased from 266 million USD at the end of the second quarter.

{kind=link}

Conclusion

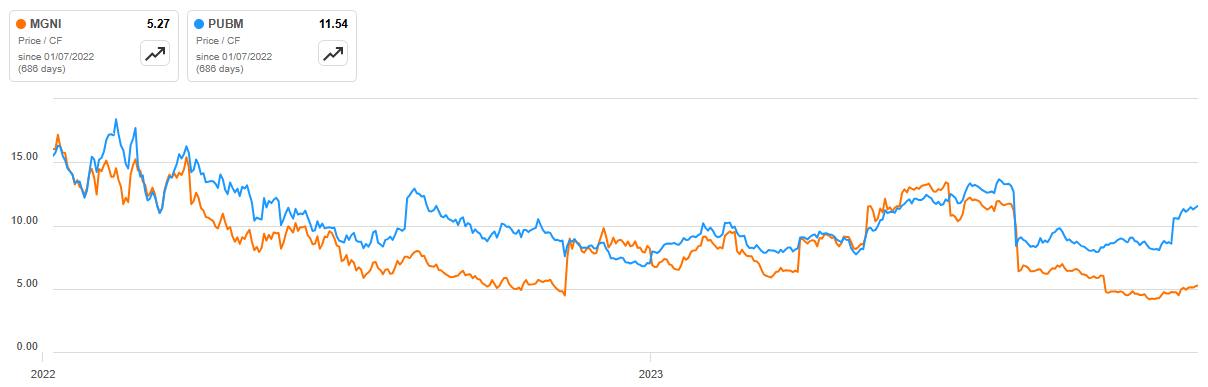

Magnite and PubMatic are similar companies with similar prospects, and as a result trade at a similar EV/S multiple. Magnite is a much larger company though and is currently generating more free cash flow. As a result, Magnite appears far less expensive based on a cash flow multiple. While PubMatic's margins should converge towards Magnite's over time, I would argue that Magnite deserves to trade at a modest premium. Regardless, both companies appear to be attractively valued, unless revenue and/or margins decline significantly.

{kind=link}

For further details see:

Magnite: Strong Cash Flows Will Matter Eventually