MNTX - Manitex International: Reweighting To Higher-Margin Exposure

2023-07-05 20:41:37 ET

Summary

- Manitex is gaining exposure to the higher-margin rental equipment business, which could provide decent profitability gains and recurring revenue streams throughout the cycle.

- Manitex delivered resilient top-line growth and strong profitability numbers during Q1 2023.

- I am more bullish on MNTX stock and believe that EBITDA margin run-levels above 10% could serve as a clear indication that the current valuation has upside potential.

The recent tilt of the revenue-mix to the higher-margin equipment rental solutions provides a decent growth opportunity for Manitex International (MNTX), which along with the resilient parts business could secure a solid revenue stream and support profitability through the cycles. I believe Manitex could hit a $300 million top-line target in 2023 thanks to the favorable and growing backlog as a result of the resilient demand from infrastructure projects, energy and general construction end-markets. I expect a profitability reading on the EBITDA line above the 10% line from Q2’23 onwards, which would be a clear indication that Manitex is executing properly on its strategy, and the current valuation is unsustainable. I am more bullish on MNTX since my previous article , as the company’s business is lined up more favorably to work out the supportive end-market demand and accumulated backlog.

Financial overview and outlook

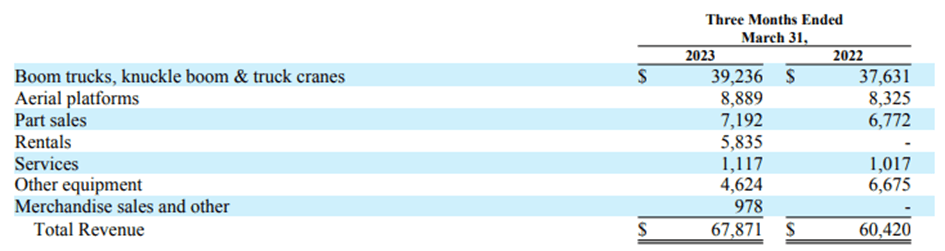

In Q1 2023, Manitex posted a strong growth of 12.3% YoY in the net revenue, benefiting from the pricing improvements despite the negative impact of lower truck chassis sales. The strong top-line performance was a result of the new offerings and mainly due to the contribution of Rentals solutions.

Financial results (company reports)

{kind=link}

Lifting solutions sales of $52.7 million were merely flat against the comparable period, mainly on lower other equipment revenue, while the breakdown shows mid-single digit growth rates in truck cranes solutions, aerial platforms and part sales. Still, the demand trends underlying the lifting equipment offerings are improving along with the improved throughput in manufacturing facilities, and adjusted to the lower truck chassis sales, the segment should have posted a 3.4% growth .

Going forward, the core business of MNTS has decent prospects due to the accumulated backlog of $238.1 million, which is accumulating faster than the revenue and was up by 16% YoY during Q1. In particular, the truck cranes sales were up by 4.3% YoY with the U.S.-based boom trucks business backlog up by 32% YoY. And despite the backlog for articulated cranes advancing slower, or by 13%, I am more bullish on the company’s PM business due to the growing adoption of knuckle boom trucks in the North American market. In the meantime, aerial work platforms (“AWPs”) continued to outpace the cranes business line, growing by 6.8% YoY. Overall, the strong order book accumulation points to the improvement in the end-market demand trends and provides a reasonable assurance that the company’s core lifting solutions business could grow by resilient single digit numbers. This could be the case following the infrastructure bill , expansion and modernization of the old national electric grid and the energy exploration investment gap .

Moving to the point, the acquisition of Rabern Rentals strengthened the company’s top-line mix with $5.8 million revenue. The rental business line benefited from a new fleet deployment, which was supported by strong demand in the company’s key Texas market. Part sales continued to deliver resilient growth (6.8% YoY), delivering $7.2 million in revenue, which along with the contribution of Rabern is shaping a significantly more favorable revenue-mix. The two business segments accounted for 19.2% of the consolidated top-line in Q1, which gives MNTX a solid fulcrum for profitability gains, since the mentioned LOBs feature a higher-margin profile. Moreover, the part sales and rental equipment tend to increase during turbulent times, hence their share in the revenue-mix, which could allow the company to withstand a downturn with more resilient profitability numbers.

Meanwhile, the company achieved its short-term gross margin target of 20-22%. In addition to the prominent Rabern contribution and the improved mix, MNTX’s operational improvement initiatives and favorable pricing brought a 440bps YoY improvement in gross margin, which settled at 21.1% during the quarter. It’s worth noting the favorable pricing, which means that the accumulated backlog is booked at higher and more favorable terms. Moreover, the backlog could showcase further growth, as the customers’ interest in the Manitex offerings during the CONEXPO trade show was not fully reflected in Q1 closing backlog.

Backlog (company presentation)

Adjusted EBITDA for the quarter came at $6.3 million on a 9.3% margin. Although the profitability deteriorated from 10.3% in Q4 2022, I believe the company is now in better condition to hit the EBITDA margin run levels of >10%.

