MSFT - Mawer Investment Management Quarterly Update - Q1 2023

2023-04-14 20:00:00 ET

Summary

- Mawer Investment Management is a privately owned, independent investment firm, managing over $67B in assets for individual and institutional investors across all major asset classes.

- Equity markets were resilient in the first quarter of 2023, finishing with a strong positive return despite ongoing recession risks.

- Our equity strategies delivered positive returns in the first quarter, with European markets outperforming Canada and the U.S. after previously facing headwinds in 2022.

- We tend to emphasize non-predictive decision making that focuses on steering away from areas where vulnerabilities are sharpest as opposed to forecasting specific events.

Market overview

Equity markets were resilient in the first quarter of 2023, finishing with a strong positive return despite ongoing recession risks. Markets benefitted from a combination of factors including inflation falling in some regions, the anticipation by market participants that the U.S. Federal Reserve may be nearing the end of its rate hike cycle, and reduced fears of a hard landing for the economy. At the same time, corporate earnings have been quite resilient. In Canada, inflation continued to ease, and the Bank of Canada paused further hikes to allow the impacts of previous tightening to make their way through the economy. Canadian bonds also finished in positive territory as yields fell across the curve. That said, the market’s advance was far from a straight line. Both equities and bonds experienced volatility, especially in connection to the bank collapses in the U.S. and Europe which sent reverberations across the world. While the possibility of further instability remains, swift intervention seemed to have restored confidence and prevented contagion across the broader banking industry.

How did we do?

Our equity strategies delivered positive returns in the first quarter, with European markets outperforming Canada and the U.S. after previously facing headwinds in 2022. While many equities were up in the quarter, significant strength in a handful of large, high growth technology-focused companies were a significant driver of the advance for equity markets.

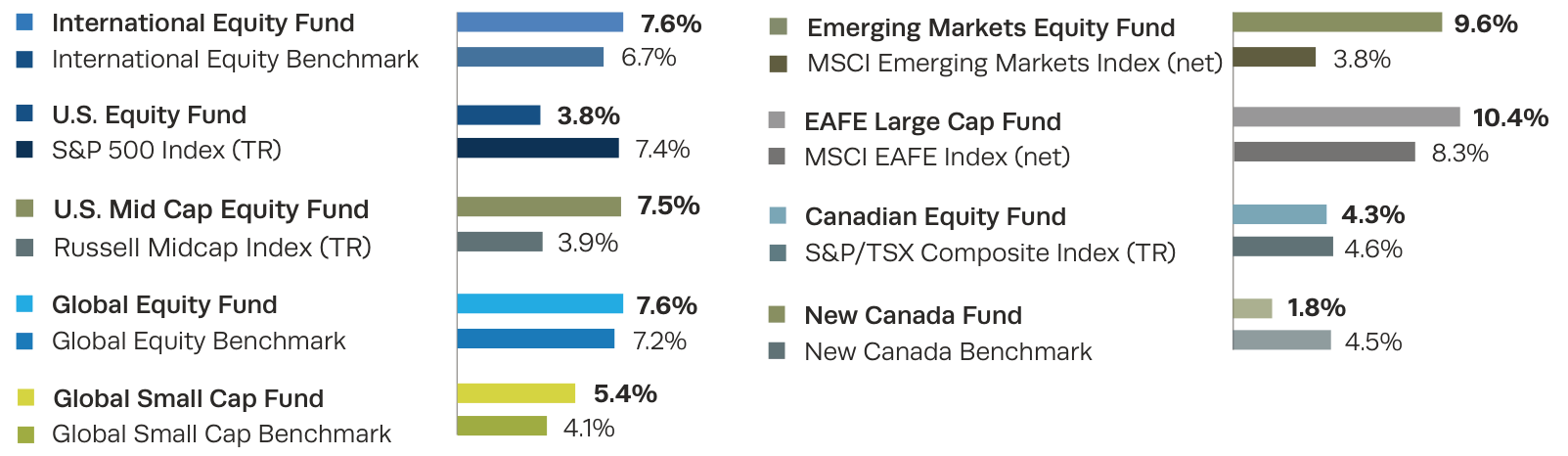

Equities: Chart A: Q1 2023, Series O, Gross of fees

{kind=link}

| Performance has been presented for the O-Series Mawer Mutual Funds in Canadian dollars and calculated gross of management fees and net of operating expenses for the 3-month period of January 1, 2023 - March 31, 2023. |

Many of the companies that faced stock price headwinds in 2022 as interest rates were rising performed well in the first quarter of 2023. Higher growth technology-focused businesses were some of the strongest including Microsoft ( MSFT ) , Alphabet ( GOOG , GOOGL ) , and Amazon ( AMZN ) , backed by falling discount rates and enthusiasm tied to cost containment measures. Elsewhere, several high-quality stalwarts and long-standing holdings had strong returns including luxury goods conglomerate LVMHF , and reference data providers Wolters Kluwer ( WOLTF ) and RELX . Holdings in defense companies such as Rheinmetall ( RNMBF ) , Thales ( THLEF ) , and BAE Systems ( BAESF ) also performed well reflecting expectations for structurally higher defense spending by NATO countries.

Conversely, many banks struggled in the quarter as the industry faced challenges as a result of the well-publicized collapse of Silicon Valley Bank and Credit Suisse. Generally, our equity portfolios have lower exposure to banks than their benchmarks, and we tend to focus on well-run, conservative banks that have clear competitive advantages in the markets in which they operate. Even so, several of our bank holdings lagged in the quarter including Italian bank FinecoBank ( FCBBF ) , Swedish bank Handelsbanken ( SVNLF ) , and Canadian bank TD .

