WMB - MEGI: Deep Discount Persists Presenting An Opportunity

2023-04-27 15:33:00 ET

Summary

- MEGI continues to trade at a wide discount but seems to be finding a bottom in this general region.

- Since the launch, the underlying portfolio has performed relatively well compared to similar funds.

- It is due to a substantial drop in the fund's share price return that has created this deep discount and opportunity.

- More recently, the fund has started to pull away in terms of its performance compared to these same popular peers.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on April 13th, 2023.

MainStay CBRE Global Infrastructure Megatrends Fund ( MEGI ) continues to trade at an excessively large discount, which can represent an opportunity for closed-end fund investors. The fund's performance has been about in line with similar peers since its launch. Perhaps more interestingly, though, the fund has been starting to lead peers in performance through 2023 so far.

While the continued outperformance would be anyone's guess going forward, we know that the valuation appears right. That's half the focus of investing in CEFs: finding opportunities to exploit discounts/premiums. Since our last update later in 2022, when I flipped to a "Buy" rating, the fund has done quite well, too. However, this didn't come from discount contraction at all, as the discount remains virtually the same.

MEGI Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -0.95

- Discount: 16.48%

- Distribution Yield: 8.84%

- Expense Ratio: 1.47%

- Leverage: 27.39%

- Managed Assets: $1.204 billion

- Structure: Term (anticipated liquidation date, December 15, 2033)

MEGI is your fairly standard closed-end fund , with the fund "seeking a high level of total return with an emphasis on current income."

To set this fund apart, the fund's twist compared to other infrastructure or utility funds is a "thematic theme." They are "focused on the investment megatrends of decarbonization, digital transformation, and asset modernization, which are reshaping the demand for infrastructure assets and driving income and growth potential."

The fund launched near the end of 2021, so it doesn't necessarily have the longest history. It's also a term fund, meaning that there is an expected liquidation date in the future. That can be exploited but is more of a concern as we get closer to that date. At this point, it could still be worth mentioning even ten years out because of having such a large discount.

This fund manager is New York Life Investments, and the subadvisor is CBRE Investment Management Listed Real Assets. Despite being a small presence in the CEF space, they were able to raise a fair bit of capital to get this fund up and running. Over $1 billion in assets is actually quite large for a CEF. Of course, some of this is thanks to the leverage. This leverage increases both the upside potential but also the downside moves.

Due to the fund's line of credit being based on the overnight bank funding rate plus 0.75%, we know that their borrowing costs have been rising. This was something that I mentioned previously, and it has been a headwind since they weren't hedged. They continue to be unhedged at this time, according to their last semi-annual report .

In hindsight, employing some interest-rate swaps or trying to get some fixed-rate financing would have helped. However, hedging also comes with costs that need to be weighed. It's very easy to look back and say that one should have hedged after the fact. So I don't see this as an unwise move from the management, as plenty of even larger fund sponsors went in unhedged through 2022 as well, but it is something that one should consider.

Performance - Discount Remains Deep

Since the fund's launch, the fund's total NAV return performance has been quite similar to other popular infrastructure/utility funds. I've included a comparison to the quite popular Cohen & Steers Infrastructure Fund ( UTF ) and Reaves Utility Income Fund ( UTG ).

YCharts

Bearing in mind trying to find peers for CEFs can be quite difficult. Even these 'peers' hold quite different positions, and MEGI has a higher allocation to international investments relative to these two. As we touched on above, MEGI's twist is also that they are playing into the decarbonization, digital, and modernization infrastructure (i.e., "megatrends") that's been gaining momentum.

With that being said, we can see that the biggest divergence between MEGI and UTF and UTG was simply the total share price performance. That's created the precise opportunity of seeing MEGI fall to a deep discount. With newer funds, this can tend to take place even though they have termination dates and investors don't pay the launch fees anymore. In other words, MEGI is a CEF 2.0 type fund that is more beneficial and friendly to shareholders.

The fund's discount seems to continue to find a bottom near this 16 to 18% level, suggesting that now could be an appealing time to consider this fund.

YCharts

Perhaps more promising is that MEGI has been the outperformer through 2023 at this point. The outperformance here is only based on a short period of time, but it has been a fairly material amount in both the total NAV and share price metrics. Discount contraction going forward, even if UTG and UTF continue to stagnate at current levels, would see MEGI be a stronger performer.

YCharts

Distribution - Attractive And Reasonable

They've continued to pay out the same $0.1083 monthly distribution. Thanks to some appreciation since our last coverage, that also meant that the distribution yield cooled to 8.84% and, on an NAV basis, went down to an even more mild 7.38%.

In our prior update, I was worried about rising interest rate costs. I thought the coverage would come under pressure, but the distribution coverage has been quite strong with the latest report once again. To be fair, interest rate expenses continue to remain a concern, but the latest report reflects relatively strong coverage.

MEGI Semi-Annual Report (MainStay CBRE)

Net investment income coverage came in at 91.04% in their last semi-annual report. Interest rate expenses came to $6.096 million, up from the $2.199 million they reported in the last period. Despite being an annual report, the last period they reported was partial, too, from launch to their fiscal year end in May. Thus, we would double these figures, but we can really see how much expenses rose due to borrowings. In this period alone, it tripled.

