META - Mawer Investment Management Quarterly Update - Q2 2023

2023-07-19 13:50:00 ET

Summary

- Mawer Investment Management is a privately owned, independent investment firm, managing over $67B in assets for individual and institutional investors across all major asset classes.

- Globally, equity markets continued to be resilient in the second quarter, with U.S. equities being among the stronger performers.

- The recent advancements in AI highlighted how technology continues to bring change, disruption, and new possibilities to the way people engage in everyday activities.

- The yield curves in many major economies remain inverted, likely signalling we are heading towards a recession, the severity and timing of which is still highly uncertain.

Market Overview

Globally, equity markets continued to be resilient in the second quarter, with U.S. equities being among the stronger performers. U.S. equity strength was driven by a handful of large technology-focused companies, including some that have been in the spotlight as notable advancements in artificial intelligence dominated news headlines. Meanwhile, Chinese equities declined in the quarter as growth anticipated from the lift in COVID-19 restrictions fell short of expectations.

In Canada, headline inflation declined while GDP growth and the employment market remained resilient despite the challenging monetary policy environment. Ultimately, the Bank of Canada reconfirmed their commitment to fighting inflation as it raised the policy interest rate 0.25% in the quarter. With yields rising over the period, Canadian bonds declined.

The Canadian dollar appreciated this quarter against many currencies, reducing the return of foreign asset classes. One notable exception was the British pound, which strengthened relative to the Canadian dollar as the Bank of England raised interest rates 0.50% in June. The Japanese yen also experienced notable weakness in the period.

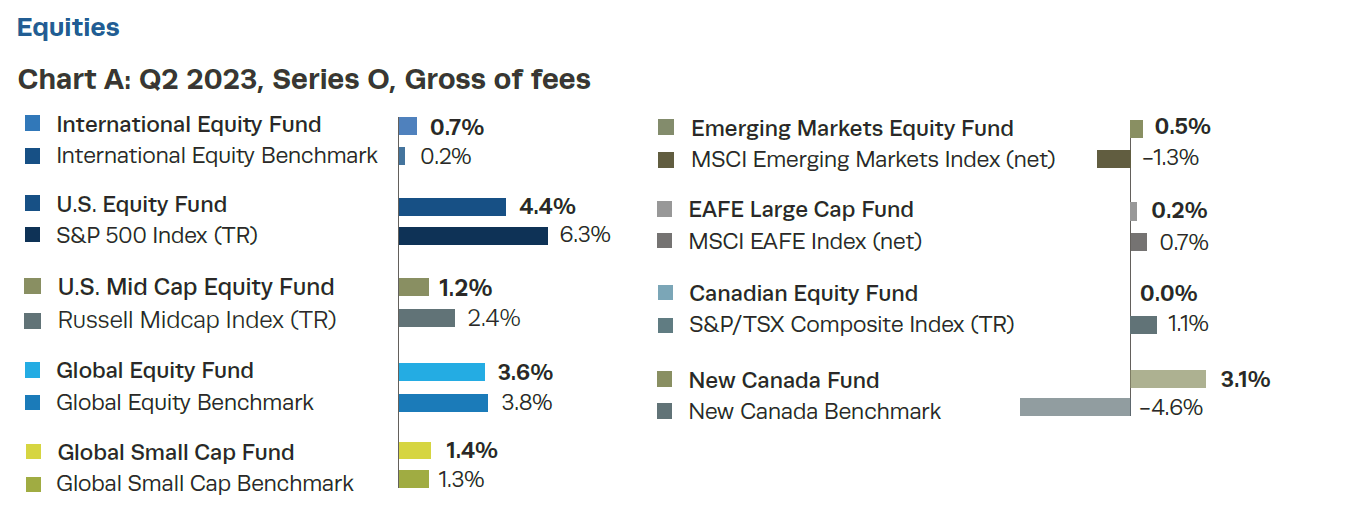

How Did We Do?