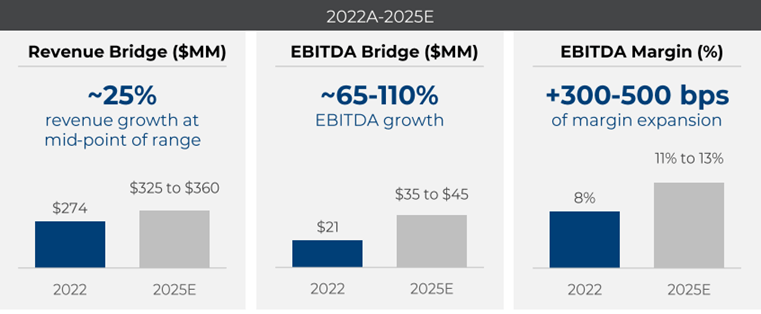

Meanwhile, the company is clearly executing its Elevating Excellence long-term targets. In particular, with the strong contribution of the rental business line coupled with the launched electric crane systems and the new high-capacity 85-ton lifting truck, I believe that the revenue could confidently cross the $300 million bar and strive to the $340 million midpoint number in the FY2025, since Manitex is going to leverage its leadership position in the straight mast cranes in order to pull up articulated, AWP and rental solutions.

Financial targets (company presentation)

{kind=link}

The current reweighting of the product mix toward higher-margin rental and parts offering, and the ongoing production efficiency initiatives could fill the delineated long-term EBITDA margin gap to 13%. And despite the headwinds from the current macro environment, the company undergoes supportive industry conditions:

Many of our key verticals are less impacted by general economic swings and are instead driven by infrastructure spending and the energy markets. General infrastructure, electrical distribution and road construction are all benefiting from federal infrastructure and stimulus money. We are also seeing global demand for minerals such as copper, improve capital goods spend and mining maintenance activities.

However, this revenue growth is facing a significant constraint going across the operating line due to the high leverage position. The $1.8 million interest expense was the main factor that pressed the bottom line down to breakeven. The acquisition of Rabern came at a “high price” against the backdrop of elevated interest rates, which led to the net debt position of $86 million. However, the strong EBITDA growth during the quarter (+131% YoY on adjusted basis) tamed the net leverage ratio down to 3.5x from 3.9x in 2022.

Risk factors

The demand for truck-mounted lifting solutions exhibits a cyclical pattern and the aggravation of the macro environment could put on hold the execution of infrastructure investments and projects. The prolonged demand weakness in the main end-markets and further supply chain bottlenecks could result in a revenue deceleration and backlog erosion, leaving the company in a difficult position with significant IB debt liabilities.

Investment takeaways

Switching to the valuation, MNTX stock is currently trading at an EV/EBITDA forward multiple of 8.1x, which is below the average levels and represents a 26.4% discount to the sector average of 11x, according to the Seeking Alpha valuation screamer.

The executives mentioned during the earnings call at least 10% adjusted EBITDA growth in FY2023, stipulating a $23.5 million figure. The latter implies a 7.8% EBITDA margin to my sales forecast of $300 million (+9.5% YoY), and puts Manitex on a 7.8x EV/EBITDA multiple. Incorporating the sector’s median, the enterprise value should arrive at $259 million and decompose to $189 million equity value following the adjustments. The valuation implies a 69% upside potential from current levels up to $9.20 per share target price. It’s worth noting that the TTM EBITDA is $24.8 million, which is already higher than the one incorporated in the valuation. Still, I would rather remain conservative and watch the evolution toward elevating excellence, as the current valuation is unsustainable against the backdrop of the strategy, in my view. And despite Manitex already taking the right steps, the main restraining factor remains IB debt, which is wiping out all of that positive financial performance at the bottom-line so far. Thus, a key point in the short-term is whether MNTX can get to the 10%+ EBITDA margin run levels, which would be a clear sign that incorporating a $23.5 million EBITDA for the valuation purpose is unsustainable.

Looking at the MNTX performance, the sock has gained about 40% so far this year. This is against the backdrop of industrial sector stocks, represented by Industrial Select Sector SPDR ETF ( XLI ) in the following chart, which have gained 10% on average since the beginning of the year, meaning that the company is outperforming the sector as a whole.

And to sum up, I am upholding the main thesis outlined in my previous piece that the company's business is now positioned better to meet the heavy investments in infrastructure projects, positive trends in key end-markets and a fleet replacement/expansion cycle. And indeed, it’s gradually reflected in financial performance. My key short-term expectations are for gross margin profitability of 20-22% and EBITDA margin of 10-11%. This target seems to me quite reasonable to be sustained once the company achieves a 20%+ contribution from higher-margin segments in the revenue mix.

My call remains for a Buy action on MNTX sock, as I am more inclined to believe that continued new orders accumulation, expansion of the rental LOB and operating improvement could result in a sustainable profitability improvement.

For further details see:

Manitex International: Reweighting To Higher-Margin Exposure