At the same time, rates were still rising after this last semi-annual report. OBFR is currently at 4.82% . That means including the fund's spread on borrowings, it is costing them 5.57%. According to their last fact sheet, they had $341 million in leverage outstanding - down slightly from the $345.5 million previously - that would cost them nearly $19 million going forward on an annualized basis. That would be up from the ~$12 million reflected in the last report if we annualized the figure.

Therefore, should we expect to see another $61.582 million in NII ($30.791 annualized), subtracting out the additional $7 million in borrowing costs would see NII at around $54.582. Against the $1.2996 annualized distribution times, the shares outstanding of 52,047,534 would mean total distributions of $67.641 million. Unsurprisingly that's exactly the annualized rate of the distributions to common shareholders in this previous report.

Considering these figures would bring NII coverage for the distribution to 80.7%. However, as a primary equity-focused fund, this isn't bad at all. In fact, this is incredibly strong. UTF, which is probably more closely matched to MEGI than UTG, last showed an NII distribution coverage of 27.08% for some context.

MEGI's Portfolio

MEGI hasn't been overly active with changes in the portfolio now that they've been initially set up. They reported only a 12% turnover rate in each of their last reports. Of course, those were partial reports, so annualized, that would come out to 24%. As noted, the primary component of the fund is equity or common stock positions. However, they come with the flexibility to invest in some preferred holdings too, which are also characteristics of UTF.

MEGI Asset Breakdown (MainStay CBRE)

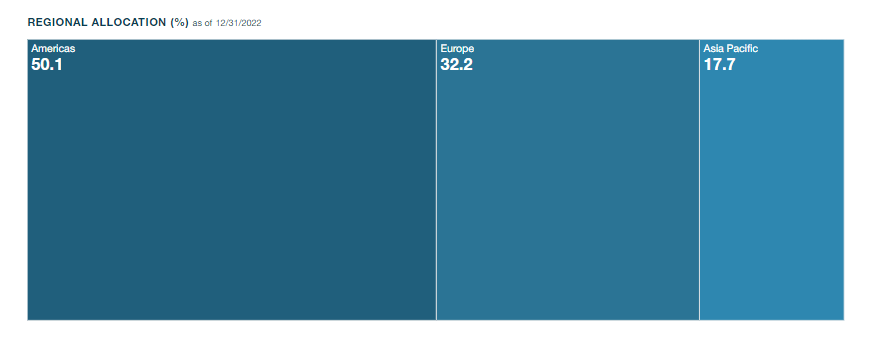

Additionally, they aren't dedicated to any specific geographic region, leaving them open to invest where they see fit across the globe. The composition of assets of the fund remained nearly unchanged from our prior update. Similarly, the geographic allocations also stayed rather stable, with only a slight decline in the Americas and a slight move higher in the Europe sleeve.

{kind=link}

The relatively limited changes are also reflected in the classifications of the megatrend themes. Decarbonization remains the largest contributor to the portfolio's weightings. Renewables within the decarbonization also remain the largest subtheme.

MEGI Portfolio Allocation (MainStay CBRE)

Despite having these themes, which would commonly be referred to as "ESG" or "green" energy plays, this fund also invests in plenty of fossil fuels as well. ESG and green energy are terms that have been politicized and often spark passionate debates. I'm agnostic in this debate. It seems pretty clear that the future will be a combination of both brown and green energy sources.

With that, I believe it highlights a positive of MEGI. The fund is investing in many of your traditional fossil fuel plays too, which will remain relevant for years, decades and possibly centuries to come. Positions such as ONEOK ( OKE ), The Williams Companies ( WMB ), and Enbridge ( ENB ) are all top ten positions in their portfolio. These midstream and infrastructure companies focus on moving good ol' fashioned energy commodities.

MEGI Top Holdings (MainStay CBRE)

I believe having the flexibility to invest more broadly can help the fund. Oil and gas are never going to go away; there seemingly will always be a demand. At the same time, they can take advantage of shifting to renewables, which are projected to be a larger share of the electricity generation pie.

{kind=link}

Even if we look at the more traditional energy plays, a shift is even taking place in names such as ENB and WMB , which are making shifts to add renewables to their portfolio of infrastructure assets. For MEGI, they categorize ENB and WMB as "asset modernization" plays. Presumably, they'd fall under the "energy transition" subtheme listed above.

Finally, along with the energy plays in the fund, we see plenty of utility investments. Utilities should help keep the portfolio relatively stable when energy is a more cyclical area of the market.

Conclusion

MEGI has the flexibility to invest in a diverse portfolio of infrastructure and utilities. This can allow the fund to invest where the managers see fit, including where they see fit, as they don't have a constraint on geographic allocations. Naturally, America being the largest economy in the world, will dominate the portfolio.

The fund's deep discount represents an interesting time to consider this fund. For a while now, the discount has stabilized in this region, which could suggest a limited downside from further discount deepening. Interest rates remain a headwind due to rising leverage costs, but MEGI also sports some relatively high distribution coverage from the dividends collected in its underlying portfolio.

One of the only reasons I don't own this fund currently is quite simply that I own plenty of CEFs already. Adding even more to my portfolio is something I'm trying to limit.

For further details see:

MEGI: Deep Discount Persists, Presenting An Opportunity