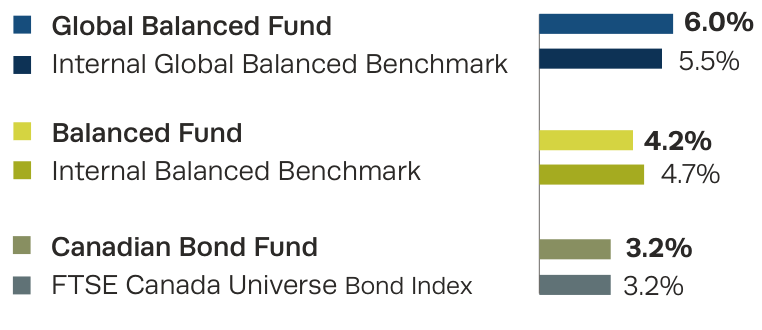

Balanced and Canadian Bond: Chart B: Q1 2023, Series O, Gross of fees

{kind=link}

After a challenging year in 2022, balanced investors benefitted from a rise in equity markets and Canadian bonds in the quarter. Canadian Bonds advanced as yields fell across the curve in the period with longer duration and high-quality bonds outperforming.

We made a change to our asset mix targets earlier in the quarter and increased modestly our Canadian bonds target, though we still remain underweight Canadian bonds relative to our benchmark until we feel there is a better sense of whether central banks’ battle with inflation is over. Our overall equity weight also FTSE Canada Universe Bond Index remains near neutral.

Looking ahead

We have often noted that one of the major risks facing markets is if something breaks when major macroeconomic variables shift quickly. And indeed, after one of the fastest periods of policy interest rate hikes by central banks, some less well-managed banks in the U.S. and Europe needed to be rescued. The possibility of further instability remains, although for now confidence in the banking system appears to be restored.

A high level of uncertainty remains not only with how high the U.S. Federal Reserve will go with the federal funds rate, but also how long it remains elevated. The tightening of credit as a result of U.S. regional bank turmoil may impact economic activity, and while a pause by the U.S. Federal Reserve may be near, challenges abating U.S. inflation partially caused by a tight employment market may require rates to stay higher. There is also often a lag between monetary policy and the resulting economic impact. We are not trying to predict the next move for policy makers, but rather ensuring our portfolios are resiliently positioned for a variety of scenarios.

With uncertainty as to the path forward, there are bound to be other unanticipated surprises on the horizon. Even the strongest businesses have vulnerabilities that can be exposed by the right trigger. This is why we tend to emphasize non-predictive decision making that focuses on steering away from areas where those vulnerabilities are sharpest as opposed to forecasting specific events. This requires a disciplined investment process, a culture in which different points of view are celebrated, and appropriate diversification that builds natural contradictions into the portfolios. And even though this “boring” approach may sacrifice possible short-term gains in certain market environments, we believe it should lead to better and more consistent outcomes over time.

As we often say it is difficult to predict when the tides will change for the better or for the worse. That is why we prepare, rather than predict.

| This document is for informational purposes only. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the fund facts and the prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. Mawer Funds are managed by Mawer Investment Management Ltd. Mutual fund securities are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. This Mawer Quarterly includes certain statements that are “forward looking statements.” All statements, other than statements of historical fact, included in this report that address activities, events or developments that the portfolio advisor, Mawer Investment Management Ltd., expects or anticipates will or may occur in the future, including such things as anticipated financial performance, are forward looking statements. The words “may”, “could”, “would”, “should”, “believe”, “plan”, “anticipate”, “expect”, “intend”, “forecast”, “objective” and similar expressions are intended to identify forward looking statements. These forward looking statements are subject to various risks and uncertainties, including the risks described in the Simplified Prospectus of the Fund, uncertainties and assumptions about the Fund, capital markets and economic factors, which could cause actual financial performance and expectations to differ materially from the anticipated performance or other expectations expressed. Economic factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. All opinions contained in forward looking statements are subject to change without notice and are provided in good faith but without legal responsibility. The portfolio advisor has no specific intention of updating any forward looking statements whether as a result of new information, future events or otherwise, except as required by securities legislation. Certain research and information about specific holdings in the Fund, including any opinion, is based upon various sources believed to be reliable, but it cannot be guaranteed to be current, accurate or complete. It is for information only, and is subject to change without notice. Index returns are supplied by a third party—we believe the data to be accurate, however, cannot guarantee its accuracy. Index returns are sourced from FTSE Russell, FactSet, and BMO Capital Markets. Performance returns for the Mawer Mutual Funds and benchmarks are calculated by Mawer Investment Management Ltd. These returns are historical simple returns for the 3 month, YTD, and 1 year periods, and annualized compounded total returns for periods after 1 year. Non-performance related material in this document reflects the opinions of the writer, and does not reflect fact or predictions of actual events or impacts, and cannot be relied upon for investing purposes or as investment advice or guarantees of any kind. MSCI Disclaimer: The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com) FTSE Disclaimer: London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2023. FTSE Russell is a trading name of certain of the LSE Group companies. FTSE® is a trade mark(s) of the relevant LSE Group companies and is/are used by any other LSE Group company under license. “TMX®” is a trade mark of TSX, Inc. and used by the LSE Group under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Mawer Investment Management Quarterly Update - Q1 2023