Performance has been presented for the O-Series Mawer Mutual Funds in Canadian dollars and calculated gross of management fees and net of operating expenses for the 3-month period of April 1, 2023-June 30, 2023.

{kind=link}

The recent advancements in artificial intelligence ((AI)) highlighted how technology continues to bring change, disruption, and new possibilities to the way people engage in everyday activities. Of significance is how fast AI is being integrated into common use. For example, how quickly Microsoft incorporated AI into their search engine, Bing. While the full impact of artificial intelligence’s capabilities is yet to be seen, markets are forward-looking, and rewarded some of the companies potentially positioned to benefit from this advancement in the quarter such as Apple ( AAPL ), Microsoft ( MSFT ), NVIDIA ( NVDA ), Amazon ( AMZN ), Meta ( META ), Tesla ( TSLA ), and Alphabet ( GOOG ) ( GOOGL ).

Of those listed, we hold Microsoft , Amazon , and Alphabet . While these technology businesses were some of our stronger performers, our relative underweight to the collective group was a headwind for relative performance.

In contrast to the businesses that may benefit from AI advancements, for others, the impact is less clear. One holding example is the call center operator, Teleperformance ( TLPFF ) ( TLPFY ). While it may be positioned to leverage artificial intelligence to more efficiently serve customers, the driving concern is future, incredibly sophisticated chatbots which may reduce the need for call centers. Considering these potential risks and benefits, we have done scenario analysis around the company’s revenue, margins, and their ultimate impact on the valuation of the company. Teleperformance was one of our weaker performers in the quarter after the market also negatively reacted to its offer to acquire a competitor.

When assessing the AI theme and considering our investment horizon, the full, possible impact of artificial intelligence developments is difficult to ascertain. That said, in our experience, rapid technological change tends to drive a wedge between high-quality management teams and weaker ones. To use a surfing analogy, artificial intelligence has the potential to be a monster wave - great management teams will catch it and surf it by improving their value proposition to customers and reducing their costs. Thus, a continued focus on great management teams - as opposed to forecasting specific winners and losers associated with a given theme - will help guide our approach.

Elsewhere, Compass Group ( CMPGF ) ( CMPGY ), the world’s largest catering company, continued their strong post-pandemic recovery. Despite the many challenges facing the catering industry, the company now earns more revenue than it did pre-pandemic. A more difficult operating environment has hurt many of its less-adept competitors, while customers are also choosing to outsource more of their catering - a combination that has provided Compass Group with opportunities to gain market share, thereby strengthening its competitive advantage.

Several of our weaker performers include those impacted by lower demand from both larger pharmaceutical customers and smaller biotech firms. Sartorius Stedim Biotech ( SDMHF ) ( SRTOY ), which provides equipment and consumables used at various stages in the production of biologic drugs, cut its guidance for the year ahead, and two life sciences companies also faced headwinds - Waters and Bio-Rad ( BIO ) ( BIO.B ).

The Mawer Balanced Fund delivered slightly positive returns in the quarter and narrowly outperformed its benchmark, supported by the outperformance of our Canadian small cap equity strategy. Meanwhile, the Mawer Global Balanced Fund delivered positive returns and performed in line with its benchmark. While our balanced strategies benefitted from positive returns from equities in the quarter, our Canadian bond strategy experienced modest declines as rising yields impacted bond prices.

Within our balanced strategies, we trimmed our target equity weight on two occasions during the quarter as equities rallied from their lows. We offset the trims by increasing our target allocation to Canadian bonds and cash. Overall, we believe this adds resilience, given the many scenarios that may unfold. Even though the market consensus appears to be calling for a soft landing, the macro picture remains very uncertain: inflation is moderating but still elevated, labour markets are resilient, the recovery in China’s economy seems lackluster, and geopolitical tensions remain.

Looking Ahead

The yield curves in many major economies remain inverted, likely signalling we are heading towards a recession, the severity and timing of which is still highly uncertain. With the market remaining hopeful for a soft landing, any perceived deviation from this path could result in volatility for equities. The renewed fight against inflation after a previous pause by the Bank of Canada also points to a potential prolonged period of higher interest rates ahead, an outcome that is also likely in Europe and the United States.

While the banking sector appears to have stabilized for now, the risk of something breaking remains. One well-reported area of concern is commercial real estate, a segment that is experiencing high vacancies and an uncertain outlook given the work-from-home theme.

To prepare against the risks, we’ve leaned into our bottom-up approach. Our investment philosophy naturally leads us to businesses with more stable demand, given the criticality of the products and services they provide to their customers. Our forensic accounting checklist is designed to ensure that we avoid getting caught up in narrative and, instead, methodically comb through financial statements for clues with respect to changes in business or management quality. In the current environment, and especially as COVID-19 supply shocks have encouraged many companies to build up their inventories, companies with excess inventory levels may face margin pressures in the coming quarters should demand abate from its current trend. As such, in addition to continuing to understand how companies are coping with inflation, we’re looking closely at cash conversion and days of inventory, especially when coupled with valuation levels that, year-to-date, have outpaced earnings.

With recession uncertainty still clouding the outlook, we continue to focus on maintaining the course, sticking with the key tenets of our investment philosophy, being balanced, and prepared for a variety of different scenarios.

DisclaimersThis document is for informational purposes only. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the fund facts and the prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. Mawer Funds are managed by Mawer Investment Management Ltd. Mutual fund securities are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. This Mawer Quarterly includes certain statements that are “forward looking information” or “forward looking statements” (collectively, “forward looking information”) within the meaning of applicable securities legislation. All statements, other than statements of historical fact, included in this report that address activities, events or developments that the portfolio advisor, Mawer Investment Management Ltd., expects or anticipates will or may occur in the future, including such things as anticipated financial performance, beliefs, plans, goals, objectives, assumptions, information and statements about possible future events, conditions, results of operations, are forward looking information. The words “may”, “could”, “would”, “should”, “believe”, “plan”, “anticipate”, “expect”, “intend”, “forecast”, “objective”, “will” and similar expressions are intended to identify forward looking information. Undue reliance should not be placed on forward looking information. Forward looking information is subject to various risks described in the Simplified Prospectus, uncertainties, and assumptions about the Fund, capital markets and economic factors, which could cause actual results to vary and in some instances to differ materially from those anticipated by the portfolio advisor and expressed in this report. Material risk factors include, but are not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition, technological change, changes in government regulations, unexpected judicial or regulatory proceedings, and catastrophic events. The foregoing list of risk factors is not exhaustive. All opinions contained in forward looking information are subject to change without notice and are provided in good faith and are based on the estimates and opinions of the portfolio advisor at the time the information is presented. The portfolio advisor has no specific intention of updating any forward looking information whether as a result of new information, future events or otherwise, except as required by securities legislation. Certain information about specific holdings in the Fund, including any opinion, is based upon various sources believed to be reliable, but cannot be guaranteed to be current, accurate or complete and is subject to change without notice. Index returns are supplied by a third party - we believe the data to be accurate, however, cannot guarantee its accuracy. Index returns are sourced from FTSE Russell, FactSet, and BMO Capital Markets. Performance returns for the Mawer Mutual Funds and benchmarks are calculated by Mawer Investment Management Ltd. These returns are historical simple returns for the 3 month, YTD, and 1 year periods, and annualized compounded total returns for periods after 1 year. Non?performance related material in this document reflects the opinions of the writer, and does not reflect fact or predictions of actual events or impacts, and cannot be relied upon for investing purposes or as investment advice or guarantees of any kind. MSCI Disclaimer: The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com) FTSE Disclaimer: London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2023. FTSE Russell is a trading name of certain of the LSE Group companies. FTSE® is a trade mark(s) of the relevant LSE Group companies and is/are used by any other LSE Group company under license. “TMX®” is a trade mark of TSX, Inc. and used by the LSE Group under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Mawer Investment Management Quarterly Update - Q2 2023